Thailand Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

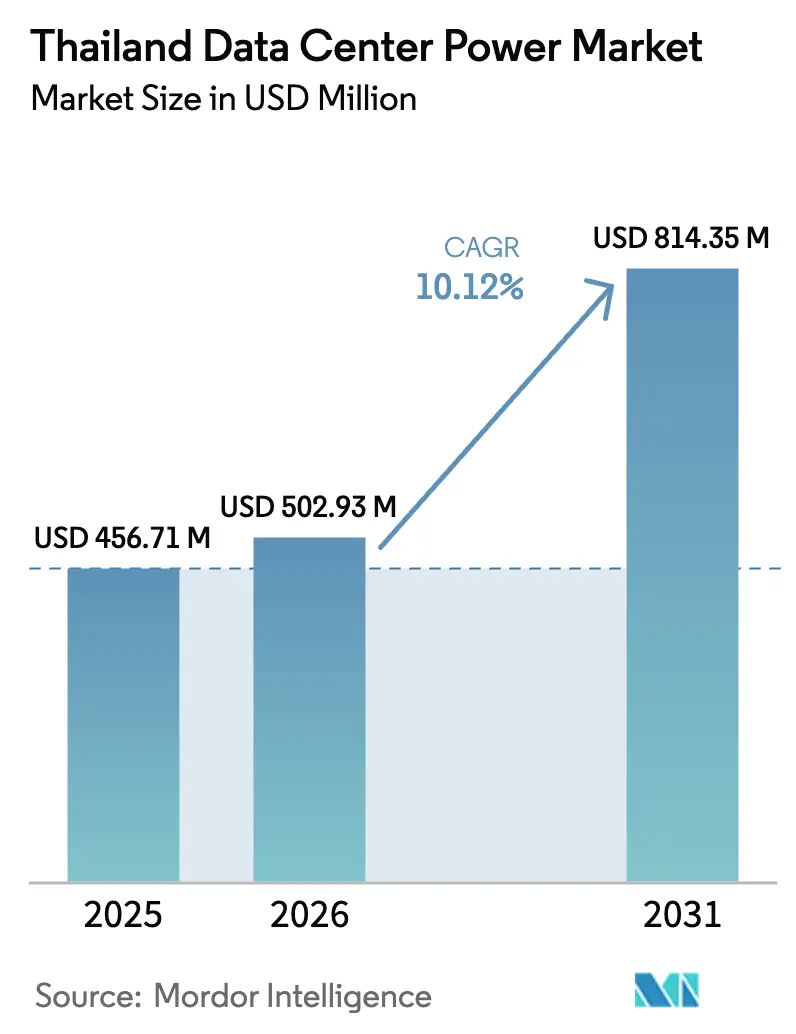

| Base Year Market Size (2025) | USD 456.71 Million |

| Market Size (2026) | USD 502.93 Million |

| Market Size (2031) | USD 814.35 Million |

| Growth Rate (2026 - 2031) | 10.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Data Center Power Market Analysis by Mordor Intelligence

Thailand data center power market size in 2026 is estimated at USD 502.93 million, growing from 2025 value of USD 456.71 million with 2031 projections showing USD 814.35 million, growing at 10.12% CAGR over 2026-2031. Robust hyperscale capital commitments, targeted policy incentives under Thailand 4.0, and an accelerating shift toward AI-intensive workloads underpin demand for resilient electrical infrastructure. The Thailand data center power market is also shaped by ambitious renewable-energy goals, with Thailand targeting renewable electricity by 2040, encouraging operators to integrate on-site solar and battery energy storage. Supply-chain investments from manufacturers of transformers, switchgear, and UPS systems help relieve component shortages, while utility-linked green-power programs lower electricity tariffs and improve sustainability options. Competitive activity concentrates on end-to-end solutions that combine power generation, distribution, and monitoring, because operators want single-source partners capable of delivering Tier III and Tier IV reliability standards.

Key Report Takeaways

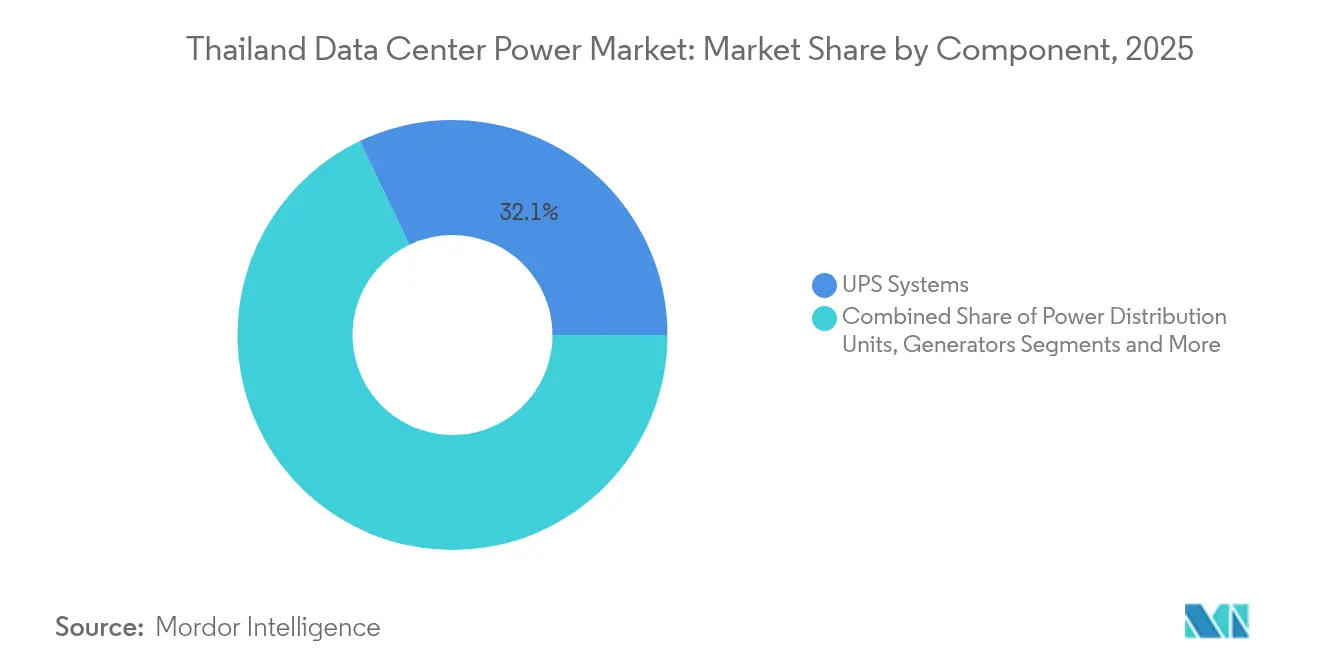

- By component, UPS Systems led with 32.10% of Thailand's data center power market share in 2025; Power Distribution Units are projected to expand at an 10.92% CAGR through 2031.

- By deployment model, Colocation Providers held a 42.35% share of the Thailand data center power market in 2025, whereas Hyperscale/Cloud Service Providers are advancing at a 12.05% CAGR toward 2031.

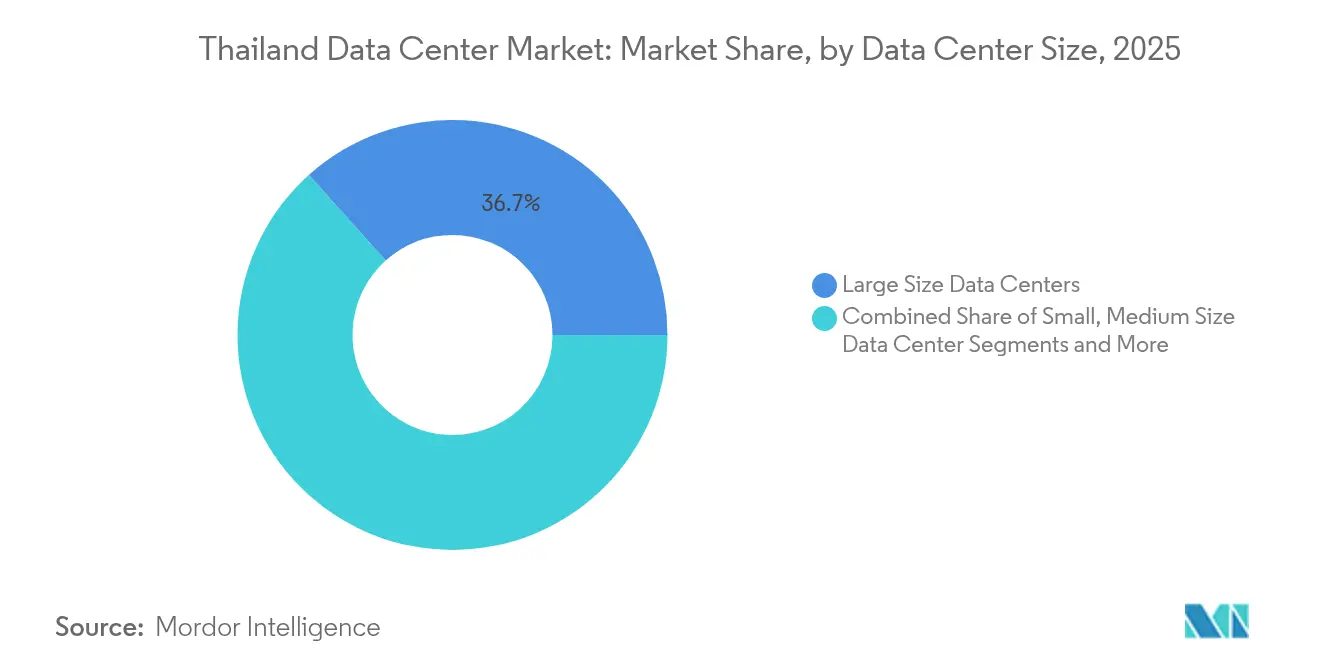

- By data-center size, Large-size facilities accounted for 36.65% of the Thailand data center power market size in 2025, while Mega-size sites are growing at a 10.63% CAGR on the back of AI-centered demand.

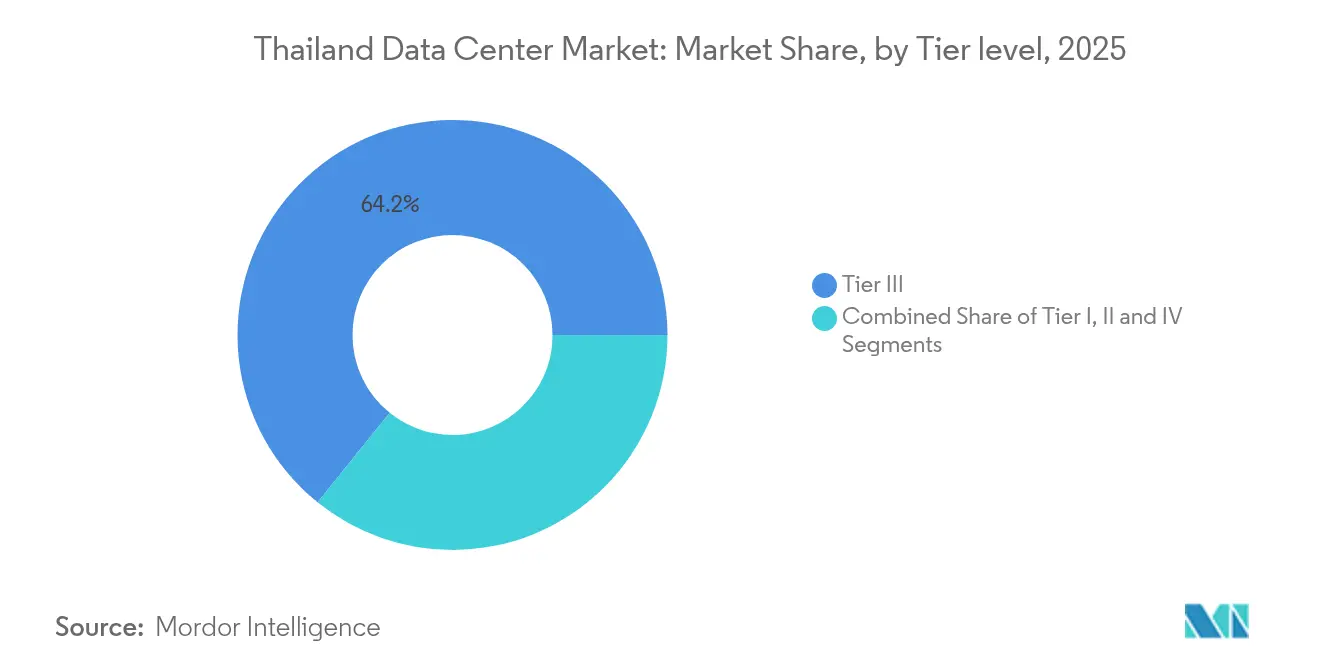

- By tier level, Tier III remained dominant with a 64.20% share in 2025, but Tier IV is the fastest mover at a 12.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust hyperscale and cloud build-outs | +2.8% | National, concentrated in Eastern Economic Corridor | Medium term (2-4 years) |

| Government incentives for "Thailand 4.0" digital economy | +1.9% | National, with early gains in Bangkok, Chonburi, Rayong | Long term (≥ 4 years) |

| Telecom shift to AI-factory data centers | +2.1% | National, spill-over to regional connectivity hubs | Medium term (2-4 years) |

| Grid-connected solar + BESS micro-grids inside campuses | +1.4% | National, enhanced adoption in high-solar regions | Long term (≥ 4 years) |

| Aggressive PUE targets by foreign colocation JVs | +1.2% | National, concentrated in major metropolitan areas | Short term (≤ 2 years) |

| AI/ML Workloads Driving High-Density Power | +2.6% | National, concentrated in hyperscale facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust hyperscale and cloud build-outs

Capital commitments from Amazon Web Services, Microsoft, and other multinationals are redefining power-system design parameters in the Thailand data center power market.[1]Amazon Web Services, “AWS expands Asia Pacific (Thailand) Region,” aws.amazon.com AWS launched a USD 5 billion Thailand region in January 2025, opening three Availability Zones that employ geographically separated electrical redundancy. Each zone requires autonomous UPS strings, 2N generator farms, and advanced switchgear, raising demand for high-reliability power equipment across Thailand. Microsoft’s entry through the “Ignite Thailand” vision intensifies the arms race for fault-tolerant, AI-ready power capacity, because its first domestic campus is expected to span tens of megawatts. Hyperscale clustering in the Eastern Economic Corridor means grid-balancing schemes must handle step-changes when multiple megawatt-scale feeders trip simultaneously. Component suppliers with strong after-sales support gain an advantage because hyperscalers insist on rapid turnaround for any field-replaceable power modules

Telecom shift to AI-factory data centers

Domestic telecom groups, led by Gulf Development and Singtel’s ADVANC JV, are transforming legacy campuses into AI-factories that start at 25 MW and scale to 50 MW.[2]Legrand, “2025 investor presentation,” legrandgroup.com AI inference and training operations require rack densities above 40 kW, pushing UPS selection toward lithium-ion architectures and forcing chilled-water loop redesigns. Utilities such as B.Grimm Power respond with tailored power-purchase agreements that blend solar, biogas, and gas-engine peakers for peaking shaving. This telecom-driven pivot strengthens the Thailand data center power market because it creates demand profiles distinct from classic enterprise colocation. Vendors able to package high-density busways, dynamic bus optimization, and quick-start generators capture share as AI workloads permeate verticals beyond telecom.

Grid-connected solar + BESS micro-grids inside campuses

A 136 MWh PV-biogas-battery testbed achieved 90.8% round-trip efficiency under tropical conditions, proving that large-scale renewables can reliably serve data centers in Thailand’s climate.[3]Gulf Energy Development, “Gulf and Singtel sign 25 MW data center JV,” gulf.co.thABB’s modular micro-grid platform lets operators island from the utility grid during disturbances while selling frequency-regulation services through spare battery capacity. The Provincial Electricity Authority has signed memoranda of understanding to pilot similar behind-the-meter systems at multiple campuses. As a result, the Thailand data center power market moves away from diesel-only standby models toward hybrid configurations that integrate solar canopies, lithium-iron-phosphate batteries, and smart inverters. Component vendors capable of integrating energy-storage management software with conventional power-distribution units occupy a strategic niche.

Aggressive PUE targets by foreign colocation JVs

NTT Global Data Centers plans to run Thai facilities on 100% renewable energy by 2030 and has pledged JPY 1.5 trillion (USD 12 billion) for regional expansion. Its design toolkit targets PUE below 1.2 through direct-to-chip cooling, phase-change materials, and short-network AC busways. AWS benchmarks claim 4.1 times higher energy efficiency than traditional on-premises infrastructure, creating competitive pressure for local entrants to match frontier metrics. Legrand’s growing portfolio of high-efficiency busway systems, which now contribute 20% of group revenue, underscores supplier opportunities.[4]Department of Alternative Energy Development and Efficiency, “Solar PV roadmap,” energy.go.th Because Thailand’s tropical humidity challenges evaporative cooling, operators deploy closed-loop water-side economizers and advanced condensing-boiler controls to maintain low PUE targets year-round, strengthening demand for intelligent power-monitoring solutions in the Thailand data center power market

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex for 2N/2N+1 redundancy | -1.8% | National, acute in Tier IV implementations | Short term (≤ 2 years) |

| Lengthy EIA approval and land-use permitting | -1.2% | National, concentrated in environmentally sensitive areas | Medium term (2-4 years) |

| Looming shortage of LV/MV switchgear and skilled technicians | -2.1% | National, acute in Eastern Economic Corridor | Short term (≤ 2 years) |

| Grid frequency jitter from clustered data center trips | -0.9% | Regional, concentrated around major data center clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront capex for 2N/2N+1 redundancy

Tier IV facilities require fully duplicated power and cooling paths, effectively doubling capital outlay relative to Tier III. Developers incur added carrying costs when long-lead items such as 500 kVA transformers arrive late because of global shortages, though Hitachi Energy’s extra USD 250 million transformer investment aims to ease constraints by 2027. NV5 Global’s USD 6 million commissioning contract for a Thai hyperscale campus highlights the specialized engineering needed to integrate redundant switchgear, static bypass modules, and automatic transfer schemes. Financing is further strained by higher interest rates and extended development cycles, so smaller entrants may delay projects, tempering near-term growth in the Thailand data center power market.

Lengthy EIA approval and land-use permitting

While the Eastern Economic Corridor offers streamlined approvals, sites near environmentally sensitive zones still face multi-month reviews. Developers must conduct soil-stability tests to prove that high-density equipment loads will not disrupt groundwater profiles, complicating land selection. In metropolitan Bangkok, land-use re-zoning extends timelines, pushing up holding costs on already expensive parcels. This bottleneck risks misalignment between power-component lead times and physical-site readiness, creating schedule uncertainty that weighs on investor confidence in the Thailand data center power market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: UPS Systems Lead Infrastructure Investments

Uninterruptible power supply systems held 32.10% of the Thailand data center power market in 2025, reflecting their foundational role in safeguarding against grid anomalies. Lithium-ion-based UPS adoption is rising because the chemistry supports higher temperature tolerance, reduces footprint, and eases maintenance compared with valve-regulated lead acid. Parallel architectures with distributed bypass modules dominate Tier IV builds, while monolithic units remain popular in Tier III. Generators retain critical importance, yet fuel-cell pilots by Bloom Energy show promise for zero-emission backup in hyperscale campuses. PDUs log the fastest 10.92% CAGR since AI rack densities require branch-level metering and adaptive load balancing. Energy-storage systems gain traction after research proved 90.8% round-trip efficiency, giving operators confidence to shift from diesel-heavy to hybrid designs. Service categories installation, commissioning, and remote diagnostics expand because technician shortages force operators to outsource more life-cycle tasks.

The Thailand data center power market size for energy-storage components is projected to grow at double-digit rates as green-power mandates align with battery price declines. Vendors of switchgear and transfer switches wrestle with long lead times, even though demand is robust. Hitachi Energy’s transformer expansion and ABB’s micro-grid platform help remedy bottlenecks by localizing manufacturing and shortening freight routes. Training services also register elevated demand because operational teams must manage advanced energy-management systems that blend grid, solar, and battery sources. Overall, the component landscape illustrates Thailand’s push toward resilient, sustainable, and AI-ready power architectures, solidifying the Thailand data center power market as a lucrative target for diversified electrical-equipment suppliers.

By Data Center Type: Hyperscalers Drive Market Transformation

Colocation providers maintained a 42.35% share of the Thailand data center power market in 2025 due to relaxed foreign-ownership rules and reliable enterprise demand. Nevertheless, hyperscale/cloud service providers are expanding at a 12.05% CAGR as global cloud majors deploy regional infrastructure to serve AI workloads that demand continuous high-density power availability. AWS’s three-zone blueprint sets a performance benchmark others must match, cascading to power-distribution architectures that support rapid fail-over. Enterprise data centers still contribute steady, albeit modest, demand for 2N topologies when firms retain sensitive workloads on private clouds. Edge sites near population centers provide latency benefits for content streaming and smart-city services, stimulating moderate investment in compact UPS units and modular switchgear.

By Data Center Size: Mega Facilities Reshape Infrastructure Requirements

Large-sized facilities captured 36.65% of Thailand's data center power market share in 2025, mirroring the stage where most campuses host mixed enterprise and cloud loads. Mega-size sites outpace others with a 10.63% CAGR through 2031 because AI workloads drive consolidation into 200 MW zones that enable cooling economies and streamlined security. The jump from 50 MW to 100 MW blocks triggers new engineering decisions: ring-bus tie-ins replace radial feeders, and embedded battery farms become cost-effective for peak shaving. Small and medium facilities retain relevance for disaster-recovery colocation, yet many operators refurbish them as edge nodes feeding content to last-mile fiber networks.

By Tier Level: Tier IV Configurations Accelerate for AI Workloads

Tier III facilities held 64.20% of the Thailand data center power market in 2025 because they balance capital intensity with acceptable uptime for enterprise workloads. AI’s ascendancy pushes hyperscalers toward Tier IV layouts that provide concurrent maintainability and withstand multiple fault events. Tier IV’s 12.45% CAGR is fueled by workloads such as generative AI training, where unplanned outages can waste millions in compute cycles. Operators integrate double-ended substations, dual feed paths, and continuous thermal monitoring to satisfy zero-downtime service-level agreements. Tier I and II venues remain only in remote regions or cost-sensitive industry niches, but continue to decline in share each year.

Geography Analysis

Thailand’s regulatory clarity and geopolitical neutrality underpin steady inflows of hyperscale capital, keeping the Thailand data center power market on a faster trajectory than regional peers. Bangkok’s metro ring attracts the first wave of builds because fiber density and financial-service customers ensure baseline demand. Chonburi and Rayong, two nodes of the Eastern Economic Corridor, host the majority of greenfield campuses because provincial authorities provide accelerated building permits and land with existing high-voltage interconnections. Electricity tariffs between USD 0.02 and USD 0.06 per kWh cement Thailand’s competitiveness against Singapore and Jakarta, whose rates typically sit higher.

Northern provinces step into secondary-site roles as demand for disaster-recovery zones grows. Operators there benefit from cooler average temperatures, cutting cooling energy use by several percentage points. However, grid connection can be slower because long-distance transmission requires new rights of way. Southern Thailand eyes edge-node deployments tied to submarine-cable landing stations, appealing to content providers serving cross-border traffic. The Thailand data center power market thereby segments geographically along the axes of latency requirements, grid availability, and renewable-energy potential.

Competitive Landscape

The Thailand data center power market features a moderate concentration, with top multinationals and domestic utilities jointly shaping supply. Integrated players that offer land acquisition, grid interconnect, and long-term renewable-energy contracts, such as Gulf-Singtel’s JV, hold favorable negotiating positions with hyperscalers seeking turnkey solutions. Hitachi Energy’s transformer investment and ABB’s micro-grid portfolio broaden the hardware footprint, while local EPC companies maintain competitive leverage by bundling construction and commissioning.

Technology differentiation now centers on energy efficiency and grid service capabilities. Legrand’s busway products, Bloom Energy’s fuel-cell backup modules, and NTT’s cooling innovations raise the performance bar for PUE and carbon metrics. Utilities like B.Grimm Power diversify into behind-the-meter solar and battery packages tailored for data centers, blurring traditional lines between generation and equipment supply. Skilled-technician shortages create opportunities for specialized service providers that combine remote diagnostics, augmented-reality maintenance, and lifetime asset-management contracts.

Thailand Data Center Power Industry Leaders

ABB Ltd.

Schneider Electric SE

Vertiv Group Corp.

Eaton Corporation plc

Cummins Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hitachi Energy committed an extra USD 250 million to expand global transformer manufacturing capacity by 2027, easing supply shortages for power-intensive projects.

- February 2024: NV5 Global secured over 250 MW worth of Thai data-center projects, including a USD 6 million commissioning mandate for a hyperscale campus

- January 2025: AWS launched the Asia Pacific (Thailand) Region after a USD 5 billion investment, adding three Availability Zones and targeting net-zero carbon by 2040.

- January 2025: The Thai Energy Regulatory Commission began the nation’s first green-electricity sales program by partnering with three utilities, allowing data-center operators direct renewable-power purchases.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Thailand's data center power market as the value generated from electrical infrastructure, uninterruptible power supplies, generators, transfer switches, switchgear, power distribution units, remote power panels, and energy storage systems, plus related installation, maintenance, and consulting services deployed in hyperscale, colocation, enterprise, and edge facilities.

Scope Exclusion: Cooling equipment, server hardware, and fiber or switching gear are purposefully left out to keep the focus on power infrastructure alone.

Segmentation Overview

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with facility design engineers in Bangkok, power component OEM sales managers covering the Eastern Economic Corridor, and procurement heads at cloud service providers. These calls clarified redundancy schemes, average selling prices, and construction lead times, letting us close data gaps and stress test every secondary datapoint.

Desk Research

We gathered baseline inputs from respected public domains such as the Energy Regulatory Commission, Board of Investment filings, National Broadcasting and Telecommunications Commission traffic statistics, Customs import codes for switchgear and UPS, and technical papers hosted on IEEE Xplore that document PUE shifts in tropical data centers. Our team also scanned annual reports and investor decks of leading colocators, trade association briefs from the Thailand Data Center Council, and major press coverage logged on Dow Jones Factiva, which rounded out recent capacity announcements. Supplementary insights flowed from paid data sets, D&B Hoovers for operator financials and Volza shipment records that quantify inbound MW of diesel gensets, to cross check public figures and identify volume spikes. The list above is illustrative; many other secondary materials were interrogated to validate and refine the evidence base.

Market-Sizing & Forecasting

A top down reconstruction built around national grid demand, new site announcements, and MW per rack density trends created the initial 2024-25 demand pool, which is then sanity checked through selective bottom up roll ups of supplier shipments and sampled ASP × volume math. Key model drivers include UPS unit shipments, average PUE improvement trajectory, megawatt utilization curves, renewable penetration targets, grid connection timelines, and enterprise cloud migration rates. Multivariate regression links these variables to historical spend, while scenario analysis adjusts for policy or supply chain shocks. Gaps arising from sparse bottom up inputs are bridged using regional benchmarks before final reconciliation.

Data Validation & Update Cycle

Outputs undergo variance checks against operator disclosures and quarterly import data, followed by peer review and senior analyst sign off. Models refresh annually, and interim updates are triggered when cumulative announced capacity moves the baseline by over five percent. A last minute pass ensures clients receive the freshest view.

Why Mordor's Thailand Data Center Power Baseline Commands Reliability

Published estimates often differ because firms pick divergent component baskets, price points, and refresh cadences.

Key gap drivers in rival numbers stem from including only hardware sales, omitting service revenue, converting at fixed exchange rates, or projecting capacity without verifying BOI approved project phasing and PUE roadmaps that our model captures.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 456.71 M (2025) | Mordor Intelligence | - |

| USD 456 M (2024) | Regional Consultancy A | excludes installation services and applies constant 2023 FX |

| USD 413.20 M (2025) | Global Consultancy B | narrower component list, does not factor Tier IV premium or EEC grid upgrades |

These contrasts show that Mordor Intelligence delivers a balanced, transparent baseline grounded in verifiable variables and a clearly repeatable process, giving decision makers numbers they can trust.

Key Questions Answered in the Report

How large is the Thailand data center power market in 2026?

The Thailand data center power market size reached USD 502.93 million in 2026 and is on track to grow to USD 814.35 million by 2031.

Which component generates the most revenue

UPS Systems lead, accounting for 32.10% of Thailand data center power market share in 2025 due to hyperscale demand for high-reliability backup

Why are hyperscalers investing aggressively in Thailand?

Eight-year tax holidays, lower green-electricity tariffs, and geopolitical neutrality create favorable conditions, while AI workloads require the large-scale, redundant power capacity hyperscalers can build.

What renewable-energy options exist for data-center operators?

Operators can access grid-connected solar contracts, on-site PV arrays, and battery energy storage systems after the 2025 green-power program launch

What is driving the shift toward Tier IV facilities?

AI and machine-learning workloads need continuous uptime; this forces operators to adopt 2N/2N+1 redundancy, propelling Tier IV capacity at a 12.45% CAGR.

Page last updated on: