Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.31 Billion |

| Market Size (2026) | USD 3.44 Billion |

| Market Size (2031) | USD 4.17 Billion |

| Growth Rate (2026 - 2031) | 3.91% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Thermal Spray Market Analysis by Mordor Intelligence

The Europe Thermal Spray Market size was valued at USD 3.31 billion in 2025 and is estimated to grow from USD 3.44 billion in 2026 to reach USD 4.17 billion by 2031, at a CAGR of 3.91% during the forecast period (2026-2031). Coating service providers are increasingly adopting outcome-linked contracts, emphasizing rewards for turbine uptime and implant longevity. This shift is largely facilitated by the IIoT functions integrated into Oerlikon’s Surface Two™ platform. While combustion-based processes maintain the majority share, it is the HVOF and HVAF methods that provide the dense carbide layers essential for wind-turbine blade rebuilds and oil-and-gas valve refurbishments. As OEMs pursue tighter tolerance bands for next-generation aero-engines and electric-vehicle powertrains, there is a notable surge in capital spending on automated spray cells. Although rare-earth supply constraints and new ESG regulations on methane fuel present challenges in procurement, they simultaneously create opportunities for nickel-free powders and hydrogen-ready equipment.

Key Report Takeaways

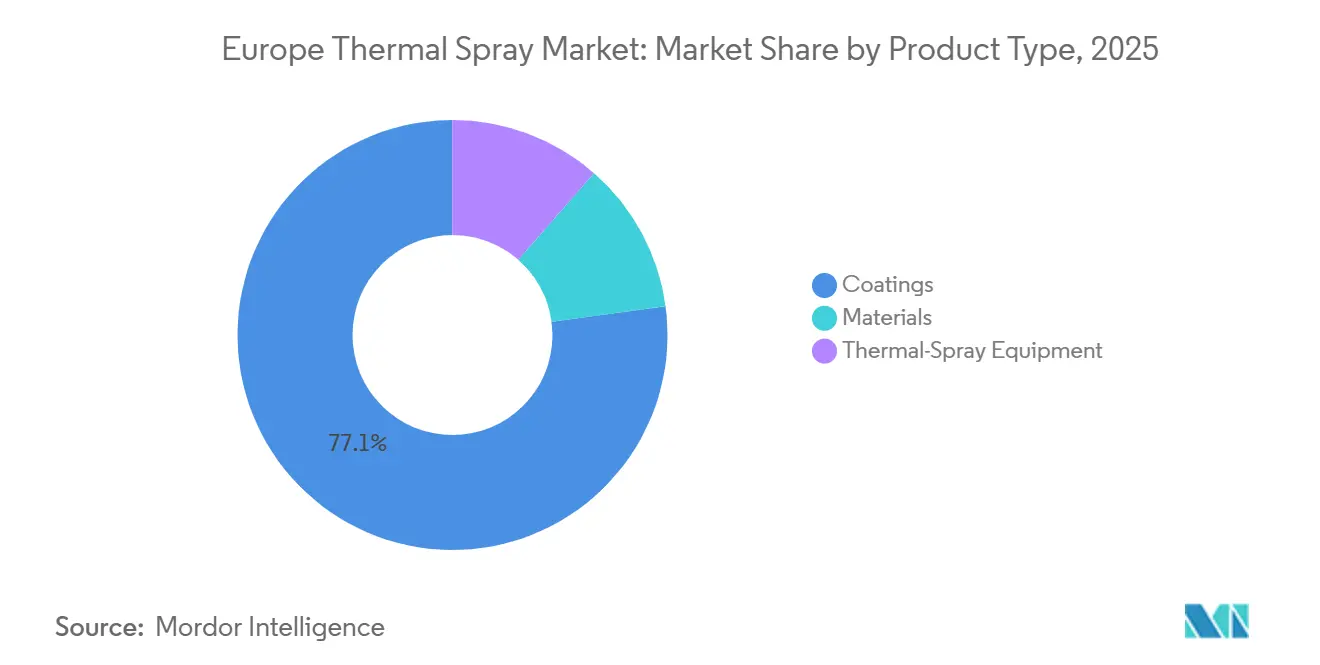

- By product category, coatings held 77.13% of the European thermal spray market share in 2025, while thermal spray equipment is projected to record the fastest 3.95% CAGR (2026-2031).

- By process, combustion methods commanded 72.11% of the European thermal spray market size in 2025 and are forecast to expand at a 4.12% CAGR (2026-2031).

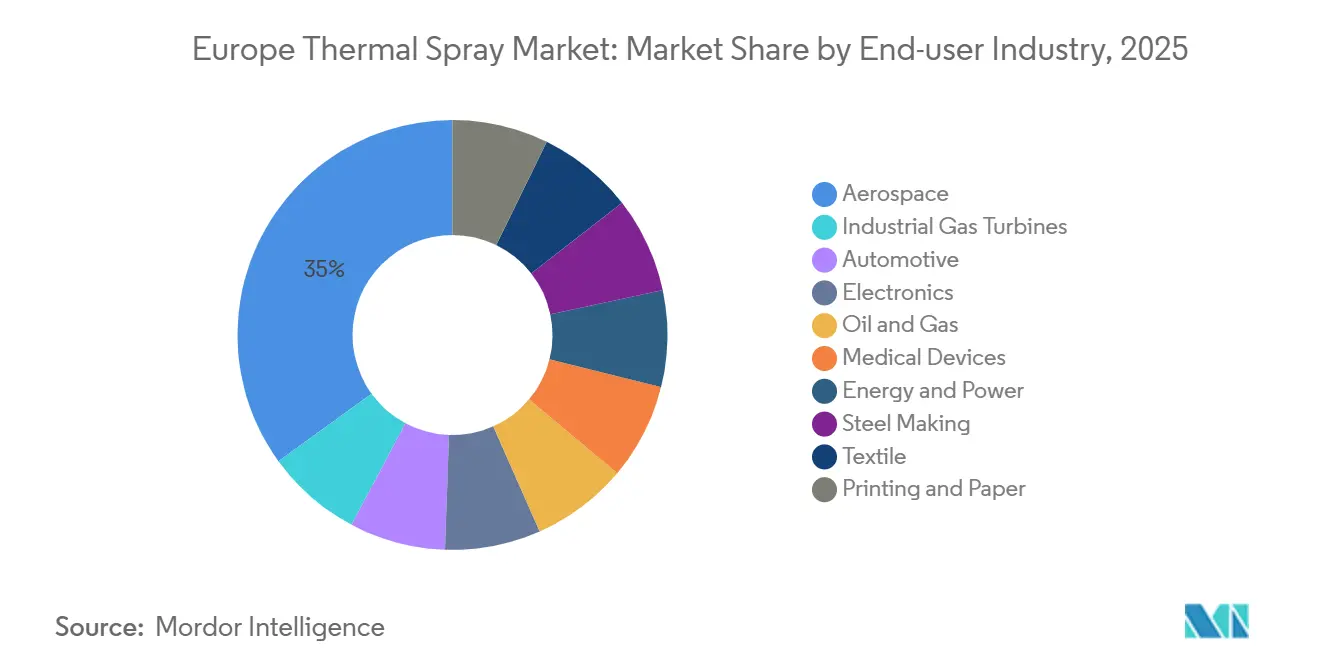

- By end-user, the aerospace sector led with a 34.99% revenue share in 2025; electronics is poised to deliver the highest 3.96% CAGR (2026-2031).

- By geography, Germany accounted for the fastest 4.06% CAGR, while the Rest of Europe represented 33.37% of the European thermal spray market size in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Thermal Spray Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Medical-grade Ti and HA implant coatings | +0.6% | Germany, France, Italy | Medium term (2-4 years) |

| EU decarbonization mandates for turbines | +1.2% | EU-wide, focus on Germany, Netherlands, Denmark | Long term (≥ 4 years) |

| HVOF ceramic coatings for EV brake rotors | +0.9% | Germany, France, United Kingdom | Short term (≤ 2 years) |

| AI-optimized spray-path algorithms | +0.5% | Germany, France, Sweden | Medium term (2-4 years) |

| Surging demand for wear-resistant coatings in European Union wind-turbine rebuilds | +0.7% | Nordics, Germany, Spain, United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Medical-Grade Ti and HA Coatings for Implants

With Europe's over-65 population set to reach nearly one-third by 2030, orthopedic and dental implant manufacturers are increasingly adopting plasma-sprayed titanium and hydroxyapatite layers. These advancements are notably shortening healing times and diminishing the necessity for revision surgeries. The evolution of suspension plasma spray now adeptly handles sub-micron HA powders, closely resembling natural bone minerals and adhering to the rigorous ISO 13779-2 certification standards. While reforms tying hospital payments to implant longevity have increased demand, a worrisome trend surfaces: over half of titanium powder is still procured from merely two North American suppliers, amplifying supply vulnerabilities.

EU Decarbonization Mandates for Turbines and Boilers

Operators, under the EU Clean Industrial Deal, face a 2030 deadline for significant emissions reductions. In response, they are retrofitting turbines with gadolinium- and lanthanum-zirconate thermal barrier coatings (TBCs), which are designed to withstand specific volumes of hydrogen blends. Early tests in Dutch combined-cycle plants have highlighted notable durability enhancements. Furthermore, the Energy Performance of Buildings Directive, which emphasizes high boiler efficiency, is accelerating the replacement cycle for MCrAlY bond coats.

Rapid Uptake of HVOF Ceramic Coatings for EV Rotors

Beginning in 2027, Euro 7 regulations will impose strict limits on brake-wear particles, prompting OEMs to transition to HVOF tungsten-carbide rotors. These advanced rotors, already featured in Porsche’s Taycan, not only reduce dust emissions but also offer a longer lifespan. In parallel, Zircotec has introduced a zirconia over-coating that significantly lowers rotor temperatures[1]Zircotec, “Thermal Barrier Coatings for Automotive Applications,” zircotec.com. This innovation enables lighter rotor designs, enhancing the EV range by several kilometers per charge.

Surging Demand for Wear-Resistant Coatings in Wind-Turbine Rebuilds

Offshore wind blades, once they reach the 12-year mark, require erosion-resistant recoats. High-Velocity Oxy-Fuel (HVOF) carbide layers can restore these blades, ensuring they retain their aerodynamic efficiency for up to two decades, even under tip speeds of 90 meters per second[2]VTT, “Thermal Spray Research Publications,” cris.vtt.fi. To improve logistics, Metallisation and GTV have developed mobile-spray units, which are now operational at service ports in the North Sea.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX of robot-integrated spray cells | -0.8% | EU-wide, acute in Southern and Eastern Europe | Short term (≤ 2 years) |

| YSZ and rare-earth oxide supply tightness | -0.6% | EU-wide, dependency on China | Medium term (2-4 years) |

| ESG phase-out of methane in spray booths | -0.4% | Germany, Netherlands, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX of Robot-Integrated Spray Cells

Small shops often find automated cells prohibitively expensive, as they are unable to distribute the costs over sufficient sales. Leasing offers a solution, converting a significant upfront cost (capital expenditure - CAPEX) into a more digestible ongoing expense (operational expenditure - OPEX). However, this convenience comes at a price, as users become tethered to costly consumables, which squeeze their profit margins. Adding to the financial stakes, the swift transition from cold-spray systems to the newer HVAF technology, just a few years apart, amplifies the risks of rapid obsolescence.

Supply Tightness of YSZ and Rare-Earth Oxides

In 2025, YSZ prices increased significantly, and lead times extended to approximately 16 weeks. In response, Höganäs introduced nickel-free Amperit 685 powders, which reduce embodied CO₂ significantly. However, the adoption of these powders has faced delays due to the aerospace qualification cycles, which span approximately 24 months.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Equipment Gains Speed as Automation Intensifies

In 2025, coatings took center stage in the European thermal spray market, securing a dominant 77.13% share. This dominance highlights the consumable nature of coatings and the aerospace sector's regular overhaul cycles. Meanwhile, the equipment segment is on an upward trajectory, with projections indicating a 3.95% CAGR growth during the forecast period of 2026–2031. This anticipated growth is fueled by OEMs' initiatives to digitize spray cells and integrate real-time diagnostics. The equipment segment of Europe's thermal spray market is set to benefit from Oerlikon's predictive-maintenance modules. These advanced modules not only trigger automatic spare-part orders but also boost aftermarket revenue. Positioned between coatings and equipment, materials are gaining momentum, thanks in part to Höganäs' recent introductions of Amperit 678 and 685. These new materials resonate with the industry's pivot towards reducing nickel and cobalt, a shift driven by REACH mandates.

Price dynamics in the European thermal spray sector showcase a clear disparity. Aerospace TBC powders fetch premium prices, while industrial tungsten-carbide grades are priced more modestly. Additionally, dust-collection systems and gravimetric feeders have evolved from secondary tools to vital compliance instruments. This transformation is primarily attributed to ISO 45001 enforcement, which emphasizes the capture of sub-micron particulates.

By Process Type: Combustion Maintains Dominance Despite ESG Pressure

In 2025, combustion routes led the European thermal spray market, capturing 72.11% of the market size and are projected to expand at a 4.12% CAGR through the forecast period of 2026–2031. Supersonic HVOF streams, which propel particles at speeds of 600–800 m/s, achieve coatings with less than 1 percent porosity. This precision remains a challenge for electric plasma, particularly with carbide deposits. HVAF technology is making significant advancements in the refurbishment of oil-and-gas valves by cutting oxygen costs by half and reducing oxide content. On the other hand, electric methods, such as APS, VPS, and arc spray, are essential for applications that require ultra-clean microstructures, including YSZ TBCs and semiconductor chamber components. Cold spray, known for its solid-state and low-heat properties, is carving a niche in the additive repair of aluminum aero-structures.

Hybrid systems are set to transform the industry. For instance, Castolin Eutectic’s XupersoniClad, which combines HVAF with laser remelt, achieves near-zero porosity in a single pass, significantly reducing cycle time. Such innovations could potentially reshape the distribution of market shares among various process families in the European thermal spray industry.

By End-User Industry: Electronics Emerges as the Fastest Climber

In 2025, Europe's thermal spray market saw the aerospace sector take the lead with a commanding 34.99% share. This surge was largely attributed to innovations like the UltraFan and RISE engines, which have successfully pushed turbine inlet temperatures beyond 1,600 °C. Meanwhile, the electronics sector is on track to expand at a 3.96% CAGR during the forecast period of 2026–2031. This growth is spurred by breakthroughs such as plasma-sprayed yttria liners. These liners not only extend the lifespan of semiconductor etch chambers but also boost productivity, adding two to three extra wafer starts per tool each month. Hydrogen-ready coatings are enhancing the performance of industrial gas turbines. In the automotive realm, there is a swift shift towards carbide-coated brake rotors, a move largely driven by the stringent Euro 7 regulations. Medical devices are benefiting from plasma-sprayed HA layers, which expedite osseointegration. Simultaneously, the offshore wind sector is actively pursuing erosion-resistant treatments for turbine leading edges.

Additionally, Europe's thermal spray industry is making significant inroads into the oil-and-gas sector, with a particular focus on downhole tools. In this arena, HVOF tungsten-carbide coatings are playing a pivotal role, notably extending the life of valve seats. Even niche segments, such as printing rolls and components in papermills, are embracing cold-spray repairs, leading to a significant reduction in downtime.

Geography Analysis

In 2025, Germany led with a CAGR of 4.06% as Fraunhofer rolls out a spray-center network. Meanwhile, automotive OEMs are swapping hard-chrome rotors for HVOF carbide versions in anticipation of Euro 7. In the UK, aerospace qualifications are centered around Rolls-Royce and GKN, driving up demand for NADCAP-grade HVOF and plasma coatings. France is utilizing the SAFIR platform, equipped with four spray technologies and two robotic booths, to advance hydrogen-energy parts from TRL 1-7.

Italy and Spain are honing in on coating services for industrial and wind turbines, with CTME pushing forward high-entropy alloy research, backed by EXC_HEAs funding. The Nordic nations, while leading in offshore wind, are also pioneering HVAF and cold-spray research and development at University West, achieving notable fatigue-life enhancements over standard NiCoCrAlY systems. Eastern Europe is carving out a niche as a cost-effective hub for tier-2 automotive supplies, but its struggle with NADCAP accreditation limits its aerospace ambitions.

Rest of Europe, which commands 33.37% of the continent's thermal spray market (2026-2031), there's a diverse landscape: Poland's automotive sector is integrating HVOF cells for transmissions, Belgium's De Beleyr-Engineering is attracting marine and chemical clientele, and the Netherlands is championing hydrogen-fuel HVOF as part of its national agenda. Switzerland's med-tech sector is emphasizing high-purity plasma coatings, not just for implants but also for watch tooling, bolstering its reputation in precision manufacturing.

Competitive Landscape

The European thermal spray market is moderately fragmented. On the research front, consortia such as Fraunhofer IKTS and CTME are at the forefront, developing AI-driven process controls. Their innovations have led to significant reductions in scrap rates, a challenge many smaller shops struggle to afford. However, the industry faces challenges; regulatory hurdles, notably REACH's restrictions on chromium trioxide and looming methane regulations, tend to benefit those with substantial research and development budgets.

Europe Thermal Spray Industry Leaders

OC Oerlikon Management AG

Bodycote

CASTOLIN EUTECTIC

Saint-Gobain

Hoganas AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Scotland-based ATL Turbine Services expanded its technological capabilities by investing in the Surface Two thermal spray system from OC Oerlikon Management AG, enabling the delivery of high-performance, precision-engineered coating solutions for turbine components across the aerospace, energy, and industrial sectors.

- January 2025: OC Oerlikon Management AG expanded its facility in Salzgitter, Germany, to offer advanced thermal spray services for large, heavy rollers. The facility was equipped with the MultiCoat 5 system, enabling self-sufficient operations and supporting HVOF, APS, and flame spray technologies for clients in the steel, battery, and printing industries.

Europe Thermal Spray Market Report Scope

Thermal spray is an industrial coating process that utilizes high-velocity heat to melt or soften materials, then sprays them onto a surface, creating a protective or functional layer. This technique applies metallic, ceramic, or polymer coatings to enhance properties like wear resistance, corrosion protection, and thermal insulation, often used to restore worn components or add new surface properties.

The European thermal spray market is segmented by product type, process type, end-user industry, and geography. By product type, the market is segmented into coatings, materials, and thermal-spray equipment. By process type, the market is segmented into combustion and electric energy. By end-user industry, the market is segmented into aerospace, industrial gas turbines, automotive, electronics, oil and gas, medical devices, energy and power, steel making, textile, and printing and paper. The report also covers the market size and forecasts for the market in 6 countries across the region. For each segment, the market sizing and forecasts are done based on value (USD).

By Product Type

| Coatings | |||

| Materials | Coating Materials | Powders | Ceramics |

| Metals | |||

| Polymer | |||

| Other Coating Materials | |||

| Wires/Rods | |||

| Other Materials | |||

| Thermal-Spray Equipment | Thermal Spray Coating System | ||

| Dust Collection Equipment | |||

| Spray Gun and Nozzle | |||

| Feeder Equipment | |||

| Spare Parts | |||

| Noise-reducing Enclosure | |||

| Other Thermal Spray Equipment | |||

By Process Type

| Combustion |

| Electric Energy |

By End-user Industry

| Aerospace |

| Industrial Gas Turbines |

| Automotive |

| Electronics |

| Oil and Gas |

| Medical Devices |

| Energy and Power |

| Steel Making |

| Textile |

| Printing and Paper |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| NORDICS Countries |

| Russia |

| Rest of Europe |

| By Product Type | Coatings | |||

| Materials | Coating Materials | Powders | Ceramics | |

| Metals | ||||

| Polymer | ||||

| Other Coating Materials | ||||

| Wires/Rods | ||||

| Other Materials | ||||

| Thermal-Spray Equipment | Thermal Spray Coating System | |||

| Dust Collection Equipment | ||||

| Spray Gun and Nozzle | ||||

| Feeder Equipment | ||||

| Spare Parts | ||||

| Noise-reducing Enclosure | ||||

| Other Thermal Spray Equipment | ||||

| By Process Type | Combustion | |||

| Electric Energy | ||||

| By End-user Industry | Aerospace | |||

| Industrial Gas Turbines | ||||

| Automotive | ||||

| Electronics | ||||

| Oil and Gas | ||||

| Medical Devices | ||||

| Energy and Power | ||||

| Steel Making | ||||

| Textile | ||||

| Printing and Paper | ||||

| By Geography | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| NORDICS Countries | ||||

| Russia | ||||

| Rest of Europe | ||||

Key Questions Answered in the Report

How big will the European thermal spray market be by 2031?

It is forecast to reach USD 4.17 billion by 2031, expanding at a 3.91% CAGR from USD 3.44 billion in 2026.

Which segment is growing fastest within Europe for thermal spray?

Equipment is projected to rise at a 3.95% CAGR (2026-2031) as manufacturers automate spray cells to meet tighter tolerances.

Why are HVOF coatings popular for EV brake rotors in Europe?

They cut brake-wear dust by up to 90% and help automakers satisfy Euro 7 particulate limits effective 2027.

What is the main supply risk facing European thermal spray producers?

Tight availability and longer lead times for yttria-stabilized zirconia and rare-earth oxides are crucial to turbine coatings.

Which European country will post the highest growth rate in thermal spray demand?

Germany, driven by automotive brake-rotor coatings and new Fraunhofer research investments, is set for a 4.06% CAGR (2026-2031).

Page last updated on: