Kazakhstan-China Freight Forwarding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

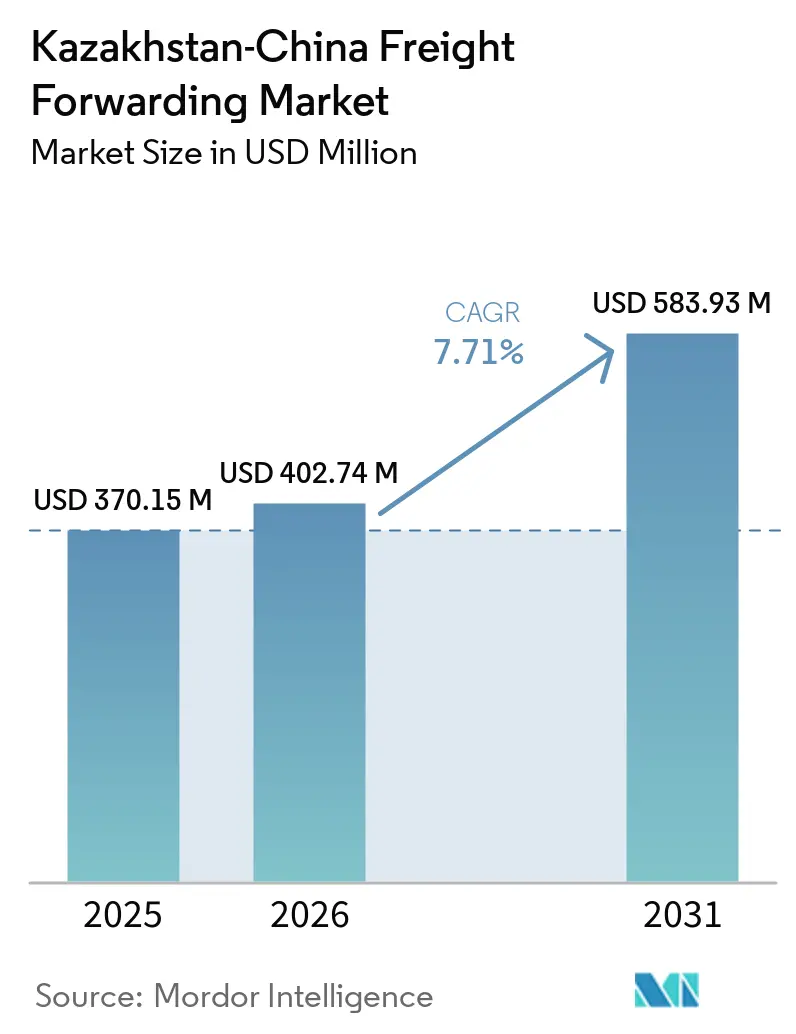

| Base Year Market Size (2025) | USD 370.15 Million |

| Market Size (2026) | USD 402.74 Million |

| Market Size (2031) | USD 583.93 Million |

| Growth Rate (2026 - 2031) | 7.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kazakhstan-China Freight Forwarding Market Analysis by Mordor Intelligence

The Kazakhstan-China freight forwarding market size is projected to expand from USD 370.15 million in 2025 and USD 402.74 million in 2026 to USD 583.93 million by 2031, registering a CAGR of 7.71% between 2026 to 2031.

A sustained pivot away from the northern Russian corridor, record bilateral trade, and Belt and Road Initiative (BRI) rail and road upgrades are enlarging freight volumes on every mode. Policy reforms such as unlimited electronic road permits and fast-track “green corridor” customs are shortening dwell times, while container hubs at Khorgos, Dostyk, Aktau, and Kuryk are lifting throughput ceilings. Digital customs integration with China and the rollout of temperature-controlled rail containers raise service quality for time-sensitive cargo and drive modal shift from expensive airfreight. Strategic investments by Chinese automakers, metals producers, and e-commerce giants have diversified Kazakhstan’s export base, improving back-haul utilization and stabilizing forwarders' margins.[1]Ministry of Transport of the Republic of Kazakhstan, “Trans-Caspian Route Volumes Grow as Digital Customs Cuts Transit Time,” gov.kz

Key Report Takeaways

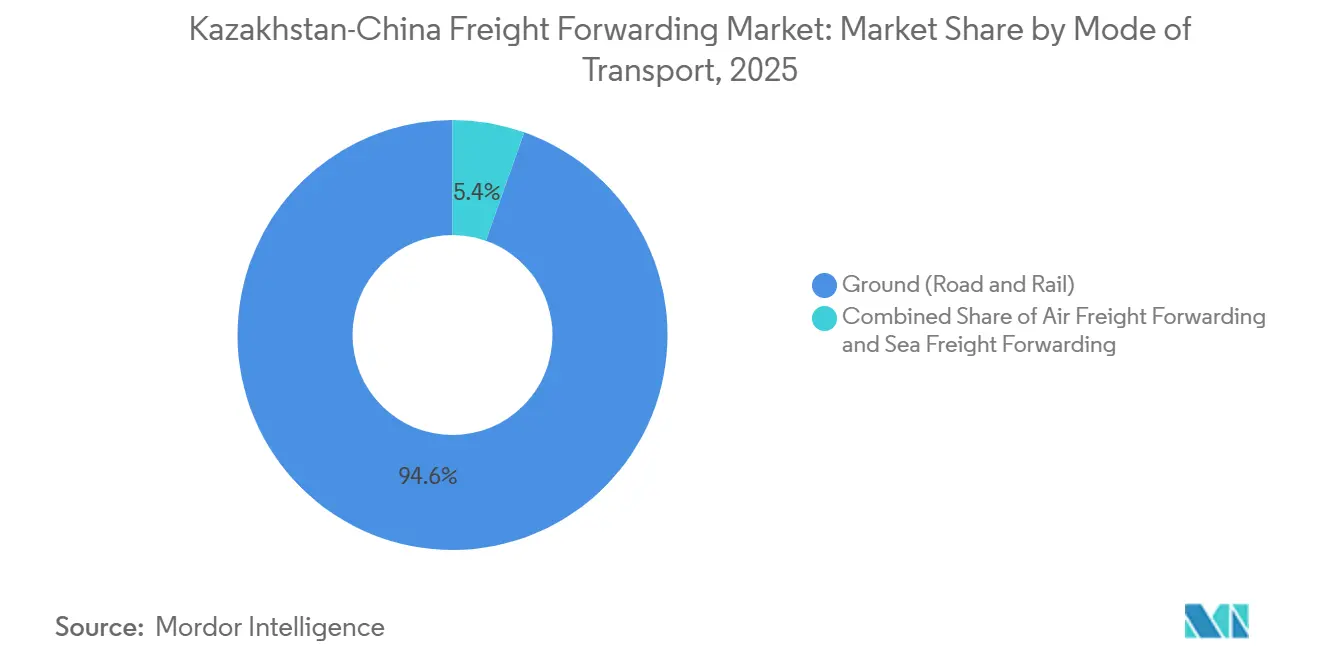

- By mode of transport, ground freight led with 94.59% for the Kazakhstan-China freight forwarding market share in 2025, while air freight is projected to expand at a 9.96% CAGR to 2031.

- By end-user industry, oil & gas and mining & quarrying accounted for 44.85% of the Kazakhstan-China freight forwarding market size in 2025. Distributive trade is advancing at a 9.21% CAGR through 2031.

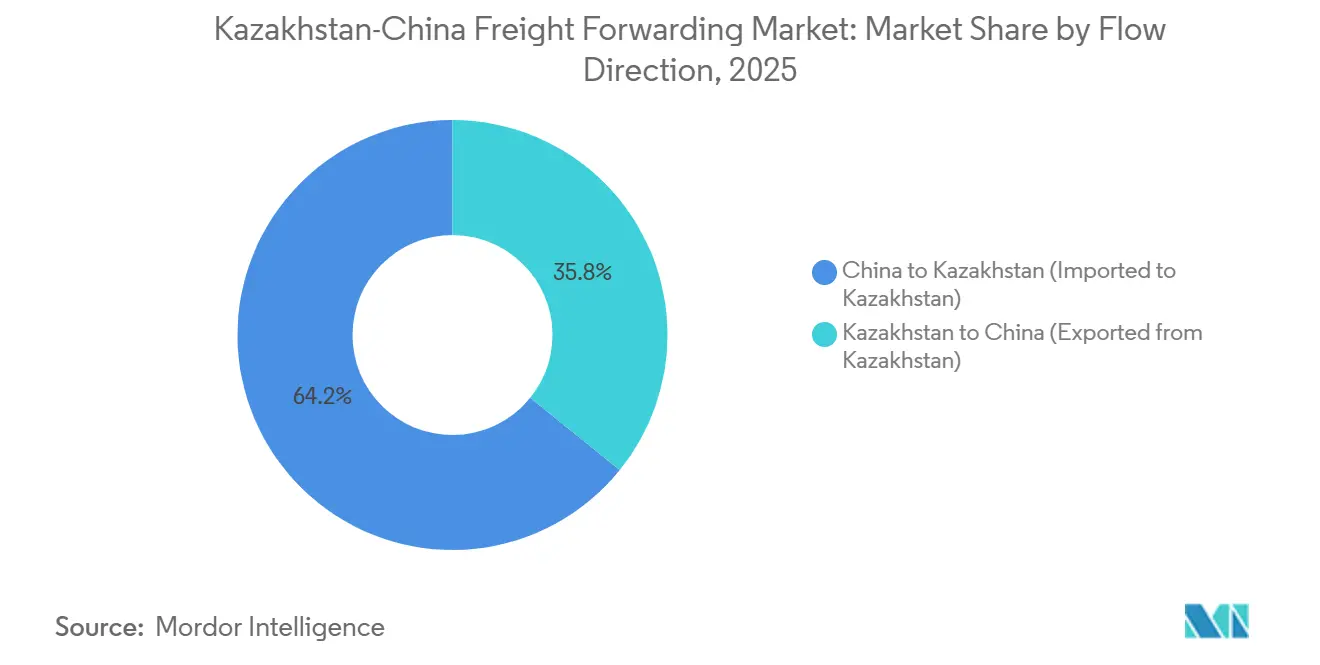

- By flow direction, China-to-Kazakhstan imports accounted for 64.25% of the Kazakhstan-China freight forwarding market share in 2025, whereas Kazakhstan-to-China exports are forecast to grow at an 8.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Kazakhstan-China Freight Forwarding Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BRI-led infrastructure investment and multi-corridor expansion generating structural freight forwarding demand | +2.1% | Kazakhstan-China corridor, Central Asia, Caspian region | Long term (≥ 4 years) |

| Record-breaking Kazakhstan-China bilateral trade volumes creating cross-sector freight forwarding demand | +1.8% | Entire Kazakhstan-China corridor | Medium term (2-4 years) |

| Geopolitical re-routing post Russia-Ukraine War: elevating Kazakhstan as an indispensable transit hub | +1.5% | Kazakhstan as the Eurasian land bridge | Medium term (2-4 years) |

| Digital customs modernization and smart logistics technology: reducing freight transit lead times | +1.0% | Khorgos, Dostyk, Bakhty, and Kolzhat crossings | Short term (≤ 2 years) |

| Diversified industrial end-user demand across mining, oil & gas, agriculture, manufacturing & automotive | +0.9% | Kazakhstan exports and Chinese imports | Long term (≥ 4 years) |

| Growth of temperature-controlled rail containers | +0.5% | Dostyk, Alashankou, Khorgos corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

BRI-Led Infrastructure Investment and Multi-Corridor Expansion Generating Structural Freight Forwarding Demand

In 2025, the Khorgos Gateway dry port significantly accelerated operational throughput by adding 10 new broad-gauge railway tracks and upgrading its intelligent infrastructure, slashing container transshipment times from 5 hours to 1 hour and driving annual handling volume past 372,000 TEUs. KTZ Express opened a 140,000 TEU container hub at Aktau in December 2025, adding cranes and yard space to shorten vessel turnaround times. Joint working groups now aim to reach 1,000 container trains on the Trans-Caspian route by 2027, doubling to 2,000 by 2029. Capacity upgrades trigger a self-reinforcing cycle: higher volume justifies fresh capital, locking the corridor into long-term growth. The strategy cements Kazakhstan as the principal land bridge between Chinese factories and European buyers.

Record-Breaking Kazakhstan-China Bilateral Trade Volumes Creating Cross-Sector Freight Forwarding Demand

Goods trade climbed to USD 48.7 billion in 2025, up 11% year on year. Chinese investment of USD 23 billion in the first half of 2025 alone financed large aluminum and copper smelters that import machinery and export metals. Agricultural freight is growing rapidly; in 2025, rail-bound grain exports to China surpassed 4.2 million tons, driven by a massive structural shift toward specialized, containerized feed shipments, which reached a record 3.1 million tons. Vehicle exports to China exceeded USD 160 million in the first half of 2025 as joint-venture assembly plants scaled output. Diversifying flows beyond hydrocarbons improves container back-haul utilization and shields forwarders from oil price swings.[2]Kazinform Agency, “Bilateral Trade Between Kazakhstan and China Hits USD 48.7 Billion in 2025,” inform.kz

Geopolitical Re-Routing Post Russia-Ukraine War: Elevating Kazakhstan as an Indispensable Transit Hub

Sanctions on Russia diverted shippers to the Middle Corridor, boosting transit container volumes in Kazakhstan by 15% to 36,000 TEU in 2025. End-to-end rail time from Xi’an to Europe compressed to 18 days, half the duration of traditional sea routes. Compliance checks increased, but electronic documentation and corridor diversification keep cargo moving. Despite episodic truck queues at the Russia border, forwarders view the shift as irreversible because alternate routes lack comparable capacity or investment momentum.

Digital Customs Modernization and Smart Logistics Technology: Reducing Freight Transit Lead Times

The Tez Customs platform has cut compliance clearance to 30 minutes at major gates. Integrated single-window links with China enable pre-arrival data exchange, reducing manual errors and shortening wagon switchover at broad-to-standard-gauge interfaces. Pilot sites with biometric driver checks reduced average crossing time from 8 hours to under 2 hours. Unlimited electronic permits introduced for Kazakh carriers from 2026 remove quota friction and lower wait costs. These reforms narrow the cost gap with maritime freight and encourage a modal shift toward rail for mid-value goods.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Physical infrastructure bottlenecks and rail gauge incompatibility at border crossings limiting throughput capacity | -1.2% | Dostyk-Alashankou, Khorgos-Altynkol | Medium term (2-4 years) |

| Declining Caspian Sea water levels constraining maritime freight capacity on the Trans-Caspian route | -0.8% | Aktau and Kuryk ports | Long term (≥ 4 years) |

| Heightened western sanctions compliance obligations and dual-use cargo scrutiny causing systemic freight delays | -0.6% | Kazakhstan-Russia border | Short term (≤ 2 years) |

| Fragmented multi-jurisdictional regulatory frameworks, non-harmonized tariffs, and multi-modal procedural complexity | -0.4% | Multicountry Middle Corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Physical Infrastructure Bottlenecks and Rail Gauge Incompatibility at Border Crossings Limiting Throughput Capacity

Standard-gauge Chinese wagons must transship to broad-gauge Kazakh wagons, adding 6-12 hours per train and saturating siding capacity during peak seasons. Although Khorgos expanded to 800,000 TEU a year, overflow already strains adjacent yards. Planned second-track projects will not deliver relief until after 2027, so forwarders must budget longer dwell times and higher demurrage in the medium term.

Declining Caspian Sea Water Levels Constraining Maritime Freight Capacity on the Trans-Caspian Route

With the Caspian Sea falling by -29.6 meters by 2025, severe draft restrictions have forced Aktau to limit vessel loading to just 80% of capacity to prevent grounding. While an emergency USD 84.5 million dredging program offers a stopgap, continuous seabed maintenance inflates port charges. Although recent channel deepening at the Kuryk port provides immediate relief, the complete capacity expansion under Kazakhstan's 2028 maritime plan remains years away, sustaining vessel bottlenecks across the Middle Corridor.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: Ground Dominance Meets Air Upswing

Ground services captured 94.59% of the Kazakhstan-China freight forwarding market share in 2025. Rail accounts for most tonnage, moving bulk copper, grain, and coal at low unit cost, while road accelerates time-critical shipments such as live plants and e-commerce returns. The TIR haul from Guangzhou to Almaty, completed in five days, shows the road’s speed advantage over the rail’s 15-day average on the same corridor. Multimodal offerings now integrate road legs with rail block trains and ferry links via the Caspian, enhancing schedule flexibility.

Air freight is the fastest-growing mode, forecast to post a 9.96% CAGR through 2031. Explosive, unprecedented year-over-year growth in cross-border parcel volumes is the primary catalyst driving this surge. Government plans for full-scale cargo hubs and removal of Kazakhstan’s 25-year aircraft age limit encourage operators like YTO Express and QazPost to invest in 60,000 m² of new warehousing. With domestic jet-fuel supply expansion and tariff revisions underway, the air component is set to transition from a niche to a mainstream option for high-value electronics and fashion.

By End-User Industry: Extractives Lead While E-Commerce Rises

Oil and gas, mining, and quarrying held 44.85% of the Kazakhstan-China freight forwarding market size in 2025. Continuous flows of crude oil through the Atasu-Alashankou pipeline and rail copper concentrates ensure baseline rail volumes. Substantial and sustained Chinese capital injections into smelting and refining infrastructure continue to underpin inbound traffic for heavy machinery and outbound flows of finished metals.

Distributive trade is the fastest-expanding segment, advancing at a 9.21% CAGR to 2031. Cross-border platforms on Temu and Alibaba enable Kazakh consumers to source low-priced household items, driving parcel inflows and last-mile demand. A 60,000 m² warehouse planned for 2026 will relieve Kazakhstan’s 1.4 million m² stock shortage and improve pick-and-pack efficiency. Agriculture also accelerates: driven by robust 2025 demand, eastbound grain shipments reached record volumes, utilizing specialized reefer wagons that maintain strict temperature integrity for premium beef and dairy exports.[3]Ministry of Foreign Affairs of the Republic of Kazakhstan, “Trade and Investment Cooperation Between Kazakhstan and China Reaches New Heights,” gov.kz

By Flow Direction: Import Heavy but Export Growth Accelerates

China-to-Kazakhstan imports generated 64.25% of 2025 revenue. Consumer electronics, automotive parts, and construction inputs dominate inbound loads that fill containers and wagons on the westbound leg to Almaty and Nur-Sultan. On the return leg, exports of crude, metals, grain, and assembled vehicles are climbing at an 8.25% CAGR, narrowing the imbalance. Rail operators now market empty-container discounts for agricultural shippers to improve back-haul utilization, while temperature-controlled services open new lanes for meat and dairy products.

Digital documentation has begun to shrink dwell times at the Dostyk and Khorgos gateways, cutting compliant truck clearance to about 30 minutes and freeing forwarders to reposition assets for the export leg. Short-haul TIR services now redeploy empty boxes from Almaty to the northern grain belts, enabling weekly wheat and rapeseed block trains bound for China to benefit from discounted back-haul tariffs. Express introduced temperature-controlled reefers in 2025 that hold –20 °C, protecting chilled beef on the two-day rail run to Urumqi and lifting average revenue per TEU. Rising SUV output in Kostanay and Almaty has prompted wagon retrofits with wheel chocks, sending finished vehicles east and driving a marked, year-over-year acceleration in wagon turnaround times. These operational tweaks are projected to lift export volumes without elongating cycle times on the larger import leg.

Geography Analysis

Khorgos Gateway and Dostyk-Alashankou remain the primary rail portals where Chinese standard-gauge lines interface with Kazakhstan’s broad-gauge network. Khorgos increased its annual capacity to 800,000 TEU after new tracks and repairs reduced wagon turnaround. Dostyk, although congested, benefits from a second-track project on the Moiynty segment that will ease throughput from 2027 onward. The Lianyungang logistics base, China’s first BRI project, now channels more than 20,000 TEU every quarter toward Central Asia, with six rail routes spanning the Trans-Caspian, Kyrgyzstan-Uzbekistan, and Russia corridors.

On the maritime leg, Aktau and Kuryk connect railheads to Ro-Ro and container vessels crossing to Baku or Turkmenbashi. Falling water levels reduced Aktau’s loading drafts, so dredging and new gantry cranes form interim fixes while a deeper transloader at Kuryk enters construction. Pioneering Trans-Caspian TIR operations now leverage Kuryk as a primary staging yard for westbound sailings, unlocking a highly competitive five-day China-to-Turkiye transit window for time-sensitive freight.

Rapid road expansion complements rail. The TIR network now covers more than 80 China-Kazakhstan-Eurasia routes. A green-corridor customs regime launched in December 2025 removes random inspections for compliant trucks and handles 30-35% annual volume growth. Abolishing quantitative road permits in 2026 further reduces administrative friction and positions Kazakhstan as Central Asia’s primary trucking hub.[4]Ministry of Transport of the Republic of Kazakhstan, “Modernization of Border Crossings and Caspian Ports Bolsters Transit Capacity,” gov.kz

Competitive Landscape

State-backed rail giants KTZ Express, China Railway Container Transport Corporation, and UTLC ERA handle the bulk of container traffic by controlling wagons, cranes, and customs interfaces. UTLC ERA alone recently moved over 745,000 TEU across its east-west services, an 11% year-over-year increase that showcases scale economics. Strategic alliances, such as the recent memorandum between UTLC ERA and CRCT, continue to expand block-train frequencies and harmonize rates.

Global integrators add multimodal depth. DSV’s USD 15 billion takeover of DB Schenker in April 2025 created the world’s largest forwarder and strengthened its rail-air-sea mesh across Almaty, Xi’an, and Duisburg. CMA CGM set up a Kazakhstan office in June 2025 to layer sea capacity with rail shuttles and controlled-temperature trucking. Kuehne+Nagel and FedEx Logistics focus on value-added warehousing and e-commerce fulfillment, where digitized inventory tracking attracts fashion and electronics brands.

Technology is now the sharp edge of competition. UTLC ERA rolled out a digital waybill platform that connects China, Kazakhstan, and the European Union, providing shippers with real-time visibility and reducing document handling costs. KTZ’s “4:3” and “3:2” train-formation model synchronizes rail departures with vessel berths, trimming idle time at Aktau and Kuryk. Smaller disruptors such as Sinotrans and Yuxinou exploit the faster TIR corridors to win time-sensitive loads, proving that service innovation, not just asset ownership, will dictate market share gains.

Kazakhstan-China Freight Forwarding Industry Leaders

CMA CGM Group (including CEVA Logistics)

Sinotrans

China Logistics Group Co., Ltd.

COSCO SHIPPING Holdings Co., Ltd.

DHL Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: KTZ dispatched 125 container trains on the Trans-Caspian route in Q1 2026, up 34.4% year on year, using new “4:3” and “3:2” formation models.

- January 2026: Guoyou Materials Group committed USD 1.1 billion to build a transloading complex at Kuryk, scheduled to be operational by 2028.

- December 2025: KTZ Express opened a 140,000 TEU container hub at Aktau with Lianyungang Port Group, which will be fully online by Mar 2026.

- December 2025: Kazakhstan launched a nationwide green-corridor system to accelerate Chinese transit trucks and trim inspection queues.

Kazakhstan-China Freight Forwarding Market Report Scope

| Air Freight Forwarding |

| Sea Freight Forwarding |

| Ground (Road and Rail) Freight Forwarding |

| Manufacturing and Automotive |

| Oil and Gas, Mining and Quarrying |

| Agriculture, Fishing and Forestry |

| Construction |

| Distributive Trade (Wholesale/Retail, FMCG) |

| Other End Users (Telecom, Pharmaceutical, etc.) |

| Kazakhstan to China (Exported from Kazakhstan) |

| China to Kazakhstan (Imported to Kazakhstan) |

| By Mode of Transport | Air Freight Forwarding |

| Sea Freight Forwarding | |

| Ground (Road and Rail) Freight Forwarding | |

| By End-User Industry | Manufacturing and Automotive |

| Oil and Gas, Mining and Quarrying | |

| Agriculture, Fishing and Forestry | |

| Construction | |

| Distributive Trade (Wholesale/Retail, FMCG) | |

| Other End Users (Telecom, Pharmaceutical, etc.) | |

| By Flow Direction | Kazakhstan to China (Exported from Kazakhstan) |

| China to Kazakhstan (Imported to Kazakhstan) |

Key Questions Answered in the Report

What is the current value of the Kazakhstan-China freight forwarding market?

The Kazakhstan-China freight forwarding market size reached USD 370.15 million in 2025 and is on track for USD 402.74 million in 2026.

How fast is the market expected to grow through 2031?

The market is projected to expand at a 7.71% CAGR between 2026 and 2031, reaching USD 583.93 million.

Which transport mode holds the largest share?

Ground freight, which combines rail and road, commanded 94.59% of market revenue in 2025.

Which end-user sector is expanding the quickest?

Distributive Trade, driven by e-commerce, is forecast to grow at a 9.21% CAGR through 2031

How significant is the trade imbalance between imports and exports?

Imports from China captured 64.25% of 2025 revenue, but exports to China are rising faster at an 8.25% CAGR, narrowing the gap

What infrastructure projects will shape capacity in the next five years?

Key projects include the second track on the Dostyk-Moiynty rail segment, the Kuryk transloading complex, and expanded dry-port facilities at Khorgos and Aktau.

Page last updated on: