China Digital Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

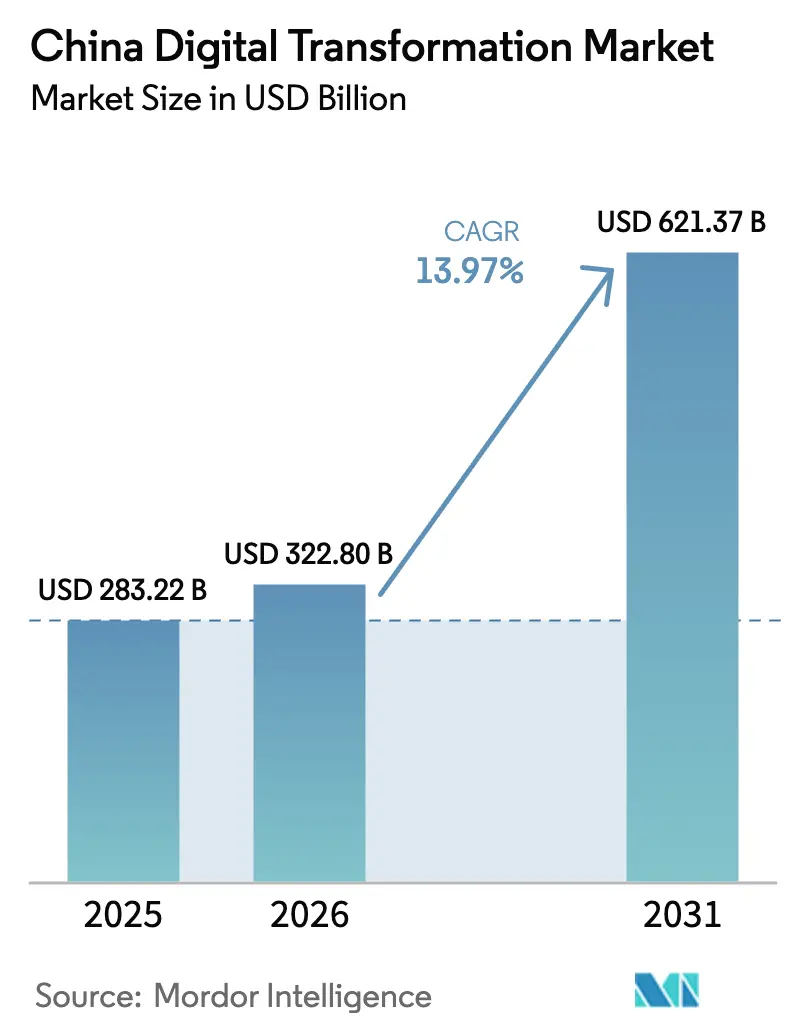

| Base Year Market Size (2025) | USD 283.22 Billion |

| Market Size (2026) | USD 322.8 Billion |

| Market Size (2031) | USD 621.37 Billion |

| Growth Rate (2026 - 2031) | 13.97% CAGR |

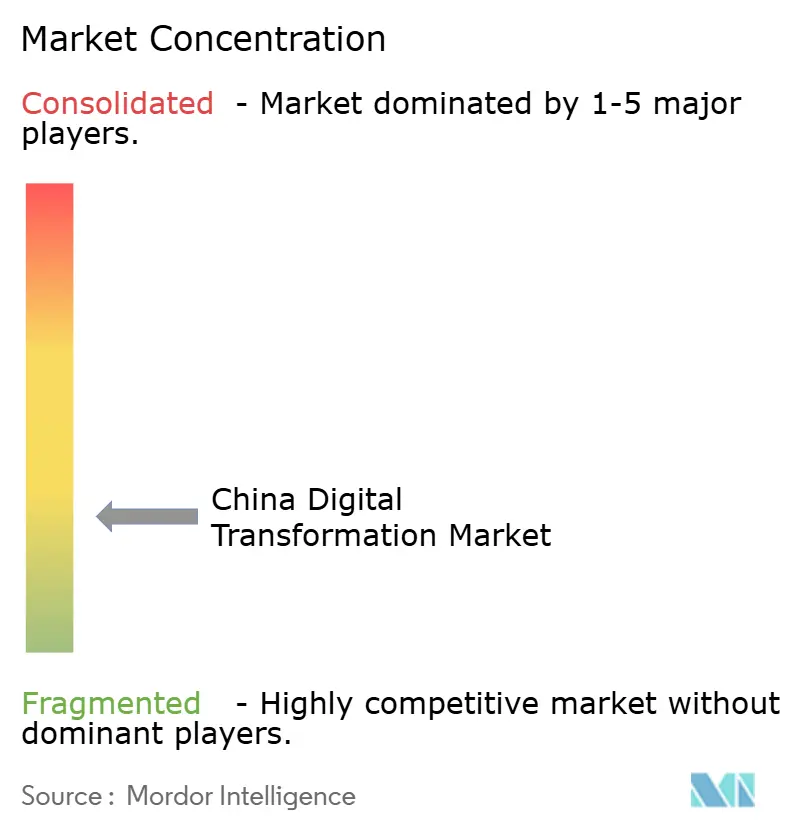

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Digital Transformation Market Analysis by Mordor Intelligence

The China Digital Transformation Market size is expected to grow from USD 283.22 billion in 2025 to USD 322.8 billion in 2026 and is forecast to reach USD 621.37 billion by 2031 at 13.97% CAGR over 2026-2031. Expansion is anchored in the national Digital China program, sustained 5G and forthcoming 6G roll-outs, and a data economy that contributed 41.5% of GDP in 2024.[1]刘崇懿, “AI-powered hospitals to offer faster, expanded care,” China Daily, chinadaily.com.cn Large-scale infrastructure spending by cloud leaders, led by Alibaba’s RMB 380 billion roadmap, strengthens core compute capacity and lowers adoption barriers. Provincial data-exchange pilots monetize data assets, while edge-ready 5G networks accelerate real-time use cases. Manufacturing, healthcare, and public services adopt AI-cloud architectures, creating persistent demand for platform and integration services across the China digital transformation market.

Key Report Takeaways

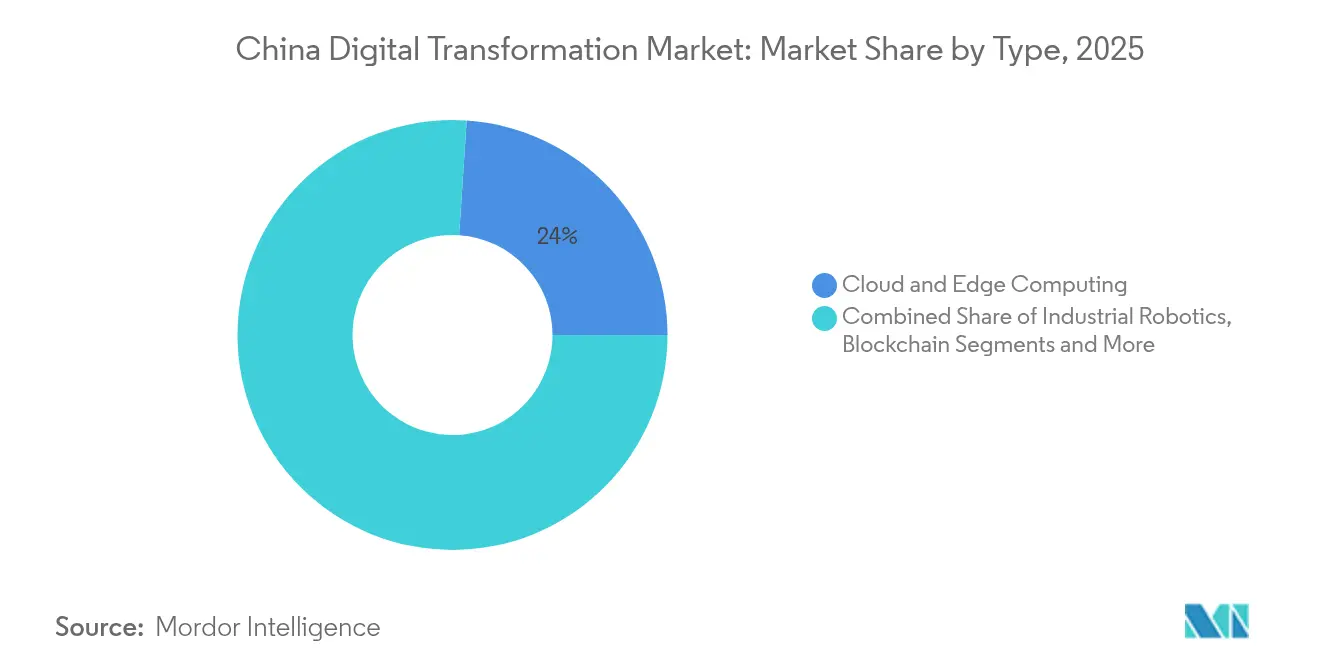

- By technology, Cloud & Edge Computing led with 23.95% revenue share in 2025, while Generative AI Platforms are projected to expand at 23.30% CAGR to 2031.

- By end-user industry, Manufacturing held 21.45% of the China digital transformation market share in 2025, and Healthcare is forecast to grow at 18.20% CAGR through 2031.

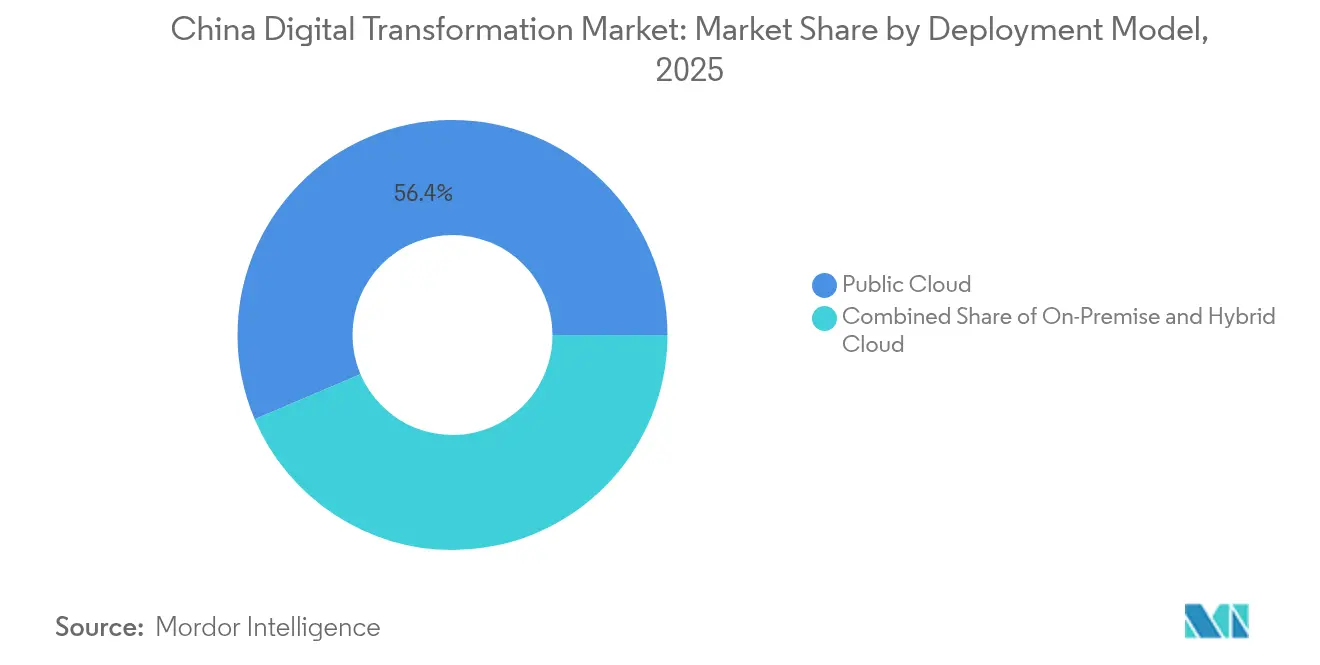

- By deployment model, the Public Cloud segment accounted for 56.40% share of the China digital transformation market size in 2025, whereas Hybrid Cloud is set to rise at 20.20% CAGR to 2031.

- By enterprise size, Large Enterprises held 59.20% share in 2025 and Small & Medium Enterprises are registering the quickest expansion at 18.74% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

National developments in China connect differently with activity unfolding across other parts of the world. In the global digital transformation (dx) market coverage, Mordor Intelligence integrates these into a single analytical framework.

China Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government “Digital China” & New Infrastructure Spend | +3.2% | Nationwide, strongest in East China | Long term (≥ 4 years) |

| AI-Cloud Convergence Accelerating Enterprise Uptake | +2.8% | Nationwide, highest in East & Southwest China | Medium term (2-4 years) |

| Industrial Internet & Smart Manufacturing Imperatives | +2.1% | Manufacturing hubs across China | Long term (≥ 4 years) |

| Low-/No-Code Platforms Unlocking SME Adoption | +1.9% | Nationwide, focus on rural & tier-2 cities | Medium term (2-4 years) |

| Provincial data-exchange markets monetize data | +1.6% | Regional pilots scaling nationally | Long term (≥ 4 years) |

| Carbon-neutrality goals drive digital efficiency | +1.4% | Industrial regions nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government “Digital China” & New Infrastructure Spend

Digital China elevates technology modernization to a policy mandate. The 2025 Digital China Action Plan channels RMB 300 billion treasury bonds into network upgrades and data-market construction, while 4.19 million 5G base stations already provide broad coverage.[2]Global Times Staff, “China plans to upgrade its 5G network, accelerate 6G innovation, and spruce up construction of national data infrastructure,” Global Times, globaltimes.cn Sichuan’s fiscal reform blueprint mirrors the national push by aligning provincial tax incentives with smart city projects. The coordinated investment climate compresses deployment timeframes and guarantees a multi-year pipeline for cloud, edge, and AI suppliers inside the China digital transformation market.

AI-Cloud Convergence Accelerating Enterprise Uptake

Enterprises converge AI and cloud to create self-reinforcing adoption loops. Tencent invested RMB 18.9 billion in R&D during Q1 2025, recording double-digit cloud revenue growth as AI tooling drove new workloads.[3]黄尘, “Tencent Q1 R&D investment rises 21%,” TechNode, technode.com Alibaba’s USD 52 billion data-center expansion attaches AI inference services to its global cloud fabric. Manufacturers deploy AI-enabled welding and inspection, gaining 40% productivity lifts. The model reduces latency, boosts utilization, and deepens cloud commitment, thereby lifting revenue across the China digital transformation market.

Industrial Internet & Smart Manufacturing Imperatives

The Industrial Internet shifts from optional modernization to competitive survival. Nearly 10,000 digital workshops integrate IoT sensors with MES platforms to create closed-loop optimization.[4]Mark Andrews, “SAIC falls, BYD is the new king,” Car News China, carnewschina.com BYD’s vertically integrated plants, enabled by digital twins, achieved 45.32% year-over-year sales growth in 2024, underscoring the production gains unlocked by data-driven orchestration. Smart manufacturing also supports carbon-neutrality pledges through energy analytics, positioning factories as prime customers in the China digital transformation market.

Low-/No-Code Platforms Unlocking SME Adoption

Low-code ecosystems lower skill thresholds and compress rollout cycles, closing the capability gap for SMEs. National support programs subsidize cloud credits and professional training that equip SME founders with rapid development. A three-year workforce plan trains digital engineers and offers housing incentives to lure talent into smaller cities. SMEs apply composable apps to digitize finance tasks and logistics, reducing upfront costs and spurring a 19.00% CAGR segment contribution to the China digital transformation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security & Data-Localization Regulations | -1.8% | Nationwide, affects cross-border business | Short term (≤ 2 years) |

| Advanced-Node Chip Supply Constraints | -2.3% | Nationwide, impacts high-tech sectors | Medium term (2-4 years) |

| Shortage of high-end digital talent | -1.5% | Nationwide, acute in tier-1 cities | Medium term (2-4 years) |

| Legacy IT fragmentation within SOEs | -1.2% | Nationwide, concentrated in traditional industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-security & Data-Localization Regulations

The Network Data Security Management Regulations, effective January 2025, impose annual risk audits and tighter cross-border transfer approvals. Multinationals must file security assessments, while domestic platforms appoint dedicated data-security officers. Compliance drives demand for indigenous security suites yet slows certain SaaS rollouts, trimming near-term velocity in the China digital transformation market.

Advanced-Node Chip Supply Constraints

Domestic semiconductor funding of CNY 344 billion expands foundry capacity, yet sub-7 nm volumes remain limited. AI model training requires high-end GPUs that still rely on external supply chains. Tech majors stockpile inventory and optimize algorithms to cut compute intensity, but allocation pressures delay edge AI programs in the China digital transformation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Cloud & Edge Computing as the Core Infrastructure

Cloud & Edge Computing held 23.95% of the China digital transformation market size in 2025, reflecting widespread preference for hybrid architectures that balance latency and compliance. Huawei Cloud recorded 77% revenue increase and a 106% upsurge in hybrid workloads, illustrating enterprise momentum toward sovereign infrastructure. Edge nodes extend compute to factory floors and traffic systems, driving real-time analytics for 2.57 billion IoT terminals.

Generative AI Platforms are scaling fastest at 23.30% CAGR to 2031 as large language models enable code generation, content creation, and autonomous decision tools. Enterprises adopt off-the-shelf models and pursue fine-tuning to protect proprietary data, while government grants encourage open-source alternatives to reduce dependence on foreign IP. Analytics, AI & ML suites integrate with existing ERP stacks, pushing diagnostic accuracy in healthcare beyond 93%, and boosting predictive maintenance accuracy in manufacturing. Cybersecurity tools embed AI engines to correlate events, decreasing manual triage. Blockchain underpins traceability for food safety and cross-border trade. Additive manufacturing remains niche but gains traction in aerospace prototypes and dental devices inside the China digital transformation market.

By End-User Industry: Manufacturing Dominates, Healthcare Accelerates

Manufacturing captured 21.45% of the China digital transformation market share in 2025. Digital twins and robotic cells in BYD factories shorten model cycles and helped deliver 419,426 vehicle sales in a single month. Predictive analytics and visual inspection reduce scrap and energy consumption, aligning with carbon-neutrality objectives.

Healthcare is advancing at 18.20% CAGR, catalyzed by the world’s first fully AI hospital launched by Tsinghua University which operates with 42 AI doctors and 4 AI nurses, serving 3,000 patients daily. Virtual consultations mitigate physician shortages in rural areas, while imaging algorithms cut diagnostic turnaround. BFSI, telecom, and government services exploit automation and digital identity to enhance citizen engagement. Energy utilities fit smart grids with IoT sensors, improving outage detection and load balancing across the China digital transformation market.

By Deployment Model: Hybrid Cloud Solves Compliance Pain Points

Public Cloud dominated with 56.40% of revenue in 2025 as enterprises sought elastic capacity without capital commitments. Alibaba Cloud’s USD 52 billion infrastructure push links domestic regions with overseas zones to meet global expansion requirements.

Hybrid Cloud is forecast to grow at 20.20% CAGR. Organizations segment workloads, placing sensitive data in private regions while using public environments for AI training. Edge computing nodes process machine-vision tasks on site before syncing distilled insights, enhancing resilience and meeting data-localization mandates. On-premise models persist in finance and defense, yet even conservative sectors pilot containerization to ease future cloud migration. As a result, hybrid strategies form the backbone of scaling paths inside the China digital transformation market.

By Enterprise Size: SMEs Close the Transformation Gap

Large Enterprises generated 59.20% revenue in 2025, supported by integrated program portfolios that link R&D, supply chain, and customer experience. Tencent’s RMB 180.02 billion quarterly revenue underscores platform power once AI tools are embedded in cloud and advertising. Continuous investment funds proprietary models and patent creation that anchor long-term competitiveness in the China digital transformation market.

SMEs are advancing at 18.74% CAGR, facilitated by low-code studios and subsidized cloud credits. National digital inclusion programs extend credit assessment engines that lower borrowing costs, which lifts innovation intensity in provincial clusters. Workforce skilling programs target 1 million engineers by 2027, easing capacity bottlenecks. SMEs deploy lightweight ERP and CRM modules first, then layer analytics and RPA to add incremental value, demonstrating a pragmatic path toward parity with larger peers inside the China digital transformation industry.

Geography Analysis

East China maintained 25.60% revenue share in 2025, benefiting from dense technology ecosystems in Shanghai, Hangzhou, and Shenzhen. Joint government–enterprise labs fast-track proof-of-concept trials and create replicable standards that cascade nationwide. The Yangtze River Delta fosters urban–rural integration, extending broadband and e-commerce services into surrounding counties, which enlarges addressable demand in the China digital transformation market. Sustained venture activity and talent inflows keep innovation velocity high, positioning the region as the policy testbed for national digital reforms.

Southwest China is growing at 17.45% CAGR through 2031. The Chengdu-Chongqing economic circle promotes integrated circuit parks and AI incubators, while Sichuan recorded 6% GDP increase in 2024 on the back of technology upgrades. Yibin attracted 34 leading digital enterprises, offering incentives for cloud and blockchain startups. Late-mover advantages permit leapfrogging to modern platforms without legacy constraints, accelerating catch-up inside the China digital transformation market.

Central and Western provinces post steady yet lower trajectories. Policy makers deploy national data exchanges and universal service funds to bridge the digital divide. Northeast pilot programs show that moderate digital-economy density generates the strongest urban–rural integration gains. Continuous fiber rollout, cloud zones, and vocational training are key levers for region-wide uplift, ensuring homogeneous contribution to the China digital transformation market over the forecast horizon.

Mordor Intelligence's coverage of the digital transformation (dx) market extends across other regions including Europe, North America, and Africa, while country-specific intelligence is also available for Japan, India, Poland, United States, Nigeria, and Mexico, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

Competition is intensifying yet remains moderately fragmented. Domestic conglomerates leverage integrated cloud-AI-IoT stacks to lock in clients and expand wallet share. Alibaba, Tencent, and Huawei collectively account for a significant portion of platform revenues, while hundreds of vertical specialists supply sector-specific modules. Chinese inventors filed 38,210 generative AI patents from 2014-2023, contributing 70% of the global total. Patent depth equips incumbents with defensive moats and licensing income across the China digital transformation market.

Strategic activity centers on infrastructure scale-up and AI model improvement. Alibaba’s QwQ-32B model advances cost-efficient inference, driving an 8.39% share rally upon release. Tencent bundles cloud credit with advertising rebates to attract game studios onto its AI toolchain. Huawei integrates Ascend chips and Kunpeng servers with its Stack offering, reducing external dependency while targeting regulated industries inside the China digital transformation market.

White-space opportunities remain in SME solutions, edge AI modules, and data brokerage platforms. Emerging firms such as DeepSeek cut compute costs by 95% against leading global models, lowering entry barriers for mid-tier customers. Government procurement preferences and cybersecurity standards advantage local champions that meet data-sovereignty criteria. As more sectors mandate digitalization, the contest shifts from point products to ecosystem lock-in, shaping the competitive outlook of the China digital transformation industry.

China Digital Transformation Industry Leaders

Alibaba Group

Tencent

Huawei

ZTE Corporation

Baidu

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Alibaba Cloud announced USD 52 billion global infrastructure investment to deploy AI models across overseas data centers.

- June 2025: Hong Kong Cyberport launched a Blockchain and Digital Asset Pilot Funding Scheme offering up to HKD 500,000 per project.

- May 2025: Tencent disclosed RMB 18.9 billion in Q1 2025 R&D outlays, up 21% year over year.

- January 2025: China enforced Network Data Security Management Regulations, mandating annual risk reviews.

China Digital Transformation Market Report Scope

Digital transformation is the process of incorporating digital technologies such as analytics, artificial intelligence, and machine learning, extended reality (XR), Iot, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud and edge computing, and others (digital Twin, mobility, and connectivity) in various end-user industries across the country.

China digital transformation market is segmented by type (analytics, artificial intelligence, and machine learning, extended reality (XR), IoT, industrial robotics, blockchain, additive manufacturing/3d printing, cybersecurity, cloud and edge computing, and others [digital twin, mobility, and connectivity]), end-user industry (manufacturing, oil, gas and utilities, retail & e-commerce, transportation and logistics, healthcare, bfsi, telecom and it, government and public sector, and others).

The market sizes and forecasts are provided in terms of value (USD) for the segments.

| Analytics, AI and ML |

| Generative AI Platforms |

| Internet of Things (IoT) |

| Industrial Robotics |

| Blockchain |

| Additive Manufacturing / 3DP |

| Cybersecurity |

| Cloud and Edge Computing |

| Others |

| Manufacturing |

| Oil, Gas and Utilities |

| Retail and E-commerce |

| Transportation and Logistics |

| Healthcare |

| BFSI |

| Telecom and IT |

| Government and Public Sector |

| Others |

| On-Premise |

| Public Cloud |

| Hybrid Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Type | Analytics, AI and ML |

| Generative AI Platforms | |

| Internet of Things (IoT) | |

| Industrial Robotics | |

| Blockchain | |

| Additive Manufacturing / 3DP | |

| Cybersecurity | |

| Cloud and Edge Computing | |

| Others | |

| By End-User Industry | Manufacturing |

| Oil, Gas and Utilities | |

| Retail and E-commerce | |

| Transportation and Logistics | |

| Healthcare | |

| BFSI | |

| Telecom and IT | |

| Government and Public Sector | |

| Others | |

| By Deployment Model | On-Premise |

| Public Cloud | |

| Hybrid Cloud | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) |

Key Questions Answered in the Report

What is the current value of the China digital transformation market?

The market generated USD 322.8 billion in 2026.

How fast will the China digital transformation market grow through 2031?

It is projected to expand at a 13.97% CAGR, reaching USD 621.37 billion by 2031.

Which technology segment is growing the quickest?

Generative AI Platforms are forecast to rise at a 23.30% CAGR through 2031.

Why is Hybrid Cloud adoption accelerating?

Hybrid designs meet data-localization rules while retaining public cloud elasticity, supporting a 20.20% CAGR.

Which region is outpacing the national average?

Southwest China is advancing at 17.45% CAGR due to targeted provincial initiatives and new industrial clusters.

What regulation most affects cross-border data flows?

The Network Data Security Management Regulations, effective January 2025, introduce strict transfer approvals and annual risk audits.

Page last updated on: