Toluene Diisocyanate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

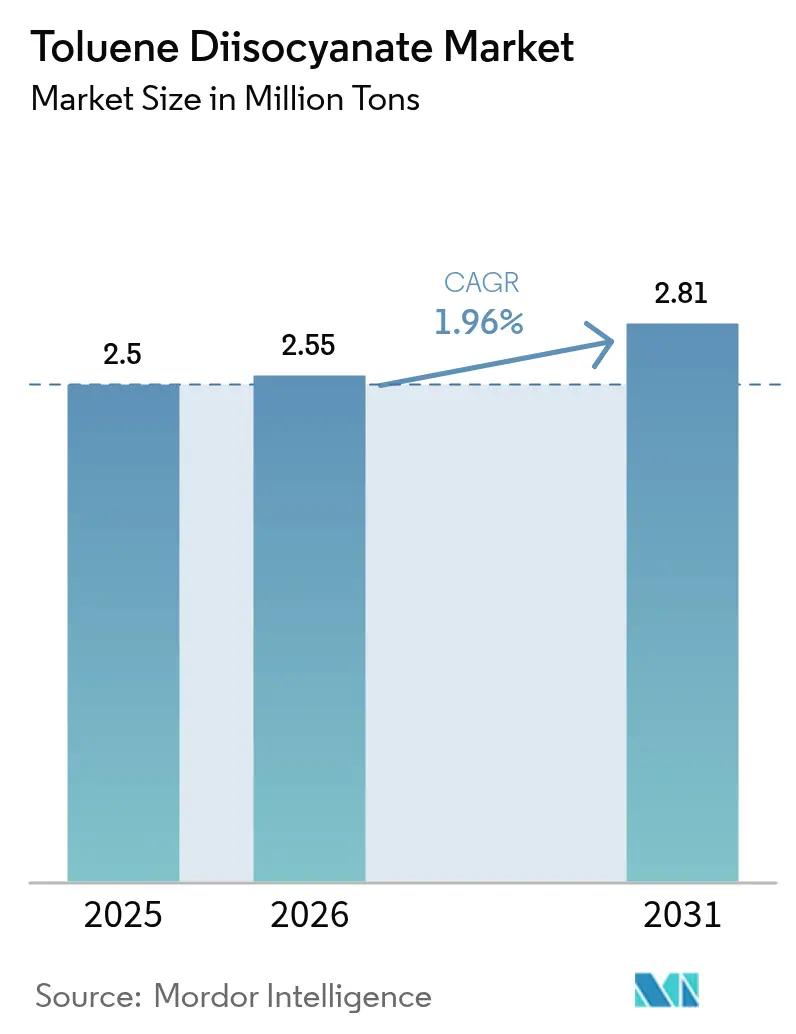

| Market Volume (2026) | 2.55 Million tons |

| Market Volume (2031) | 2.81 Million tons |

| Growth Rate (2026 - 2031) | 1.96% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Toluene Diisocyanate Market Analysis by Mordor Intelligence

The Toluene Diisocyanate Market size was valued at 2.5 Million tons in 2025 and estimated to grow from 2.55 Million tons in 2026 to reach 2.81 Million tons by 2031, at a CAGR of 1.96% during the forecast period (2026-2031). Current growth reflects a sector moving from rapid expansion toward steady maturity, shaped by stricter worker-safety rules, a shift toward phosgene-free routes, and sustained capital spending in Asia-Pacific’s integrated petrochemical hubs. Producers are emphasizing low-viscosity, high-purity grades for flexible foams, while downstream users seek lighter, more energy-efficient materials for furniture, transportation, and construction applications. Regional price spikes in 2024–2025—such as Wanhua Chemical’s USD 200/ton lift in ASEAN and BASF’s USD 300/ton rise in South Asia—underscore persistent feedstock and logistics pressures. Investments like SABIC’s USD 6.4 billion ethylene complex in Fujian illustrate long-term confidence in polyurethane demand. Phosgene-free pilot plants, inspired by UC San Diego’s bio-based aromatic diisocyanate breakthrough, signal the next technology frontier.

Key Report Takeaways

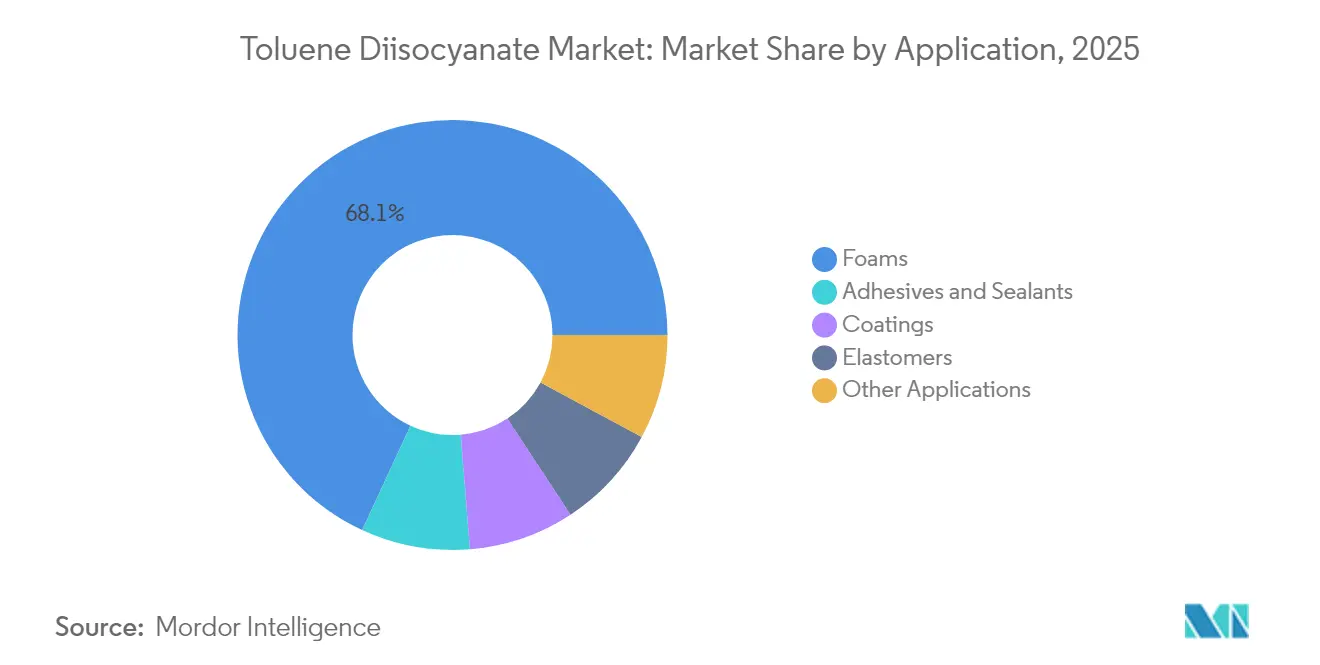

- By application, foams held 68.10% of the Toluene diisocyanates market share in 2025 while adhesives and sealants are projected to advance at a 2.27% CAGR between 2026 and 2031.

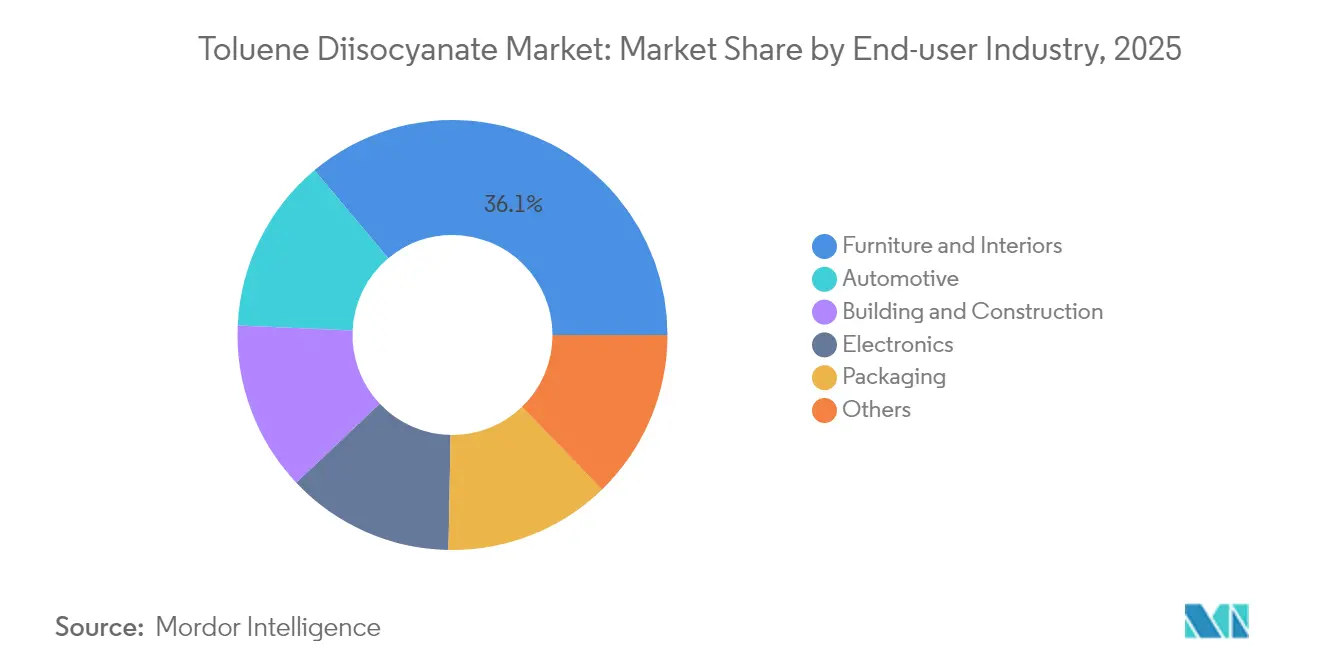

- By end-user industry, furniture and interiors commanded 36.10% of the Toluene diisocyanates market size in 2025; automotive leads growth with a 2.48% CAGR through 2031.

- By geography, Asia-Pacific captured 47.62% volume share in 2025 and Middle East and Africa is set to post the fastest 2.18% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Toluene Diisocyanate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flexible PU-Foam Demand in Furniture And Bedding | +0.6% | Global, strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Automotive Seat and Interior Lightweighting | +0.4% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Building-Insulation Codes (Rigid/Flexible Foams) | +0.3% | Europe and North America primarily | Long term (≥ 4 years) |

| EV Battery Thermal-Management Foams | +0.2% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Phosgene-Free TDI Scale-Up | +0.1% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Flexible PU-Foam Demand in Furniture and Bedding

Household and commercial furniture makers consume large volumes of TDI because flexible polyurethane delivers soft-touch cushioning, high rebound, and long service life. U.S. furniture and bedding sales topped USD 106 billion in 2024, sustaining foam off-take that exceeded 1.5 billion lb annually[1]American Chemistry Council, “Polyurethanes and Flexible Foams Statistics 2024,” americanchemistry.com . Memory-foam mattresses that blend TDI and MDI enhance pressure relief and command premium retail pricing, while thinner office-chair cushions reduce raw-material use without sacrificing comfort. In Asia-Pacific, urban housing growth, rising disposable incomes, and e-commerce furniture channels spur steady TDI uptake. China’s GB 18584-2024 furniture standard, effective July 2025, limits hazardous substances including toluene, prompting local converters to adopt cleaner TDI grades. Collaborative R&D among diisocyanate, polyol, and additive suppliers now focuses on smaller-cell, lower-density foams that support lifetime warranties.

Automotive Seat and Interior Lightweighting

Vehicle makers rely on TDI-based foams for seat cushions, headliners, and acoustical pads because the material cuts weight and improves passenger comfort. Light-duty electrified models intensify weight-reduction targets, lifting TDI demand at a 2.54% CAGR to 2030. Optimal 70:30 TDI:MDI blends raise tensile strength and transparency, delivering consistent feel in hot-and-cold cycles. Automakers also apply TDI in two-component polyurethane coatings that withstand abrasion and chemicals. However, higher MDI ratios shorten pot life, so finishing shops fine-tune catalyst packages to keep processing windows open. Regional sourcing strategies limit supply risk: North American assemblers lean on BASF’s expanding Louisiana capacity, while Chinese OEMs source from Wanhua and Covestro clusters.

Building-Insulation Codes (Rigid/Flexible Foams)

Tighter energy-efficiency directives in Europe and North America boost rigid-foam applications that rely partially on TDI for skin layers or composite panels. Covestro’s Baytherm Microcell technology shrinks cell size 40%, improving thermal performance 10% and lowering cold-chain losses in refrigerators. Green-building programs reward low-VOC, low-acidity foams for spray-applied insulation. Renovation subsidies in Germany and the United States accelerate retrofit activity, keeping panel and spray-foam plants running at high utilization. Producers are testing bio-based surfactants and flame retardants to keep pace with evolving safety and environmental codes.

EV Battery Thermal-Management Foams

High-energy battery packs generate localized heat that degrades performance and safety, creating white-space demand for thermally conductive yet electrically insulating foams. Laboratory work shows composite silica-gel plates can cut maximum cell temperature 12.9 °C in fast-discharge cycles. Polyurethane researchers are experimenting with graphite- and boron-nitride-filled TDI foams that promise lower density and easy die-cutting compared with silicone sheets. Asia-Pacific leads prototyping, with Korean tier-one suppliers targeting serial production by 2027. Automotive OEMs seek materials that pass nail-penetration, crush, and flammability tests under the UN GTR 20 regulation without adding process complexity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicity And Worker-Safety Regulations | -0.4% | Global, strictest in Europe and North America | Short term (≤ 2 years) |

| Toluene/Crude-Oil Price Volatility | -0.3% | Global, most severe in import-dependent regions | Short term (≤ 2 years) |

| EU Ecolabel Limits for TDI In Mattresses | -0.1% | Europe primarily, potential spillover to other developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Toxicity And Worker-Safety Regulations

TDI is a potent respiratory sensitizer classified as Group 2B by IARC, prompting regulators to enforce low exposure thresholds. OSHA sets an 8-hour TWA of 0.02 ppm, while ACGIH recommends 0.001 ppm TWA and 0.005 ppm STEL. Sensitized workers can react at 1–5 ppb, which pushes converters to improve enclosure, ventilation, and personal protective equipment. EPA’s Toxic Substances Control Act requires significant-new-use notifications for certain TDI-bearing polymers, adding administrative cost. In the United Kingdom, the Health Security Agency advises complete avoidance of unreacted TDI for sensitized individuals, forcing companies to adopt closed-mix systems and rigorous leak detection.

Toluene/Crude-Oil Price Volatility

TDI economics hinge on toluene and phosgene costs, both linked to oil and chlorine markets. China’s TDI spot price swung from CNY 17 200/ton in early 2024 to CNY 12 700/ton later that year, a 26% peak-to-trough range. Subsequent supplier hikes of USD 200–300/ton in January 2025 aimed to offset higher freight, energy, and chlorine costs. Import-dependent regions such as South Asia face amplified swings due to freight surcharges and currency depreciation. Since only a handful of global producers operate large-scale units, any unplanned outage can tighten supply and spark sharp price shifts that ripple through polyurethane converters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Foams Maintain Dominance Despite Diversification

Foams represented 68.10% of the Toluene diisocyanates market share in 2025, confirming the segment’s long-standing position as the principal consumer of difunctional aromatic isocyanates. Within foams, flexible grades command the majority, backed by robust furniture and bedding demand in Asia-Pacific and North America. The Toluene diisocyanates market size for foams is projected to rise in line with downstream capacity additions in China and Southeast Asia. Memory-foam innovations, including viscoelastic and breathable outdoor variants, build on TDI’s low viscosity and fast cure, offering lighter mattress cores without compromising rebound or durability.

Growth prospects outside foams continue to improve. Adhesives and sealants account for a modest volume today but are forecast at a 2.27% CAGR through 2031 thanks to stringent bonding requirements in modular construction and electric-vehicle assembly. In coatings, TDI affords high cross-link density for glossy, chemical-resistant finishes on automotive and wood substrates. Elastomers such as rollers and anti-vibration pads round out the portfolio, with niche grades featuring low acidity and narrow isomer ratios for superior mechanical performance.

By End-user Industry: Automotive Growth Outpaces Traditional Furniture Demand

Furniture and interiors remained the largest end-user industry, capturing 36.10% of the Toluene diisocyanates market size in 2025. Demand correlates with household formation, e-commerce logistics, and hospitality refurbishment cycles. Converters are moving toward water-borne adhesives and reduced-VOC foams to comply with incoming standards in China and the European Union.

Automotive industry, while smaller today, lead growth at a 2.48% CAGR as lightweighting and electrification intensify material-performance requirements. Seats, head restraints, and acoustic panels specify TDI-rich foams for consistent support and crash-energy absorption. Battery-pack seals and gap fillers open new volume streams, particularly in Asia-Pacific where electric-vehicle output accelerates. Building and construction follows, propelled by national building-insulation codes that favor rigid and spray-foam systems with high R-values. Electronics, packaging, and medical devices collectively add diversity, absorbing specialty foam grades for cushioning, vibration control, and wound-care dressings.

Geography Analysis

Asia-Pacific’s 47.62% share underscores its integrated supply chains and cost-advantaged feedstock slate. China hosts multiple TDI lines, including Covestro’s Shanghai facility expanding from 310 000 tpa to 370 000 tpa by 2025 and Fujian Wanhua’s 360 000 tpa project that cleared environmental review. The Toluene diisocyanates market size in the region benefits from export-oriented strategies, with average 2024 FOB prices of USD 1 700–1 800/ton supporting shipments across Southeast Asia. India’s rising disposable income and furniture output add incremental demand, while Japan and South Korea emphasize high-purity grades for electronics and specialty elastomers.

North America shows stable consumption underpinned by furniture and automotive sectors. BASF’s Geismar expansion will push regional MDI capacity to 600 000 tpa by 2026, indirectly bolstering aromatic diisocyanate value chains. TDI imports enter primarily through Gulf Coast ports, balancing domestic supply fluctuations. Canadian cold-storage retrofits and Mexican vehicle-assembly growth keep converters operating near capacity.

Europe confronts elevated energy costs and stringent decarbonization targets that pressure margins, yet the region retains technological leadership in low-monomer-residual grades. Covestro’s chlorine-plant upgrade in Tarragona deploys oxygen-depolarized-cathode technology that trims power needs 25% and secures feedstock for local diisocyanate units. Regulatory initiatives such as EU Ecolabel criteria for mattresses could further limit TDI content, spurring adoption of lower-emission systems.

Middle East and Africa posts the fastest 2.18% CAGR on the back of GCC investments like the Sadara complex, which positions the region for downstream polyurethane diversification. South America remains a smaller but steady outlet, with Brazil’s construction recovery and Argentina’s auto-parts output supporting gradual volume gains.

Competitive Landscape

The TDI market exhibits high concentration among five major producers thanks to proprietary phosgenation technology, large-scale reactors, and integrated chlorine supply. BASF deploys a multi-hub strategy, investing EUR 10 billion in China’s Zhanjiang Verbund to secure aromatics and chlorine streams[2]BASF, “Zhanjiang Verbund Investment Details,” basf.com . Wanhua leverages domestic logistics advantages to align capacity with China’s upholstery and footwear clusters. Covestro differentiates through high-purity TDI brands for low-emission foams, while Dow focuses on tailored blends such as VORANATE T 80 for flexible slabstock. GNFC and Hanwha contribute regional supply, ensuring competitive tension in price-sensitive markets.

Strategic maneuvers center on capacity debottlenecking, product-quality upgrades, and customer-centric technical service. Coordinated 2025 price increases highlight oligopolistic behavior that protects margins during feedstock volatility. Producers collaborate with seating and mattress makers to co-develop low-VOC, fast-cure systems that comply with upcoming indoor-air-quality rules.

Innovation pipelines target phosgene-free pathways, circular-carbon raw materials, and specialty foam grades for EV thermal management. UC San Diego’s bio-based aromatic diisocyanate pilot has piqued industry interest, although commercialization will require multi-ton manufacturing proof and regulatory clearances. Companies are also testing real-time VOC sensors and advanced scrubbers to lower workplace exposure, aiming to pre-empt stricter occupational-health legislation.

Toluene Diisocyanate Industry Leaders

BASF SE

Covestro AG

Wanhua

Dow

Mitsui Chemicals, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Wanhua started a new 360,000-tonne-per-year Toluene Diisocyanate (TDI) Phase II plant at the Fujian Industrial Park, achieving qualified product output. This new production line increases Wanhua's total TDI capacity from 1.11 million tonnes to 1.44 million tonnes annually.

- March 2025: Covestro completed and commissioned the modernization of its Toluene Diisocyanate (TDI) plant in Dormagen, implementing new energy efficiency targets for production operations. The modernization improved the plant's sustainability performance and competitive capabilities, achieving an annual CO2 reduction of 22,000 tons.

Global Toluene Diisocyanate Market Report Scope

Toluene Diisocyanate is an organic compound that is produced in a pure state. However, it is often marketed as 80/20 and 65/35 mixtures of the 2,4 and 2,6 isomers. They are majorly used to make polyurethane products, such as rigid and flexible foams, coatings, adhesives, sealants, and elastomers. The toluene diisocyanate market is segmented by application, end-user industry, and geography. The market is segmented by application into foam, coatings, adhesives and sealants, elastomers, and other applications. The market is segmented into furniture and interiors, building and construction, electronics, automotive, packaging, and other end-user industries by end-user industry. The report also covers the market size and forecasts for the toluene diisocyanate market in 15 countries across major regions. Market sizing and forecasts are done for each segment based on volume (kilotons).

| Foams |

| Coatings |

| Adhesives and Sealants |

| Elastomers |

| Other Applications |

| Furniture and Interiors |

| Building and Construction |

| Automotive |

| Electronics |

| Packaging |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Foams | |

| Coatings | ||

| Adhesives and Sealants | ||

| Elastomers | ||

| Other Applications | ||

| By End-user Industry | Furniture and Interiors | |

| Building and Construction | ||

| Automotive | ||

| Electronics | ||

| Packaging | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected global demand for TDI in 2031?

Global consumption is forecast to reach 2.81 million tons by 2031.

Which region drives the highest volume for TDI?

Asia-Pacific holds the lead with 47.62% of global volume in 2025, supported by China’s integrated petrochemical base.

Which end-use segment is growing fastest?

Automotive applications are slated to expand at a 2.48% CAGR between 2026 and 2031 on the back of lightweighting and EV adoption.

How do regulatory limits affect TDI producers?

Strict exposure limits (OSHA 0.02 ppm TWA) and EU ecolabel criteria compel manufacturers to invest in containment, low-emission grades, and phosgene-free R&D.

Page last updated on: