Tire Retreading Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.87 Billion |

| Market Size (2031) | USD 10.39 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

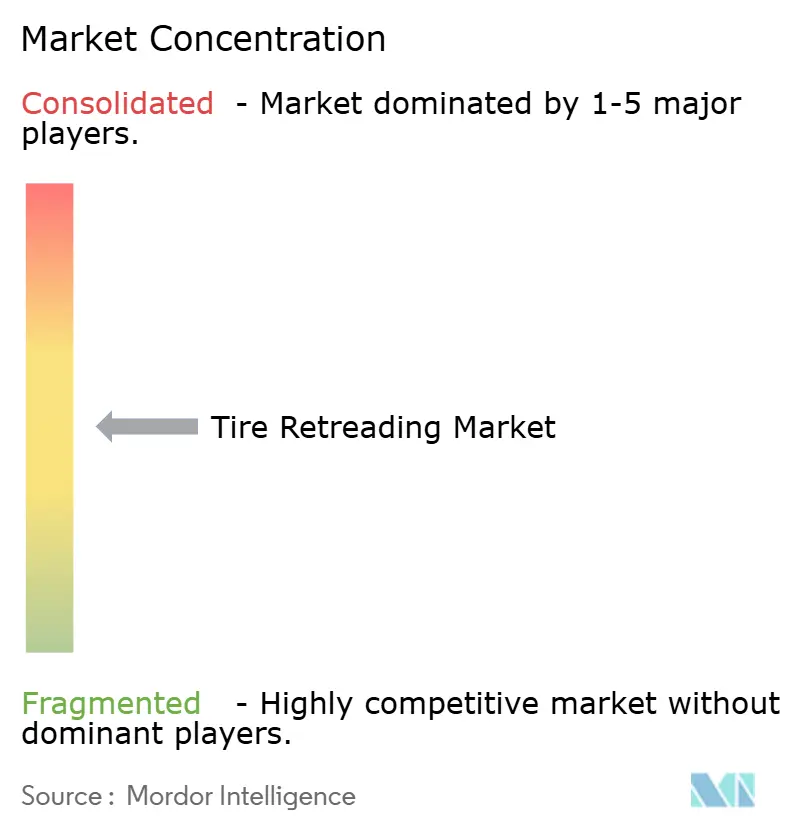

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tire Retreading Market Analysis by Mordor Intelligence

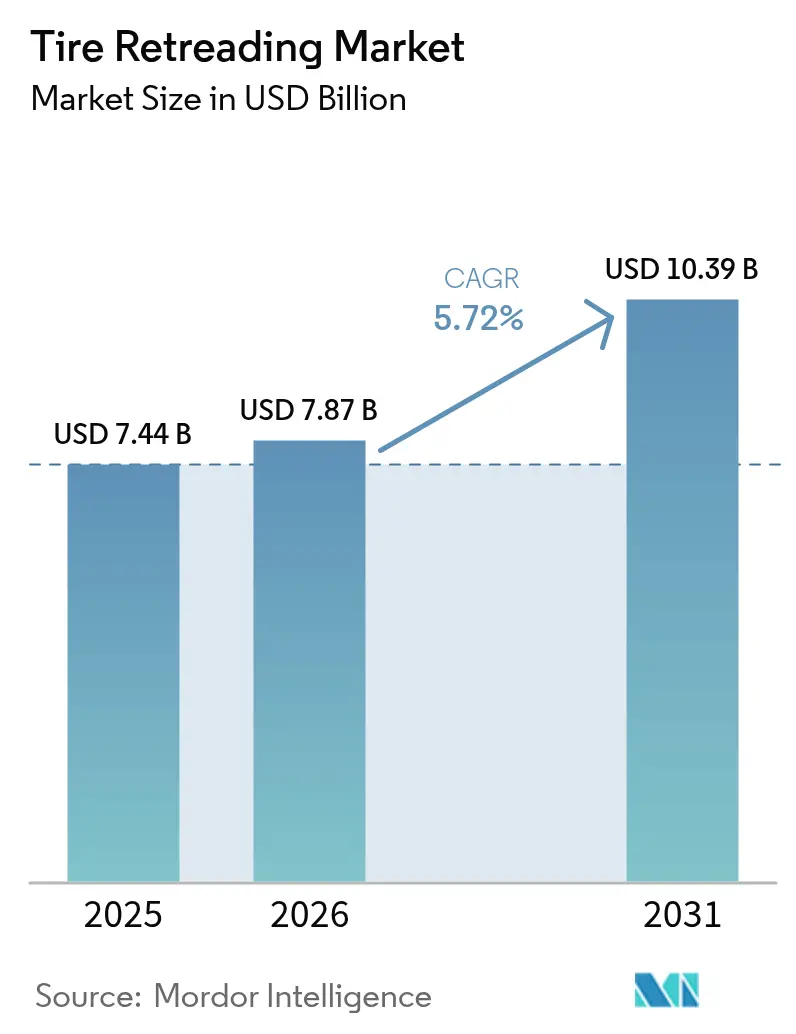

The Tire Retreading Market size was valued at USD 7.44 billion in 2025 and estimated to grow from USD 7.87 billion in 2026 to reach USD 10.39 billion by 2031, at a CAGR of 5.72% during the forecast period (2026-2031). Driven by rising raw-material prices, ongoing carbon-reduction targets, and the imperative to maximize truck uptime, the momentum in the retreading industry continues. Retreaded casings offer significant cost savings and achieve notable reductions in carbon emissions and energy consumption, underscoring their dual economic and environmental advantages. The Asia-Pacific region commands the largest share of the market, thanks to China's expansive heavy-duty fleet and India's rapidly expanding logistics networks. In contrast, the Middle East & Africa emerge as the region with the most robust growth, driven by heightened off-road tire usage spurred by booming mining and infrastructure projects. Furthermore, advancements like RFID tracking, automated inspection lines, and predictive maintenance analytics are evolving from a mere cost-saving measure to a pivotal, data-centric service integral to comprehensive fleet contracts.

Key Report Takeaways

- By vehicle type, medium and heavy-duty trucks led with 45.02% of the tire retreading market share in 2025, whereas off-the-road and mining tires are forecast to accelerate at a 5.96% CAGR through 2031.

- By production method, the pre-cure process controlled 60.95% of the tire retreading market size in 2025, while mold-cure technology is expanding at a 5.88% CAGR between 2026 and 2031.

- By tire type, radial construction dominated with 73.05% of the tire retreading market share in 2025, whereas solid and foam-filled variants are projected to expand at a 6.04% CAGR through 2031

- By sales channel, independent retreaders commanded 57.22% of the tire retreading market size in 2025, whereas OEM and captive fleet facilities are progressing at a 5.93% CAGR to 2031.

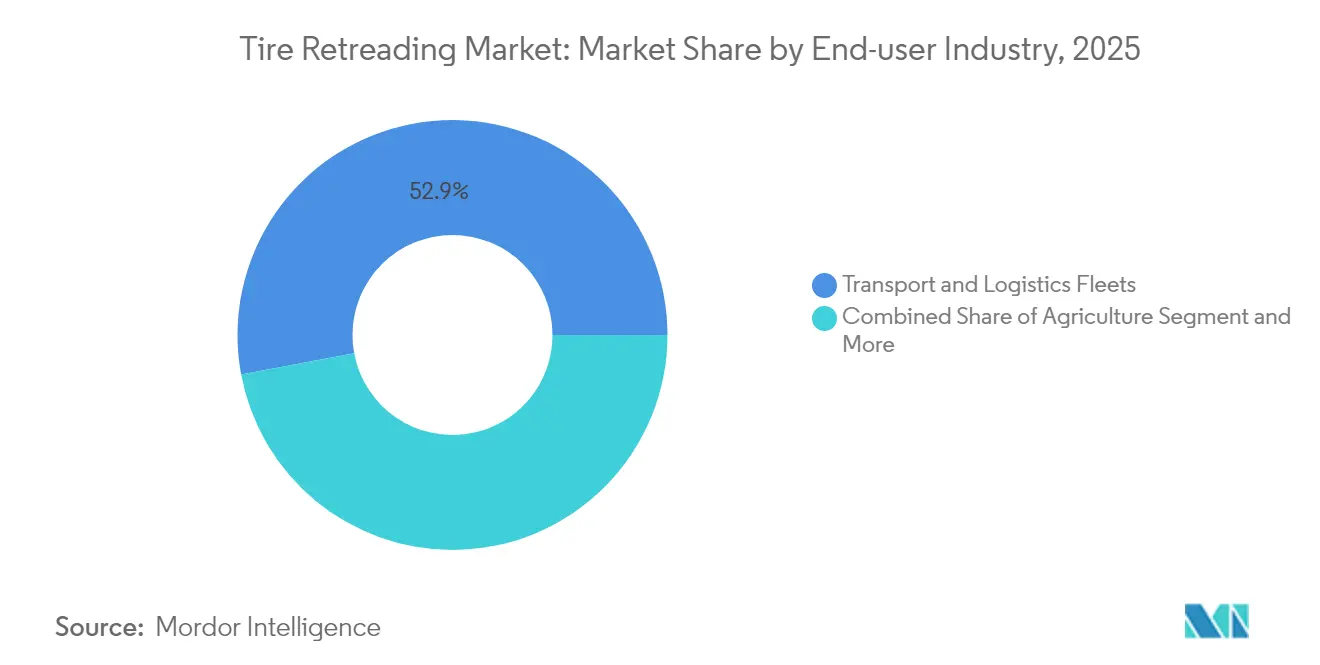

- By end-user industry, transport and logistics fleets accounted for 52.94% of 2025 revenue, while aviation is forecast to post the highest 6.01% CAGR to 2031.

- By application, on-road service held 67.41% revenue share in 2025; off-road use is expected to grow at a 6.02% CAGR between 2026 and 2031.

- By geography, Asia-Pacific captured a 38.51% revenue share in 2025, but the Middle East and Africa are set to grow the fastest, at a 6.06% CAGR during the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tire Retreading Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-Savings Over New Tires | +1.8% | Global, strongest in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Stricter Circular-Economy | +1.2% | EU core, expanding to North America and Asia Pacific | Medium term (2-4 years) |

| Fleet-Mileage Growth | +1.1% | Global, concentrated in urban centers | Medium term (2-4 years) |

| Government Tax-Credit Schemes | +0.7% | North America, select EU markets | Short term (≤ 2 years) |

| RFID-Enabled Lifecycle Tracking | +0.6% | North America and EU early adoption | Long term (≥ 4 years) |

| Green Procurement Policies | +0.5% | Global, led by multinational logistics companies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-savings Over New Tires

Commercial operators now embed retreading in annual budget planning because a single retread delivers two-fifths purchase-price relief versus a comparable new tire. That differential widens as synthetic rubber and petroleum costs trend upward, reinforcing retreading’s payback in high-utilization fleets such as long-haul trucking and express-parcel delivery. China’s heavy-duty sector, which logged almost 300,000 truck sales in the first half of 2025, epitomizes this cost calculus, while airlines stretch aviation-tire service life across multiple cycles to preserve thin operating margins [1]“2025 Heavy-Duty Truck Sales Report,” SINOTRUK, sinotruk.com.

Stricter Circular-Economy & CO₂ Regulations

EU Circular Economy Action Plan rules oblige transport operators to prioritize reuse over disposal, turning tire retreading into a compliance tool rather than a discretionary measure. Euro 7 emission thresholds reinforce the mandate by penalizing premature tire replacement, and similar stimuli surface in North America and key Asia-Pacific economies. Environmental math is straightforward: every retread slashes carbon output by 30% and energy inputs by 70%, metrics that help carriers meet Scope 3 reporting targets [2]“Euro 7 Emission Standards,” European Commission, europa.eu .

Fleet-Mileage Growth From E-Commerce Logistics

B2C parcel volumes keep city trucks in near-constant duty cycles marked by dense stop-and-go routes that accelerate tread wear. Asia-Pacific, already the world’s largest e-commerce arena, amplifies this mileage surge and positions retreading as the default cost-containment lever for last-mile operators. Providers that can adjust curing patterns for smaller rim diameters and mixed-service tread designs are winning share within this logistics niche.

Government Tax-Credit Schemes For Domestic Retreads

Proposed U.S. federal credits and Canada’s retention of accelerated depreciation for retread equipment reduce the total cost of ownership gap between retread and new alternatives. Several EU states also reimburse up to one-fifth of qualifying retread capital spending, incentivizing fleets to channel tire budgets toward local plants and reinforcing the security of domestic supply [3]“Tire Retread Facilities Survey 2024,” Government of Canada, canada.ca .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Casing and Rubber Prices | -1.4% | Global, most acute in import-dependent regions | Short term (≤ 2 years) |

| Influx Of Ultra-Low-Cost Import Tires | -0.9% | North America and EU primary impact | Medium term (2-4 years) |

| Passenger-Car Safety Perception Gaps | -0.8% | Global, strongest in developed markets | Long term (≥ 4 years) |

| Limited EV-Ready Retread Designs | -0.6% | North America and EU early adoption markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Casing & Rubber Prices

Sudden swings in natural-rubber benchmarks and petroleum-linked synthetic rubber costs erode profit margins and complicate pricing grids for retread shops. Smaller independents often lack forward-buying capacity, exposing them to spot-market shocks that compress gross margin or force price hikes that narrow retread’s cost edge against new imports. When raw material prices pull back, new-tire discounts can temporarily curb retread demand until equilibrium reasserts.

Influx Of Ultra-Low-Cost Import Tires

Budget-tier imports from newer Asian producers challenge retread economics, particularly in the passenger and light-truck categories. These tires undercut domestic retread price points, prompting fleets to weigh immediate savings against shorter service life and uncertain warranty. Quality audits and anti-dumping tariffs mitigate some pressure, yet the price gap remains a recurring headwind in North America and parts of the EU.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Dominance Drives Growth

Medium and heavy-duty trucks generated 45.02% of 2025 revenue, confirming that high-mileage cycles make retreading indispensable for line-haul and regional-haul carriers. This segment will continue anchoring the tire retreading market through 2031 as freight demand remains resilient. Off-the-road and mining tires are charted for a 5.96% CAGR, riding on mineral extraction activity in Africa and South America, where specialized casings cost multiples of on-road equivalents. With its 4-10 approved retread cycles, the aviation niche reveals how rigorous safety oversight can coexist with aggressive cost management, forecasting a robust CAGR that outpaces most ground-based segments.

Passenger car retreading remains marginal in Europe and North America amid safety perceptions but maintains footholds in Latin America and Asia, where regulatory barriers are lower. Light commercial vans, pivotal in e-commerce logistics, now adopt shorter retread cycles adjusted to urban stop frequency. Emerging double-articulated rigs in Japan require retread designs capable of handling higher axle loads, a technical capability that only the most advanced independent retreaders currently offer.

By Production Method: Pre-cure Maintains Leadership

The pre-cure process held 60.95% of global revenue in 2025 and remains the go-to for high-volume truck casings. Its competitive advantage stems from lower per-unit cost and faster throughput. Mold-cure is gaining a 5.88% CAGR owing to improved precision heating and automated presses that shorten cycle times while allowing bespoke tread patterns. Automation, from AI-based surface inspection to collaborative robotic handlers, props up both methods by standardizing quality and trimming labor input. However, capitalization requirements could accelerate industry consolidation as smaller shops struggle to fund upgrades.

The tire retreading market size attributed to mold-cure lines is projected to increase as fleet demand for custom patterns grows. Yet, pre-cure’s simplicity and lower energy load keep it the preferred method for cost-sensitive fleets. OEM-integrated retread plants hedge their bets by running hybrid facilities that switch methods based on order mix and casing availability.

By Tire Type: Radial Construction Dominates

Radial casings accounted for 73.05% of 2025 revenue because their steel-belted architecture offers superior heat dispersion and fuel economy. Solid and foam-filled variants, while still niche, will post a 6.04% CAGR through 2031 as warehouses and construction sites seek puncture-proof options that curb downtime. Increased axle weights on battery-electric trucks are ushering in next-gen radial sidewalls and bead packages engineered to withstand higher torque loads without compromising retreadability. Bias-ply remains viable only in specialized off-road settings where sidewall stiffness trumps fuel efficiency.

As sustainability metrics penetrate procurement scorecards, fleet managers evaluate whether new radial designs can realize two retread lives instead of one, amplifying total-cost-of-ownership benefits. Manufacturers respond by optimizing compound formulations for repeated curing cycles without sacrificing baseline performance standards.

By Sales Channel: Independent Retreaders Lead

Independent operators served 57.22% of global customers in 2025, leveraging proximity to fleets and flexible casing stock to deliver fast turnaround. Yet OEM-linked and captive fleet facilities, growing at 5.93% CAGR, are compressing this lead through bundled tire-service contracts that guarantee warranty coverage and data integration across the vehicle lifecycle. Large logistics providers now negotiate framework agreements stipulating minimum retread volumes that often favor OEM plants capable of digital tracking from original fitment through the final retread.

To stay competitive, independents deploy cloud-based CRM systems and subscription maintenance dashboards that mimic the digital experience offered by multinationals. Franchise alliances are also emerging, letting smaller shops share procurement clout and technology investments while preserving local brand equity.

By End-user Industry: Transport Fleets Drive Demand

Transport and logistics operators generated 52.94% of 2025 sales, reflecting route density and mileage rates that perfectly fit retreading economics. Aviation’s 6.01% CAGR shows how strict safety compliance aligns with multi-cycle tire management when full traceability is embedded. Mining and construction fleets, burdened by abrasive terrains and high casing prices, remain dependable buyers as retreading often halves per-hour tire costs.

Agricultural usage ebbs and flows with planting seasons; yet demand for flotation tires that minimize soil compaction is nudging retread shops to invest in wider curing envelopes. With predictable daily routes, waste management fleets continue to embed retreading in three-year tire contracts that fix operating costs amid volatile commodity prices.

By Application: On-road Dominates

On-road applications delivered 67.41% of 2025 revenue, a function of highway freight prevalence and established inspection standards safeguarding safety perceptions. Off-road, slated for a 6.02% CAGR, is buoyed by mining equipment operating in remote sites where supply-chain delays make new tire lead times untenable. Urban transit buses also lean on retreading, where predictable depot schedules dovetail with retread turnaround times.

Specialty sectors such as oversized load haulage demand bespoke tread patterns and reinforced shoulders that mold-cure lines are best suited to provide. Under stringent regulation, hazardous-material carriers increasingly specify RFID-enabled casings to prove maintenance compliance, a service capability that only technologically equipped retreaters can meet.

Geography Analysis

Asia-Pacific commanded 38.51% revenue in 2025, due to China’s gigantic truck fleet and India’s infrastructure push that multiplies highway ton-kilometers. Government policies emphasizing circular-economy compliance, such as China’s Large-scale Equipment Renewal Action Plan, channel fleets toward retreading while they phase into new-energy vehicles. Japan’s emphasis on total-life cost modeling translates into sophisticated demand for retread services that plug directly into predictive maintenance dashboards.

Middle East & Africa, the fastest-advancing region at 6.06% CAGR, gains from energy and mineral projects that lift off-road tire usage in deserts and open-pit mines. Saudi Arabia’s ban on retread imports, combined with incentives for domestic production, shields local plants from foreign price shocks. South Africa and Botswana mining corridors underpin steady demand, although logistical constraints require mobile inspection units and on-site buffing rigs to curtail equipment downtime.

North America remains a mature yet tech-progressive territory where RFID programs and government incentives foster plant modernization. Canada hosts multiple dedicated retread facilities focused mainly on truck casings, and proposed U.S. credits would boost domestic volumes if passed into law. Europe blends regulatory tailwinds, Euro 7 and waste-framework directives, with competitive headwinds from low-priced imports, prompting retreaters to invest in automated stereography and robotics to achieve cost and quality leadership.

Competitive Landscape

The tire retreading market features a moderate concentration where top global brands hold scale advantages, but regional independents sustain strong footholds. Bridgestone’s commitment to expand its Warren County plant illustrates the tire-maker's bets on vertically integrated retread programs that lock customers into cradle-to-grave service loops. Goodyear is deploying a vast amount to automate its Oklahoma site, including AI inspection that trims cycle time while guaranteeing traceability for fleet warranties. Michelin threads RFID data from the original tire built through each retread pass, folding analytics into fleet dashboards that predict optimum pull-points and extend casing life.

Technology vendors are disrupting the space with AI vision systems that scan, causing anomalies in seconds, reducing scrap rates, and unlocking higher plant throughput. Yokohama’s acquisition of Goodyear’s off-the-road tire unit arms it with mining-grade casings that are routinely retreaded, securing a quicker entry into heavy-equipment segments. Continental’s Thailand expansion melds new-tire and retread production under one roof, shortening logistics chains for Asia-Pacific fleets.

Smaller independents retain local market share by offering fast turnaround, personalized service, and multi-brand casing pools. Still, many face capital hurdles to match their larger rivals' automation and data services. Franchise networks and regional alliances are emerging as survival strategies that preserve independent ownership while enabling shared investments in robotics, stereography, and ERP platforms.

Tire Retreading Industry Leaders

Bridgestone Corporation

Goodyear Tire and Rubber Company

Marangoni S.p.A.

Southern Tire Mart

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Goodyear committed USD 320 million to Oklahoma facility modernization, incorporating automated retreading systems and RFID integration capabilities for enhanced fleet service offerings.

- February 2025: Yokohama Rubber acquired Goodyear’s off-the-road tire business for USD 905 million, significantly expanding its mining and construction tire portfolio while adding retreading capabilities for specialized applications.

- October 2024: Continental invested USD 315 million in Thailand facility expansion, enhancing production capacity for both new tires and retreading operations to serve Asia-Pacific commercial vehicle markets.

Global Tire Retreading Market Report Scope

Tire retreading is a remanufacturing process to replace the worn tread on used tires with new treads to help extend the life of the tire.

The tire retreading market is segmented into vehicle type, production method, sales channel, tire type, and geography. By vehicle type, the market is divided into passenger cars, light commercial vehicles, medium and heavy-duty trucks, and buses. By production method, the market is categorized into pre-cure and mold cure methods. By sales channel, the market is segmented into OEMs and independent retreaders. By tire type, the market is classified into radial, bias, and solid tires. Geographically, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World.

For each segment, the market sizing and forecasts have been done based on the value (USD).

| Passenger Car |

| Light Commercial Vehicle |

| Medium & Heavy-Duty Truck |

| Bus & Coach |

| Off-the-Road & Mining |

| Agriculture & Specialty |

| Pre-cure |

| Mold-cure |

| Radial |

| Bias |

| Solid / Foam-filled |

| Independent Retreaders |

| OEM / Captive Fleet Facilities |

| Transport & Logistics Fleets |

| Construction & Mining |

| Agriculture |

| Aviation |

| Military & Defense |

| Waste Management & Others |

| On-road |

| Off-road |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Car | |

| Light Commercial Vehicle | ||

| Medium & Heavy-Duty Truck | ||

| Bus & Coach | ||

| Off-the-Road & Mining | ||

| Agriculture & Specialty | ||

| By Production Method | Pre-cure | |

| Mold-cure | ||

| By Tire Type | Radial | |

| Bias | ||

| Solid / Foam-filled | ||

| By Sales Channel | Independent Retreaders | |

| OEM / Captive Fleet Facilities | ||

| By End-user Industry | Transport & Logistics Fleets | |

| Construction & Mining | ||

| Agriculture | ||

| Aviation | ||

| Military & Defense | ||

| Waste Management & Others | ||

| By Application | On-road | |

| Off-road | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the tire retreading market in 2026?

The tire retreading market size is USD 7.87 billion in 2026.

What is the expected growth rate for tire retreading to 2031?

Market revenue is forecast to expand at a 5.72% CAGR through 2031.

Which region leads global sales?

Asia-Pacific captured 38.51% of 2025 revenue, the highest regional share.

Why do fleets prefer tire retreading over new tires?

Retreading cuts purchase costs by two-fifth and lowers carbon emissions by one-third, offering economic and environmental gains.

Which production method dominates global retreading?

The pre-cure method held 60.95% of 2025 sales thanks to cost efficiency and high throughput.

What technology trends are reshaping the sector?

RFID-enabled lifecycle tracking and AI-based casing inspection are moving toward predictive maintenance and full traceability.

Page last updated on: