Thermoplastic Composites Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

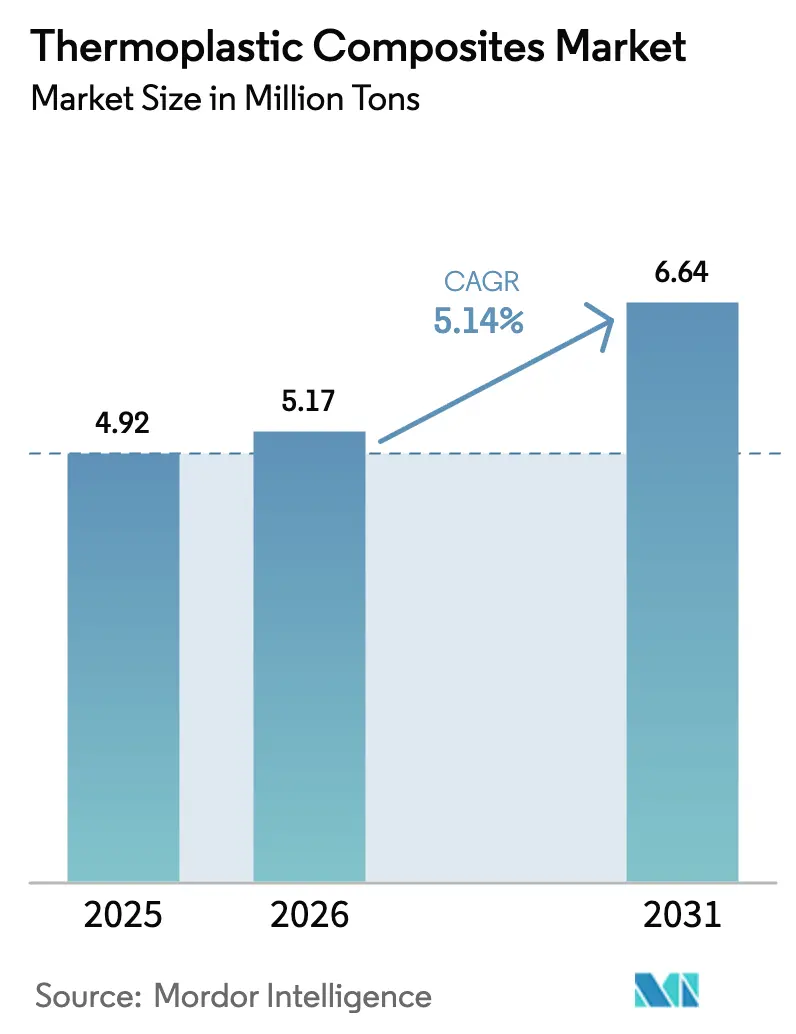

| Market Volume (2026) | 5.17 Million tons |

| Market Volume (2031) | 6.64 Million tons |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

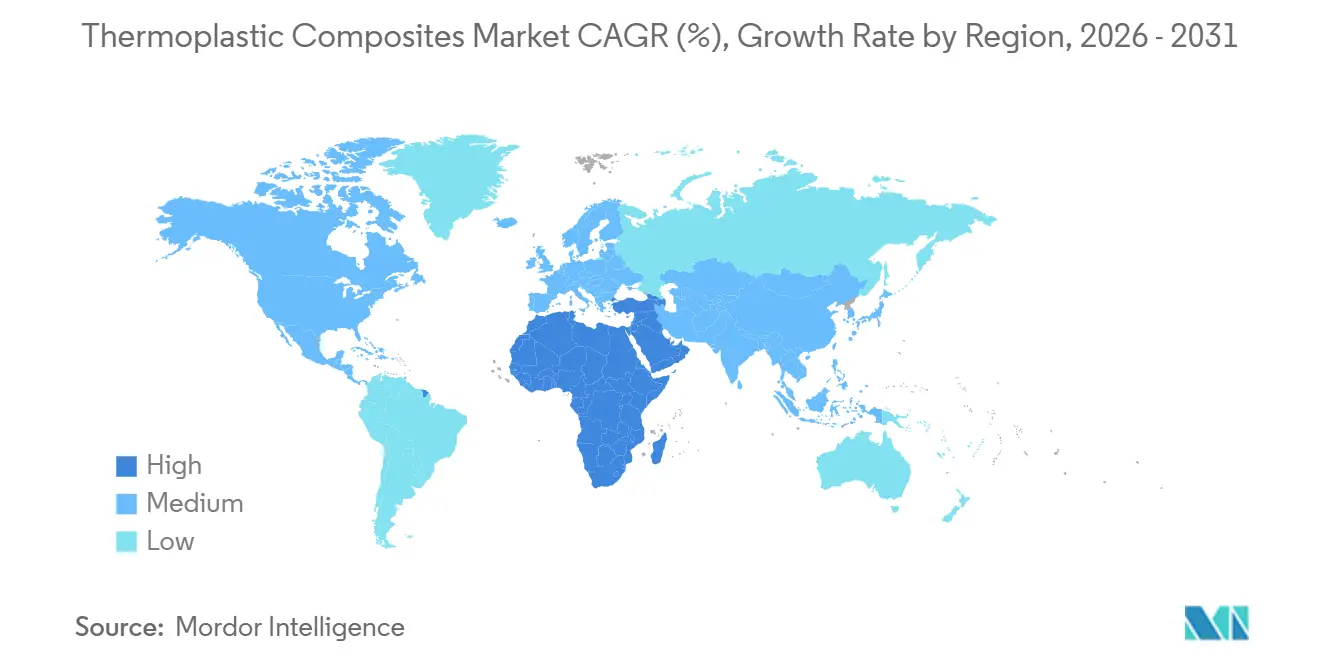

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

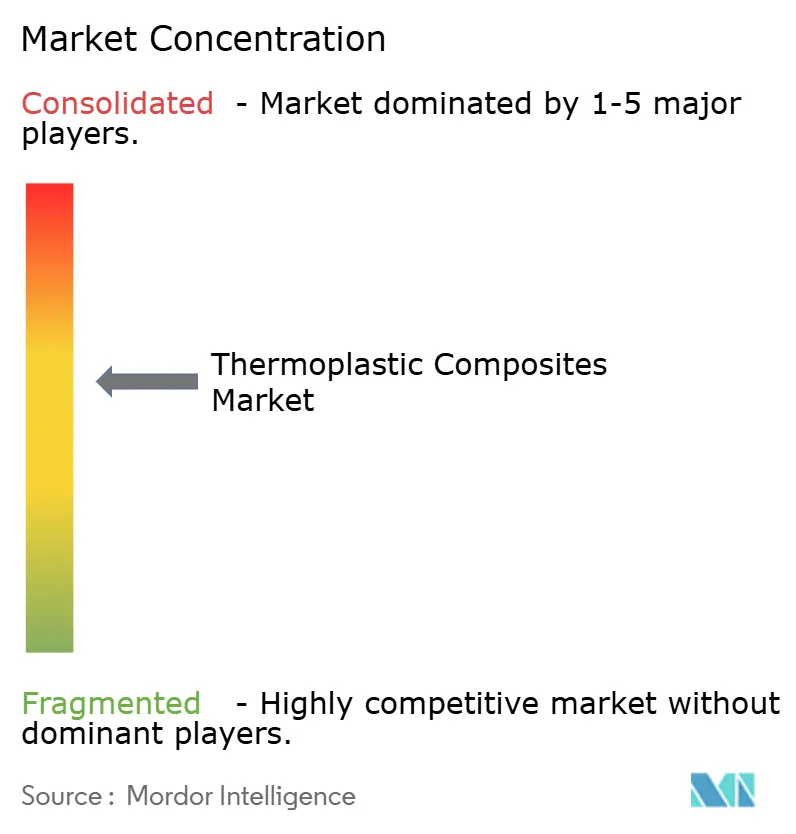

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermoplastic Composites Market Analysis by Mordor Intelligence

The Thermoplastic Composites Market size is expected to increase from 4.92 Million tons in 2025 to 5.17 Million tons in 2026 and reach 6.64 Million tons by 2031, growing at a CAGR of 5.14% over 2026-2031. This growth reflects sustained demand from automotive lightweighting mandates, aerospace production ramp-ups, and energy-infrastructure upgrades that increasingly favor mechanically robust yet recyclable materials. Polyamide, glass-fiber, and short-fiber products continue to dominate high-volume programs because they align with established injection-molding and compression-molding lines. Continuous-fiber formats are gaining share as automated tape-laying cells cut cycle times to below 60 seconds, making structural parts such as battery trays cost-competitive with stamped aluminum. Pressure-vessel makers are also shifting to thermoplastic wraps because Type IV cylinders resist hydrogen embrittlement and trim 40% of curb weight versus steel.

Key Report Takeaways

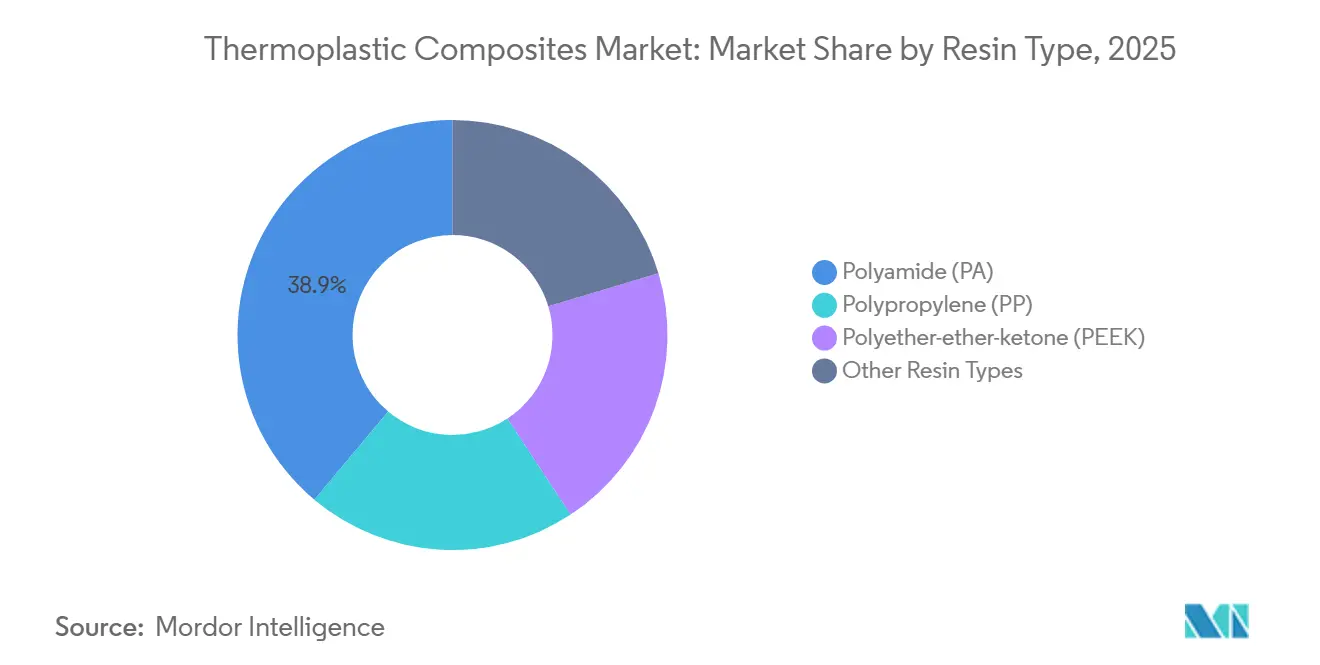

- By resin type, polyamide captured 38.89% of volume in 2025, while polyether-ether-ketone (PEEK) recorded the fastest forecast CAGR at 6.08% through 2031.

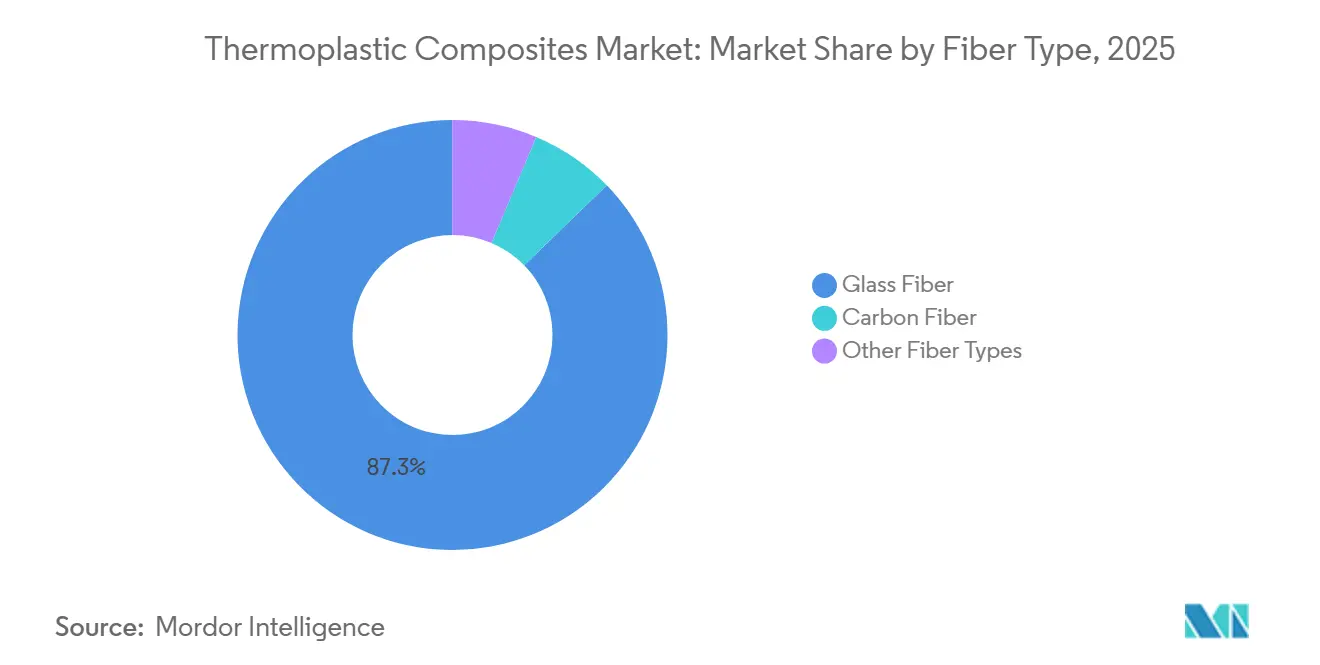

- By fiber type, glass accounted for 87.27% of the 2025 volume; carbon fiber is projected to grow at a 5.81% CAGR through 2031.

- By product type, short-fiber held 39.54% of volume in 2025, whereas long-fiber is set to rise at a 5.36% CAGR to 2031.

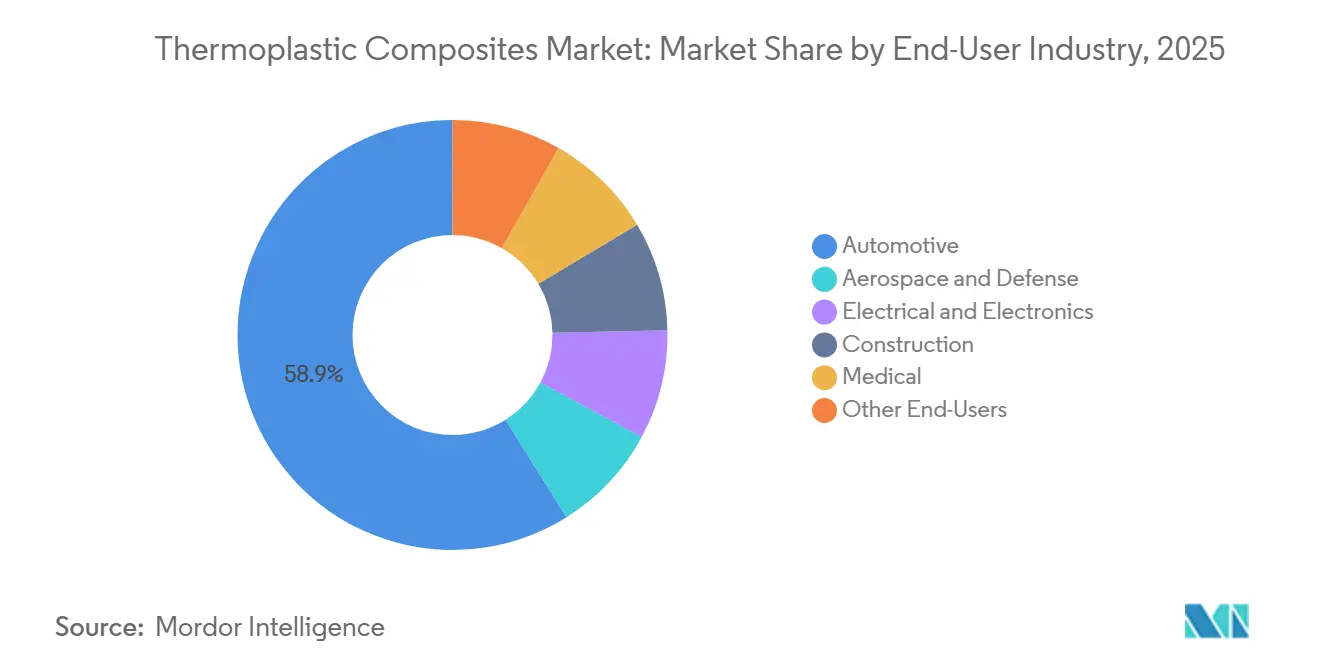

- By end-user industry, automotive dominated with 58.91% of 2025 demand; aerospace and defense are expected to expand at a 6.18% CAGR over the same horizon.

- By geography, Asia-Pacific led with 48.76% of global volume in 2025; the Middle East and Africa are forecast to grow the fastest, at 5.72% annually through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thermoplastic Composites Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Vehicle Lightweighting Mandates in Europe and the United States | +1.2% | Europe, North America | Medium term (2-4 years) |

| OEM Push for Recyclable Composite Solutions in E-Mobility | +1.0% | Global, with concentration in Europe, China | Medium term (2-4 years) |

| Asia-Pacific LNG and Hydrogen Storage Megaproject Pipeline | +0.8% | Asia-Pacific core, spillover to Middle East | Long term (≥4 years) |

| Thermoplastic Over-Molding Adoption in Smart Electronics Housings | +0.6% | Asia-Pacific (China, South Korea, ASEAN), North America | Short term (≤2 years) |

| Military Demand for Damage-Tolerant, Radar-Transparent Structures | +0.5% | North America, Europe, Middle East | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Vehicle Lightweighting Mandates in Europe and the United States

Euro 7 rules effective mid-2025 and the U.S. EPA’s 2027-2032 greenhouse-gas standards oblige automakers to remove 8%–12% of curb weight to stay inside fleet-average limits. Thermoplastic composites deliver 30%–40% savings versus steel yet cycle in under 60 seconds, enabling line-side integration. BMW’s iX roof panel shows structural feasibility while trimming 15 kg per vehicle[1]BMW Group, “Annual Report 2025,” bmwgroup.com. Penalties above EUR 95 per excess gram of CO₂ make adoption financially unavoidable.

OEM Push for Recyclable Composite Solutions in E-Mobility

EU Battery Regulation thresholds on recycled content and digital passports promote closed-loop enclosures built from remeltable matrices. Mercedes-Benz recovers short-fiber polyamide housings for reuse, achieving 22% recycled content with no impact-strength loss. China’s draft design-for-disassembly rules amplify the shift, and the American Chemistry Council targets 30% composite scrap circularity by 2030[2]American Chemistry Council, “Durable Plastics Circularity Roadmap,” americanchemistry.com .

Asia-Pacific LNG and Hydrogen Storage Megaproject Pipeline

Japan’s 12 Mt hydrogen target and South Korea’s 5.26 Mt goal spur demand for Type IV cylinders that weigh 40% less than steel and avoid embrittlement. Strohm’s 10-km composite pipe for a Chinese offshore project validated 100-bar service at −40 °C. NEOM and NEDO adoption further extend the regional scale.

Thermoplastic Over-Molding Adoption in Smart-Electronics Housings

Electronics brands bond rigid frames and soft-touch grips in a single cycle, cutting adhesive steps. Apple’s 2024 iPhone 15 Pro chassis marries titanium with short-fiber polyamide inserts, keeping weight under 200 g. Samsung’s 2025 Galaxy S25 mid-frames raise battery capacity 12% without aluminum. MIIT data show thermoplastic housings doubled to 18% of smartphone mass by 2025.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Raw Materials and Forming Processes | −0.9% | Global | Short term (≤2 years) |

| Limited Awareness and Standardization | −0.5% | Asia-Pacific, South America, Middle East and Africa | Medium term (2-4 years) |

| Competitive Pressure from Thermoset Composites | −0.9% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Cost of Raw Materials and Forming Processes

Polyamide resins fluctuated between USD 2,800 and USD 3,400/ton in 2024-2025 as caprolactam supply tightened, and PEEK still commands USD 60–80/kg, curbing penetration outside aviation and implants. Carbon fiber at USD 15–25/kg remains a premium over glass. Automated tape-laying cells exceed USD 5 million, limiting SME entry, whereas epoxy systems price in at USD 4–6/kg and keep share in low-volume aerospace runs.

Limited Awareness and Standardization

ISO 527 and ASTM D3039 were drafted for thermosets, so weld-line strength and strain-rate effects in thermoplastic composites are under-documented. EASA guidance on primary-structure certification will not finalize before 2027, delaying aircraft adoption. New ISO working groups aim to harmonize test methods by 2028, but until then regional standards add 12–18 months to qualification cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyamide Dominance Meets PEEK’s Niche Expansion

The thermoplastic composites market size for polyamide reached 38.89% of total volume in 2025, owing to high-speed injection lines that meet automotive cycle-time targets. Moisture absorption cuts stiffness 15%–20% but boosts impact toughness, sustaining bumper-beam appeal. PEEK, although just a fraction of tonnage, is on a 6.08% CAGR path as aircraft brackets need 180 °C service and spine cages demand radiolucency. Polypropylene retains non-structural covers where cost and recycled-content mandates align, while PPS and PEI satisfy under-hood flame-retardant niches.

Heightened electrification keeps demand for chemical-resistant matrices; battery-tray suppliers are trialing recycled-content polyamide to meet 25% ELV thresholds. Meanwhile, the U.S. FDA’s 510(k) clearance of PEEK spinal cages spurs hospital demand even as surgeons weigh titanium familiarity. Over the forecast horizon, polyimide blends and low-smoke zero-halogen PAEK grades could carve out cabin-interior volume once fire-smoke-toxicity testing matures.

By Fiber Type: Glass-Fiber Economics Versus Carbon’s Performance Premium

Glass fiber supplied 87.27% of 2025 volume, offering 72 GPa modulus for USD 1.50–2.00/kg - adequate for battery trays and seat backs. Carbon fiber’s 5.81% CAGR outlook is underpinned by programs like Mercedes-Benz EQS roof bows that trim 8 kg and lower center of gravity 12 mm. Basalt and aramid remain below 3% combined because supply chains lack scale.

Crash-standards tightening will gradually expand carbon into B-pillar reinforcements once cost drops below USD 12/kg, expected as two new 25 kt lines in China come online in 2027. Natural-fiber hybrids are testing well for door-trim acoustics in EU vans, though moisture uptake challenges persist.

Product Type: Long-Fiber Gains Ground in Structural Applications

Short-fiber formats kept a 39.54% share in 2025; cycle times under 30 seconds fit high-cavitation tools for intake manifolds. Yet long-fiber’s 5.36% CAGR reflects seat-frame and front-end-carrier conversions that require 150–200 MPa tensile strength. Continuous-fiber tapes already exceed 800 MPa and are entering A350 fuselage frames under Toray’s 2025 supply deal.

Glass-mat thermoplastic (GMT) shields battery packs from road debris, providing quasi-isotropic impact resistance in 90-second cycles. As automotive part-consolidation targets intensify, compression-molded LFT and GMT offerings will capture metal stampings, trimming tool sets by up to 50%.

By End-User Industry: Automotive Lightweighting Versus Aerospace Certification Momentum

Automotive accounted for 58.91% of 2025 tonnage; the Tesla Model Y battery tray alone removed 18 kg and cut assembly time by 35%. Aerospace and defense, however, hold the fastest-growing slot at a 6.18% CAGR as Airbus validates PAEK frames that slash cure time 40% and weight 15% versus aluminum.

Electronics suppliers demand radar-transparent housings; Samsung’s Galaxy Watch 6 case achieved MIL-STD-810H shock-proofing while weighing 30% less than stainless steel. Construction pilots, including composite rebar in marine bridges, show a 50-year life without cathodic protection. Medical adoption pivots on surgeon familiarity, yet radiolucent implants reduce follow-up imaging time and costs.

Geography Analysis

Asia-Pacific held 48.76% share in 2025, powered by China’s 26.1 million vehicle output and electronics clusters along the Pearl River Delta. Beijing’s NEV plan, extended to 2030, requires recyclable lightweight components, fueling short- and long-fiber feedstock imports. Japan’s JPY 300 billion subsidy backs 1,000 hydrogen stations by 2030, pulling Type IV cylinder demand. South Korea’s multi-material mid-frame adoption reduced smartphone assembly steps 40%. India’s production-linked incentive cuts capital costs for composite cells, while Vietnam and Thailand expand over-molding capacity as supply chains diversify.

North America and Europe account for significant consumption volume. U.S. CAFE rules force Detroit to drop 100–150 kg per model using composite closures and seating. Boeing’s 777X floor beams showcase cost and cycle reductions, and Euro ELV mandates place 25% recycled-plastic thresholds by 2030. The U.K.’s GBP 18 million wing-skin project targets 50% labor cuts at ATI facilities.

The Middle East and Africa lead by growth rate at 5.72% through 2031. Saudi Aramco’s 200-km hydrogen pipeline at NEOM highlights 60% weight savings and embrittlement resistance. Masdar City specs thermoplastic façades that survive 50 °C swings. South Africa’s Nampak compounding line readies for export vehicles bound for Europe, while Nigeria assesses sour-gas composite pipe to meet local content rules. South America trails, though Brazilian agri-equipment gains from lightweight harvesters that consume less diesel.

Value Chain Analysis

The value chain starts with upstream feedstocks (caprolactam and other monomers), resin producers (PP, PA, PPS, PEI and PAEK/PEEK/PEKK families), and fiber suppliers (glass and carbon). Inputs then move to compounders and semi-finished goods producers that deliver short- and long-fiber pellets, GMT sheets, and continuous-fiber tapes or prepregs (for example, Toray Cetex thermoplastic composite material systems used across fabric and UD tape formats).

Midstream conversion relies on specialized forming and joining equipment, including automated stamp forming or overmolding cells and induction welding solutions that enable faster assembly of large thermoplastic composite structures. Downstream, tier suppliers and fabricators convert these materials into automotive structural parts (battery trays, beams and carriers), aerospace brackets and frames, electronics housings, construction products, and medical components. Qualification and industrialization partnerships increasingly shape go-to-market routes and reduce adoption friction, as reflected in the June 2025 KVE Composites Group and Pinette PEI arrangement to integrate induction welding into thermoplastic composite manufacturing cells, and the June 2026 Syensqo and Bucci Composites collaboration around Double Diaphragm Forming (DDF) for high-volume structural parts. Distribution alliances also influence reach for advanced tape offerings, with BUFA distributing Covestro Maezio UD tapes, while constraints remain concentrated in premium resin pricing (PEEK at USD 60-80/kg in 2024-2025 per report context), carbon-fiber lead-time volatility, and the capital intensity of automated tape-laying and forming lines.

Competitive Landscape

The thermoplastic composites market is moderately consolidated, with the leading players holding considerable production capacities and advancing the production of innovative products. BASF’s Ultramid Structure couples long-fiber pellets with simulation software, letting OEMs consolidate metal stampings and carve 25% off tooling cost. Long-term success hinges on backward-integrated resin supply, forward-integrated automated fabrication, and partnerships that guarantee closed-loop recycling streams. Suppliers that match material innovation with digital traceability will capture an outsized share as circular-economy mandates tighten.

Thermoplastic Composites Industry Leaders

TORAY INDUSTRIES, INC.

Solvay

Hexcel Corporation

SABIC

TEIJIN LIMITED

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Aerospace-grade qualification and industrial-scale processing create whitespace for thermoplastic composite systems that can transition from lab validation to repeatable production, especially where fusion bonding and welding displace multi-step fastening. The May 2026 expansion of NCAMP qualifications for Toray Cetex TC1225 LMPAEK, adding a TC1225/TORAYCA T700 UD tape prepreg, highlights how standardized material allowables and broader qualified formats can support faster sourcing and multi-tier adoption for aircraft structures. Equipment integration partnerships, including induction welding solutions for thermoplastic composite cells, also point to a pathway for suppliers that bundle materials, process windows, and automation-ready intermediate forms into application-specific kits for battery enclosures, aircraft frames, and high-volume structural brackets.

Circularity and upcycling are emerging as actionable, near-term opportunity areas because thermoplastic matrices can be remelted and reprocessed, enabling closed-loop programs that extend beyond production scrap into end-of-life parts. A proof point is the June 2025 end-of-life aircraft recycling program launched by Toray, Daher and TARMAC Aerosave (supported by Airbus) to recover and reuse continuous fiber-reinforced thermoplastic composite parts. Daher also reported in March 2026 that it structured an upcycling value chain producing carbon PPS pellets (4-8 metric tons per year). On the supply side, announced capacity and footprint investments add commercial pathways for specialty thermoplastic composites and engineered thermoplastics, including Mitsubishi Chemical Advanced Materials securing a USD 20.3 million investment in July 2026 to expand its Reading, Pennsylvania site with an adjacent facility and new machinery. Taken together, these steps align with opportunities in certified aerospace materials, automated welding and forming integration for automotive and high-rate aircraft production, and scalable recycling and upcycling streams that can help OEMs meet recycled-content and traceability needs referenced in the report context, such as EU Battery Regulation-driven closed-loop enclosures.

Recent Industry Developments

- July 2026: Mitsubishi Chemical Advanced Materials secured a USD 20.3 million investment to expand its Reading, Pennsylvania site, including construction of an adjacent facility and new machinery for specialty engineering thermoplastics and composites. The expansion strengthens North American supply availability for higher-performance thermoplastic materials used in composite applications and supports shorter lead times for qualified programs.

- December 2025: Toray Advanced Composites completed NCAMP qualification for Toray Cetex TC1225 LMPAEK fabric-based thermoplastic composite material, offered in semi-preg and large pre-consolidated reinforced thermoplastic laminate formats. The qualification improves usability across aerospace supply chains by easing material allowables acceptance and enabling more standardized sourcing for thermoplastic composite structures.

- March 2024: Hexcel reported the realization of an aeronautical structure demonstrator using thermoplastic composite tapes (HexPly) developed with Arkema using Kepstan PEKK resin, under the HAICoPAS project. The demonstrator validated multi-partner pathways for thermoplastic composite primary-structure concepts and reinforced the role of resin-tape co-development in moving toward welded, high-rate aerospace assemblies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the thermoplastic composites market covers fiber reinforced materials that use melt processable thermoplastic resins and are sold as pellets, sheets, prepregs, or molded forms to downstream processors and part makers for industrial use.

Scope exclusions: We exclude thermoset matrix composites and any adjacent materials that are not sold as thermoplastic composite material forms.

Segmentation Overview

- By Resin Type

- Polypropylene (PP)

- Polyamide (PA)

- Polyether-ether-ketone (PEEK)

- Other Resin Types

- By Fiber Type

- Glass Fiber

- Carbon Fiber

- Other Fiber Types

- By Product Type

- Short-Fiber Thermoplastic (SFT)

- Long-Fiber Thermoplastic (LFT)

- Continuous-Fiber Thermoplastic (CFT)

- Glass-Mat Thermoplastic (GMT)

- By End-User Industry

- Automotive

- Aerospace and Defense

- Electrical and Electronics

- Construction

- Medical

- Other End-Users

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Nigeria

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the supply chain from resin and fiber inputs through compounders, prepreg producers, and converters, then linking it to end use activity. We pull foundational production and trade signals from public sources such as UN Comtrade, national customs and statistics offices, and industry safety and standards bodies that publish polymer and composite related references.

To keep assumptions realistic, we also review manufacturer technical datasheets, publicly available investor materials, and credible press coverage for capacity additions, product launches, and application shifts. Where needed, subscription datasets are used for company financials and intelligence, patent lookups, and shipment level import export screening, which helps fill gaps when public data is not specific to composites. The desk sources listed here are illustrative, and we also used other public references as cross checks and for clarification.

Primary Interviews and Surveys

Primary work is used to test what we see in public data against what is happening in real procurement and processing. We spoke with a mix of material suppliers, compounders, converters, and downstream users across APAC, EMEA, and the Americas, and we checked views on pricing, substitution (thermoplastic versus thermoset), and adoption in end uses such as automotive and aerospace.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 19% | APAC: 45% |

| Mid tier: 48% | Functional/Unit leaders: 26% | EMEA: 34% |

| Smaller Players: 20% | Managers: 55% | Americas: 21% |

Market-Sizing & Forecasting

Sizing is built by using top down reconstruction, where polymer and composite relevant production and trade series are translated into an addressable demand pool, then filtered using thermoplastic composite penetration by end use and region. To keep the totals grounded, we corroborate the outcome with selective bottom-up checks such as sampled supplier output ranges, channel feedback on volumes, and typical price per ton bands for major formats.

A few inputs that shape the model include aerospace build rates and qualifying programs, vehicle lightweighting intensity and platform material shifts, pressure vessel and pipe adoption where applicable, regional manufacturing output in key end uses, and the mix shift across short fiber, long fiber, and continuous fiber formats. Pricing is handled through an ASP progression that reflects resin index movements, fiber cost direction, and mix effects, and then it is normalized into a consistent USD time point. For forecasting, scenario analysis is used so adoption rate changes and capacity ramp timelines can be flexed, and expert feedback is used to keep the scenarios aligned with what processors can realistically convert each year.

Data Validation & Update Cycle

Model outputs are checked against independent signals like trade flows, capacity announcements, and end use production indicators, and then variances are investigated before final sign off. When a number looks out of pattern, we re check unit conversions, regional splits, and the pricing logic, and we may re contact an interviewee group to confirm what changed.

Each report is refreshed annually, and interim updates are made when material events occur such as major plant start ups, regulatory shifts, or demand shocks in automotive or aerospace. Right before delivery, an analyst runs a final pass on the dataset and key assumptions so clients receive the latest updated view.

Mordor Intelligence's Thermoplastic Composites Market Size Compared With Other Published Estimates

Published market sizes for thermoplastic composites can vary widely because the boundaries are not always the same, and because some studies mix volume and value without clearly stating the conversion logic. Differences also come from the year chosen for pricing, currency timing, and whether adoption curves are treated as smooth or stepwise.

The benchmark table shows a volume based estimate, and in Mordor Intelligence's model the market counts thermoplastic composite material forms sold into downstream processing, rather than the value of finished composite parts or assemblies. When other sources use value based totals, the gap is often driven by whether they include part fabrication margins, the mix of higher priced continuous fiber formats, and how quickly they step up aerospace and automotive penetration in the early years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.92 M (2025) | |

| Global Consultancy A | USD 23.58 B (2024) | Uses a value based definition, which can fold in higher priced end use mixes and may capture additional layers like part level pricing rather than material form volumes. |

| Industry Publisher B | USD 19.92 B (2025) | Publishes a value estimate tied to assumed ASPs and mix shifts, and the total can move if continuous fiber adoption and regional price normalization are handled differently. |

Reading the table together, the spread is mainly explained by unit and scope choices, plus how pricing and mix are treated over time. The approach here stays traceable to clear demand indicators and repeatable steps, which makes it easier for buyers to adjust assumptions without rebuilding the whole model.

Key Questions Answered in the Report

How big is the thermoplastic composites market in 2026?

The thermoplastic composites market is estimated to reach 5.17 million tons in 2026 and is forecast to grow at a 5.14% CAGR to 2031.

Which resin dominates current demand?

Polyamide holds the lead with 38.89% of 2025 volume thanks to cost-effective injection-molding compatibility.

What end-use segment is growing fastest after automotive?

Aerospace and defense applications are projected to rise at a 6.18% CAGR as airframers shift to continuous-fiber thermoplastic structures.

Why are thermoplastic composites preferred for hydrogen storage?

Type IV cylinders with thermoplastic wraps weigh 40% less than steel and resist hydrogen embrittlement, improving fuel-cell vehicle range and safety.

Which region will add the most incremental volume by 2031?

Asia-Pacific leads in absolute tonnage, while the Middle East and Africa post the highest growth rate at 5.72% per year, driven by hydrogen infrastructure builds.

Page last updated on: