Neurovascular Thrombectomy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

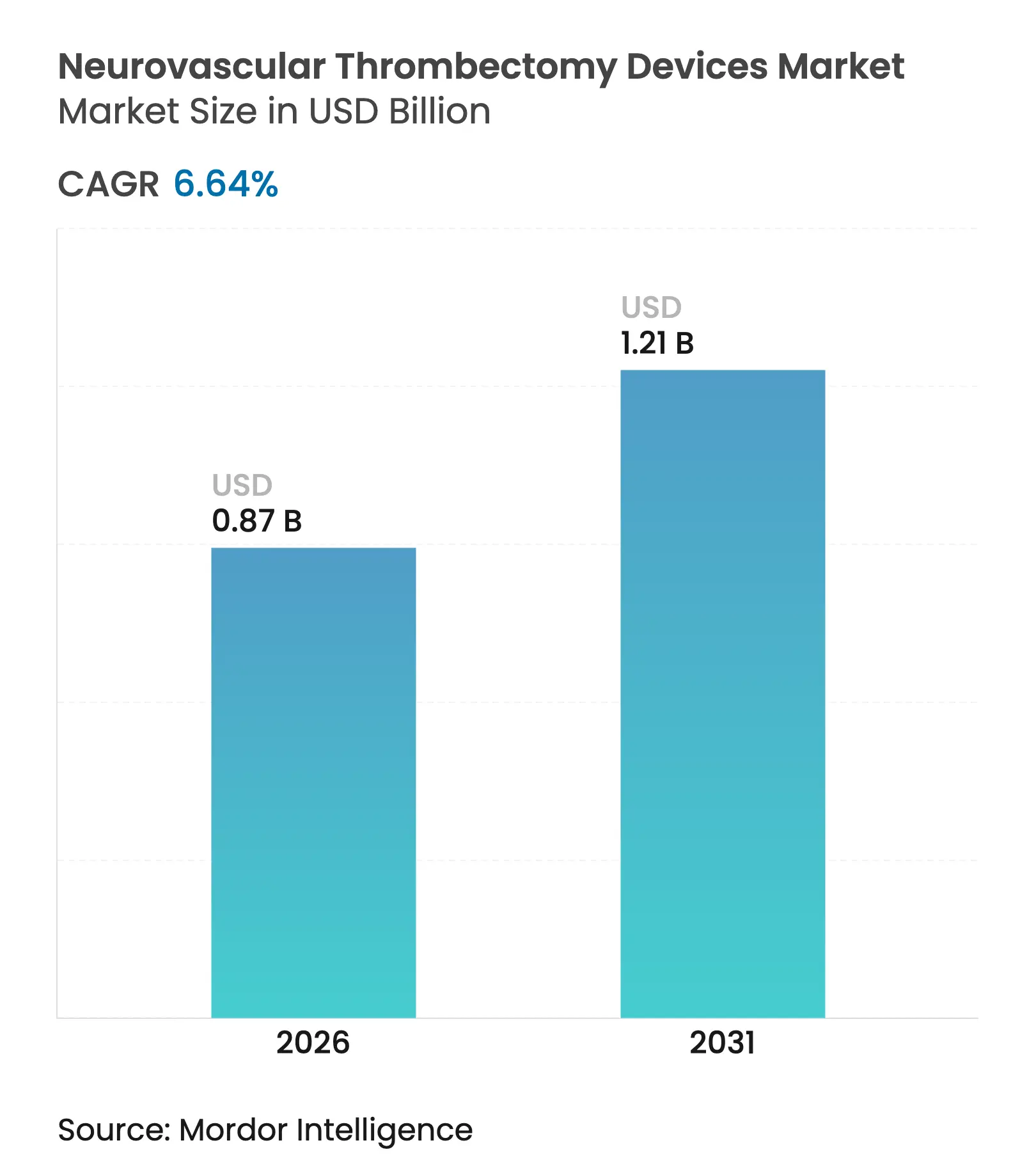

| Market Size (2026) | USD 0.87 Billion |

| Market Size (2031) | USD 1.21 Billion |

| Growth Rate (2026 - 2031) | 6.64 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Neurovascular Thrombectomy Devices Market Analysis by Mordor Intelligence

Neurovascular thrombectomy devices market size in 2026 is estimated at USD 0.87 billion, growing from 2025 value of USD 0.82 billion with 2031 projections showing USD 1.21 billion, growing at 6.64% CAGR over 2026-2031. Demand accelerates as the procedure shifts from a niche intervention to routine frontline therapy, a change sparked by clinical evidence that widened the treatment window to 24 hours after stroke onset[1]Source: American Journal of Neuroradiology, “Extended‐Window Thrombectomy Outcomes,” ajnr.org . Stroke programs now send eligible patients directly from imaging to the angiography suite, trimming door-to-puncture times and raising device utilization. Stent retrievers still account for more than half of revenue, yet large-bore aspiration catheters are growing fastest as physicians prioritize higher first-pass recanalization rates. Tertiary-care hospitals perform most procedures while ambulatory surgical centers log the quickest volume gains, even as supply-chain cost pressures and a shortage of neuro-interventional specialists weigh on smaller manufacturers.

Key Report Takeaways

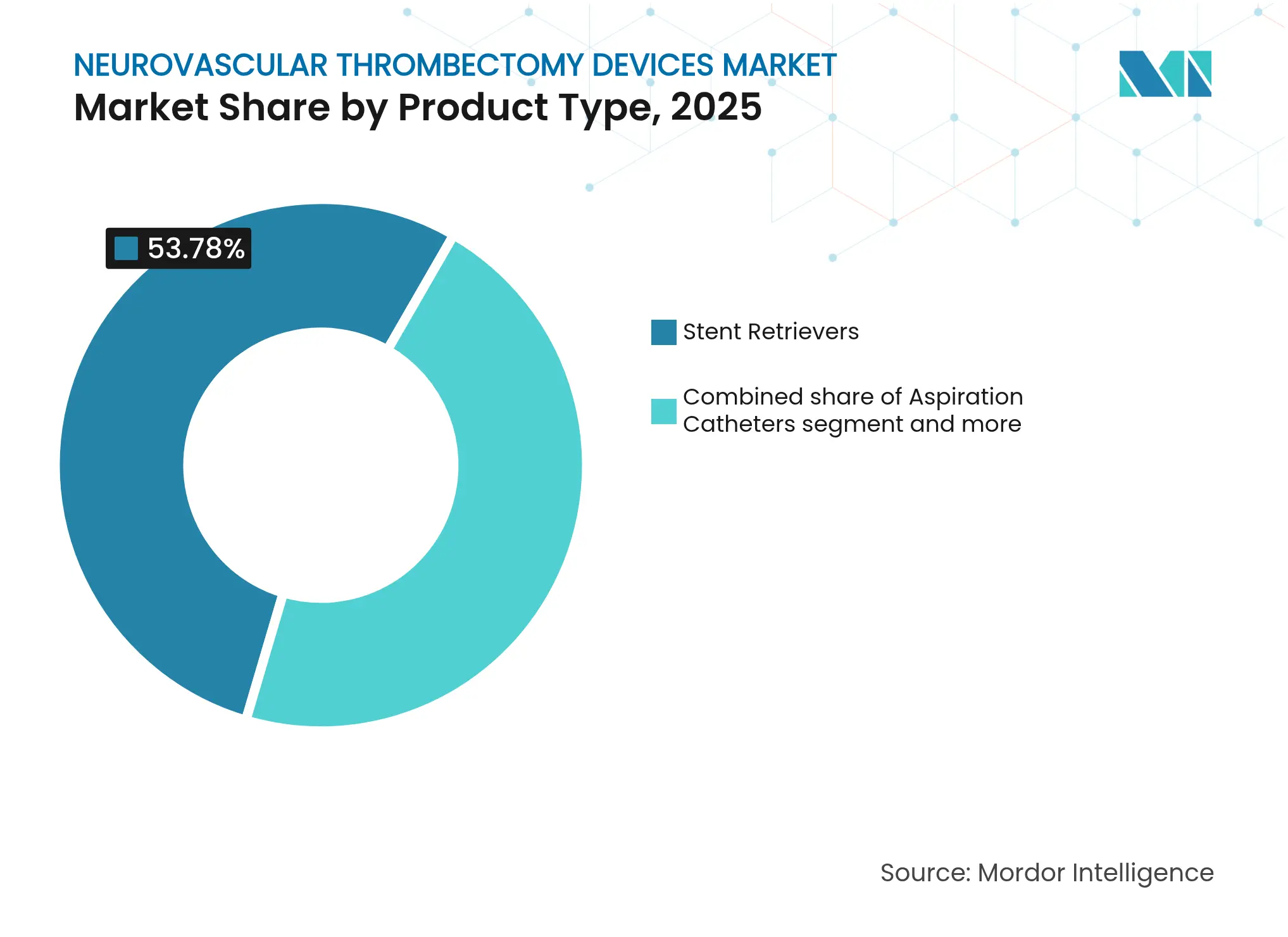

- By product type, stent retrievers led with 53.78% neurovascular thrombectomy devices market share in 2025, whereas large-bore aspiration catheters are forecast to expand at 7.08% CAGR to 2031.

- By end user, tertiary-care hospitals held 61.45% share of the neurovascular thrombectomy devices market size in 2025, while ASCs register the fastest 7.62% CAGR through 2031.

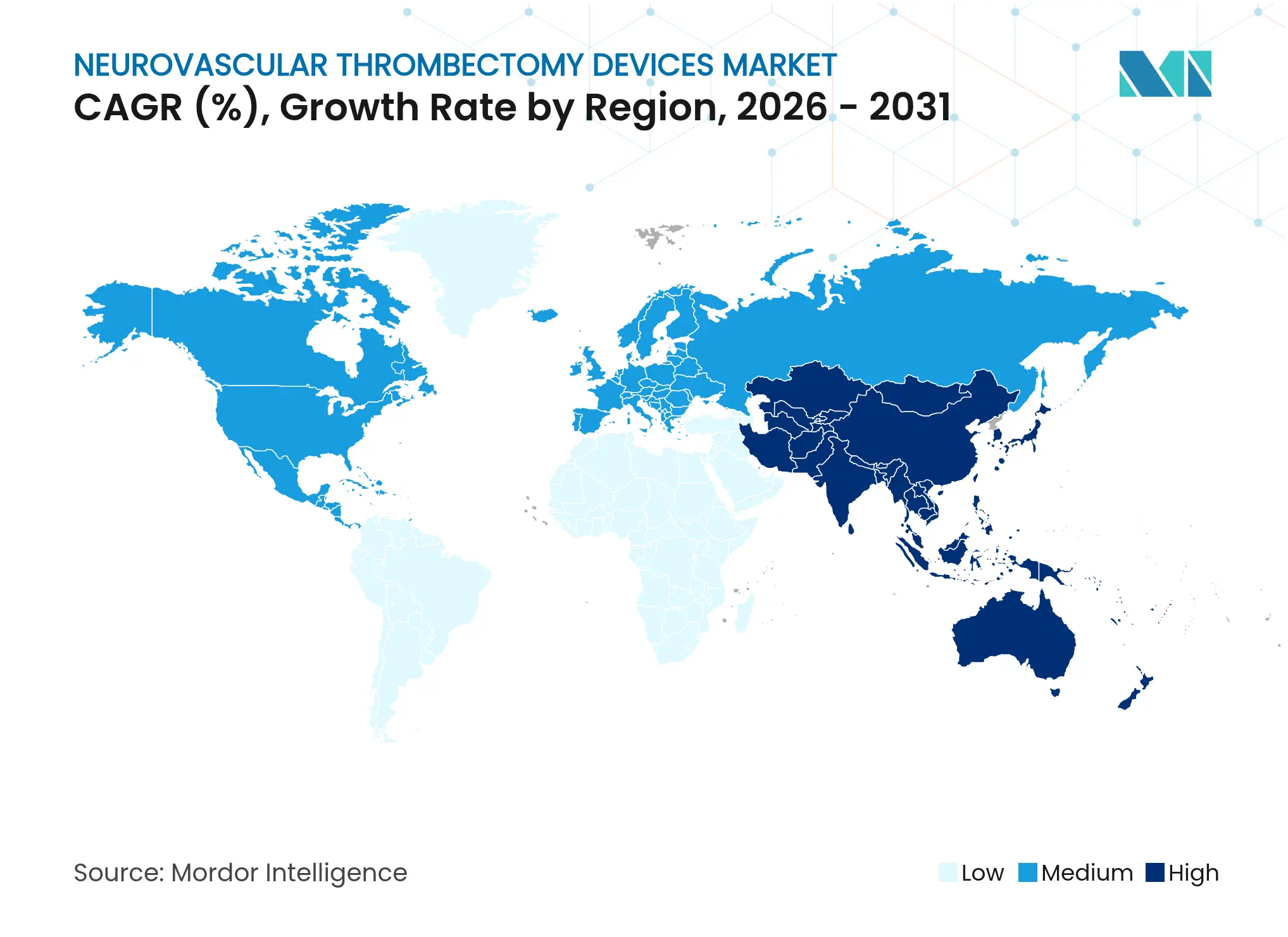

- By geography, North America captured 38.12% revenue share in 2025; Asia-Pacific is projected to grow at 8.11% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neurovascular Thrombectomy Devices Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin | |||

|---|---|---|---|---|---|---|

The global pipeline of biologics and biosimilars is expanding rapidly. The global pipeline of biologics and biosimilars is expanding rapidly. | +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Global, with concentration in North America & Europe | Impact Timelin:Medium term (2-4 years) |

Rapid growth of cell & gene therapy outsourcing Rapid growth of cell & gene therapy outsourcing | +1.5% | North America & EU, expanding to APAC | Long term (≥ 4 years) | |||

Rising cost & complexity of late-phase clinical trials Rising cost & complexity of late-phase clinical trials | +1.2% | Global, particularly North America & Europe | Short term (≤ 2 years) | |||

Capacity crunch in high-potency fill-finish suites (HPAPI, ADC) Capacity crunch in high-potency fill-finish suites (HPAPI, ADC) | +1.0% | North America & Europe, emerging in APAC | Medium term (2-4 years) | |||

US/EU on-shoring incentives & supply-chain security mandates US/EU on-shoring incentives & supply-chain security mandates | +0.8% | North America & EU, spillover to allied nations | Long term (≥ 4 years) | |||

AI-enabled process optimization lowering CDMO entry barriers AI-enabled process optimization lowering CDMO entry barriers | +0.4% | Global, led by technology-advanced regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Incidence of Acute Ischemic Stroke & Aging Population

Stroke prevalence keeps rising beyond demographic forecasts as lifestyle risk factors intersect with post-COVID vascular sequelae. Individuals aged ≥65 experience stroke rates 2.5 times higher than younger cohorts, driving long-run demand for intervention. Untreated large-vessel occlusion imposes USD 140,000 in lifetime costs per patient, so healthcare payers increasingly prioritize thrombectomy despite the up-front device expense. Cost-effectiveness strengthens when reduced disability and shortened rehabilitation are factored in, cementing a structural growth pillar for the neurovascular thrombectomy devices market. Health systems respond by scaling 24/7 stroke coverage, yet specialist scarcity tempers near-term capacity.

Adoption of Minimally-Invasive Thrombectomy as New Standard of Care

Clinical guidelines upgraded neurovascular thrombectomy to a Class I, Level A recommendation, replacing intravenous thrombolysis as the default for large-vessel occlusion. Contemporary devices achieve 85-90% reperfusion versus 30-40% with thrombolysis alone. Regulators monitor door-to-puncture metrics, prompting hospitals to refine rapid-response protocols. Liability risk for delayed care forces smaller centers to refer patients promptly, reinforcing hub-and-spoke networks and bolstering procedure volumes at comprehensive stroke centers. Device makers benefit from recurring revenue streams as protocols standardize and procedure counts climb.

Expanded Treatment Window Following DAWN/DEFUSE-3 Trials

Late-window thrombectomy quadrupled the treatable population by stretching eligibility to 24 hours when imaging shows salvageable tissue. Rural and underserved areas now qualify through streamlined transfer routes, broadening the neurovascular thrombectomy devices market footprint. The approach depends on advanced CT perfusion or MRI, increasing capital demand for imaging platforms that partner synergistically with thrombectomy devices. Hospitals scramble to maintain around-the-clock on-call teams, amplifying staffing pressures but also boosting case numbers for early-adopting centers.

AI-Based Pre-Hospital Stroke Triage Platforms Boosting Eligible Patient Pool

Artificial-intelligence tools such as Viz.ai and RapidAI detect large-vessel occlusions with ≥90% accuracy in the ambulance, slashing door-to-puncture times by up to 30 minutes. Rapid team activation lets smaller hospitals funnel candidates to thrombectomy-capable hubs, enlarging the potential pool of procedures. Subscription pricing limits budget impact, and accumulating data improve algorithm precision over time, creating virtuous adoption cycles that push forward the neurovascular thrombectomy devices market.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin | |||

|---|---|---|---|---|---|---|

High device cost & reimbursement disparities High device cost & reimbursement disparities | -1.4% | Global, most acute in emerging markets | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:Global, most acute in emerging markets | Impact Timelin:Long term (≥ 4 years) |

Shortage of neuro-interventional specialists, especially in emerging markets Shortage of neuro-interventional specialists, especially in emerging markets | -1.1% | APAC, Latin America, Africa | Medium term (2-4 years) | |||

Device efficacy variability due to clot phenotype heterogeneity Device efficacy variability due to clot phenotype heterogeneity | -0.8% | Global, with higher impact in complex case centers | Medium term (2-4 years) | |||

Nitinol & PEEK supply chain constraints inflating input prices Nitinol & PEEK supply chain constraints inflating input prices | -0.6% | Global, with manufacturing concentration in Asia | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Device Cost & Reimbursement Disparities

A single thrombectomy procedure costs USD 15,000-25,000, with devices accounting for 30-40% of the total[2]Source: Boston Scientific, “2025 Coding & Reimbursement Guide,” bostonscientific.com. Coverage gaps persist in economies where per-capita health spending falls below USD 500, limiting mass adoption despite proven clinical benefit. Value-based payment models scrutinize outcomes to justify reimbursement, pressing manufacturers to offer tiered-pricing structures without compromising innovation investment. The economics become more acute for ASCs that must absorb capital equipment costs while competing on procedural price.

Shortage of Neuro-Interventional Specialists

Roughly 10,000 additional neuro-interventionalists are needed worldwide, with Africa fielding <500 specialists for 1.3 billion people. Training spans 6-8 years, so pipeline expansion cannot meet near-term demand. Tele-mentoring and remote-robotic assistance alleviate gaps but confront licensure and latency hurdles. Consequently, procedure volumes in emerging markets lag potential, holding back the neurovascular thrombectomy devices market despite strong epidemiologic demand.

Segment Analysis

By Product Type: Stent Retrievers Lead Despite Aspiration Surge

Stent retrievers generated USD 441 million in 2025, equivalent to 53.78% of neurovascular thrombectomy devices market size, underlining physician familiarity and extensive clinical data. Yet aspiration catheters are accelerating at 7.08% CAGR as evidence mounts for higher first-pass success, which lowers procedure time and radiation exposure. Physician preference shifts to larger-bore aspiration systems for proximal occlusions, while hybrid platforms aim to capture crossover demand. Accessory sales grow in lockstep with primary devices, providing a stable annuity for suppliers. The competitive pivot toward aspiration reflects the broader transition of the neurovascular thrombectomy devices market toward simplified, high-efficacy solutions.

Second-generation stent retrievers now incorporate higher radial force and radiopaque markers to defend share. Meanwhile, aspiration vendors fine-tune lumen geometry and pump algorithms for stronger, safer suction. Combined systems—integrating retrieval scaffolds with aspiration—move through regulatory dossiers and could reset product leadership if outcomes prove superior. Providers favor suppliers offering full portfolios, enabling tailored clot-specific strategies and reducing inventory complexity.

Note: Segment shares of all individual segments available upon report purchase

By End User: Tertiary Care Leadership With ASC Growth

Tertiary-care hospitals held 61.45% of 2025 revenue, leveraging critical care units, advanced imaging, and 24/7 specialist teams. ASCs, though embryonic in stroke care, register 7.62% CAGR as payers push outpatient settings for stable patients to curb costs. Neuro-catheterization labs within academic centers provide high-throughput environments that elevate trial enrollment and clinician training, reinforcing their strategic role despite higher capital intensity.

ASCs must overcome stringent patient-selection criteria and arrange rapid transfer pathways for complications, yet their lower overhead translates to 30-40% cost savings versus hospital settings. Device makers tailor value propositions by highlighting predictable turnaround times and reduced bed-stay expenses—factors that resonate in outcome-based reimbursement models. The net effect propels diversified channel growth within the neurovascular thrombectomy devices market.

Geography Analysis

North America generated USD 313 million in 2025, equating to 38.12% of the neurovascular thrombectomy devices market revenue. Robust Medicare and private-payer coverage underpin utilization, while FDA breakthrough-device pathways speed next-generation approvals. Comprehensive stroke centers in the United States average door-to-puncture times under 60 minutes, further validating procedural efficacy. Canada maintains universal access yet struggles with rural specialist shortages that lengthen transport intervals and limit late-window eligibility.

Asia-Pacific represents the fastest-expanding region at 8.11% CAGR. China’s stroke-center accreditation policy mandates thrombectomy capability, stimulating widespread installation of biplane angio-suites and neuro-ICUs. India’s private hospital chains add capacity to serve an insured middle class, though public facilities remain resource-constrained. Japan, South Korea, and Australia feature high neuro-interventional density and favorable payment systems, enabling rapid technology refresh cycles. Regulatory heterogeneity obliges manufacturers to juggle pricing tiers and clinical-evidence submissions across markets, but the demographic stroke burden ensures sustained expansion of the neurovascular thrombectomy devices market.

Europe accounts for a mature yet solid demand base. Germany boasts the highest neuro-interventionalist per-capita ratio, while the United Kingdom’s National Health Service delivers universal coverage but contends with queue bottlenecks that can extend transfer times. France, Italy, and Spain allocate stimulus funds to stroke-unit modernization, albeit under fiscal scrutiny. The European Medicines Agency offers harmonized device approval, but stringent post-market surveillance imposes extra cost layers that favor large incumbents. In aggregate, regional procedural growth remains steady, supporting vendor scale economies and R&D cash flow within the neurovascular thrombectomy devices market.

Competitive Landscape

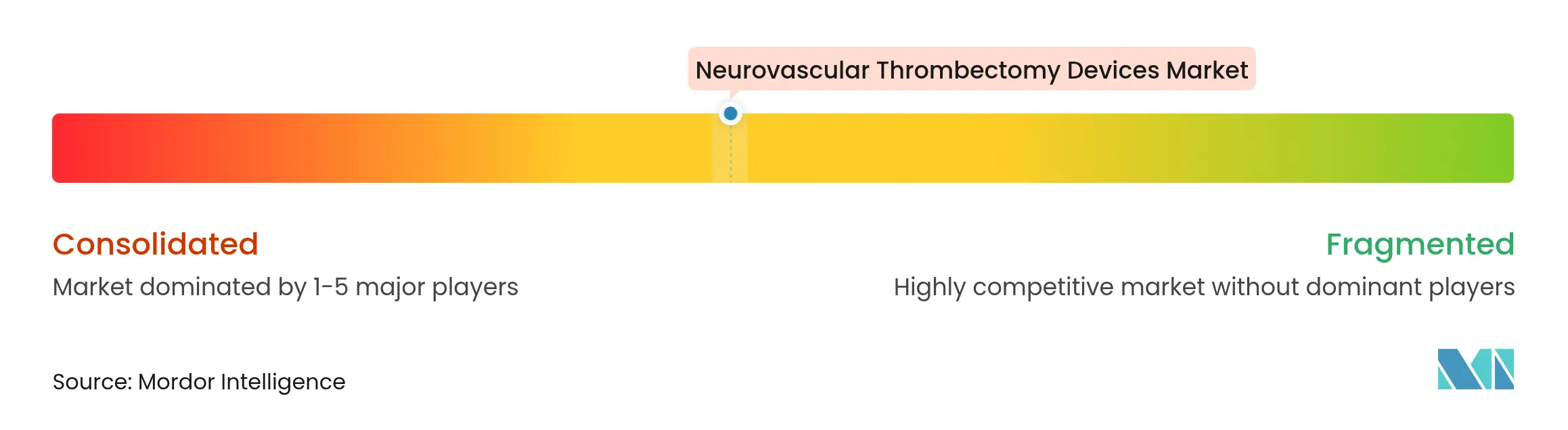

Market Concentration

The neurovascular thrombectomy devices market exhibits moderate concentration. Medtronic, Stryker, and Penumbra anchor global share by capitalizing on seasoned sales networks, extensive clinical evidence, and diversified neurovascular portfolios. Yet disruption looms from aspirational entrants refining bimodal aspiration-retriever hybrids and AI-augmented navigation.

Stryker’s USD 4.9 billion acquisition of Inari Medical in February 2025 expanded its scope into peripheral thrombectomy, unlocking cross-selling synergies and deepening R&D resources. Penumbra’s record USD 321.3 million Q4 2024 sales reflect strong uptake of the Ruby XL catheter, while its forthcoming Lightning Bolt vacuum system targets lower radiation exposure and shorter learning curves. Medtronic leverages pipeline depth and nimble regulatory navigation to sustain share, emphasizing integrated imaging-catheter ecosystems. Supply-chain constraints for nitinol and PEEK escalate material costs, particularly for smaller OEMs, accelerating consolidation as scale becomes essential for input-price negotiation. Patent cliffs on first-generation stents invite lower-cost competition, but next-wave aspiration platforms preserve intellectual-property protection through 2030, cushioning margin profiles.

Emerging players such as Route 92 Medical trial fractional-flow-guided catheters that promise refined distal navigation. Robotics vendors pursue tele-thrombectomy models to mitigate specialist scarcity, but current systems extend procedure duration and depend on high-bandwidth networks, constraining uptake. Strategic collaboration between AI-triage software developers and device manufacturers seeks to integrate pre-hospital imaging with in-room guidance, aspiring to a seamless, data-driven stroke-care continuum that fortifies the neurovascular thrombectomy devices market trajectory.

Neurovascular Thrombectomy Devices Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Stryker Corporation completed its USD 4.9 billion acquisition of Inari Medical, expanding its thrombectomy portfolio to include peripheral vascular applications and creating synergies between neurovascular and peripheral device platforms.

- September 2024: AngioDynamics initiated the RECOVER-AV clinical trial across 20 European sites to evaluate the AlphaVac F1885 System for acute pulmonary embolism treatment, following CE Mark approval.

Table of Contents for Neurovascular Thrombectomy Devices Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Incidence Of Acute Ischemic Stroke & Aging Population

- 4.2.2Adoption Of Minimally-Invasive Thrombectomy As New Standard Of Care

- 4.2.3Expanded Treatment Window (0-24 H) Following DAWN/DEFUSE-3 trials

- 4.2.4Ai-Based Pre-Hospital Stroke Triage Platforms Boosting Eligible Patient Pool

- 4.2.5Next-Generation Large-Bore Aspiration Catheters Improving First-Pass Success

- 4.2.6Hospital “direct-to-angio-suite” Workflow Reducing Door-To-Reperfusion Times

- 4.3Market Restraints

- 4.3.1High Device Cost & Reimbursement Disparities

- 4.3.2Shortage Of Neuro-Interventional Specialists, Especially In Emerging Markets

- 4.3.3Device Efficacy Variability Due To Clot Phenotype Heterogeneity

- 4.3.4Nitinol & PEEK Supply Chain Constraints Inflating Input Prices

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Bargaining Power of Buyers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Stent Retrievers

- 5.1.2Aspiration Catheters

- 5.1.3Combined / Bimodal Systems

- 5.1.4Accessories (Guidewires, Sheaths, Pumps)

- 5.2By End User

- 5.2.1Tertiary-Care Hospitals

- 5.2.2Neuro-Catheterization Labs

- 5.2.3Ambulatory Surgical Centers

- 5.3By Geography

- 5.3.1North America

- 5.3.1.1United States

- 5.3.1.2Canada

- 5.3.1.3Mexico

- 5.3.2Europe

- 5.3.2.1Germany

- 5.3.2.2United Kingdom

- 5.3.2.3France

- 5.3.2.4Italy

- 5.3.2.5Spain

- 5.3.2.6Rest of Europe

- 5.3.3Asia-Pacific

- 5.3.3.1China

- 5.3.3.2India

- 5.3.3.3Japan

- 5.3.3.4South Korea

- 5.3.3.5Australia

- 5.3.3.6Rest of Asia-Pacific

- 5.3.4South America

- 5.3.4.1Brazil

- 5.3.4.2Argentina

- 5.3.4.3Rest of South America

- 5.3.5Middle East and Africa

- 5.3.5.1GCC

- 5.3.5.2South Africa

- 5.3.5.3Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Medtronic plc

- 6.3.2Stryker Corporation

- 6.3.3Penumbra Inc.

- 6.3.4Terumo (MicroVention)

- 6.3.5Johnson & Johnson (CERENOVUS)

- 6.3.6Abbott Laboratories

- 6.3.7Balt USA

- 6.3.8Rapid Medical

- 6.3.9Route 92 Medical

- 6.3.10Imperative Care

- 6.3.11Phenox GmbH

- 6.3.12Kaneka Corp.

- 6.3.13Vesalio

- 6.3.14Acandis GmbH

- 6.3.15Anaconda Biomed

- 6.3.16Inari Medical

- 6.3.17CERUS Endovascular

- 6.3.18Wallaby Medical

- 6.3.19Sequent Medical

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Global Neurovascular Thrombectomy Devices Market Report Scope

Per the report's scope, neurovascular thrombectomy devices are used to retrieve or destroy the blood clots in the cerebral region. The Neurovascular Thrombectomy Devices Market is Segmented by Product Type (Stent Retrievers, Aspiration, Vascular Snares, and Other Product Types), End User (Hospitals, Ambulatory Surgery Centers, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.