Tumor Necrosis Factor Inhibitors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 42.57 Billion |

| Market Size (2031) | USD 50.77 Billion |

| Growth Rate (2026 - 2031) | 3.59% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

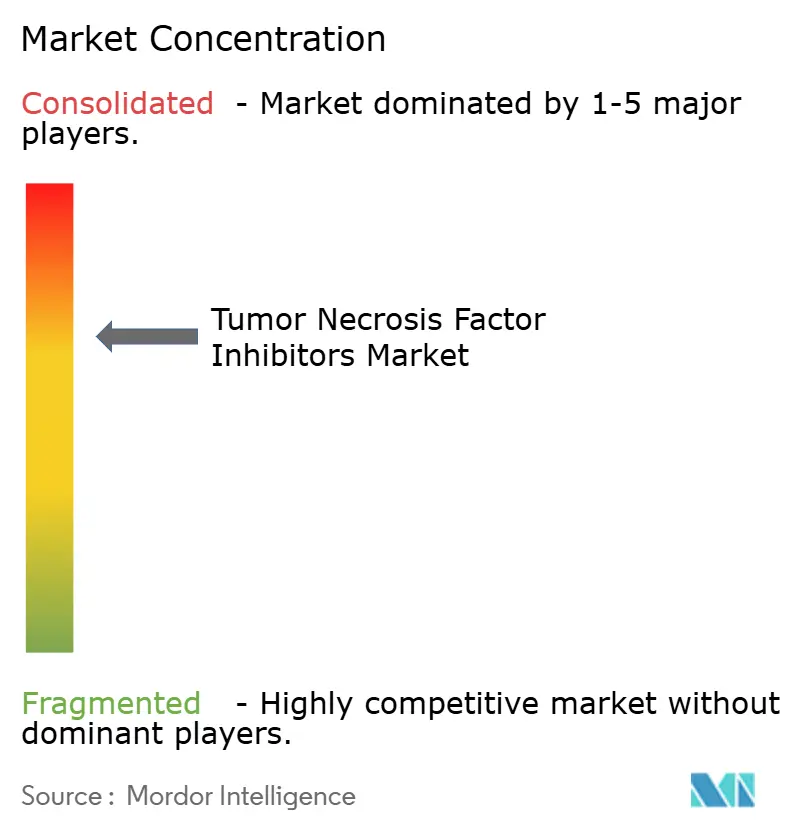

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tumor Necrosis Factor Inhibitors Market Analysis by Mordor Intelligence

The Tumor Necrosis Factor Inhibitors Market size is estimated at USD 42.57 billion in 2026, and is expected to reach USD 50.77 billion by 2031, at a CAGR of 3.59% during the forecast period (2026-2031).

Uptake is shifting from originator brands to biosimilars as pharmacy benefit managers exclude high-priced reference products, while prescribers respond to payer incentives that reward cost containment. The expanding prevalence of autoimmune diseases, earlier diagnostic imaging, and an aging population create a steady flow of biologic-naïve patients entering therapy, offsetting price erosion. Connected self-injection devices improve adherence, positioning auto-injector pens as growth drivers. Meanwhile, favourable reimbursement policies in North America and Europe have kept volumes resilient, even as discounts spread across formularies. Competitive dynamics now hinge on local manufacturing scale, digital health integrations, and the pace of regulatory approvals rather than on traditional promotional spend.

Key Report Takeaways

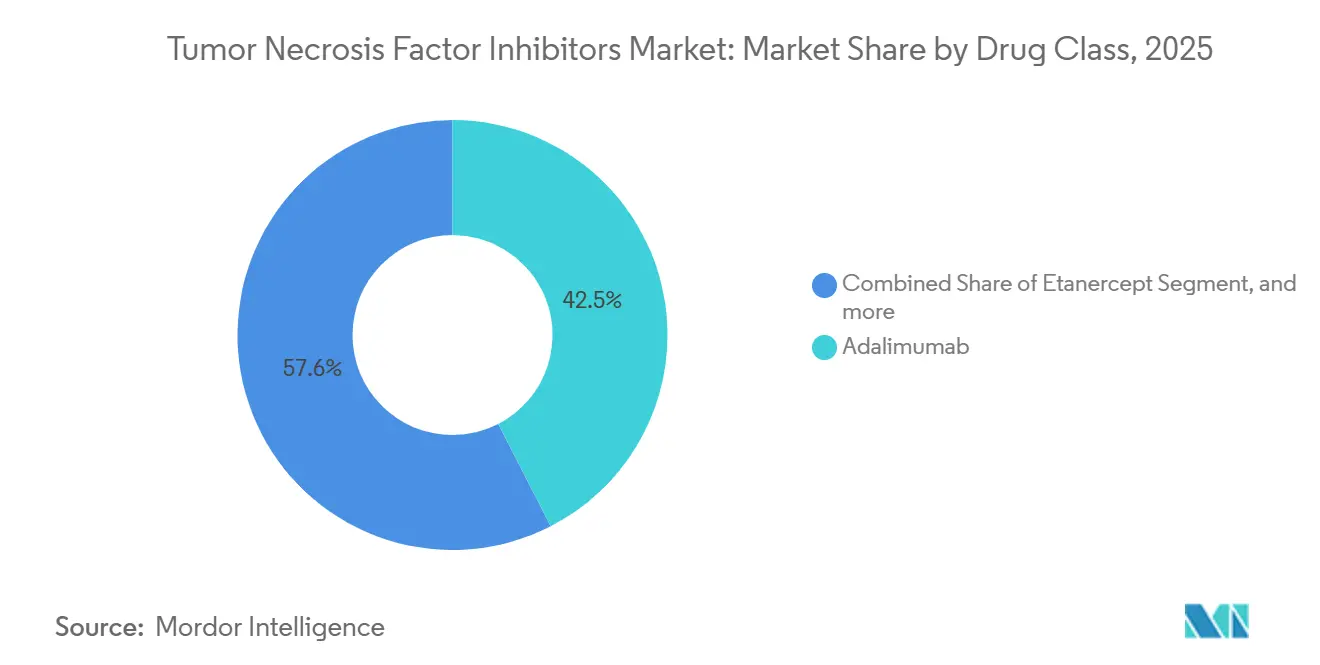

- By drug class, adalimumab led with a 42.45% revenue share in 2025; biosimilars are projected to expand at a 5.43% CAGR through 2031.

- By indication, rheumatoid arthritis accounted for 28.54% of 2025 revenue; ulcerative colitis is advancing at a 6.89% CAGR to 2031.

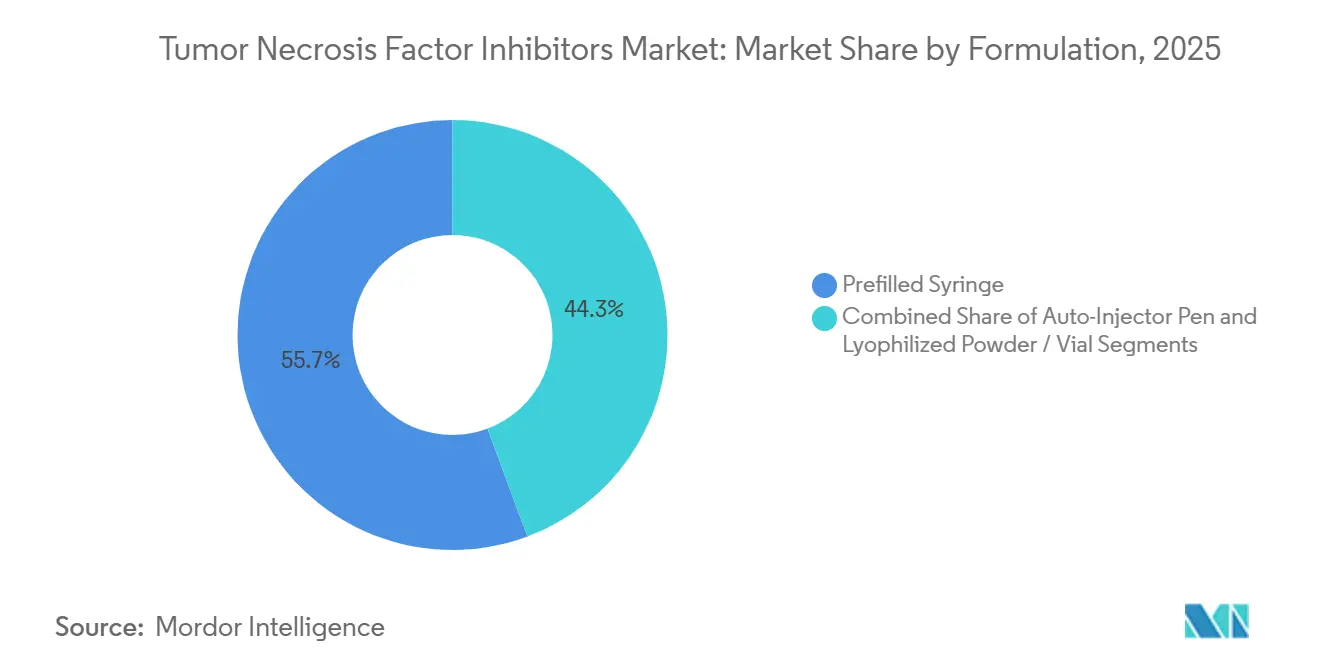

- By formulation, prefilled syringes accounted for 55.67% of 2025 sales; auto-injector pens are forecast to rise at a 5.76% CAGR over the same horizon.

- By end user, hospital pharmacies accounted for 52.65% of the 2025 turnover; online pharmacies are projected to grow at a 6.76% CAGR through 2031.

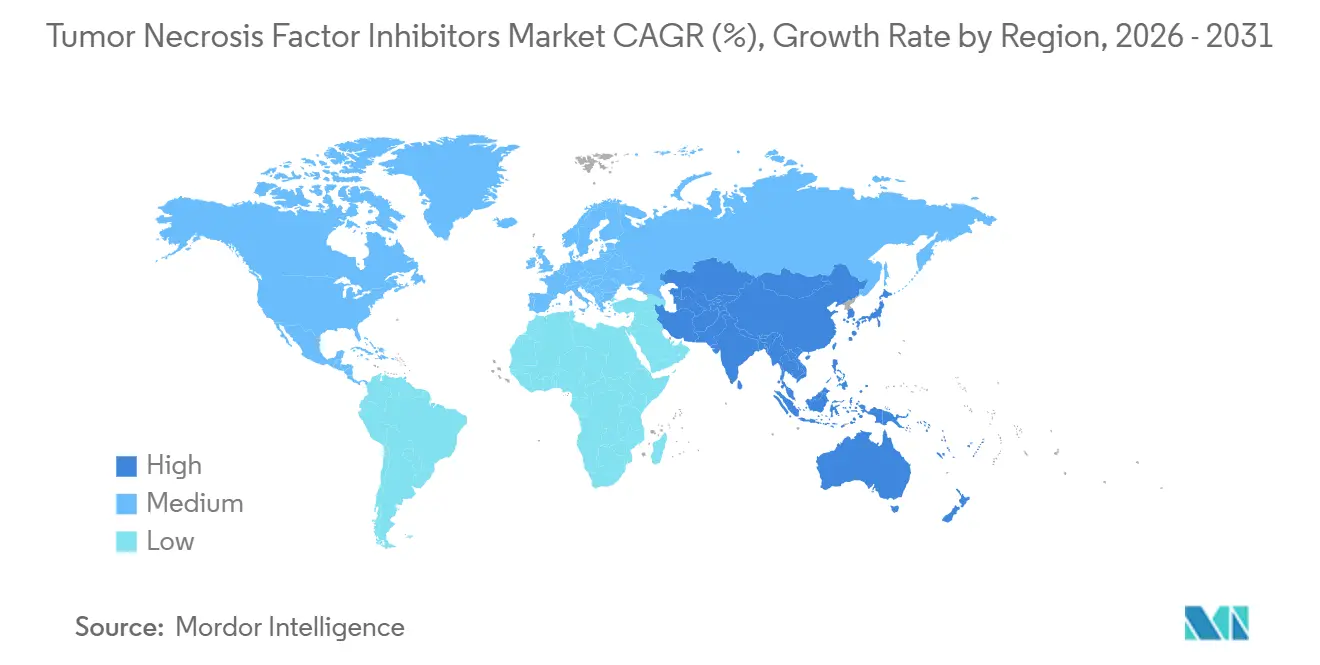

- By geography, North America secured 42.65% of the 2025 spend; Asia-Pacific is projected to increase at a 4.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tumor Necrosis Factor Inhibitors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Global Prevalence of Autoimmune Disorders and Rise in Geriatric Population | +0.9% | Global, with highest concentration in North America and Europe | Long term (≥ 4 years) |

| Accelerated Biosimilar Approvals & New Product Launches | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Expanding Clinical Indications of TNF Inhibitors | +0.7% | Global, with early adoption in North America | Medium term (2-4 years) |

| Favorable Reimbursement Policies in Developed Markets | +0.8% | North America, Europe | Short term (≤ 2 years) |

| Subcutaneous Self-Injection Pen Innovations | +0.4% | North America, Europe, Japan | Medium term (2-4 years) |

| AI-Enabled Pharmacovigilance Shortening Risk Evaluation | +0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Global Prevalence of Autoimmune Disorders and Rise in Geriatric Population

Rheumatoid arthritis affects roughly 18 million people worldwide, and incidence climbs in populations older than 65, a cohort expanding faster than any other age group. Earlier imaging with ultrasound and MRI now detects subclinical inflammation, raising the treatment-eligible pool for psoriatic arthritis and ankylosing spondylitis by nearly 20% since 2024. Inflammatory bowel disease registries document double-digit growth in cases of Crohn’s disease and ulcerative colitis, partly attributed to lifestyle factors that alter the gut microbiota[1]Gastroenterology Journal, “Dietary Drivers of IBD,” gastrojournal.org. This epidemiologic pressure sustains baseline demand even when unit prices fall. As a result, the tumor necrosis factor inhibitors market continues to widen its treated base, enabling manufacturers to preserve revenue streams despite biosimilar penetration.

Accelerated Biosimilar Approvals & New Product Launches

The FDA cleared eight adalimumab biosimilars through July 2023, with Cyltezo and Simlandi earning interchangeability status that permits pharmacy substitution. European tender systems are expected to drive infliximab biosimilar uptake above 90% in Denmark and Norway by 2024. Samsung Bioepis and Celltrion expanded their portfolios with copies of etanercept and infliximab, securing approvals in China, Japan, and India, while leveraging their domestic plants to lower the cost of goods. As patent cliffs approach for certolizumab pegol and golimumab, pipeline entrants aim to maintain the biosimilar price-volume flywheel. Collectively, these launches accelerate the shift toward lower-priced alternatives, reshaping formulary access across mature markets.

Expanding Clinical Indications of TNF Inhibitors

Real-world evidence published in 2024 confirmed response rates of 50% or higher for adalimumab in hidradenitis suppurativa, leading dermatologists to adopt biologic therapy earlier in the treatment algorithm. FDA boxed warnings issued in 2021 for JAK inhibitors prompted gastroenterologists to consider TNF blockers as first-line biologics in ulcerative colitis, driving the fastest indication-level CAGR through 2031. Trials in pediatric Crohn’s disease and non-infectious uveitis report remission rates comparable to those in adult populations, encouraging off-label use while formal label expansions progress. These additional use cases diversify revenue beyond legacy rheumatology segments, buffering the tumor necrosis factor inhibitors market against competitive encroachment from newer mechanisms.

Favorable Reimbursement Policies in Developed Markets

Medicare Part D rules effective January 2025 obligate plans to list at least one biosimilar for every reference biologic and cap certain patient co-pays, immediately improving affordability for senior citizens. Germany and France employ value-based contracting, which awards multi-year tenders to biosimilar firms, resulting in savings of over 20% and compressing branded price premiums. Japan similarly cuts reference-product list prices upon biosimilar entry, accelerating switch rates. Private U.S. insurers layer step-edit protocols that withhold coverage of brand-name Humira until biosimilar trials fail, shrinking adalimumab’s net pricing power. Collectively, these policies expand patient access but intensify margin pressure on originators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe Adverse Events & Safety Warnings | -0.6% | Global, heightened scrutiny in North America and Europe | Short term (≤ 2 years) |

| High Cost of Patented Biologics & Access Barriers | -0.9% | Emerging markets in Asia-Pacific, Middle East, Africa, South America | Medium term (2-4 years) |

| Stringent Regulatory Compliance & REMS Costs | -0.4% | Primarily North America and Europe | Long term (≥ 4 years) |

| Cold-Chain Disruptions From Extreme Weather Events | -0.3% | Global, pronounced in tropical and subtropical regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Adverse Events & Safety Warnings

All TNF inhibitors carry boxed warnings for serious infections, with 2024 guidance emphasizing tuberculosis screening and vigilance for opportunistic pathogens[2]U.S. Food & Drug Administration, “Boxed Warning Updates for TNF Inhibitors,” fda.gov. Pediatric malignancy alerts prompt mandatory cancer registries, boosting compliance costs for sponsors. Sporadic but fatal hepatosplenic T-cell lymphoma cases, especially among adolescent males on combination therapy, heighten prescriber caution. Safety monitoring elevates operational expenses and can delay treatment initiation, temporarily damping volume growth. Competing biologics with cleaner safety profiles, such as IL-23 inhibitors, capitalize on these concerns to gain market share in dermatology and rheumatology.

High Cost of Patented Biologics & Access Barriers

List prices for branded TNF blockers exceed USD 60,000 per patient annually in the United States, and even a 55% biosimilar discount often leaves net costs above USD 25,000, a hurdle in low-income settings. Out-of-pocket spending surpasses 50% of healthcare expenditure in many emerging markets, curbing uptake. Temperature excursions during last-mile delivery spoil up to 12% of shipments in tropical regions lacking reliable cold chains. Absent tiered pricing or local assembly, the tumor necrosis factor inhibitors market remains under-penetrated across large swaths of Asia, Africa, and South America.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biosimilars Erode Adalimumab Dominance

Adalimumab retained a 42.45% share of 2025 sales; however, the tumor necrosis factor inhibitors market share for this molecule is declining as eight U.S. biosimilars compete directly with it. Hyrimoz alone garnered a double-digit share within a year of its launch, as pharmacy benefit managers delisted Humira in favor of lower-cost options. The tumor necrosis factor inhibitors market now favors biosimilars that replicate proven efficacy while underpricing reference brands by as much as 55%. Etanercept and infliximab face similar pressure, with European tender systems mandating wholesale switching. Certolizumab pegol and golimumab occupy smaller yet more stable niches: one offers monthly dosing, while the other avoids placental transfer, making them appealing options for pregnant patients. Longer-acting TNF inhibitors in early pipelines may offset some erosion if they secure quarterly or twice-yearly dosing, but commercial timelines stretch beyond 2030.

Biosimilar volumes climb at a 5.43% CAGR, nearly double the class average, a dynamic that compresses revenue per dose yet broadens total patient reach. Originators are pivoting toward next-generation agents, such as Skyrizi and Rinvoq, to protect their profitability. Investors, therefore, judge incumbents more on the depth of their pipeline than on their ability to defend legacy franchises. For new entrants, manufacturing scale and device partnerships with firms like Ypsomed matter more than Salesforce's size. The path forward rewards low-cost producers and companies that pair molecules with digital adherence ecosystems.

By Indication: Ulcerative Colitis Outpaces Rheumatoid Arthritis

Rheumatoid arthritis accounted for 28.54% of 2025 revenues, anchoring the largest patient population treated with TNF blockers. Yet ulcerative colitis posts the fastest trajectory, expanding at a 6.89% CAGR as boxed warnings constrain JAK inhibitor use and payers institute step-therapy that starts with TNF inhibition. The tumor necrosis factor inhibitors market size for gastroenterology indications is forecast to surpass USD 15 billion by 2031, making this specialty a priority for biosimilar marketers seeking large-volume contracts. Psoriatic arthritis and ankylosing spondylitis each benefit from earlier imaging-based diagnoses that extend biologic eligibility, while Crohn’s disease growth stabilizes at mid-single digits.

Hidradenitis suppurativa, although currently a niche condition, presents a high unmet need and a strong real-world response, allowing for premium pricing despite class-wide discounts [3]Journal of the American Academy of Dermatology, “Real-World Hidradenitis Suppurativa Outcomes,” jaad.org. Pediatric trials, if successful, will unlock longer treatment durations per patient, as children initiating therapy may remain on TNF inhibitors through adolescence and early adulthood. Hence, sustained label expansion neutralizes some of the revenue loss from price pressure, keeping the tumor necrosis factor inhibitors market relevant across various specialties.

By Formulation: Auto-Injector Pens Gain on Adherence Features

Prefilled syringes generated 55.67% of 2025 turnover, primarily because they are the default presentation for originator brands. However, connected auto-injector pens are projected to record a 5.76% CAGR, doubling the growth rate of syringes, as payers increasingly value real-time adherence data. The tumor necrosis factor inhibitors market size for digital-enabled pens is projected to double by 2031, reflecting both new patient starts and conversion from manual devices. IoT functionality, haptic cues, and injection-log transmission support medication-possession ratios above 80%, reducing flare-related costs for insurers.

Hospitals still rely on lyophilized vials for infliximab infusions, but the launch of subcutaneous infliximab in Europe signals a migration toward self-administration even for traditionally intravenous molecules. Manufacturers choosing between developing proprietary pens and licensing proven platforms often opt for the latter to accelerate their speed-to-market. Over time, connectivity will become a table-stakes requirement, and legacy syringes risk being delisted from formularies that rank devices by adherence performance.

By End User: Online Pharmacies Leverage Cold-Chain Advances

Hospital pharmacies accounted for 52.65% of the 2025 value, bolstered by infusion services and initiation protocols that require observation. Specialty pharmacies manage the bulk of subcutaneous dispensing, but online platforms are emerging as the fastest-growing channel, with a 6.76% CAGR. IoT sensors embedded in packaging now keep excursion rates below 2%, assuaging payer and regulator concerns about biologic stability during home delivery. The tumor necrosis factor inhibitors market, therefore, witnesses a gradual shift toward click-to-ship fulfillment, especially in urban centers in the U.S. and Europe, where next-day delivery is reliable.

Regulatory requirements for pharmacist counseling continue to limit e-pharmacy penetration in Japan and certain parts of the European Union. Yet integrated telehealth models—which combine virtual consults, remote monitoring, and doorstep delivery—illustrate a path to compliance. Cold-chain logistics providers that guarantee lane-level temperature integrity stand to win exclusive contracts, reinforcing the strategic link between distribution competence and prescription capture.

Geography Analysis

North America dominated spending with a 42.65% share in 2025, driven by Medicare policy that mandates the inclusion of biosimilars and caps co-pays, thereby directly stimulating volume. Private insurers widened the gap by excluding branded Humira from formularies, accelerating biosimilar uptake, and illustrating how payer policy overrides nominal list-price cuts. The tumor necrosis factor inhibitors market is shifting toward lower-cost options, even as total prescriptions increase, reflecting demographic realities and the broad clinical applicability of these treatments.

Europe follows as the second-largest region, where national tender systems drive aggressive price competition, resulting in infliximab biosimilar penetration exceeding 90% in several Scandinavian countries. Germany and France deploy value-based contracts that lock in multi-year supply at predetermined discounts, ensuring price stability while safeguarding continuity of care. The region also leads in the adoption of subcutaneous infliximab, thereby easing hospital burdens and creating additional room for home-based care models.

The Asia-Pacific region is forecast to post a 4.56% CAGR through 2031 as Samsung Bioepis and Celltrion scale their regional manufacturing capacity and secure approvals in China, India, and Japan, without having to clear the interchangeability hurdles that slow U.S. penetration. Local production lowers landed cost, allowing more aggressive tender bids. Emerging economies in Southeast Asia, however, remain constrained by fragmented reimbursement systems and uneven cold-chain infrastructure. Tiered pricing and public-private manufacturing deals will be critical to unlocking latent demand.

The Middle East, Africa, and South America collectively trail due to affordability limits, high out-of-pocket costs, and weak distribution networks, keeping utilization confined mainly to urban private hospitals. Biosimilar discounts alone have not closed the access gap. Strategic partnerships with domestic pharmaceutical companies and regional logistics providers could help narrow disparities, but political and currency risks temper investment enthusiasm.

Competitive Landscape

The tumor necrosis factor inhibitors market exhibits moderate concentration, with AbbVie, Amgen, Johnson & Johnson, and Pfizer collectively controlling approximately 60% of the market revenue in 2025. AbbVie reported a 36% year-over-year decline in Humira sales to USD 2.8 billion in Q3 2024, yet offset the decline with Skyrizi and Rinvoq, indicating a pivot to the IL-23 and JAK pipelines. Amgen leads the adalimumab biosimilar wave with Amjevita, leveraging early-mover advantage, while Johnson & Johnson’s Remicade yields share in Europe under tender pressure.

Samsung Bioepis and Celltrion leverage cost advantages from South Korean biomanufacturing clusters, underpricing Western originators by up to 30% in the Asia-Pacific region and expanding aggressively into Europe through partnerships with local distributors. Indian entrants Cadila and Lupin received domestic approvals in 2025 and aim to serve the Middle East and African markets, where Western companies remain underrepresented. Success will hinge on demonstrating quality equivalence and securing cold-chain integrity across challenging geographies.

Technology is playing an increasingly important role in differentiation. Ypsomed’s Bluetooth-enabled pens, adopted by multiple biosimilar licensees, set a de facto standard for digital adherence, while AbbVie explores proprietary connected devices to retain brand stickiness amid price erosion. Patent filings in 2025 reveal work on extended-interval TNF inhibitors designed for quarterly dosing, which, if successful, could reset the competitive field by 2032. Until then, scale manufacturing, tender acumen, and device integration drive success.

Tumor Necrosis Factor Inhibitors Industry Leaders

Pfizer Inc

Johnson & Johnson

Amgen Inc.

AbbVie Inc

UCB SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: TNF Pharmaceuticals, Inc. announced a key safety milestone for its TNF-α inhibitor drug, isomyosamine. The company completed an FDA-recommended 13-week safety study, showing no adverse issues at any dose level. This achievement supports the further extension of clinical trials for multiple autoimmune and inflammatory conditions.

- October 2025: Celltrion received FDA approval for AVTOZMA (tocilizumab-anoh) IV, a biosimilar to Actemra, in the United States for the treatment of autoimmune conditions. This marks Celltrion’s fifth immunology biologic and seventh biosimilar approved by the FDA. The launch expands Celltrion’s immunology portfolio to include an IL-6 inhibitor, targeting multiple inflammatory pathways.

- October 2025: AbbVie announced positive topline results from the Phase 3b/4 SELECT-SWITCH study, showing that upadacitinib 15 mg daily is effective and safe compared to adalimumab in adults with moderate to severe rheumatoid arthritis on methotrexate who didn't respond well to other TNF inhibitors. The study met its primary and secondary endpoints at week 12, with no new safety concerns. This highlights upadacitinib's potential as an alternative treatment option for RA patients.

Global Tumor Necrosis Factor Inhibitors Market Report Scope

As per the scope of the report, tumor necrosis factor (TNF) Inhibitors are a class of biologic drugs that block the activity of TNF, a pro-inflammatory cytokine involved in immune responses. They are primarily used to treat autoimmune diseases such as rheumatoid arthritis, Crohn's disease, and psoriasis. By reducing inflammation, TNF inhibitors help manage symptoms and slow the progression of the disease.

The Tumor Necrosis Factor Inhibitors Market is Segmented by Drug Class (Adalimumab, Etanercept, Infliximab, Golimumab, Certolizumab Pegol, TNF-Inhibitor Biosimilars, and Other Drug Classes), Indication (Rheumatoid Arthritis, Psoriatic Arthritis, Ankylosing Spondylitis, Crohn's Disease, Ulcerative Colitis, Psoriasis, Hidradenitis Suppurativa, and Other Indications), Formulation (Prefilled Syringe, Auto-Injector Pen, and Lyophilized Powder/Vial), End-user (Hospital Pharmacies, Specialty Pharmacies, Retail Pharmacies, and Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Adalimumab |

| Etanercept |

| Infliximab |

| Golimumab |

| Certolizumab Pegol |

| TNF-Inhibitor Biosimilars |

| Other Drug Classes |

| Rheumatoid Arthritis |

| Psoriatic Arthritis |

| Ankylosing Spondylitis |

| Crohn's Disease |

| Ulcerative Colitis |

| Psoriasis |

| Hidradenitis Suppurativa |

| Other Indications |

| Prefilled Syringe |

| Auto-Injector Pen |

| Lyophilized Powder / Vial |

| Hospital Pharmacies |

| Specialty Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East And Africa | GCC |

| South Africa | |

| Rest Of Middle East And Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Drug Class | Adalimumab | |

| Etanercept | ||

| Infliximab | ||

| Golimumab | ||

| Certolizumab Pegol | ||

| TNF-Inhibitor Biosimilars | ||

| Other Drug Classes | ||

| By Indication | Rheumatoid Arthritis | |

| Psoriatic Arthritis | ||

| Ankylosing Spondylitis | ||

| Crohn's Disease | ||

| Ulcerative Colitis | ||

| Psoriasis | ||

| Hidradenitis Suppurativa | ||

| Other Indications | ||

| By Formulation | Prefilled Syringe | |

| Auto-Injector Pen | ||

| Lyophilized Powder / Vial | ||

| By End-user | Hospital Pharmacies | |

| Specialty Pharmacies | ||

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | GCC | |

| South Africa | ||

| Rest Of Middle East And Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the tumor necrosis factor inhibitors market in 2026?

The market is valued at USD 42.57 billion in 2026 and is forecast to reach USD 50.77 billion by 2031.

Which drug class leads current revenue?

Adalimumab remains the largest contributor, representing 42.45% of 2025 sales.

Which indication is growing fastest?

Ulcerative colitis is expanding at a 6.89% CAGR through 2031, outpacing other indications.

Why are auto-injector pens gaining share?

Connected pens improve adherence and reduce flare-related costs, prompting payers to favor them over prefilled syringes.

What policy change is accelerating U.S. biosimilar uptake?

Medicare Part D now mandates at least one biosimilar per reference biologic and caps certain co-pays, encouraging wider usage.

Which region offers the highest growth potential to 2031?

Asia-Pacific is projected to grow at a 4.56% CAGR, driven by local manufacturing scale-up and expanding regulatory approvals.

Page last updated on: