Benzene-Toluene-Xylene (BTX) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 155.83 Million tons |

| Market Volume (2031) | 189.68 Million tons |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benzene-Toluene-Xylene (BTX) Market Analysis by Mordor Intelligence

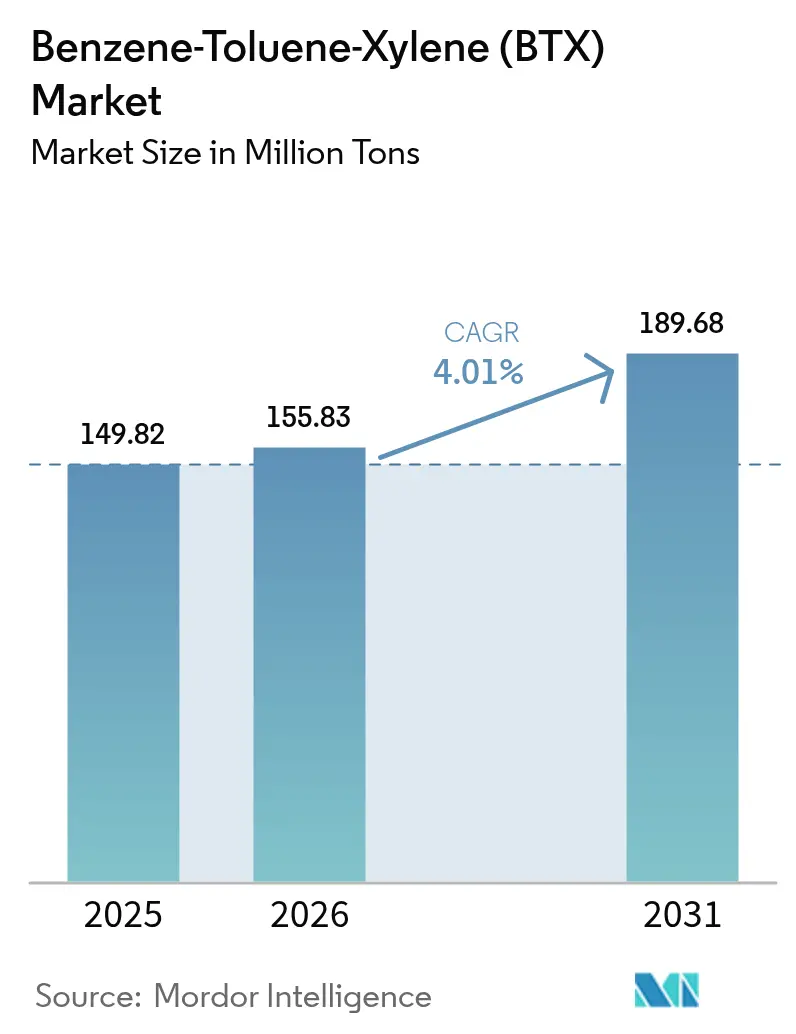

The Benzene-Toluene-Xylene Market size is projected to be 149.82 million tons in 2025, 155.83 million tons in 2026, and reach 189.68 million tons by 2031, growing at a CAGR of 4.01% from 2026 to 2031. Asia-Pacific holds 62.41% of global volume, supported by large integrated aromatics complexes in China, India, and Malaysia that feed the downstream polyester, styrene, and solvent value chains. Benzene remains the largest product-type slice at 38.33% because it underpins ethylbenzene-to-styrene and cyclohexane-to-nylon routes, whereas toluene is the fastest-growing component at 4.48% CAGR as chemical-intermediate demand for benzene and xylene derivatives outpaces legacy solvent uses. Refinery-petrochemical integration is realigning supply economics; new captive configurations in the United States and Saudi Arabia lift para-xylene and benzene yield while tightening merchant availability, a trend that pushes independent buyers toward long-term offtake contracts. Near-term opportunities lie in bio-based aromatics and circular feedstock loops, but commercial volumes remain limited to pilot-scale demonstration plants in North America and Europe.

Key Report Takeaways

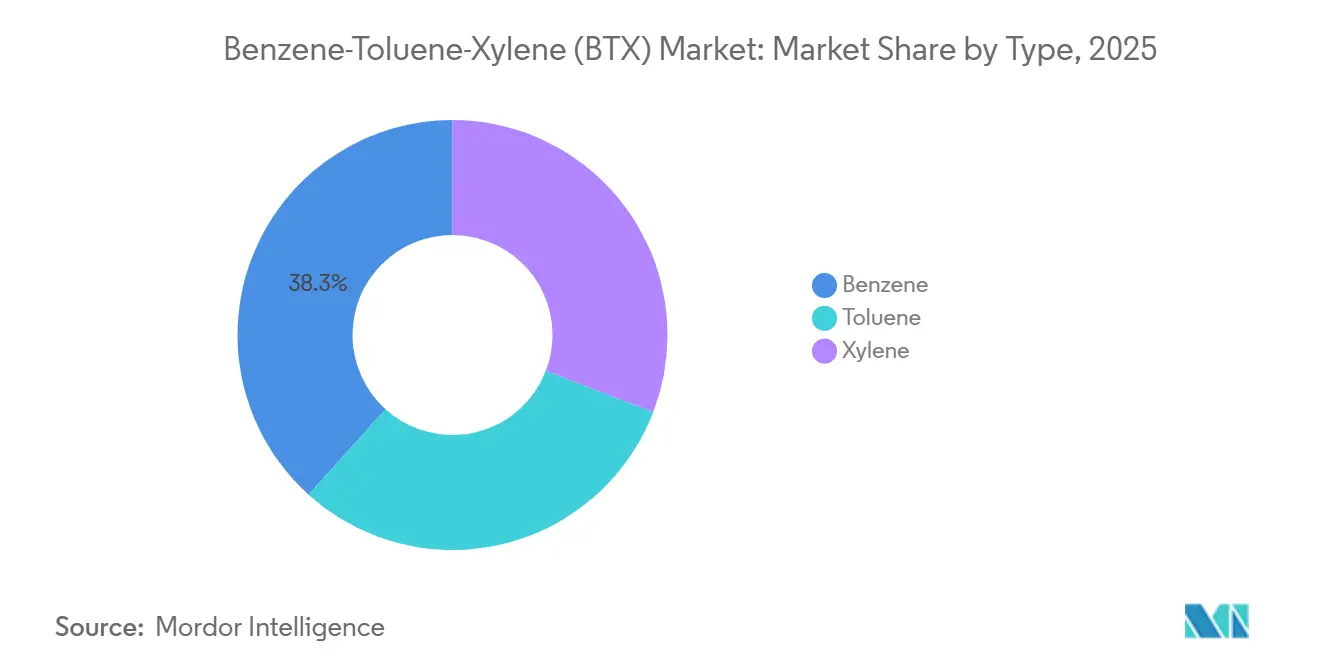

- By product type, benzene accounted for 38.33% of the BTX market share in 2025, whereas toluene is projected to post the fastest 4.48% CAGR through 2031.

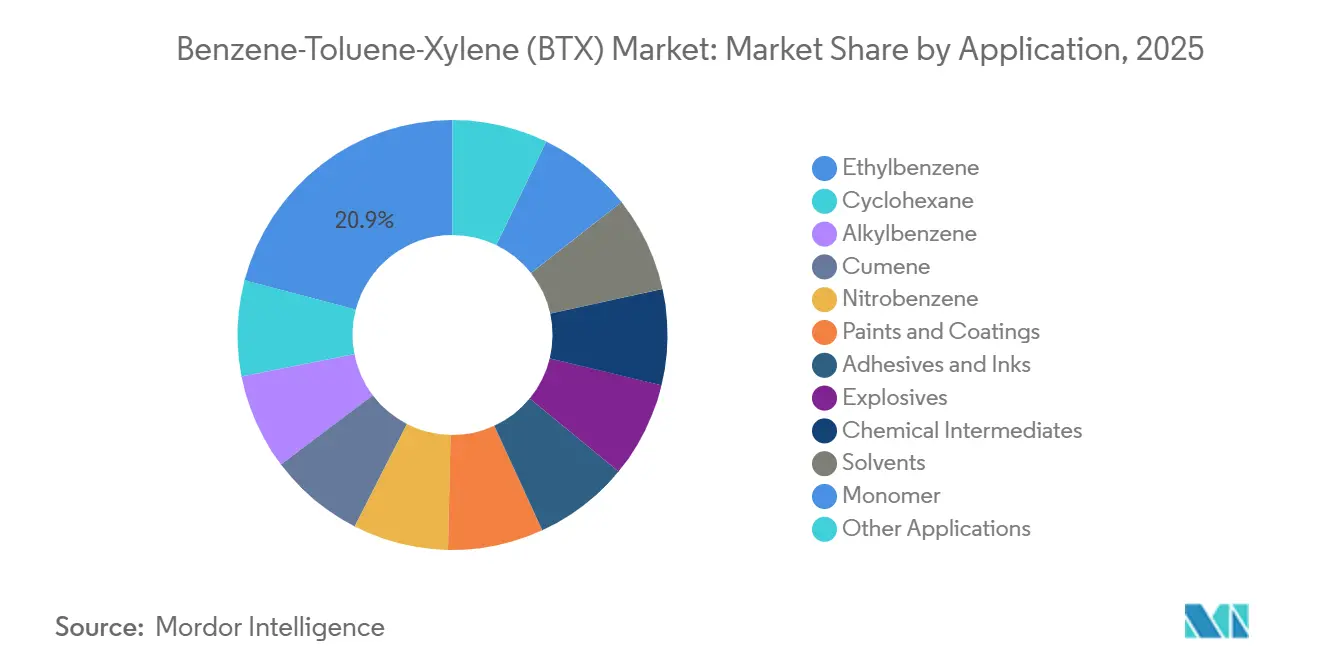

- By application, ethylbenzene retained a 20.91% share of the BTX market size in 2025, while chemical intermediates are set to expand at a 4.79% CAGR between 2026 and 2031.

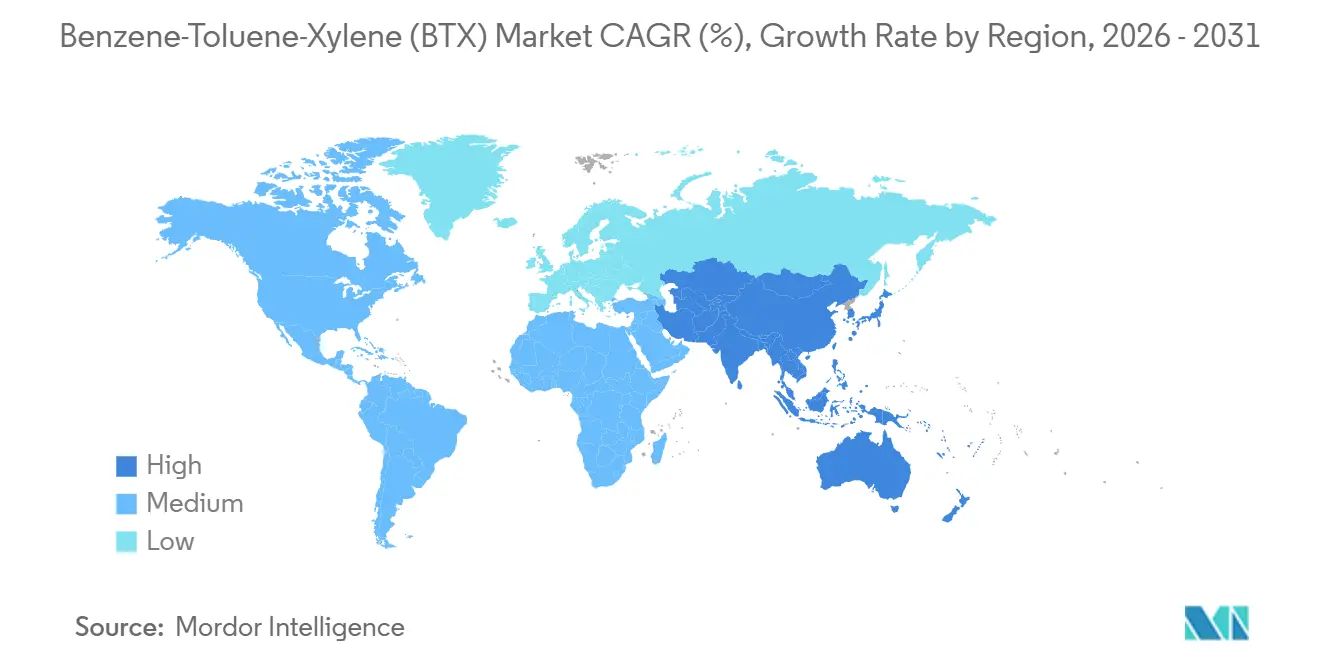

- By geography, the Asia-Pacific region commanded 62.41% of the BTX market share in 2025 and is projected to advance at a 4.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Benzene-Toluene-Xylene (BTX) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CAPEX boom in new aromatics complexes (Asia and Middle-East) | +1.2% | Asia-Pacific (China, India, Malaysia) and Middle East (Saudi Arabia) | Medium term (2-4 years) |

| Surging PET demand keeps para-xylene balances tight | +0.9% | Global, concentrated in Asia-Pacific | Short term (≤ 2 years) |

| Refinery-petrochemical integration unlocking captive BTX extraction | +0.8% | Global (Middle East, Asia-Pacific, North America) | Medium term (2-4 years) |

| Styrene-linked ethylbenzene revival in post-tariff U.S. and India | +0.6% | United States and India | Short term (≤ 2 years) |

| China's Aromatics-Plus policy incentives for high-purity BTX | +0.7% | China, spillover to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

CAPEX Boom in New Aromatics Complexes Reshapes Regional Supply

Between 2024 and 2027, China, India, Saudi Arabia, and Malaysia are set to unveil greenfield and brownfield aromatics projects. In March 2024, a para-xylene unit was inaugurated in Gulei, boasting a significant capacity. Meanwhile, a facility at Pengerang is on the verge of completion, eyeing a mid-2026 debut. Late in 2024, a project expanded its capacity by leveraging a toluene hydro-dealkylation loop for benzene production. Together, these ventures contribute to BTX supply, further solidifying Asia-Pacific's dominance in production. By mandating compliance with ISO 9001 and ISO 14001, the projects emphasize construction quality, emissions monitoring, and worker safety. This commitment elevates initial capital intensity but mitigates operational risks over the project's lifespan[1]International Organization for Standardization, “ISO 9001 Quality Management,” iso.org.

Surging PET Demand Keeps Para-Xylene Balances Tight

In India, Indonesia, and Vietnam, where per-capita PET penetration lags behind North America's, the demand for polyethylene terephthalate resin is surging, predominantly for beverage bottles. Para-xylene, accounting for the majority of xylene demand, is in high demand because producing purified terephthalic acid (PTA) requires this feedstock. Zhejiang-based Rongsheng Petrochemical operates para-xylene facilities with significant annual capacity, running at high utilization, which leaves little room for unexpected demand surges. While ortho and meta-xylene together make up a smaller portion of xylene consumption, their growth is tempered, largely due to phthalic anhydride's struggle against plasticizer substitutions. In January 2026, the premium of para-xylene over mixed xylene reached its peak since 2021. This price surge has led refiners to modify their toluene disproportionation loops, resulting in a trade-off where ortho-xylene and benzene outputs are compromised. To protect downstream polymer catalysts, adherence to ASTM D5453 standards is crucial, ensuring sulfur levels remain below 1 ppm[2]ASTM International, “ASTM D5453 – Total Sulfur,” astm.org.

Refinery-Petrochemical Integration Unlocks Captive Extraction

Integrated crude-to-chemicals schemes now represent a significant portion of the newly added refining capacities. ExxonMobil's Beaumont upgrade merges a crude unit with an aromatics recovery train, producing mixed BTX for nearby styrene and polyethylene assets. Similarly, Saudi Aramco and ExxonMobil push forward with the Samref VFA project, targeting a 2027 launch. This initiative will convert Arabian Heavy crude into benzene and para-xylene streams. Motiva has greenlit an aromatics hub at Port Arthur, Texas, aiming to reroute reformate away from gasoline. These integrations reduce BTX cash costs compared to standalone naphtha crackers, capitalizing on heavy ends and sidestepping merchant feed premiums. However, this strategy comes with diminished spot liquidity, heightening the risk of price surges during unexpected outages.

Styrene-Linked Ethylbenzene Revival in Post-Tariff Markets

In 2025, U.S. styrene production surged year-on-year, as Section 232 tariffs effectively sidelined Asian imports from the Gulf Coast. In August 2024, Chevron Phillips Chemical executed a debottlenecking process, boosting its styrene output, which in turn elevated ethylbenzene demand annually. Trinseo, in January 2025, augmented its styrene capacity and secured benzene supply through tolling agreements. India is on a similar trajectory, forecasting a CAGR in styrene demand through 2031. This trend has led Reliance Industries to explore an expansion, leveraging its captive ethylbenzene. To prevent polymer yellowing, the Bureau of Indian Standards mandates a styrene purity of over 99.7% under IS 517, steering producers towards higher-spec benzene feed.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carcinogenicity-driven occupational exposure curbs | -0.5% | Global (OSHA in United States, EU regulations, WHO guidance) | Long term (≥ 4 years) |

| VOC caps in paints/adhesives favour low-aromatic blends | -0.4% | North America and Europe (EPA, EU Directive 2004/42/EC) | Medium term (2-4 years) |

| Octane-for-aromatics trade-off in gasoline pool after E10 rollout | -0.3% | Global, primarily North America, Europe, Brazil | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Carcinogenicity-Driven Exposure Limits Raise Compliance Costs

The U.S. Occupational Safety and Health Administration (OSHA) enforces strict benzene exposure limits: a time-weighted average of 1 ppm and a short-term ceiling of 5 ppm. These measures are in response to links between benzene overexposure and acute myeloid leukemia. Operators are now mandated to invest in sealed loading arms, vapor-recovery systems, and real-time air monitors. Additionally, they must finance annual blood tests for staff with exposure records surpassing the set thresholds. The World Health Organization (WHO) and corresponding EU directives advocate for these stringent thresholds on a global scale. Retrofitting a mid-1980s aromatics extraction train to meet contemporary ventilation and monitoring standards demands significant investment. Furthermore, for a plant with 100 personnel, ongoing surveillance and personal protective equipment (PPE) expenses are considerable. In 2025, Shell closed its aging Pulau Bukom benzene unit, deeming the upgrade costs economically unviable. Similarly, SABIC shut down its Geleen operations for the same reason.

VOC Caps in Coatings Redirect Solvent Demand

In a move to tighten regulations, the EPA has updated its aerosol-coating air-toxic rules, designating high reactivity factors to benzene, toluene, and xylene. As a result, these substances are now limited to a combined content of 5 wt% in spray paints. Meanwhile, Europe's Directive 2004/42/EC imposes stringent restrictions on VOCs in decorative paints: water-based grades are capped at 30 g/L, and solvent systems at 300 g/L. This effectively sidelines aromatics from products boasting eco-labels. In response to these regulations, AkzoNobel has pivoted, now using aromatic-free carriers in its European paint range, albeit at the expense of pricier isoparaffinic solvents. Similarly, PPG has reformed its North American industrial coatings, replacing xylene annually with propylene glycol ethers. These shifts underscore a broader trend: as regulatory pressures mount and retailers lean away from legacy solvents, there's a noticeable pivot, channeling more toluene and xylene into chemical-intermediate applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Benzene Maintains Volume Leadership While Toluene Sets the Pace

In 2025, benzene accounted for 38.33% of the total volume, bolstering chains from ethylbenzene to styrene, cyclohexane to nylon, and cumene to bisphenol A. Ethylbenzene, in particular, consumed a major share of the 2025 benzene output. The market for benzene derivatives within the Benzene-Toluene-Xylene (BTX) segment is projected to grow steadily through 2031. Demand from detergents and polyurethanes has secured an additional share from cumene, nitrobenzene, and alkylbenzene. Cyclohexane, accounting for a notable portion of benzene's usage, is witnessing growth, driven by the increasing adoption of nylon 6 fiber in automotive under-hood components.

Toluene, while smaller today, is the Benzene-Toluene-Xylene (BTX) market’s fastest-advancing aromatic at a 4.48% CAGR. As of now, a significant portion of toluene is being funneled into disproportionation and trans-alkylation units, producing benzene and para-xylene, a notable rise from earlier years. While traditional sectors like paint, ink, and adhesives—previously accounting for a substantial share of toluene's consumption—have diminished due to VOC regulations, niches such as explosives and nitration chemistry continue to thrive. Adhering to ASTM purity standards ensures that metal and sulfur contaminants remain within catalyst-tolerance limits, thereby enhancing downstream efficiency.

By Application: Ethylbenzene Dominates but Intermediates Grow Fastest

Ethylbenzene held 20.91% of 2025 demand and remains the single-largest outlet. This trend is set to continue, especially with global styrene capacities projected to grow significantly by 2031. Despite the growth of other derivatives, ethylbenzene's share in the Benzene-Toluene-Xylene (BTX) market is anticipated to remain strong. Meanwhile, chemical intermediates, primarily through toluene disproportionation and transalkylation, are forecast to record a 4.79% CAGR. These processes convert surplus toluene into benzene and xylene, addressing para-xylene shortfalls. Cyclohexane maintains a consistent share, closely linked to nylon fiber demand. At the same time, cumene and alkylbenzene are benefiting from rising demands in detergents and polycarbonates.

Toluene's usage is evolving. While paints, coatings, and inks are facing tighter solvent-content regulations, there's a growing trend of using toluene as a chemical intermediate, driven by refiners aiming for enhanced value. In the xylene market, para-xylene dominates, commanding the majority of isomer demand. It's primarily used to produce purified terephthalic acid for PET. Ortho-xylene, with its niche share in phthalic anhydride, is gradually gaining ground, albeit slowly, due to shifts in plasticizer preferences. Meta-xylene's allocation in isophthalic acid is predominantly linked to the demand for high-performance coatings.

Geography Analysis

Asia-Pacific anchored 62.41% of 2025 volume and is forecast to clock a 4.22% CAGR through 2031. China commands a significant portion of the regional demand, driven by para-xylene production operating at near full capacity. Meanwhile, India is set to bolster this demand further, with additional aromatics capacity being added between 2024 and 2026. In Japan and South Korea, capacity dynamics shift as output is reduced in some units and exports are redirected towards Southeast Asia.

North America sees its Benzene-Toluene-Xylene (BTX) market size stabilize, albeit with greater integration. By 2026, new capacity is set to be introduced, predominantly targeting in-house styrene and polyester chains. While Canada maintains steady benzene output, Mexico faces challenges with unit utilization, hindered by delays in refinery modernization.

Europe’s share shrinks as traditional refineries shift focus from aromatics. Some units have been closed or repurposed for biofuel production. However, certain facilities remain resilient, boasting significant production capacities. South America, spearheaded by a major complex, contributes to the global volume, while contributions from the Middle-East and Africa rise, buoyed by capacity extensions and new projects.

Competitive Landscape

The Benzene Toluene Xylene (BTX) market is moderately fragmented. ExxonMobil’s Singapore and Beaumont hubs pair crude units with aromatics extraction and downstream styrene, removing merchant benzene exposure. Strategic themes center on scale integration, regional arbitrage, and feedstock agility. Bio-BTX and chemically recycled aromatics still sit at pilot scale. Mounting capacity additions in Asia-Pacific and the Middle-East are already compressing merchant benzene margins, sharpening the focus on integrated models and low-cost logistics.

Benzene-Toluene-Xylene (BTX) Industry Leaders

Exxon Mobil Corporation

China Petrochemical Corporation

Reliance Industries Limited

Shell plc

SABIC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Union Minister of Petroleum and Natural Gas launched Mangalore Refinery and Petrochemicals Limited (MRPL)'s product, Toluene, during his visit to the refinery. With an annual production capacity of 40,000 metric tons (TMT), MRPL’s Toluene facility exemplifies India’s progress toward self-reliance.

- June 2024: Encina Development Group, LLC (Encina), known for its ISCC PLUS-certified circular chemicals, signed a long-term supply agreement with BASF. The agreement centers on chemically recycled circular benzene, sourced from post-consumer end-of-life plastics. BASF plans to integrate this recycled benzene into its extensive Ccycled product lineup.

Global Benzene-Toluene-Xylene (BTX) Market Report Scope

Benzene is a colorless liquid that is highly volatile in nature and slightly soluble in water. Some of the standard applications of benzene include manufacturing rubbers, dyes, lubricants, pesticides, detergents, and other drugs. It is also used to prepare intermediates to manufacture resin, plastics, and synthetic and nylon fibers.

Toluene is a clear liquid that is naturally found in crude oil. It is widely used in producing paints, fingernail polish, adhesives, rubber, lacquers, and paint thinners, as well as in some leather tanning and printing applications.

Xylene is an aromatic hydrocarbon widely used in staining and cover-slipping applications in the laboratory and tissue processing.

The Benzene-Toluene-Xylene (BTX) market is segmented by type, by application, and by geography. By type, the market is segmented into benzene, toluene, and xylene. By application, the market is segmented into benzene by application (ethylbenzene, cyclohexane, alkylbenzene, cumene, nitrobenzene, and other applications), toluene by application (paints and coatings, adhesives and inks, explosives, and chemical intermediates), and xylene by application (solvents, monomer, and other applications). The report covers the market size and forecasts for the market in 15 countries across the world. For each segment, the market sizing and forecasts are based on volume (Tons).

| Benzene | |

| Toluene | |

| Xylene | Ortho-xylene |

| Meta-xylene | |

| Para-xylene |

| Benzene | Ethylbenzene |

| Cyclohexane | |

| Alkylbenzene | |

| Cumene | |

| Nitrobenzene | |

| Other Applications | |

| Toluene | Paints and Coatings |

| Adhesives and Inks | |

| Explosives | |

| Chemical Intermediates | |

| Xylenes | Solvents |

| Monomer | |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Benzene | |

| Toluene | ||

| Xylene | Ortho-xylene | |

| Meta-xylene | ||

| Para-xylene | ||

| By Application | Benzene | Ethylbenzene |

| Cyclohexane | ||

| Alkylbenzene | ||

| Cumene | ||

| Nitrobenzene | ||

| Other Applications | ||

| Toluene | Paints and Coatings | |

| Adhesives and Inks | ||

| Explosives | ||

| Chemical Intermediates | ||

| Xylenes | Solvents | |

| Monomer | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global BTX demand be by 2031?

It is forecast to reach 189.68 million tons by 2031, rising at a 4.01% CAGR, from 155.83 million tons in 2026.

Which region consumes the most BTX today?

Asia-Pacific leads with 62.41% of 2025 volume and is also the fastest-growing region at 4.22% CAGR.

Why is para-xylene so important to BTX producers?

Para-xylene supplies majority of xylene demand because it is the essential feedstock for purified terephthalic acid used in PET resin.

What is driving benzene demand in the United States?

Post-tariff styrene capacity additions are lifting ethylbenzene consumption, which in turn raises benzene requirements at Gulf Coast complexes.

Page last updated on: