Market Overview

| Study Period | 2021 - 2031 |

|---|---|

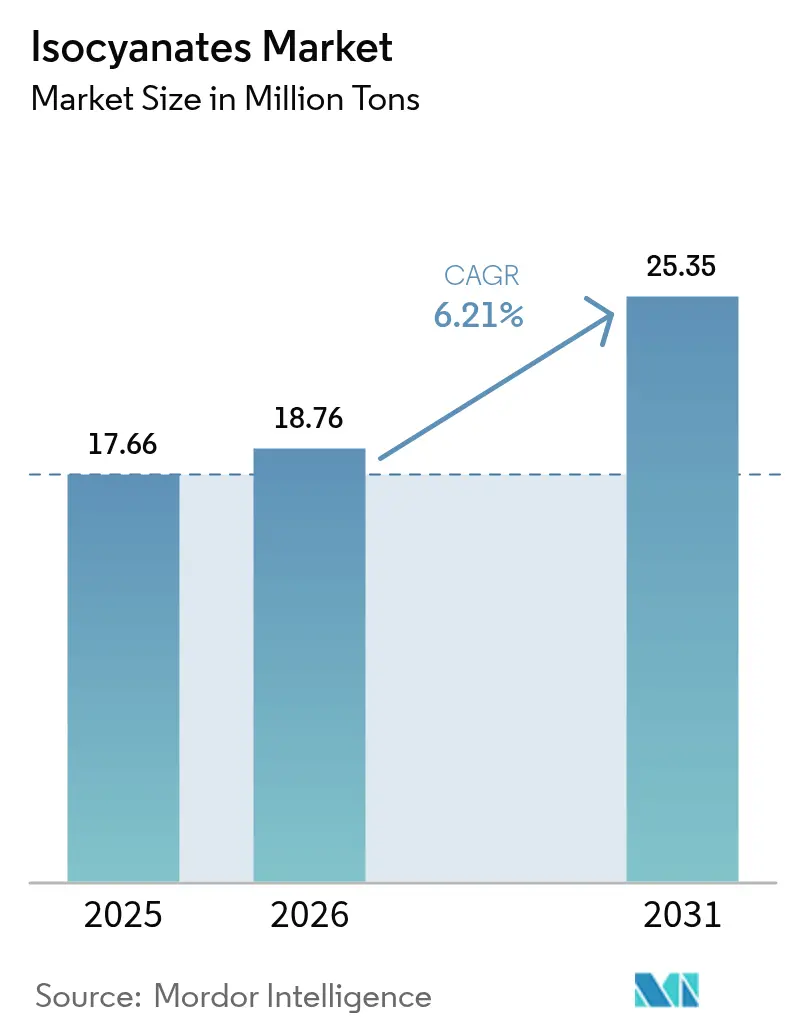

| Market Volume (2026) | 18.76 Million tons |

| Market Volume (2031) | 25.35 Million tons |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

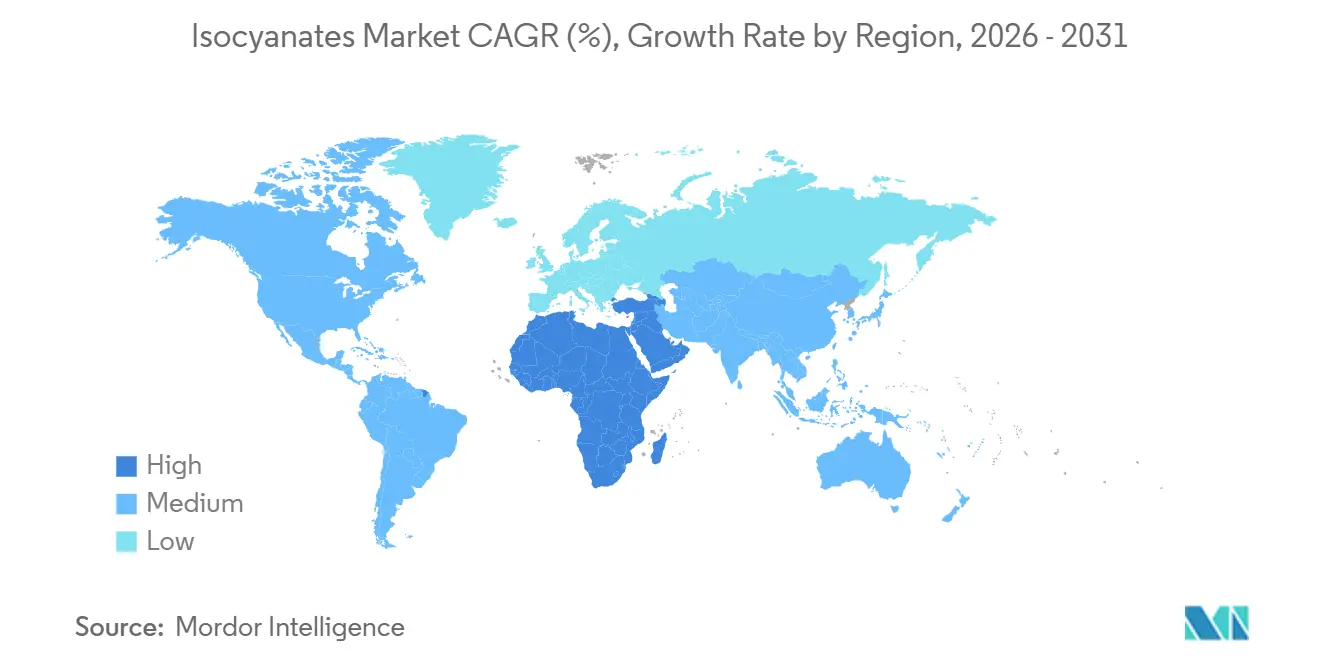

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Isocyanates Market Analysis by Mordor Intelligence

The Isocyanates Market size is projected to be 17.66 million tons in 2025, 18.76 million tons in 2026, and reach 25.35 million tons by 2031, growing at a CAGR of 6.21% from 2026 to 2031. Demand is buoyed by tighter building-energy codes, the automotive transition toward electric vehicles, and persistent growth in the Asia-Pacific construction. Methylene diphenyl diisocyanate (MDI) dominates because rigid polyurethane foam remains the insulation of choice for walls, roofs, and appliance panels. Aliphatic grades such as hexamethylene diisocyanate (HDI) and isophorone diisocyanate (IPDI) are gaining momentum in automotive clearcoats and industrial maintenance coatings that require ultraviolet durability. Feedstock volatility, especially in benzene-to-aniline chains, compresses producer margins and accelerates vertical integration.

Key Report Takeaways

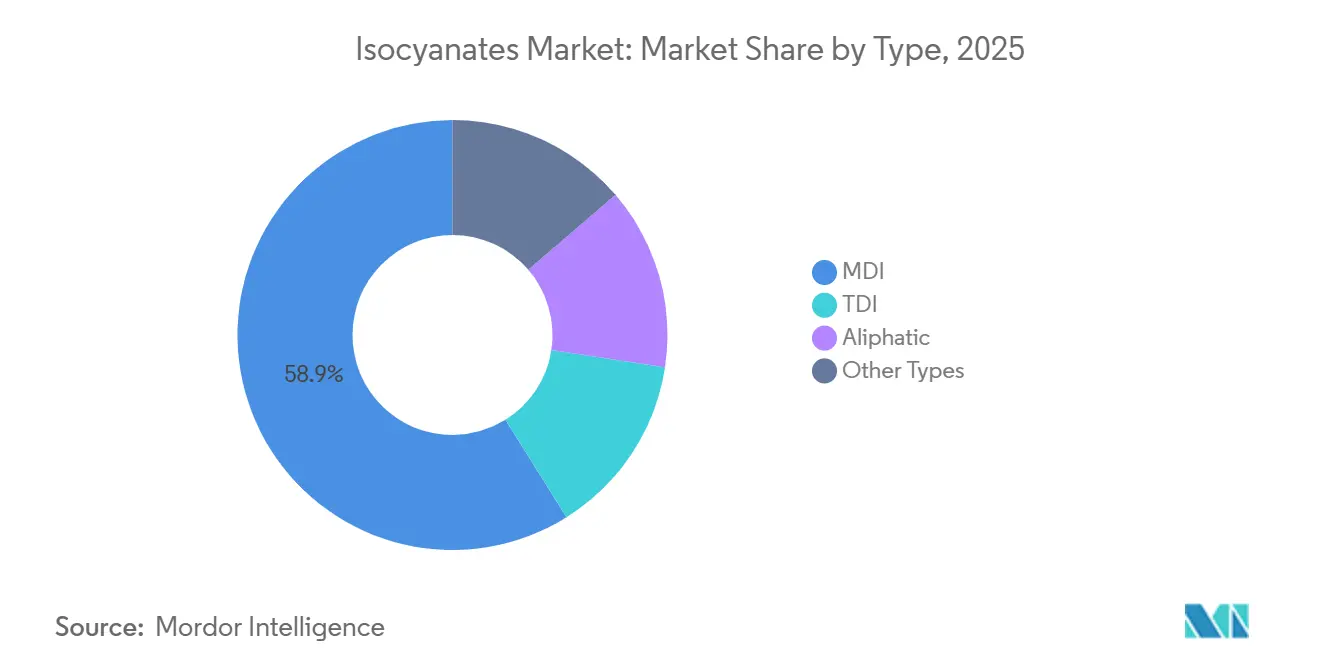

- By type, MDI commanded 58.90% of the isocyanates market share in 2025. Aliphatic isocyanates are forecast to register a 6.78% CAGR through 2031.

- By application, rigid foam represented 32.51% of the 2025 share, while paints and coatings are advancing at a 6.52% CAGR to 2031.

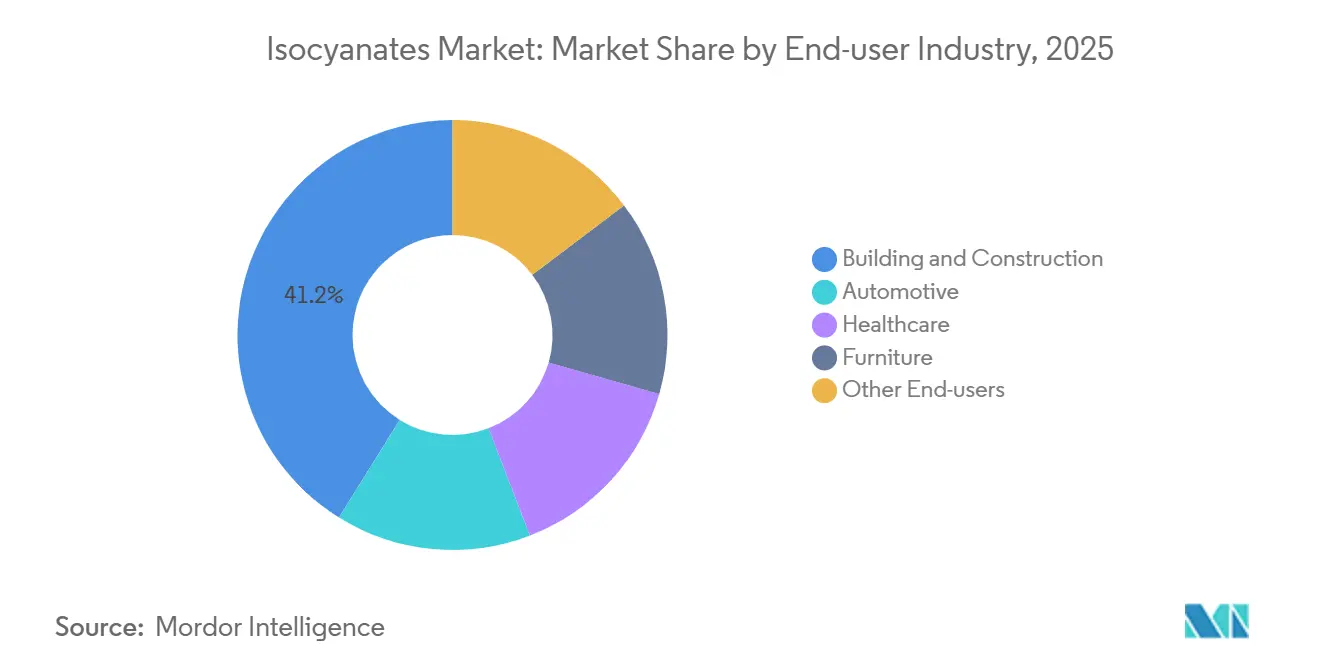

- By end-user, building and construction held 41.15% of the 2025 volume; automotive is projected to expand at a 6.67% CAGR through 2031.

- By geography, the Asia-Pacific region held a 46.91% share of the isocyanates market in 2025; the Middle-East and Africa are expected to post the highest regional CAGR of 6.33% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Isocyanates Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for rigid polyurethane foam in building insulation | +1.8% | Global, with peak intensity in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Rapid industrialization and urbanization in Asia-Pacific | +1.5% | Asia-Pacific core, spill-over to Middle-East and Africa | Medium term (2-4 years) |

| Lightweight vehicle trend driving polyurethane composites adoption | +1.2% | Global, led by North America, Europe, China | Medium term (2-4 years) |

| Cold-chain and e-commerce packaging growth | +0.9% | Asia-Pacific, North America, Europe | Short term (≤ 2 years) |

| Wind-turbine blade production using isocyanate composites | +0.7% | Europe, North America, Asia-Pacific (China, India) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Rigid Polyurethane Foam in Building Insulation

Builders are increasingly opting for high-R-value materials in response to tightening energy-efficiency codes. California's 2025 code sets the bar at R-15 for walls with 2 × 4 framing and R-21 for those with 2 × 6 framing[1]California Energy Commission, “2025 Building Energy Efficiency Standards,” energy.ca.gov. In Rhode Island, the RISBC-8 code mandates R-30 continuous insulation for commercial roofs[2]Rhode Island State Building Code, “RISBC-8 Energy Conservation,” building-standards.ri.gov. Polyisocyanurate boards, celebrated for their low thermal conductivity and structural rigidity, have become the go-to choice in North America's commercial roofing landscape. California's stringent measures require that installations of spray polyurethane foam undergo Quality Insulation Installation verification, emphasizing a preference for certified applicators and trusted suppliers. Canada's national endorsements for medium-density spray systems signal a regulatory shift, championing products that excel in both air-sealing and thermal resistance. Such trends underscore the pivotal role of rigid foam in net-zero and passive-house projects, particularly in regions where annual heating demands fall below 15 kWh/m².

Rapid Industrialization and Urbanization in Asia-Pacific

In 2025, new housing projects in China's tier-2 and tier-3 cities, public infrastructure initiatives in India, and a growing industrial base in Vietnam, Thailand, and Indonesia propelled the Asia-Pacific region to dominate global isocyanate consumption. In Q2 2026, Wanhua Chemical expanded its Fujian MDI complex, achieving an annual capacity in the millions of tons. Concurrently, in January 2026, Covestro made a significant increase to its TDI output in Shanghai. China's substantial TDI exports in 2025 cemented its role as a regional price influencer. Furthermore, as cold-chain infrastructure sees expansion, the Asia-Pacific region leads globally, fueled by surging demand for polyurethane insulated panels (boasting a thermal conductivity below 0.022 W/m·K) essential for online grocery deliveries and the logistics of pharmaceutical biologics.

Lightweight Vehicle Trend Driving Polyurethane Composites Adoption

Electric vehicles (EVs) are now incorporating a greater amount of plastics and composites than traditional internal-combustion vehicles. For instance, a North America mid-size EV slated for 2025 is utilizing polyurethane in both foam and elastomer forms. The encapsulation systems for battery packs are meticulously designed to withstand temperature variations ranging from –40 °C to 85 °C, achieve an IPX7 water resistance rating, and minimize permanent deformation. These rigorous standards are achieved through the use of battery-pack foams in combination with specific modules. Additionally, composite covers offer a notable weight advantage over steel counterparts. Due to China's dual-credit policy promoting lightweighting, there has been a marked increase in the use of polyurethane per vehicle.

Cold-Chain and E-Commerce Packaging Growth

The Asia-Pacific region has emerged as the frontrunner in expanding the global refrigerated storage capacity. Rigid polyurethane and polyisocyanurate panels, which boast superior R-value ratings per inch, outperform expanded polystyrene in terms of performance. These panels account for a significant share of expenses in cold-store construction. The pharmaceutical logistics sector, focusing on oncology and biologics that demand precise temperature transport, is further amplifying the need for top-tier insulation. Additionally, hybrid boxes, which combine vacuum-insulated panels with polyurethane cores, not only boost payloads but also maintain temperature consistency over extended periods. This capability is critical for ensuring the successful transcontinental shipping of biologics.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile benzene and nitro-benzene feedstock pricing | -1.3% | Global, with acute pressure in Europe and non-integrated producers | Short term (≤ 2 years) |

| EU REACH training and classification hurdles | -0.6% | Europe, with indirect compliance costs in export markets | Medium term (2-4 years) |

| Supply tightness from China environmental shutdowns | -0.8% | Asia-Pacific, with spill-over to global spot markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Benzene and Nitro-Benzene Feedstock Pricing

In 2024-2025, benzene prices fluctuated within a specific range, while aniline, a precursor to MDI, was priced within another range. Non-integrated producers found it challenging to transfer cost increases downstream before contract renewals. In contrast, integrated industry leaders like Wanhua and BASF mitigated volatility by managing their own benzene-to-aniline production chains. However, they experienced significant swings in quarterly earnings due to feedstock price changes. Additionally, European facilities grappled with high natural gas prices, which elevated nitrobenzene hydrogenation costs and diminished their global competitiveness.

EU REACH Training and Classification Hurdles

Beginning August 2025, European workers handling specific concentrations of diisocyanates will be mandated to complete a tiered training program, with certifications valid for five years. Small businesses, frequently lacking dedicated Environmental Health and Safety (EHS) personnel, grapple with the steep compliance costs. This financial strain has resulted in a deceleration of spray foam adoption in renovation markets. As downstream clients increasingly request proof of certification, procurement cycles have extended. This delay has led some buyers to explore alternatives, such as mineral wool or EPS, even if it means accepting certain performance compromises. Furthermore, innovation is stymied, as any alteration in formulation triggers a need for new safety data sheet evaluations and might also require refresher training sessions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: MDI Dominance Meets Aliphatic Specialty Growth

MDI captured 58.90% of the isocyanates market volume in 2025. Polymeric MDI, with a functionality ranging between 2 and 3, enables formulators to fine-tune viscosity, catering to applications from low-density spray foams to structural panels surpassing 200 kg/m³. TDI remains the preferred choice for flexible foams, especially the 80:20 isomer blend, which is in high demand for furniture and bedding. Aliphatic isocyanates, mainly HDI and IPDI, are rapidly carving out a niche, projected at 6.78% CAGR through 2031, driven by the automotive sector's demand for UV-resistant clearcoats. Strategic acquisitions, including HDI assets in Texas and Thailand, as well as an HDI purchase in France, underscore the industry's shift toward these premium grades. The portfolio also includes specialty prepolymers, blocked systems tailored for powder coatings, and pioneering CO₂-based isocyanates, all aimed at minimizing the carbon footprint.

Aliphatic isocyanate grades are poised for steady growth over the forecast period of 2026–2031. By the end of this period, these grades are anticipated to command a significant share of the overall isocyanates market. Producers are strategically focusing on sectors such as automotive, wind energy, and industrial flooring, where clients prioritize and are willing to invest in enhanced durability and aesthetics.

By Application: Rigid Foam Anchors Volume, Coatings Lead Growth

Rigid foam represented 32.51% of the 2025 share, driven by its high R-value and structural strength. Rigid foam emerged as the preferred choice for building insulation, refrigeration, and spray-applied systems. North American commercial roofs predominantly featured polyisocyanurate boards, securing a dominant share of the market. Closed-cell spray foam gained traction in residential retrofits, appealing to homeowners seeking quick energy-cost paybacks. Meanwhile, flexible foam maintained its essential role in bedding and automotive seating, underscored by robust demand in China's automotive polyurethane foam sector.

Paints and coatings growing 6.52% CAGR by 2031, buoyed by waterborne dispersions keeping VOC levels in check, and two-component aliphatic clearcoats passing stringent Q-UV tests. The isocyanates market for coatings saw notable expansion. Simultaneously, adhesives, sealants, and elastomers found increasing application in electric-vehicle battery modules, catering to vibration damping and thermal management needs. Furthermore, the versatility of polyurethane chemistry shone through its wide-ranging applications, from foundry binders and textile coatings to composite matrices.

By End-User Industry: Construction Leads, Automotive Accelerates

In 2025, ongoing insulation retrofits and a surge in cold-storage warehouses drove the building and construction sector to consume a 41.15% share of isocyanates. As net-zero-energy codes gain traction, the demand for spray foam - valued for its air-sealing properties and durability exceeding forty years - has intensified. At the same time, the automotive sector is outpacing all other end-users, with a 6.67% CAGR anticipated during the forecast period of 2026–2031. Features such as electric-vehicle battery packs, lightweight composite structures, and acoustic damping foams are increasing the value of polyurethane content in vehicles.

The healthcare, furniture, electronics, and marine sectors collectively demonstrate a strong consumption trend. Hospitals are choosing low-emission, CertiPUR-US-compliant foams for their mattresses. Furniture manufacturers are adopting bio-based polyols, leading to a notable decrease in life-cycle greenhouse gas emissions. In the aerospace sector, thermoplastic polyurethane wire coatings are meeting stringent flame-retardancy and low-outgassing benchmarks. The marine sector is leveraging polyurethane's resistance to saltwater and UV rays, utilizing it in decks and buoyancy foams.

Geography Analysis

Asia-Pacific controlled 46.91% of the isocyanates market volume in 2025. By mid-2026, China was not only ramping up its MDI capacity but also increasing TDI output, all supported by an expanding network of cold-chain warehouses. India's housing initiatives, coupled with a manufacturing boom in ASEAN nations, have kept utilization rates in the region high. Furthermore, Vietnam is poised to unveil an MDI splitter, addressing the surging demands from Southeast Asia's furniture and electronics industries.

In 2025, North America grappled with tepid growth, largely due to high interest rates stifling housing starts. However, an expansion in Geismar, Louisiana, increased the region's MDI capacity by 2026. With a more favorable monetary climate anticipated in late 2026, a resurgence in both the construction and automotive sectors is likely. Europe, on the other hand, faced challenges with escalating natural gas prices, a slowdown in new construction, and new REACH training mandates that hindered spray foam adoption. While spot imports from Asia exerted downward pressure on European prices, buyers remained cautious about potential supply disruptions from China.

The Middle-East and Africa are projected to outpace others with a 6.33% CAGR during the forecast period of 2026–2031. A recent acquisition not only secures feedstock proximity but also broadens capabilities from aromatics to polyurethane. The Sadara complex, a collaboration between Saudi Aramco and Dow, stands as the world's largest single-phase chemical facility. It is now intensifying production of downstream polyurethane systems, adhesives, and coatings, targeting local sectors such as construction, automotive, and renewable energy. In South America, Brazil's automotive and agribusiness sectors are key drivers, while Nigeria, Egypt, and Turkey, though smaller players, are emerging markets, particularly as they enhance their infrastructure and cold-chain facilities.

Competitive Landscape

The isocyanates market is moderately consolidated. ADNOC's strategic acquisition of Covestro underscores a burgeoning trend: oil giants are venturing deeper into downstream chemicals, a move aimed at offsetting the stagnation in fuel growth. Investments are gravitating towards aliphatic niches, which enjoy price premiums over their aromatic counterparts. Technology differentiation acts as a secondary competitive edge. Tosoh's innovative CO₂-based isocyanate route not only captures CO₂ annually but also reduces the aniline carbon footprint. Looking ahead, potential disruptions could arise from non-isocyanate polyurethane chemistries, which sidestep hazardous reagents. While early-stage candidates like cyclic-carbonate systems are still in pilot-scale, they are drawing increasing research and development investments.

Isocyanates Industry Leaders

Wanhua Chemical Group Co. Ltd.

BASF SE

Covestro AG

Huntsman Corporation LLC

Dow Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Covestro AG announced the acquisition of two former Vencorex production sites for HDI (Hexamethylene Diisocyanate) derivatives in Freeport, USA, and Rayong, Thailand, expanding its Coatings and Adhesives production footprint. The transaction is expected to close by the end of 2025.

- February 2025: BASF SE announced to expand its MDI (Methylene Diphenyl Diisocyanate) capacity in Shanghai to 401.76 ktpa, addressing rising regional demand. The upgrade involves optimizing production efficiency and extending operational hours of key units. Additionally, BASF is expanding its MDI splitting capacity in Chongqing to 530 ktpa.

Global Isocyanates Market Report Scope

A family of compounds with low molecular weight and high reactivity is known as isocyanates. These chemicals, characterized by the isocyanate group (-NCO), react with alcohol (hydroxyl) groups to produce polyurethane polymers.

The isocyanates market is segmented by type, application, end-user industry, and geography. By type, the market is segmented into MDI, TDI, aliphatic (e.g., HDI, IPDI), and other types. By application, the market is segmented into rigid foam, flexible foam, paints and coatings, adhesives and sealants, elastomers, binders, and other applications. By end-user industry, the market is segmented into building and construction, automotive, healthcare, furniture, and other end-users (aerospace, electronics, marine). The report also covers the market size and forecasts for the isocyanates market in 27 countries across major regions. The market sizing and forecasts for each segment are provided based on volume (Tons).

By Type

| MDI |

| TDI |

| Aliphatic (e.g., HDI, IPDI) |

| Other Types |

By Application

| Rigid Foam |

| Flexible Foam |

| Paints and Coatings |

| Adhesives and Sealants |

| Elastomers |

| Binders |

| Other Applications |

By End-user Industry

| Building and Construction |

| Automotive |

| Healthcare |

| Furniture |

| Other End-users (Aerospace, Electronics, Marine) |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Turkey | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | MDI | |

| TDI | ||

| Aliphatic (e.g., HDI, IPDI) | ||

| Other Types | ||

| By Application | Rigid Foam | |

| Flexible Foam | ||

| Paints and Coatings | ||

| Adhesives and Sealants | ||

| Elastomers | ||

| Binders | ||

| Other Applications | ||

| By End-user Industry | Building and Construction | |

| Automotive | ||

| Healthcare | ||

| Furniture | ||

| Other End-users (Aerospace, Electronics, Marine) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Turkey | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand for isocyanates be by 2031?

The isocyanates market size is projected to be 18.76 million tons in 2026, and reach 25.35 million tons by 2031, growing at a CAGR of 6.21% from 2026 to 2031.

Which end-user sector is growing fastest after 2026?

Automotive applications, especially in electric-vehicle battery encapsulation and lightweight composites, are projected to advance at a 6.67% CAGR.

Why do aliphatic isocyanates command premium prices?

Grades such as HDI and IPDI offer superior UV resistance and gloss retention, making them essential for automotive clearcoats and high-end industrial coatings.

How is regulation affecting European polyurethane markets?

EU REACH now requires mandatory worker training for diisocyanate handling, increasing compliance costs and slowing adoption of spray foam and specialty coatings.

Page last updated on: