Aerosol Paints Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

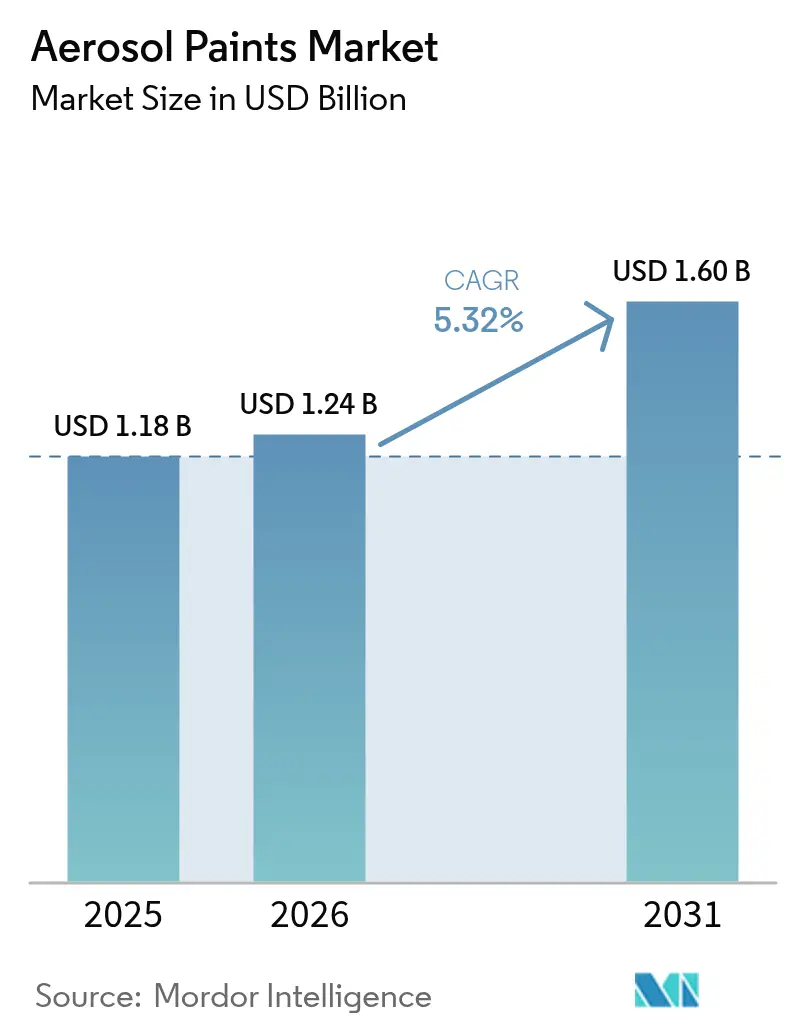

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 1.60 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerosol Paints Market Analysis by Mordor Intelligence

The Aerosol Paints Market size is expected to increase from USD 1.18 billion in 2025 to USD 1.24 billion in 2026 and reach USD 1.60 billion by 2031, growing at a CAGR of 5.32% over 2026-2031. Supply is shifting away from large contractor orders toward project-based, on-demand purchases, a pattern reinforced by growth in urban micro-manufacturing, infrastructure touch-ups, and a do-it-yourself culture that values speed and minimal cleanup. Solvent-borne chemistries still dominate because water-borne alternatives lengthen dry time and struggle with year-round adhesion, yet regulatory tightening under U.S. VOC limits and the Kigali Amendment is forcing gradual technology migration. Asia-Pacific remains the largest demand center, underpinned by rapid residential construction in China and India, while North America’s expansion is driven by consumer refurbishment and infrastructure maintenance. Competitive intensity stays moderate: the top ten suppliers control roughly half of global capacity, but regional brands persist where localized color palettes and fire-code storage limits deter multinationals.

Key Report Takeaways

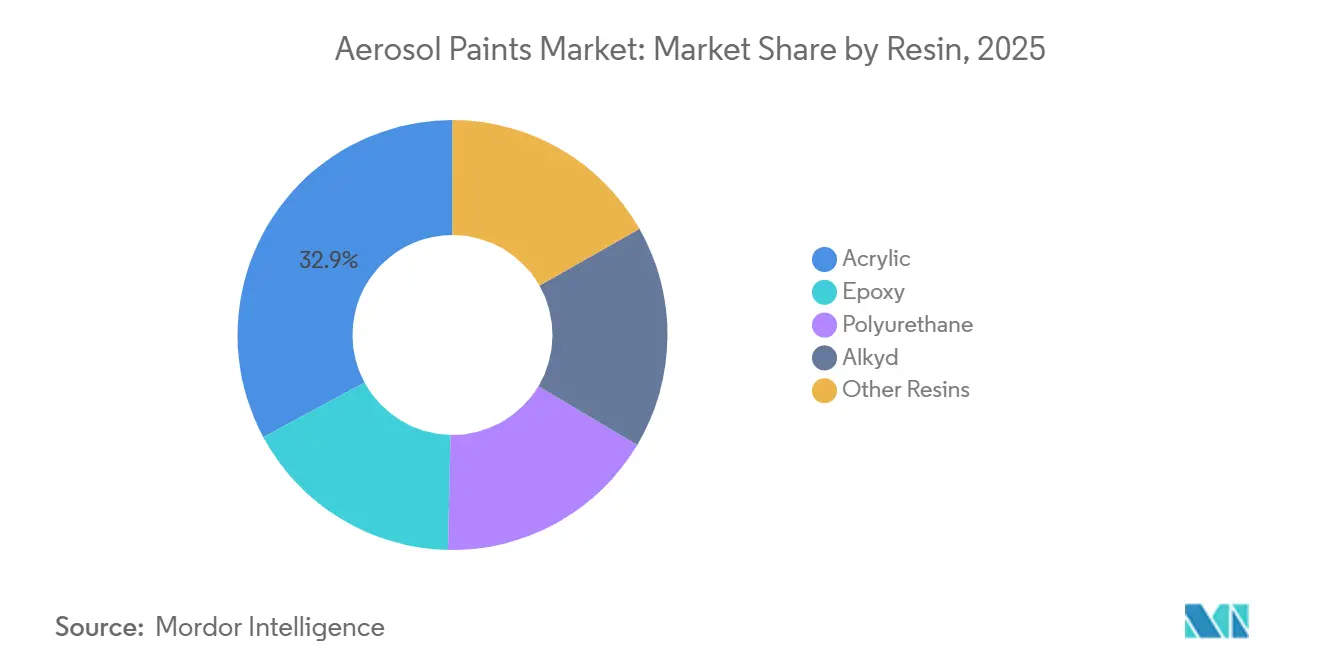

- By resin, acrylic dominated with 32.89% aerosol paints market share in 2025 and registered the fastest 5.59% CAGR to 2031.

- By technology, solvent-borne held 53.35% share of the aerosol paints market size in 2025, whereas water-borne is forecast to expand at a 5.94% CAGR through 2031.

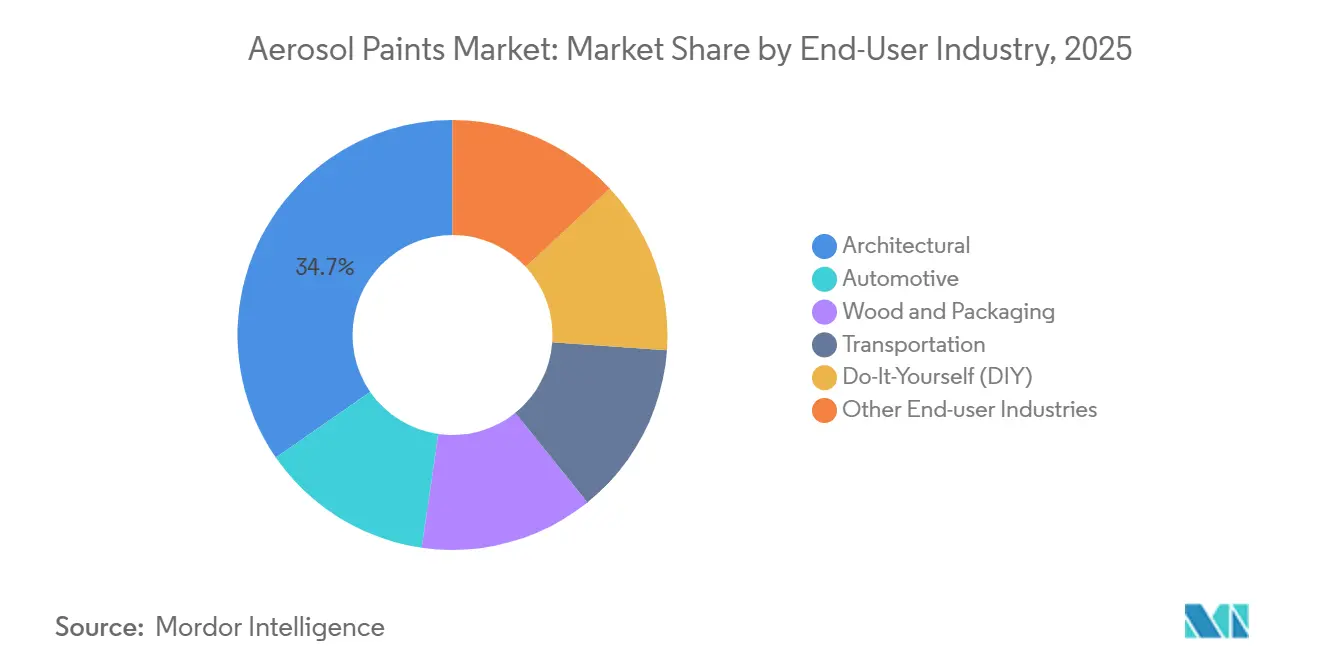

- By end-user industry, the architectural segment led with 34.66% revenue share in 2025; the Do-It-Yourself (DIY) segment is advancing at a 7.18% CAGR to 2031.

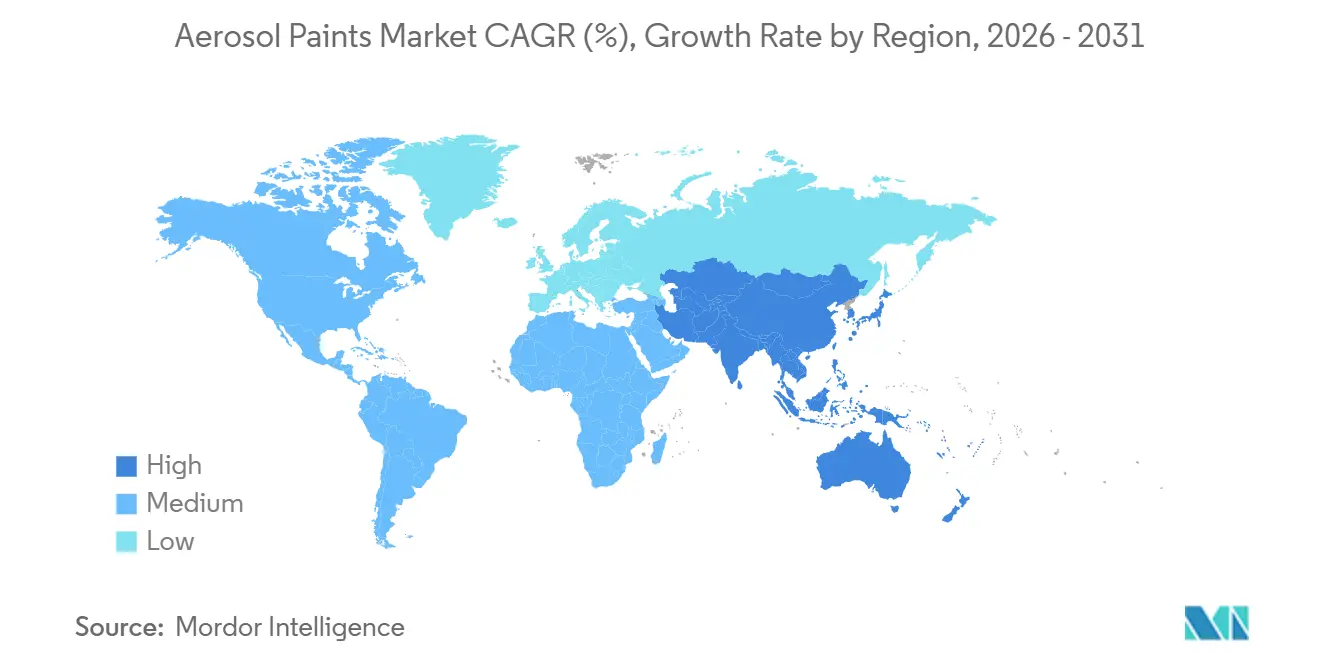

- By geography, Asia-Pacific captured 45.47% of the aerosol paints market size in 2025 and is progressing at a 5.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aerosol Paints Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Residential and Commercial Construction Activities | +1.2% | Asia-Pacific (China, India), Middle East (Saudi Arabia), North America | Medium term (2-4 years) |

| Increasing DIY Refurbishment and Décor Projects | +1.5% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Growing Automotive Customization and Refinishing Culture | +0.9% | Global, with concentration in North America, Europe, China | Medium term (2-4 years) |

| Urban Micro-Manufacturing and Maker-Space Adoption of Spray Finishes | +0.6% | North America, Europe (Berlin, London, Paris), Asia-Pacific (Seoul, Tokyo) | Long term (≥ 4 years) |

| Nano-Ceramic Direct-to-Metal Sprays for Ageing Infrastructure | +0.8% | North America (Gulf Coast), Europe (North Sea offshore), Asia-Pacific coastal zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Residential and Commercial Construction Activities

In China, India, and Saudi Arabia, where housing mandates impose penalty clauses for delays, completion speed has become the primary criterion for paint selection, surpassing square-footage expansion. By reducing labor hours on trim and punch-list work, aerosol coatings help alleviate the pressures of skilled-worker shortages and rising wages. The Neom program in Saudi Arabia emphasizes modular building methods, which align seamlessly with single-coat aerosol primers. In North America, design-build contracts are increasingly internalizing finishing tasks, leading general contractors to favor aerosol paints to sidestep scheduling conflicts with subcontractors. Collectively, these trends are boosting the penetration of aerosol paints in new-build activities.

Increasing DIY Refurbishment and Décor Projects

PPG's Glidden Max Flex range, with a five-minute dry time and a no-drip formulation, underscores the growing preference among Millennials and Gen-Z homeowners for DIY projects, like accent walls and furniture up-cycling[1]PPG, “GLIDDEN MAX FLEX Spray Paint,” PPG.COM. Instead of purchasing contractor-sized liquid gallons, these homeowners now typically buy two to four aerosol cans per project. Furthermore, online sales saw an uptick in fiscal 2024, highlighting the strength of direct-to-consumer channels in bolstering overall demand. The fast-dry feature not only expedites the process but also minimizes the need for masking and cleanup, making the higher per-square-foot cost of aerosols more palatable.

Growing Automotive Customization and Refinishing Culture

European body shops grapple with a technician shortfall. This gap has spurred the adoption of Sherwin-Williams’ Collision Core Pronto dispenser. The dispenser adeptly mixes colors daily, achieving a precision of 0.01 grams, and reduces setup time by half. Meanwhile, driven by social media trends, hobbyists are gravitating towards aerosol kits. These kits allow for color-shift effects, eliminating the need for costly booths. In China, the market for touch-up aerosols is booming. Consumers are opting for aerosols, sidestepping traditional dealer repair networks. With performance specs like gasoline resistance and a swift 30-minute cure, aerosol enamels seamlessly blend consumer convenience with professional-grade durability.

Urban Micro-Manufacturing and Maker-Space Adoption of Spray Finishes

In Berlin, London, and Tokyo, maker-space networks are witnessing a surge in small-batch prototyping, with a growing demand for color flexibility and a desire to avoid the cleanup hassles associated with traditional spray guns. Portable fume extractors meet ventilation regulations, enabling the use of aerosols in co-working spaces, especially where fixed booths come at a premium. Aerosol coatings have significantly expedited product-development cycles for contract manufacturers, reducing the time from eight weeks to three. While this channel accounts for a small portion of the global volume, it positions suppliers in a lucrative niche, shielded from the volatility of commodity price competition.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC-Content Regulations | -1.1% | North America (EPA jurisdiction), Europe (EU Directive 2004/42/EC), California (CARB) | Short term (≤ 2 years) |

| Phase-Down of HFC Propellants under Kigali Amendment | -0.9% | Global, with earliest impact in EU, North America; Article 5 countries from 2029 | Medium term (2-4 years) |

| Fire-Code Restrictions on Pressurised Paint Storage | -0.5% | North America (NFPA 30), Europe (ATEX zones), Asia-Pacific urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC-Content Regulations

In 2024, the U.S. EPA set a flat-finish limit of 50 g/L, effectively phasing out legacy alkyd aerosols unless costly exempt solvents are used in place of xylene and toluene. California is set to impose a stricter 25 g/L cap on consumer aerosols in 2025, intensifying cost pressures, particularly for fast-dry lacquers favored by DIY enthusiasts. Meanwhile, Germany's TA Luft mandates third-party testing and annual emissions reporting, incurring an added cost for medium-sized companies[2]German Federal Gazette, “TA Luft 2024 Update,” BUND.DE . As a result, compliant raw material costs have surged, tightening margins for regional brands that lack the scale to distribute research and development and audit expenses.

Phase-Down of HFC Propellants under Kigali Amendment

By 2029, a reduction from 2024 baselines and a significant cut by 2036 have driven HFC-152a spot prices up. While dimethyl ether substitutes share similar vapor-pressure properties, they are classified as flammable gases. This distinction has led to necessary warehouse retrofits, a task only a portion of U.S. fillers accomplished by 2025. Hydrofluoro-olefin-1234ze finds its niche solely in premium industrial lines. Additionally, supply-chain frictions have extended reformulation lead times from the usual timeframe, limiting SKUs that struggle to adapt to escalating sustainability mandates without altering their propellants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Acrylic Versatility Sustains Leadership

Acrylics accounted for 32.89% of 2025 revenue, the largest aerosol paints market share among resins, and are forecast to grow at a 5.59% CAGR through 2031. These resins, with a chemical backbone that seamlessly integrates solvent-borne and water-borne systems, offer tack-free surfaces in just 20 minutes. This rapid curing, combined with UV protection, caters to the needs of vehicle refinishers and furniture upcyclers. Sherwin-Williams’ K2 two-component acrylic enamel boasts impressive coverage and excels in durability, passing rigorous salt-spray tests and meeting ISO C5 corrosion standards, making it particularly attractive to markets in humid coastal regions.

Epoxies, though lesser in volume, carve out a niche in maintenance-repair-operations. Here, they provide the robust adhesion needed for marginally prepared steel. As infrastructure budgets increasingly favor refurbishment, the adoption of epoxies is set to surge. Meanwhile, polyurethanes have carved a niche as specialty coatings, especially for chemical-resistant touch-ups. This is underscored by Sherwin-Williams’ Acrolon 680, which boasts resilience against a 10% sulfuric acid immersion. On the sustainability front, innovations in recycled PET-based alkyds highlight potential eco-friendly pathways, though their price premiums currently hinder widespread adoption.

By Technology: Solvent-Borne Persistence Under Regulatory Squeeze

Solvent-borne products accounted for 53.35% of 2025 demand, while water-borne formulations posted the highest 5.94% CAGR. Solvent-borne formulations maintained the largest slice of the aerosol paints market size thanks to low-temperature film formation and adjustable solvent blends for leveling control. Transfer efficiency in trained hands is comparable with HVLP spray, but without the booth investment. Krylon’s Iron Guard water-borne enamel counters by adding flash-rust inhibitors, enabling damp-steel application and gaining NSF food-contact certification.

Growth upside for water-borne technology lies in DIY and institutional environments where odor and VOC limits drive procurement. However, freeze-thaw sensitivity still requires stabilizers, restricting winter use in northern climates. Patent activity around bio-based coalescing agents signals future competitiveness, yet until low-temperature coalescence breakthroughs materialize, solvent-borne aerosols will keep priority share in the aerosol paints market.

By End-User Industry: DIY Upswings Shift Channel Economics

The architectural segment represented 34.66% of 2025 demand, anchored in trim, accent walls, and touch-ups where aerosol convenience outweighs per-can price. The do-it-yourself channel delivers the fastest 7.18% CAGR as project frequency rises and average ticket sizes fall, reinforcing SKU fragmentation and just-in-time fulfillment strategies at big-box retailers.

Automotive refinishing splits between precision body-shop color-match work and consumer customization kits. Sherwin-Williams’ automated dispensers shrink color-mixing time and tackle skilled-labor shortages, while hobbyist demand gravitates toward gasoline-resistant aerosols for motorcycles and classic cars. Segments like transportation, wood, and packaging utilize aerosols for quick color changes. This is evident in applications like municipal traffic marking, which adheres to APWA color standards, prioritizing speed over the economics of high-volume spray lines.

Geography Analysis

Asia-Pacific held 45.47% of global volume in 2025, and sustained a 5.72% CAGR through 2031. China rolled out significant urban housing units, while India's PMAY-Urban 2.0 fast-tracked affordable housing projects, ensuring completion within 18 months. In tier-2 cities of India, aerosol primers are proving their worth by slashing skilled labor hours, a timely advantage given the rising wage trends. Meanwhile, Japan and South Korea are increasingly adopting maker-space applications. At the same time, ASEAN nations are diversifying their demand, navigating the complexities of fragmented local VOC regulations that pose challenges for multinational entries.

North America accounted for a significant portion of the 2025 revenue pie. Here, the aerosol paints market is buoyed not by new constructions but by residential refurbishments, a surge in e-commerce, and ongoing infrastructure maintenance. Home Depot reported an uptick in online aerosol sales, crediting bundled project kits for easing customer decisions. With an infrastructure shortfall, Canadian provinces are turning to nano-ceramic aerosols, which notably extend coating lifespans, thereby slashing life-cycle costs. Additionally, Mexico's vehicle exports have spurred a surge in refinishing demand, especially along the U.S. border.

Europe secured a substantial share of the global volume in 2025. The region grapples with stringent VOC and fire-code regulations. For instance, Germany's TA Luft and the UK's post-Brexit standards, which, while inflating compliance costs, also favor players with robust regulatory budgets. Italy, with its heritage-restoration fund, mandates low-VOC aerosols for interior work to minimize disruptions. Concurrently, Eastern Europe's transport upgrades are driving demand for fast-cure marking paints.

South America and the Middle East-Africa regions together represent a modest portion of global consumption. Petrobras, with an offshore maintenance budget, is leaning towards single-coat aerosol systems, which significantly reduce the need for rope-access days. In a similar vein, Saudi Arabia's ambitious Neom project is utilizing aerosol primers for its modular units to expedite processes. Furthermore, South Africa's push towards renewable energy is fueling a demand for UV-stable topcoats. These topcoats are engineered to withstand intense radiation without chalking, with suppliers incorporating premium UV absorbers to meet the heightened specifications.

Regulatory Landscape

Regulation for aerosol paints is tightening around VOC emissions and propellant choices, which is pushing formulators toward lower-reactivity solvent packages and more water-borne lines. In the United States, the U.S. Environmental Protection Agency (EPA) finalized amendments to the National Volatile Organic Compound (VOC) Emission Standards for Aerosol Coatings on January 6, 2025, using a reactivity-based approach to limit ozone formation. A July 2, 2025 interim final rule extended the compliance deadline to January 17, 2027, giving manufacturers additional time to rework product-weighted reactivity (PWR) compliance pathways.

In Europe, chemical and eco-label frameworks are increasingly shaping product design and claims. Commission Decision 2025/2607 (adopted December 17, 2025) set new EU Ecolabel criteria for water-based aerosol spray paints, with tighter requirements on VOC during application and restrictions on hazardous substances, including endocrine disruptors and Persistent, Mobile, and Toxic (PMT) substances. The European Commission also released user manuals and application guidance in early 2026. These measures reinforce a compliance premium for suppliers that can document performance and emissions, while raising the bar for smaller regional brands that lack testing and reporting resources.

Value Chain Analysis

The aerosol paints value chain starts with upstream feedstocks for binders (acrylic, alkyd, polyurethane, epoxy), pigments, solvents, and propellants, then moves to packaging inputs such as metal cans, valves, and gaskets. Manufacturing and filling are capital- and compliance-intensive, requiring explosion-proof zones (for example, Class 1 Division 1 layouts), controlled propellant storage, crimping and leak-detection systems, and multi-stage gas dosing. This concentrates capability among specialized fillers and integrated producers.

Downstream, branded owners and private-label programs source from in-house plants or contract fillers, then distribute product through regional distributors, big-box retail, and e-commerce channels that increasingly favor small, project-based orders. Contract manufacturing providers (e.g., Global Aerosols and Schwartz Advanced Chemical Solutions) lower entry barriers for brands by bundling formulation, filling, and packaging. Still, the chain is exposed to regulatory-driven reformulation cycles tied to VOC standards (including U.S. federal aerosol coatings rules) and to bottlenecks in specialized components and safe storage and transport requirements for pressurized, often flammable, propellant systems.

Competitive Landscape

The aerosol paints market is moderately consolidated. Technology adoption bifurcates: tier-one players invest in automated mixing systems like Collision Core Pronto to mitigate labor shortages, whereas small brands push rapid formulation cycles that match regional color fads within six weeks. Vertical integration trends upward. Compliance-driven consolidation is likely, as fire-code–driven storage retrofits and HFC quota costs squeeze under-capitalized competitors.

Aerosol Paints Industry Leaders

The Sherwin-Williams Company

PPG Industries Inc.

Akzo Nobel N.V.

Nippon Paint Holdings Co., Ltd.

RPM International Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory and procurement shifts are creating whitespace for water-borne and low-odor aerosol formats with credible environmental credentials, particularly in DIY and institutional settings where VOC limits increasingly affect shelf placement and project choice. The EU has created a clearer pathway for differentiated, water-based offerings through Commission Decision 2025/2607 (December 2025), which established EU Ecolabel criteria for water-based aerosol spray paints and was supported by European Commission user manuals issued in early 2026. This gives suppliers a practical route to compete on verified formulation and use-phase performance, not just color range.

Manufacturing localization and capacity additions are also changing competitive options in key demand centers, supporting faster replenishment for fragmented SKUs and region-specific palettes. In India, Nippon Paint announced an initiative (June 2026) to add eight manufacturing plants with an investment of EUR 56 million over the next 18 months, aligning with demand drivers tied to construction activity and faster completion cycles. In North America, PPG’s advanced manufacturing program includes a new 250,000-square-foot paint and coatings facility in Loudon County, Tennessee, scheduled for completion in 2026, which supports domestic supply for faster-turn product formats used in refurbishment and maintenance.

Recent Industry Developments

- July 2026: Sherwin-Williams launched Heat-Flex AEB, a spray-applied thermal insulative coating aimed at storage tanks and piping where corrosion under insulation is a concern. The offering extends spray-applied maintenance solutions that reduce downtime versus traditional insulation and coating sequences. It also reinforces the shift toward higher-value, performance-led spray systems that can be deployed for field touch-up and maintenance cycles.

- June 2026: Nippon Paint Group and Sherwin-Williams ended their pursuit of acquiring Akzo Nobel after the Dutch company rejected their joint all-cash offers. The decision removed a potential consolidation outcome among major coatings suppliers and kept competitive structures intact across multiple coatings categories. It also redirected strategic attention and capital toward organic investments and product and process innovation rather than large-scale M&A integration.

- March 2026: PPG introduced PPG AQUACRON waterborne shop primers for structural steel, designed to cure rapidly under standard heat conditions. The launch supports broader adoption of waterborne systems in spray-applied applications where throughput and compliance are key. It also strengthens PPG’s position in fast-cure, lower-VOC coating platforms that align with tightening emissions requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the aerosol paints market covers ready-to-spray paints and coatings sold in pressurized cans and applied through an actuator nozzle for coloring, protection, and surface touch-ups across consumer and industrial use.

Scope exclusions: We exclude bulk architectural wall paints sold in pails, spray equipment hardware, and aerosol propellants sold as standalone chemicals.

Segmentation Overview

- By Resin

- Acrylic

- Epoxy

- Polyurethane

- Alkyd

- Other Resins

- By Technology

- Solvent-borne

- Water-borne

- By End-User Industry

- Automotive

- Architectural

- Wood and Packaging

- Transportation

- Do-It-Yourself (DIY)

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand context and the operating constraints that shape aerosol paint consumption. We reviewed public statistics and technical references such as U.S. EPA VOC rules and state-level air quality guidance, Eurostat trade and production tables, UN Comtrade shipment trends for relevant paint and coating codes, and customs and tariff schedules that signal cross-border movement.

To translate these signals into a usable model, we also checked association publications and standards material such as coatings industry bodies, safety and labeling requirements, and peer-reviewed papers on solvent-borne and water-borne formulations and resin behavior. Public company filings, investor presentations, and trusted press coverage helped us understand capacity additions, channel focus, and product mix changes, which are then tested against a paid subscription used for company financials and another for patent and innovation activity. These desk sources are illustrative only, and many additional references were used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on validating what the desk sources cannot show cleanly, especially application mix shifts, average selling price movement, and how regulations are changing product portfolios. We spoke with participants across the value chain such as manufacturers, distributors, retailers, and end users in DIY, automotive refinish, and light industrial maintenance, and we made sure coverage included the major consuming regions so assumptions were checked from more than one angle.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 46% |

| Mid tier: 56% | Functional/Unit leaders: 37% | EMEA: 30% |

| Smaller Players: 19% | Managers: 51% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down reconstruction that links coatings and aerosol usage indicators to an addressable demand pool, and then narrows it to aerosol paint formats by checking regional production and trade flows and the likely share going into spray can delivery. Once the country and regional totals were built, selective bottom-up approximations were used to keep the value in a realistic band, including sampled price checks by can size and finish, channel mix checks, and supplier-side capacity and product mix discussions.

Key inputs in the model include automotive touch-up and refinish activity, DIY and home improvement participation trends, resin and solvent-borne versus water-borne technology shift signals driven by VOC compliance, and import and export movement for paints and coatings that typically track availability and pricing pressure. Where a clean volume series was missing, gaps were handled by using nearby proxy indicators such as trade changes, construction maintenance intensity, and expert-validated share assumptions, which were then stress-tested across regions.

For forecasting, we primarily used scenario analysis supported by a light multivariate regression layer where data series were consistent, so the outlook reflects how demand reacts to macro cycles and regulatory tightening without overfitting. Assumptions on pricing were adjusted using expected raw material pass-through timing and observed can-format price bands discussed in interviews.

Data Validation & Update Cycle

Outputs were validated by comparing modeled demand with independent signals such as trade direction, regulatory timelines, and realistic application intensity in key end-use areas, before the totals were finalized. Variance checks were run across regions and years, and any sharp jumps were reviewed back to the driver level so the cause was understood and documented.

A second analyst review is completed before sign-off, and re-contact is triggered when an assumption drives a large swing versus prior-year behavior or when a new policy or capacity change is identified. Reports are refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery review so clients receive the latest view.

Mordor Intelligence's Aerosol Paints Market Size Compared With Other Published Estimates

Published market values for aerosol paints often do not match, even when the topic name looks the same, because the scope boundary is set differently and the base year and currency treatment are not aligned. Differences also come from how companies treat adjacent items like broader paints and coatings delivered through other packaging formats, and whether they include downstream retail markups.

By tracking aerosol can-only revenue and refreshing key inputs with regional trade checks and VOC-driven mix shifts, Mordor Intelligence keeps the total tied to pressurized paint formats rather than wider coatings demand that can inflate the number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.18 B (2025) | |

| Global Consultancy A | USD 281.01 M (2024) | Uses an earlier base year and a narrower counted revenue pool in practice, which can happen when only specific resin and application slices are captured and the rest of the aerosol paint mix is not fully normalized. |

| Industry Publisher B | USD 286.10 M (2025) | Reports in million USD and often applies a tighter definition of aerosol paints, which can exclude parts of industrial maintenance and transportation touch-up demand and can also differ on whether channel markups are included. |

The spread in the table is mainly explained by scope and counting rules, not by a disagreement that demand exists. When the addressable market is anchored to pressurized paint cans and then cross-checked through trade signals, application intensity, and realistic price bands, the resulting number is easier to trace, repeat, and update year over year.

Key Questions Answered in the Report

What is the current value of the aerosol paints market, and how fast is it growing?

The aerosol paints market size stands at USD 1.24 billion in 2026 and is projected to reach USD 1.60 billion by 2031, advancing at a 5.32% CAGR.

Which region leads global demand for aerosol spray coatings?

Asia-Pacific holds 45.47% of the 2025 global volume, driven by rapid housing construction in China and India.

Why do solvent-borne aerosol paints still dominate amid stricter VOC rules?

They dry faster, adhere better to non-porous or cold substrates, and allow fine control over flow and leveling, benefits that outweigh regulatory compliance costs in many industrial and automotive jobs.

How is the DIY channel reshaping sales strategies?

Average ticket sizes are shrinking while purchase frequency rises; retailers respond with project-specific bundles and expanded color decks available through e-commerce and click-and-collect models.

Which new technology segment offers the highest price premium?

Nano-ceramic direct-to-metal aerosol sprays command higher prices because they combine corrosion protection and insulation in a single coat, cutting maintenance downtime.

Page last updated on: