Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

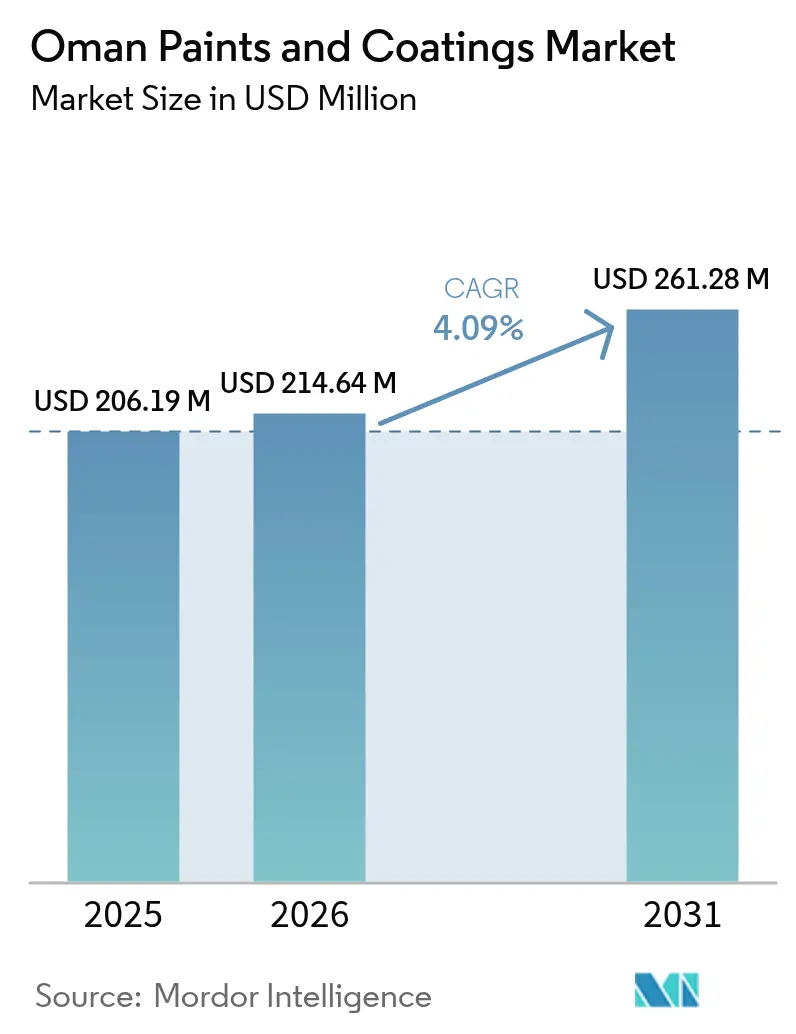

| Base Year Market Size (2025) | USD 206.19 Million |

| Market Size (2026) | USD 214.64 Million |

| Market Size (2031) | USD 261.28 Million |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Paints And Coatings Market Analysis by Mordor Intelligence

Oman Paints And Coatings Market size in 2026 is estimated at USD 214.64 million, growing from 2025 value of USD 206.19 million with 2031 projections showing USD 261.28 million, growing at 4.09% CAGR over 2026-2031. Robust capital spending on housing, transport corridors, industrial zones, and tourism complexes keeps the Oman paints and coatings market steadily growing. Residential programs led by the Ministry of Housing and Urban Planning, the expansion of special economic zones at Duqm and Sohar, and a rising pipeline of luxury resorts all translate into firm demand for decorative, protective, and specialty finishes. Tighter national VOC (Volatile Organic Compound) limits promote faster adoption of water-borne technologies, while the rising profile of green hydrogen and large-scale solar projects unlocks niche opportunities in high-performance protective systems. Competition remains intense as global majors defend their share with sustainability-aligned portfolios and local producers leverage cost advantages and proximity to public-sector buyers. Supply-chain vulnerability to imported specialty resins tempers the outlook, yet expanding domestic petrochemicals capacity offers a partial buffer.

Key Report Takeaways

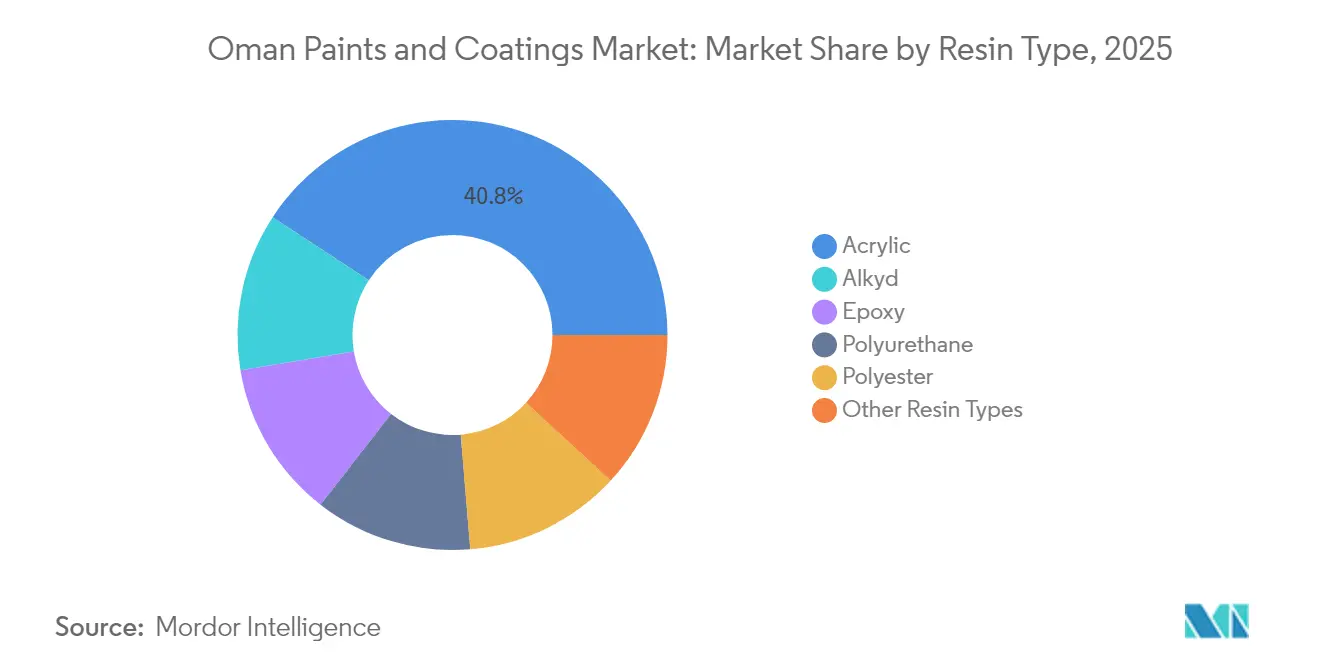

- By resin type, acrylic captured 40.77% of the Oman paints and coatings market share in 2025. Polyurethane is projected to expand at a 4.29% CAGR through 2031.

- By technology, water-borne products led with 61.92% revenue share in 2025. UV-cured systems are forecast to post the fastest 4.71% CAGR to 2031.

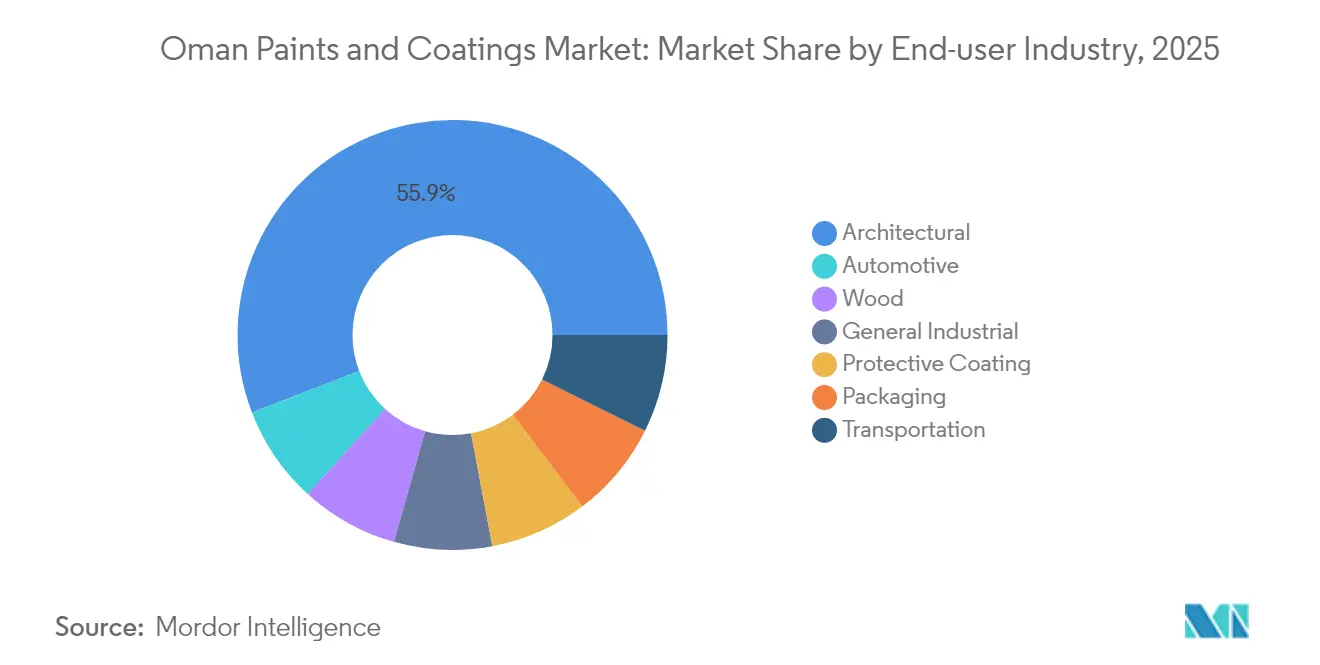

- By end-user industry, architectural applications accounted for 55.86% of the Oman paints and coatings market in 2025. Wood coatings are advancing at a 4.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Oman Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led Housing Projects Boosting Decorative Paints Demand | +1.2% | National, concentrated in Muscat, Al Batinah, Dhofar | Medium term (2-4 years) |

| Infrastructure Investments Under “Oman Vision 2040” | +1.5% | National, with focus on Duqm, Sohar, Salalah economic zones | Long term (≥ 4 years) |

| Rising need for Corrosion-resistant Coatings in Oil and Gas Assets | +0.8% | Concentrated in petroleum-producing regions, offshore facilities | Short term (≤ 2 years) |

| Tourism-driven Hotel Construction Fuelling Premium Coatings Uptake | +0.6% | Coastal areas, Muscat, Salalah, mountain tourism zones | Medium term (2-4 years) |

| New Low-VOC Regulations Accelerating Switch to Water-borne Systems | +0.9% | National, with stricter enforcement in industrial zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-led Housing Projects Boosting Decorative Paints Demand

Ongoing public housing and school construction is the largest single demand engine for the Oman paints and coatings market. Twelve new government-funded schools with 40 classrooms and completion deadlines extending to 2028 ensure multi-year procurement cycles for interior and exterior architectural finishes. Concurrently, 4,800 integrated residential units are under development, and heritage authorities require breathable mineral coatings on more than 100 fort and castle restoration sites[1]Ministry of Housing and Urban Planning, “Integrated Residential Projects Progress Report 2025,” mohup.gov.om. These specifications favor high-grade, water-borne acrylics that satisfy durability, color-fastness, and historical authenticity requirements, securing predictable volumes for compliant suppliers. Long-term horizons enhance production planning accuracy and inventory optimization.

Infrastructure Investments Under “Oman Vision 2040”

A USD 25 billion project pipeline covering highways, rail, ports, and metro systems underpins the long-term expansion of the Oman paints and coatings market. The 400 km Adam-Haima-Thumrait dual carriageway, the Sohar-Abu Dhabi rail link, and Muscat metro plans demand road-marking, bridge protection, and anti-corrosion products. The Duqm Special Economic Zone’s refinery, petrochemical, and port assets drive uptake of marine and chemical-resistant systems. Large-scale solar farms targeting a 30% renewable mix by 2030 require UV-stable structural coatings. The breadth of infrastructure assets sustains baseline consumption while creating specialist niches that reward technically advanced suppliers.

Rising Need for Corrosion-Resistant Coatings in Oil and Gas Assets

Mature upstream fields, high-salinity pipelines, and high-temperature separators accelerate corrosion, keeping protective volumes resilient. Block 61’s Khazzan and Ghazeer phases illustrate scale: over 500 km of coated pipe, extensive separators, heat exchangers, and storage tanks specified for epoxy and polyurethane systems rated above 80 °C. Plans for more than 1 million tpa of green hydrogen capacity introduce hydrogen-compatible linings. Global majors leverage proven offshore track records, while local applicators gain share through competitive labor and quick mobilization. The segment remains sensitive to oil-price swings but benefits from mandatory maintenance cycles that cannot be deferred indefinitely.

Tourism-Driven Hotel Construction Fuelling Premium Coatings Uptake

The USD 500 million Trump International Oman resort and a USD 2.4 billion mountain destination project headline an expanding luxury pipeline that stimulates premium decorative, wood, and protective systems. Salalah’s khareef season drew over 1 million visitors in 2024, prompting more resort permits that stipulate weather-proof, UV-resistant façades and marine-grade deck finishes. Elevated altitude developments at 2,400 m require coatings capable of large thermal‐cycle tolerance and enhanced UV durability. International hotel chains impose global brand standards, pushing demand toward high-performance, warranty-backed product lines where multinationals enjoy a competitive edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Crude-oil-based Raw-material Prices | -0.7% | Global supply chain impact, affecting all regions | Short term (≤ 2 years) |

| Slow Recovery of Domestic Automotive OEM Production | -0.4% | National, concentrated in industrial zones | Medium term (2-4 years) |

| Import Dependence for Specialty Resins Causing Supply Risk | -0.5% | National, affecting all manufacturers and distributors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Oil-Based Raw-Material Prices

Petroleum-derived inputs account for roughly 30% of formulation costs and move with Brent benchmarks; every USD 10 per-barrel fluctuation shifts average unit costs by 2-3%. Upstream entities reported higher gas expenses in early 2025, amplifying cost pass-through pressure. European anti-dumping duties on Asian epoxy suppliers further tightened global availability, prompting local manufacturers to negotiate alternate sources at premium levels. Price uncertainty encourages long-term supply contracts and indexed pricing, but these arrangements erode competitiveness in fixed-price government tenders.

Slow Recovery of Domestic Automotive OEM Production

Oman’s modest assembly base remains below pre-pandemic output, constraining original-equipment volumes for automotive topcoats, primers, and electro-deposition products. While aftermarket refinishing sustains baseline consumption, subdued original equipment manufacturer (OEM) demand keeps utilization rates at dedicated coating lines below break-even thresholds. Manufacturers redirect capacity toward industrial or wood-coating batches to maintain asset productivity, yet product-mix shifts dilute margins and limit innovation budgets earmarked for next-generation auto finishes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Leadership Anchored in Coastal Durability

Acrylic systems generated 40.77 % of the Oman Paints and Coatings market share in 2025, thanks to superior salt-spray resistance, color retention, and fast drying that satisfy coastal housing and public-works specifications. The Oman paints and coatings market continues to favor acrylics in both flat and glossy sheens for exterior façades, while interior spaces migrate toward low-odor, water-borne variants that ease on-site application. Alkyds remain in budget interior segments, yet regulatory VOC pressure accelerates substitution. Epoxies serve mid-film and tank-lining uses where solvent-free or high-solids formulations meet stringent chemical-resistance requirements in hydrocarbon processing plants.

Polyurethane registers the fastest 4.29% CAGR through 2031, buoyed by rising furniture manufacturing, parquet flooring, and long-life industrial topcoat demand. Polyesters carve out niches in powder-coated façades, handrails, and HVAC louvers that adorn Muscat’s skyline. Specialty silicone, polysiloxane, and fluoropolymer chemistries gain traction in marquee projects demanding 15-year color warranties. Capital investment in OQ’s polymer complex could feedstock locally produced intermediates, yet specialty resin production remains mostly imported, anchoring international supplier relationships in high-performance segments of the Oman paints and coatings market.

By Technology: Water-Borne Dominance Under Environmental Mandates

Water-borne systems held 61.92% of the Oman Paints and Coatings market size in 2025 as stricter VOC ceilings and growing consumer health awareness converged. National enforcement and architectural contractor preference for low-odor job sites convert previously solvent-rich segments into latex acrylics and self-crosslinking polyurethane dispersions. Solvent-borne alkyds and epoxies persist in niche roles where ambient-cure performance or deep-penetrating primers are indispensable, but manufacturers now deploy higher-solids versions to reduce emissions footprints.

Powder coatings benefit from a near-zero VOC status, expanded by local metal-fabrication demand for cladding, window frames, and railing systems. UV-cured formulations record the quickest 4.71% CAGR, driven by high-throughput wood lines serving furniture exporters and regional joinery workshops. Capital outlays for UV lamps and inert-atmosphere tunnels remain barriers for small job shops, yet large players offset upfront costs via productivity gains, shorter takt times, and reduced floor space. The technology mix underscores how environmental regulation reshapes competitive advantage across the Oman paints and coatings market.

By End-User Industry: Architectural Spending Sets the Pace

The architectural sector contributed 55.86% of 2025 revenue as public housing, educational facilities, and hospitality complexes dominated project pipelines. Government budget visibility to 2028 secures demand for steady base coats, putties, and finish coats. Mid-to-high-end decorative lines now integrate anti-microbial additives and solar-reflective pigments to meet emerging green-building codes and thermal-comfort targets.

Wood coatings post a leading 4.58% CAGR, propelled by furniture clusters in Sohar and Salalah that supply hotel fit-outs and residential refurbishments. Protective coatings remain indispensable for pipelines, storage tanks, and port structures, sustaining recurring demand cycles even during oil-price downturns. General industrial volumes track broader manufacturing activity, expanding with downstream metals processing and food-packaging facilities. Automotive consumption improves gradually via import vehicle refinishing centers rather than OEM lines, while transportation coatings await the Sohar-Abu Dhabi rail and fleet renewal programs to unlock future upside for the Oman paints and coatings market.

Geography Analysis

Muscat Governorate anchors consumption, underpinned by flagship hospitality investments such as the USD 500 million Trump International resort and a vibrant expatriate real-estate market that logged OMR 545.6 million in foreign property contracts during H1 2024. High-rise residential towers, premium retail malls, and office fit-outs ensure diversified coatings pull-through, while well-established distributor networks shorten delivery lead times. Large applicator companies headquartered in the capital command robust bargaining power, influencing product specification and driving early adoption of low-VOC and color-retention technologies in the Oman paints and coatings market.

Al Batinah North and South rank as the fastest-growing regions to 2031. Sohar’s deep-sea port, free-zone incentives, and the USD 300 million polymer plant bolster industrial coatings uptake for storage tanks, conveyor frames, and process equipment. Proximity to raw-material imports via port facilities lowers logistics costs and attracts further fabrication activity that consumes primers, mid-coats, and heat-resistant finishes. Concurrently, Al Batinah’s coastal resorts and mid-income housing estates lift decorative volumes, cementing the governorate’s status as a dual-track growth engine.

Dhofar Governorate leverages the khareef monsoon season to expand hotel capacity, resort villas and supporting infrastructure. High humidity and salt-laden breezes necessitate specialized anti-fouling and weather-resistant systems, differentiating supplier offerings in the Oman paints and coatings market. Construction at Salalah Free Zone and a methane-to-blue-ammonia complex supports protective demand, while plans for the Duqm-Salalah economic corridor promise improved logistics that could further integrate Dhofar into national distribution grids. Interior governorates, including Ad Dakhiliyah and Ash Sharqiyah, benefit from highway corridors like Adam-Haima-Thumrait and the scattered school-building program, yet thinner contractor networks and longer transit distances constrain volume density. Musandam’s strategic fuel-storage initiatives provide niche opportunities but remain limited by small population and challenging topography.

Competitive Landscape

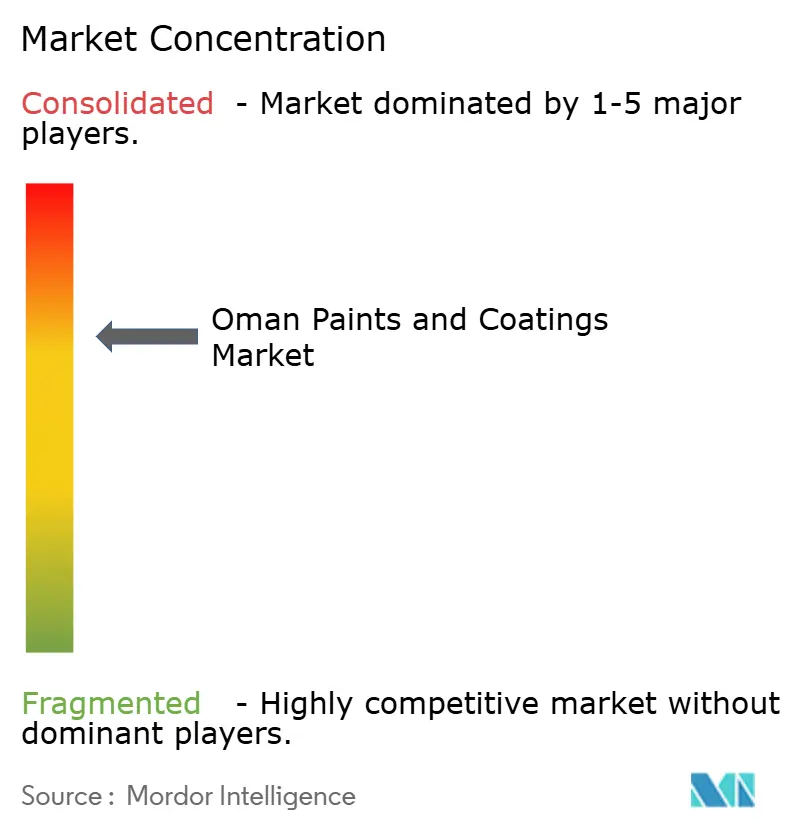

The Oman Paints and Coatings market is consolidated. AkzoNobel, Jotun, and BASF defend decorative leadership through premium branding, nationwide tinting systems, and compliance credentials that satisfy public-sector tender criteria. Local champions such as Gulf Paints and National Paints Factories exploit proximity to projects, quick color-match turnaround, and aggressive pricing to penetrate value-driven segments. Price competition remains fiercest in government housing and education projects, where tender rules emphasize the lowest cost compliant bid. Conversely, premium tourism developments and energy infrastructure favor lifecycle-cost arguments that reward high-performance products, balancing the opportunity portfolio across the Oman paints and coatings market.

Oman Paints And Coatings Industry Leaders

Jotun A/S

AkzoNobel N.V.

National Paints Factories

Hempel A/S

Oasis Paints

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: PPG Industries, Inc. secured its 50th order for electrostatic marine fouling control coatings. The project, set to take place at Asyad Drydock Company shipyard in Oman, involves the VLCC SIDR, a 336-meter oil tanker managed by Bahri Ship Management. The hull will be treated with PPG's NEXEON 810 antifouling coating.

- July 2023: Delta Coatings International, a Dubai-based waterproofing and protective coatings company, unveiled a three-year strategic growth blueprint targeting the Middle East. The plan emphasizes bolstering its presence in Oman and Egypt. Furthermore, Delta is set to introduce a new lineup of self-applied products and significantly enhance its turnkey project delivery services.

Oman Paints And Coatings Market Report Scope

Paints or coatings are various multiphase colloidal systems that are applied onto a surface in a continuous manner, fundamentally applying principles of colloids and interface surfaces. The application of paints or coatings is done in a bid to provide protection to the surface or serve decorative purposes. Oman's paints and coatings market is segmented by resin type, technology, and end-user industry. By resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types. By technology, the market is segmented into water-borne and solvent-borne. By end-user industry, the market is segmented into architectural, automotive, wood, industrial coatings, transportation, packaging, and other end-user industries. For each segment, market sizing and forecasts have been done on the basis of volume (kilotons) and value (USD million).

By Resin Type

| Acrylic |

| Alkyd |

| Epoxy |

| Polyurethane |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

| Powder Coating |

| UV-cured Coating |

By End-user Industry

| Architectural |

| Automotive |

| Wood |

| General Industrial |

| Protective Coating |

| Packaging |

| Transportation |

| By Resin Type | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyurethane | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| Powder Coating | |

| UV-cured Coating | |

| By End-user Industry | Architectural |

| Automotive | |

| Wood | |

| General Industrial | |

| Protective Coating | |

| Packaging | |

| Transportation |

Key Questions Answered in the Report

How fast is the Oman paints and coatings market expected to grow through 2031?

The market is projected to expand from USD 214.64 million in 2026 to USD 261.28 million by 2031, showing a 4.09% CAGR.

Which resin type leads national demand?

Acrylic resins command 40.77% share in 2025 thanks to superior durability in Oman's coastal climate.

What share do water-borne technologies hold?

Water-borne coatings accounted for 61.92% of 2025 revenue and continue to rise under stricter VOC limits.

Which end-user segment is growing the fastest?

Wood coatings lead with a 4.58% CAGR, driven by expanding furniture production for hospitality and housing projects.

Where is regional demand expanding most quickly?

Al Batinah governorates, anchored by Sohar’s industrial base, post the highest regional growth through 2031.

Page last updated on: