Isobutylene Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.58 Billion |

| Market Size (2031) | USD 37.15 Billion |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Isobutylene Market Analysis by Mordor Intelligence

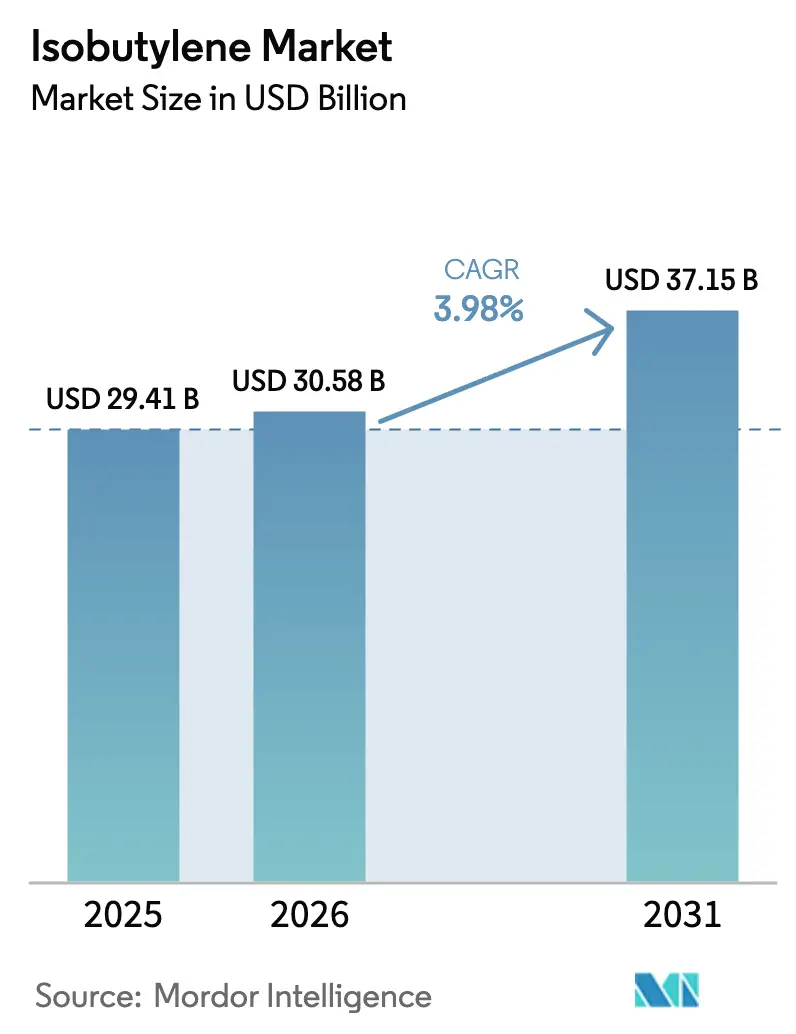

The isobutylene market size was valued at USD 29.41 billion in 2025 and estimated to grow from USD 30.58 billion in 2026 to reach USD 37.15 billion by 2031, at a CAGR of 3.98% during the forecast period (2026-2031). Steady progress comes from isobutylene’s central role in fuel-additive blending, butyl rubber synthesis, and a growing set of specialty materials. Recent regulatory moves—including the U.S. Environmental Protection Agency’s withdrawal of the 1-psi RVP waiver for E10 gasoline across eight Midwestern states—are reshaping octane-boosting demand and encouraging refiners to extract more C4 streams. New capacity additions such as the Texas PO/TBA complex and Asia-Pacific’s petrochemical buildouts are strengthening supply, yet regional over-capacity in light olefins continues to pressure margins. High-purity grades needed for pharmaceutical closures and aerospace sealants are carving out premium niches, while bio-isobutylene start-ups signal a longer-term pivot toward low-carbon routes.

Key Report Takeaways

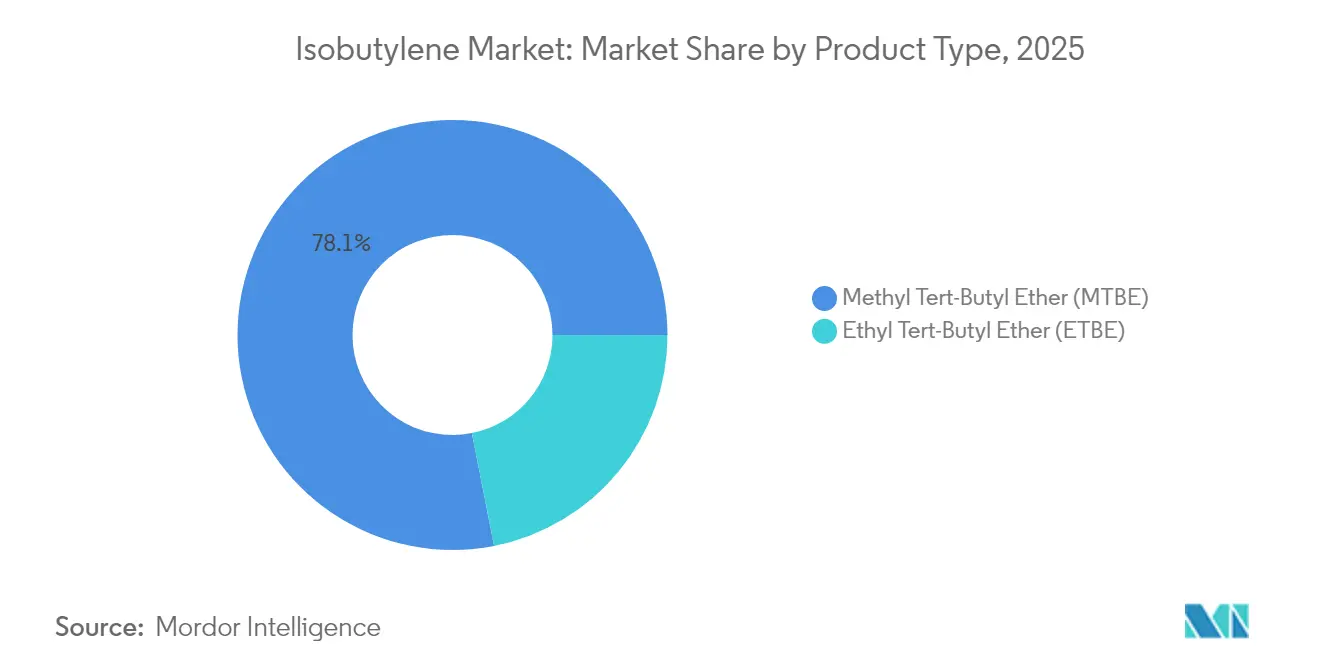

- By product type, MTBE maintained 78.10% of isobutylene market share in 2025, whereas ETBE is projected to record the fastest 5.06% CAGR through 2031.

- By application, monomer for butyl rubber captured 39.20% share of the isobutylene market size in 2025; fuel additives are anticipated to expand at a 5.42% CAGR between 2026-2031.

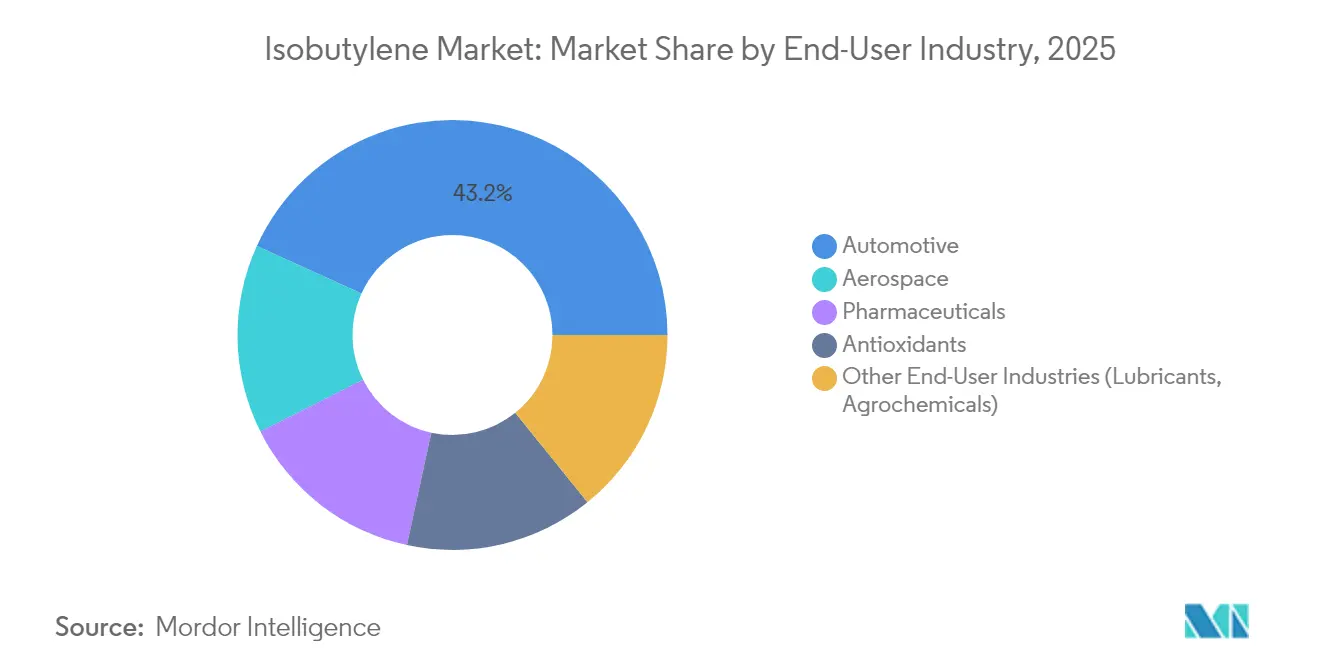

- By end-user industry, the automotive sector held 43.20% revenue share in 2025, while pharmaceuticals are forecast to advance at a 5.05% CAGR to 2031.

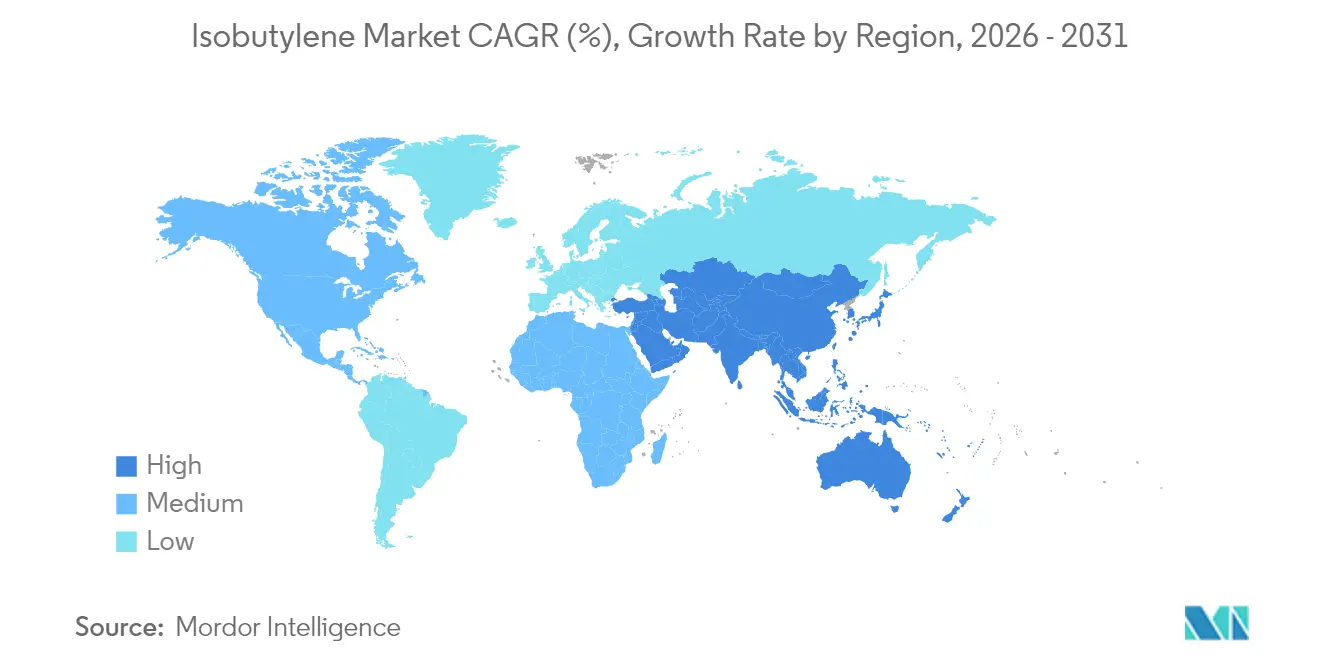

- By geography, Asia-Pacific dominated with 54.80% of isobutylene market share in 2025 and is set to grow at a 4.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Isobutylene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rebound of global butyl rubber tire production | +1.2% | Global, with Asia-Pacific leading | Medium term (2-4 years) |

| Growing demand for MTBE & ETBE anti-knock additives | +0.8% | North America, Europe, emerging markets | Short term (≤ 2 years) |

| Shift to high-purity isobutylene in pharma elastomers | +0.6% | North America, Europe, Japan | Long term (≥ 4 years) |

| Aerospace composites adopting isobutylene-based PIB sealants | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Adoption of bio-isobutylene routes to monetize surplus corn-based bio-ethanol | +0.3% | North America, Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Rebound of Global Butyl Rubber Tire Production

Butyl rubber demand climbed as automotive build rates recovered, prompting a 7% rise in North American polypropylene and 4% rise in polyethylene consumption in 2024[1]LyondellBasell, “LyondellBasell Breaks Ground on World’s Largest PO/TBA Plant,” lyondellbasell.com . Electric-vehicle platforms now favor halogenated butyl inner liners for superior air retention, directly supporting isobutylene monomer offtake. ARLANXEO’s X Butyl line widened medical-grade options, underscoring the material’s span into sterile applications. Newly formulated polyisoprene compounds certified under USP <381> further highlight the migration toward regulation-ready elastomers.

Growing Demand for MTBE & ETBE Anti-Knock Additives

The United States exported 38,000 barrels/day of MTBE in 2024, chiefly to Mexico and Chile[2]U.S. Energy Information Administration, “U.S. Exports of MTBE,” eia.gov. Stricter 2027-2032 vehicle standards are paradoxically boosting high-octane blending to keep combustion engines compliant[3]U.S. Environmental Protection Agency, “Greenhouse Gas Emissions Standards for Light-Duty Vehicles,” epa.gov. Brazil’s liquid-fuel market is expanding 1.4% in 2025 and 1.9% in 2026, with ethanol holding a 47% share of Otto-cycle fuels, encouraging downstream ETBE production. Peer-reviewed work shows MTBE coupled with metal-oxide nano-additives can curb CO and unburned hydrocarbons while raising engine efficiency. Russian forecasts extending to 2035 reinforce the worldwide appetite for octane boosters despite geopolitical headwinds.

Shift to High-Purity Isobutylene in Pharma Elastomers

TPC Group expanded high-purity isobutylene output to serve medical elastomer, adhesive resin, and personal-care formulators. Demand stems from injectable drug closures requiring airtight, low-extractable seals. RJ651-30 polyisoprene meets USP <381> for Type I and II stoppers while delivering 15% higher tensile strength than prior formulations. Green cationic routes using FeCl₃ and tris(pentafluorophenyl)-gallium cut halogen waste, answering sustainability screens for pharma supply chains. Emerging-market vaccine fill-finish expansions, notably in India and Southeast Asia, are bolstering demand for ultra-clean elastomers.

Aerospace Composites Adopting Isobutylene-Based PIB Sealants

BASF leverages 85 years of PIB know-how to furnish moisture-proof sealants for fuel systems and fuselage joints. PIB’s chemical inertness ensures compatibility with composite airframe resins where bisphenol restrictions loom. Global Bioenergies achieved >95% selectivity toward sustainable aviation fuel (e-SAF) intermediates, positioning bio-isobutylene for future jet-fuel blends. Long certification cycles create high switching costs, enabling suppliers of PIB sealants to capture margins that exceed commodity elastomers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing penetration of alkyl-tertiary-amyl ether (TAME) as MTBE substitute | -0.7% | Global, particularly developed markets | Medium term (2-4 years) |

| Volatility in refinery C4 streams limiting captive feedstock | -0.5% | Global, with acute impact in Asia-Pacific | Short term (≤ 2 years) |

| Scale-up risk of bio-isobutylene technologies | -0.2% | Global, with focus on North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Penetration of Alkyl-Tertiary-Amyl Ether (TAME) as MTBE Substitute

Twenty-three U.S. states banned MTBE following groundwater issues, leading refiners to weigh TAME’s lower solubility and comparable octane performance. Vapor-pressure balancing during RFG blending complicates a direct switch, yet ISOMALK-3 isomerization technology cuts operational cost 20% and extends catalyst life a decade, making TAME feedstock cheaper. Future Renewable Fuel Standard volume targets emphasize advanced bio-oxygenates, putting additional pressure on MTBE economics.

Volatility in Refinery C4 Streams Limiting Captive Feedstock

Margins at several Southeast Asian crackers turned negative in 2024, triggering unplanned shutdowns that tightened regional C4 supply. Spot n-butane swings track Brent volatility, causing feedstock price whiplash for isobutylene producers. ONGC will import 800,000 t/y of U.S. ethane by mid-2028 to stabilize cracker yields, underscoring the lengths firms take to derisk supply. EU cracker rationalization aims to mothball another 1 Mt/y of ethylene by 2026 to restore 86-88% utilization. Upcoming U.S. fuel-streamlining rules effective July 2025 layer extra compliance costs that could divert C4 streams toward alkylate over isobutylene extraction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: MTBE Dominance Faces ETBE Challenge

MTBE held 78.10% share of the isobutylene market in 2025, owing to its entrenched role in octane upgrading, while ETBE is forecast to climb at 5.06% CAGR through 2031. Evonik’s German and Belgian units keep Europe supplied, illustrating MTBE’s resilience even under stricter fuel directives. Conversely, ETBE’s bio-ethanol linkage is at the heart of decarbonization strategies: Thailand approved a 200,000 t/y bio-ethylene project supporting downstream ETBE pathways. The isobutylene market size for MTBE-based derivatives is projected to reach USD 28.2 billion by 2031, even as ETBE’s smaller base expands briskly.

R&D combining MTBE with nano-TiO₂ additives to trim tail-pipe emissions keeps MTBE competitive. Still, renewable fuel mandates favor ETBE, especially across the EU and Brazil, suggesting gradual share erosion for MTBE beyond 2030. Both derivatives benefit from integrated PO/TBA complexes that co-produce high-purity TBA for downstream isobutylene recovery.

By Application: Butyl Rubber Leads, Fuel Additives Accelerate

Butyl rubber synthesis accounted for 39.20% of isobutylene market share in 2025, supported by steady tyre-replacement cycles and electric-vehicle uptake. ExxonMobil emphasizes butyl’s pivotal role in air-retention liners and EV battery gaskets. The isobutylene market size attributable to butyl rubber is anticipated to grow at a 4.05% CAGR, reaching USD 14.6 billion by 2031.

Fuel additives show the steepest 5.42% CAGR amid revived MTBE/ETBE demand in Latin America and Asia. Brazilian Otto-cycle growth and U.S. high-octane blending bolster additive offtake. Specialty elastomers and sealants rely on PIB’s impermeability for pharmaceutical stoppers and aerospace joints, creating high-margin pockets. Chemical intermediates such as butadiene from OXO-D processing widen downstream versatility.

By End-User Industry: Automotive Dominance, Pharma Acceleration

Automotive retained a 43.20% share in 2025 thanks to tyre, lubricant, and octane-enhancer demand. Stricter 2027-2032 rules prompt OEMs to intensify engine calibration, raising high-octane additive blends. The isobutylene market size for automotive is forecast to reach USD 16.7 billion by 2031.

Pharmaceutical applications advance at a 5.05% CAGR, benefiting from stricter container-closure mandates. RJ651-30 polyisoprene’s USP <381> compliance typifies the shift toward low-extractable elastomers. Aerospace, although volume-light, captures premium margins, while antioxidant and lubricant uses add diversification across agriculture and industrial fluids.

Geography Analysis

Asia-Pacific controlled 54.80% of the isobutylene market share in 2025 and should log a 4.72% CAGR through 2031. China’s olefin output is forecast to outstrip domestic C2 demand by 121% and C3 by 179% in 2025, creating abundant feedstock yet compressing margins. India’s petrochemical road-map channels USD 87-142 billion to lift capacity from 29.62 Mt to 46 Mt by 2030. Japan pursues carbon-neutral ethylene, potentially catalyzing bio-isobutylene demand.

North America capitalizes on low-cost shale liquids. LyondellBasell’s USD 5 billion PO/TBA complex near Houston will reinforce regional supply from 2026 onward. The EPA’s loss of the 1-psi waiver boosts butane extraction by 26,000 b/d, expanding isobutylene feed availability. Mexico remains a key MTBE import market, absorbing U.S. exports tied to regional refining economics.

Europe faces rationalization: ExxonMobil and SABIC already shuttered 955 kt/y of ethylene, and another 1 Mt/y is scheduled to exit by 2026 to reach sustainable utilization. INEOS’s purchase of LyondellBasell’s EO/D unit signals strategic focus on high-purity intermediates.

South America’s biofuels drive offers growth. Petrobras earmarked USD 111 billion for 2025-2029 downstream investments, aligning with RenovaBio credit incentives.

The Middle East and Africa exploit advantaged feedstock; SABIC’s USD 6.4 billion Fujian complex and collaborations with Aramco and Sinopec deepen integration with Asian customers.

Competitive Landscape

The isobutylene market is moderately consolidated in nature. Established participants leverage vertically integrated complexes to manage cost and secure feedstock. BASF runs PIB operations from the 1930s, supplying pharmaceuticals and aerospace. ExxonMobil and SABIC pursue joint ventures that capture scale while optimizing cracker utilization. LyondellBasell’s new PO/TBA facility will be the world’s largest and pairs propylene-oxide value with tertiary butyl alcohol that can be dehydrogenated to isobutylene, tightening the company’s grip on global trade flows.

TPC Group’s OXO-D technology yields high-reactivity isobutylene for performance polymers, underpinned by 300+ patents. Huntsman’s partnership with Sinopec anchors Chinese PO/MTBE output that feeds both domestic and export markets.

Bio-based entrants remain niche yet strategic: Global Bioenergies scaled to 1,000 t/y and targets aviation fuel demonstration by 2027, appealing to airlines seeking low-carbon scope 3 reductions. Consolidation is likely as sustainability certification, pharma GMP compliance, and aerospace NADCAP audits raise capital intensity.

Isobutylene Industry Leaders

-

Exxon Mobil Corporation

-

TPC Group

-

BASF

-

Shell plc

-

LyondellBasell Industries Holdings B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: LyondellBasell started constructing a USD 5 billion PO/TBA complex in Texas that will be the world’s largest integrated facility for these co-products, boosting U.S. isobutylene derivative capacity.

- May 2023: ExxonMobil Catalysts & Licensing and Axens formed an alliance giving Axens exclusive rights to ExxonMobil’s MTBE Decomposition technology for high-purity isobutylene production.

Global Isobutylene Market Report Scope

Isobutylene is a colorless gas with a mild odor of petroleum. Isobutylene is utilized as an intermediate in the manufacture of a wide range of products. It is used in the manufacture of aviation gasoline, other chemicals, antioxidants for food, packaging, plastics, etc., among others. The Isobutylene market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into Methyl Tert-Butyl Ether and Ethyl Tert-Butyl Ether. By end-user industry, the market is segmented into aerospace, automotive, rubber, pharmaceuticals, and other end-user industries. The report also covers the market size and forecasts for the market in 15 countries across the globe. For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

| Methyl Tert-Butyl Ether (MTBE) |

| Ethyl Tert-Butyl Ether (ETBE) |

| Fuel Additives |

| Monomer for Butyl Rubber |

| Chemical Intermediate |

| Specialty Elastomers & Sealants |

| Automotive |

| Aerospace |

| Pharmaceuticals |

| Antioxidants |

| Other End-User Industries (Lubricants, Agrochemicals) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Methyl Tert-Butyl Ether (MTBE) | |

| Ethyl Tert-Butyl Ether (ETBE) | ||

| By Application | Fuel Additives | |

| Monomer for Butyl Rubber | ||

| Chemical Intermediate | ||

| Specialty Elastomers & Sealants | ||

| By End-User Industry | Automotive | |

| Aerospace | ||

| Pharmaceuticals | ||

| Antioxidants | ||

| Other End-User Industries (Lubricants, Agrochemicals) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Isobutylene Market size?

The Isobutylene Market is valued at USD 30.58 billion in 2026 and is forecast to reach USD 37.15 billion by 2031.

Which product holds the largest isobutylene market share?

In the Isobutylene Market, MTBE dominates with 78.10% of global revenue in 2025, thanks to its entrenched role as an octane enhancer.

Which application segment is growing fastest?

In the Isobutylene Market, fuel additives are projected to grow at a 5.42% CAGR between 2026-2031 as regulators tighten octane and emissions requirements.

Why is Asia-Pacific the leading region?

In the Isobutylene Market, the region commands 54.80% of global demand due to large-scale petrochemical expansions in China and India that secure abundant C4 feedstock and end-use growth.

Page last updated on: