Vietnam Data Center Power Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

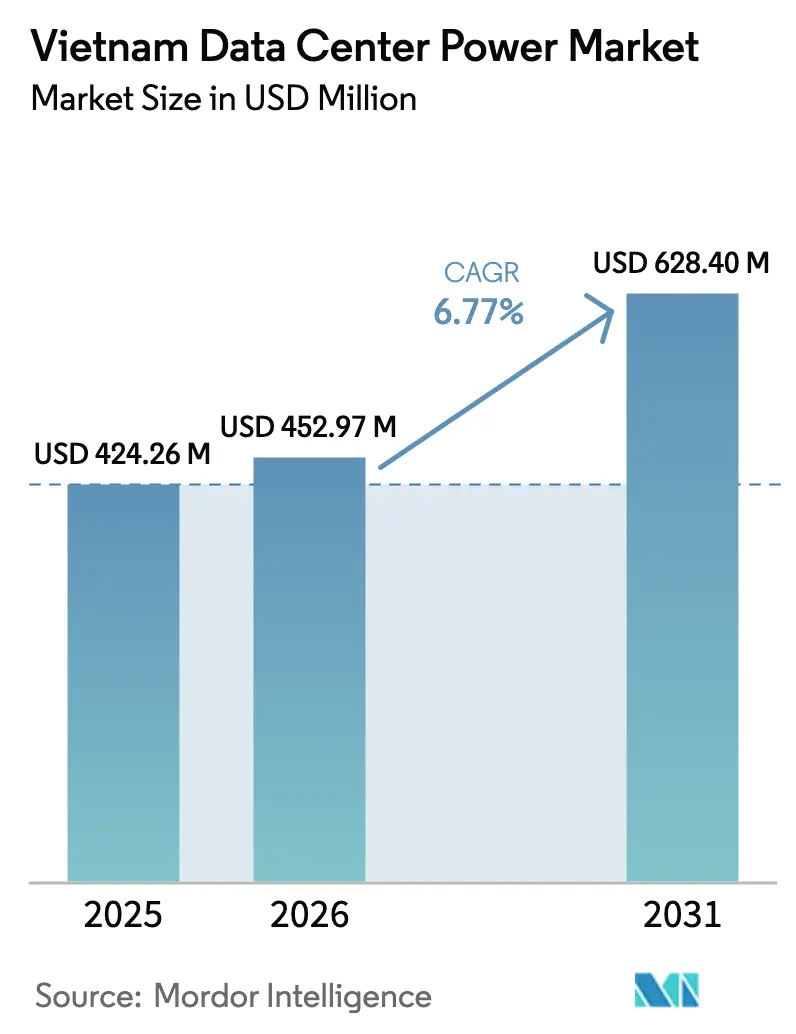

| Base Year Market Size (2025) | USD 424.26 Million |

| Market Size (2026) | USD 452.97 Million |

| Market Size (2031) | USD 628.4 Million |

| Growth Rate (2026 - 2031) | 6.77% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vietnam Data Center Power Market Analysis by Mordor Intelligence

The Vietnam data center power market size was valued at USD 424.26 million in 2025 and estimated to grow from USD 452.97 million in 2026 to reach USD 628.4 million by 2031, at a CAGR of 6.77% during the forecast period (2026-2031). This pace underscores Vietnam’s evolution into a preferred digital hub within Southeast Asia as operators pivot away from higher-cost regional locations. Foreign-ownership liberalization, expanding cloud and AI workloads, and national energy plans that double generation capacity to 155 GW by 2030 are converging to lift demand for resilient and efficient power infrastructure. Accelerated rack densities that now reach 40 kW and above per cabinet are reshaping power distribution architectures, while utility price reforms encourage upgrades to high-efficiency UPS and intelligent PDUs. Strategic partnerships between global power-equipment leaders and domestic telecom operators are also catalyzing technology transfer and new service models that strengthen competitive positioning in the Vietnam data center power market.

Key Report Takeaways

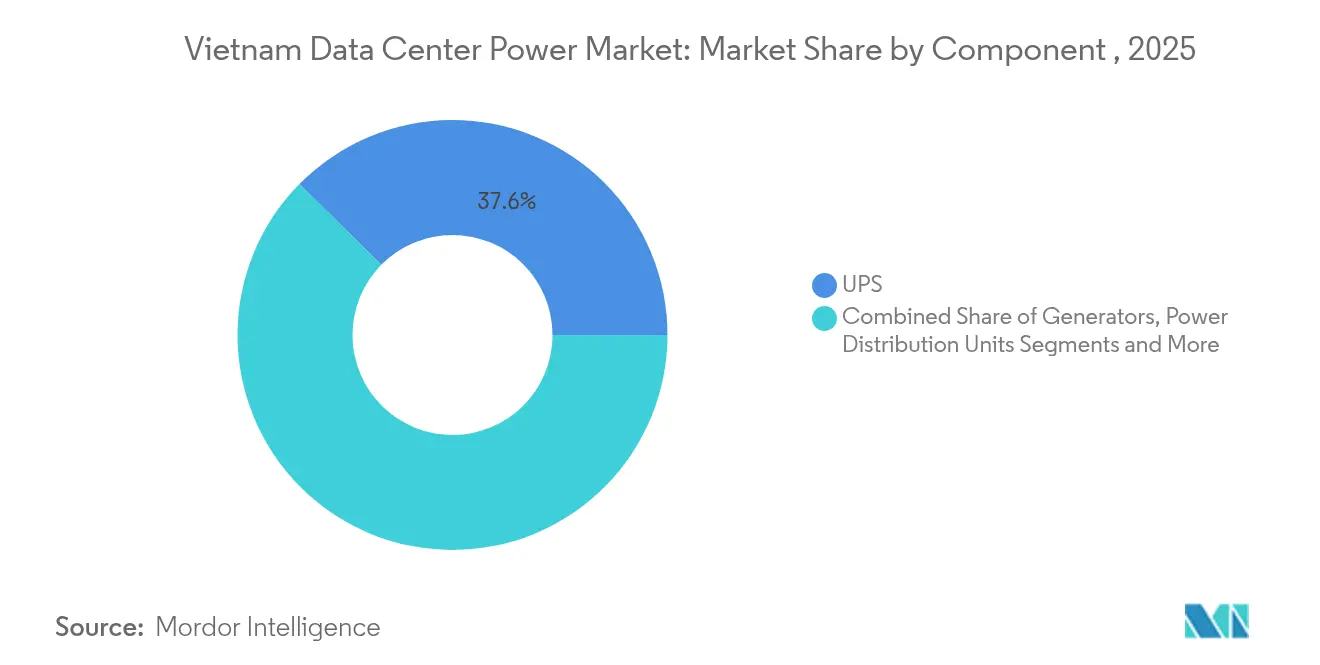

- By component, UPS Systems dominated with 37.62% revenue share in 2025; Power Distribution Units are on track to grow at an 8.38% CAGR to 2031.

- By data center type, the colocation segment held 36.18% of the Vietnam data center power market size in 2025, whereas hyperscale/cloud facilities recorded the fastest 7.78% CAGR for 2026-2031.

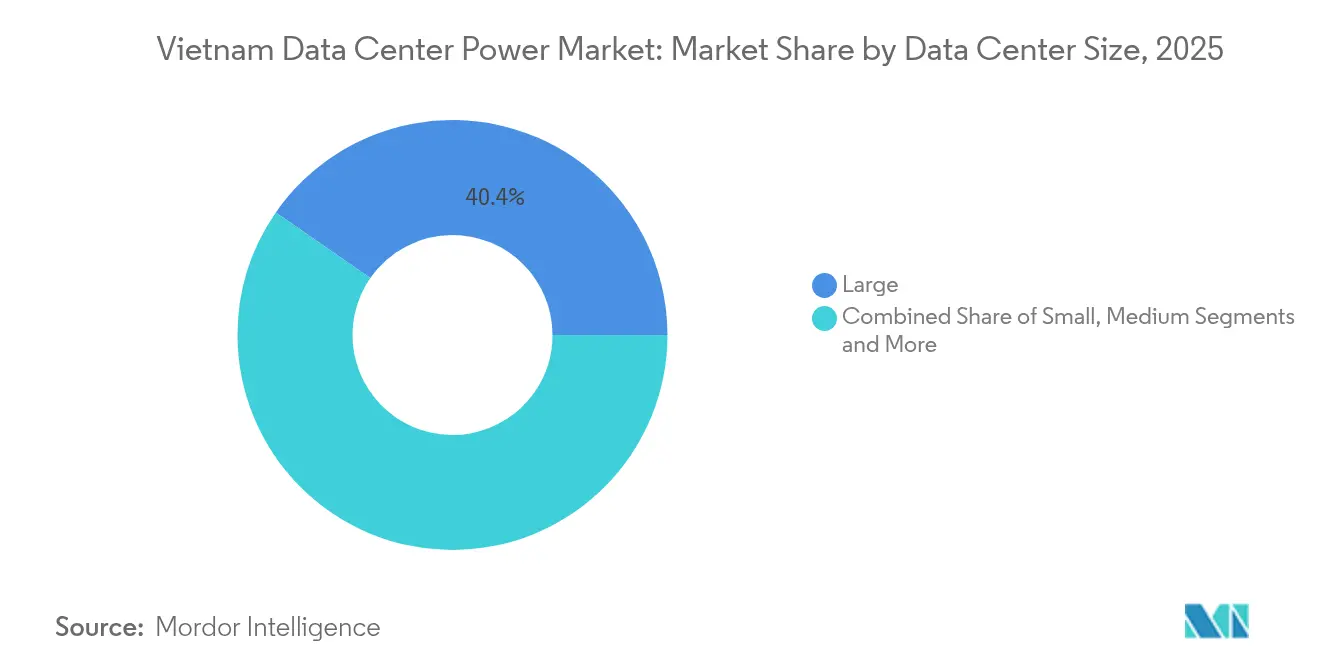

- By facility size, large data centers accounted for 40.35% of revenue in 2025; massive facilities are forecast to expand at 8.57% CAGR during 2026-2031.

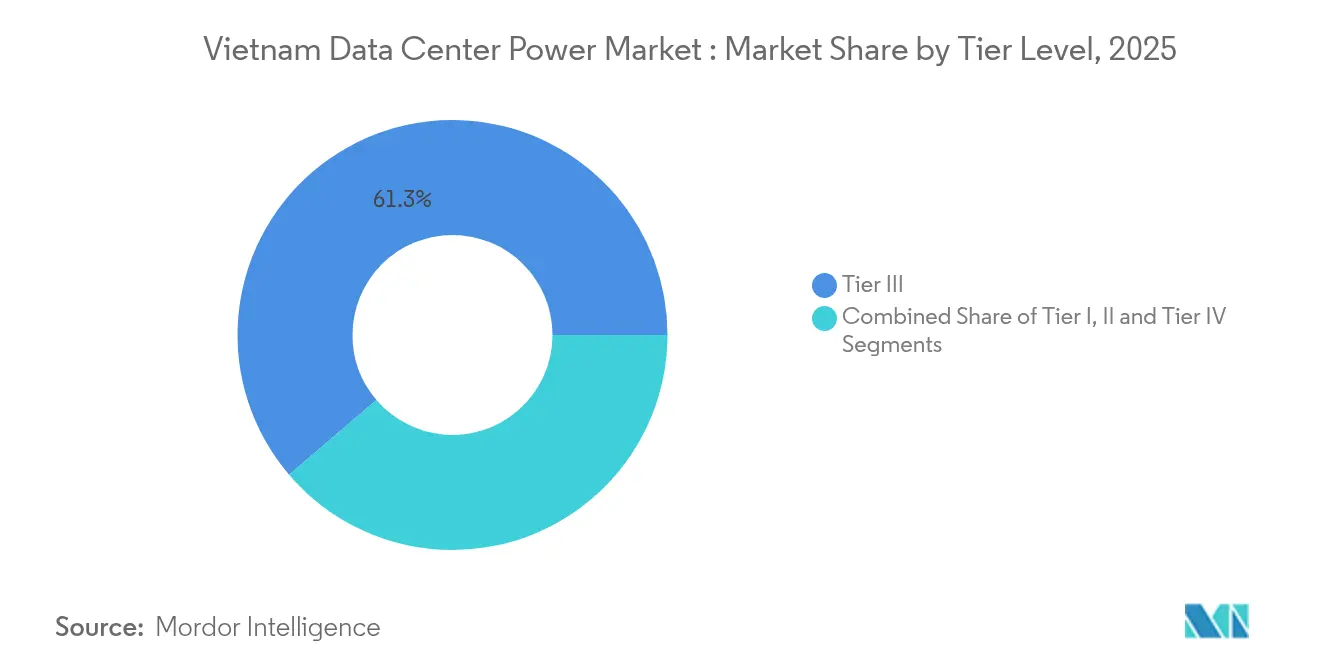

- By tier, Tier III facilities captured 61.25% of the total 2025 revenue, while Tier IV venues advanced at a 8.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Data Center Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | Driver |

|---|---|---|---|---|

| Expansion of hyperscale and cloud–led mega facilities | +2.1% | Southern Vietnam (HCMC), with emerging presence in Northern Vietnam (Hanoi) | Medium term (2-4 years) | Expansion of hyperscale and cloud–led mega facilities |

| Government-backed National Digital Transformation Program and new Data-Localization Law compel enterprises to host workloads domestically | +1.8% | National, with concentration in major urban centers | Short term (≤ 2 years) | Government-backed National Digital Transformation Program and new Data-Localization Law compel enterprises to host workloads domestically |

| Accelerated 5G rollout and IoT proliferation are pushing both edge and core data-center capacity | +1.2% | National, with initial concentration in urban centers | Medium term (2-4 years) | Accelerated 5G rollout and IoT proliferation are pushing both edge and core data-center capacity |

| PUE targets (≤1.4) and rising EVN electricity tariffs trigger retrofit cycles toward high-efficiency UPS, bus-duct and intelligent PDUs | +0.9% | National, with higher impact in Southern Vietnam | Short term (≤ 2 years) | PUE targets (≤1.4) and rising EVN electricity tariffs trigger retrofit cycles toward high-efficiency UPS, bus-duct and intelligent PDUs |

| Surge in AI/ML power-dense racks (≥40 kW) | +1.7% | Southern Vietnam (HCMC), with growing impact in Northern Vietnam | Medium term (2-4 years) | Surge in AI/ML power-dense racks (≥40 kW) |

| Shift to Hydrotreated Vegetable Oil (HVO)-ready generators for Green Power Purchase Agreements | +0.6% | National, with early adoption in foreign-owned facilities | Long term (≥ 4 years) | Shift to Hydrotreated Vegetable Oil (HVO)-ready generators for Green Power Purchase Agreements |

| Source: Mordor Intelligence | ||||

Expansion of hyperscale and cloud-led mega facilities

Capacity is projected to climb from 80 MW to more than 200 MW as flagship projects such as the USD 1.5 billion SAM DigitalHub campus in Binh Duong add 150 MW of supply.[1]Lien Thuong & Hai Yen, “SAM to develop USD 1.5 billion data center in southern Vietnam,” The Investor, theinvestor.vn Hyperscale sites require denser power feeds, typically 10-30 kW per rack, with AI zones peaking at 60 kW. Operators therefore deploy bus-duct systems and high-efficiency UPS that sustain target PUE figures below 1.4 even at elevated thermal loads, exemplified by Viettel’s 140 MW facility in Ho Chi Minh City

Government-backed National Digital Transformation Program drives domestic hosting

Mandatory domestic storage of critical data, combined with the goal of three national-level data centers by 2025, is accelerating new builds that meet Uptime Tier III standards with PUE of 1.4 . CMC Telecom’s Tan Thuan site has already met Level 4 Information Security criteria, positioning domestic providers to support regulated workloads

5G rollout accelerates edge and core data center capacity

Nationwide 5G coverage unlocks latency-sensitive applications and fuels parallel growth of edge cabinets and core halls. FPT Telecom’s urban micro data centers illustrate the need for compact, resilient power topologies that can operate in constrained footprints while still reaching 97% UPS efficiency.[2]FPT Telecom, “FPT leverages innovative technologies to advance Data Center Development in Vietnam,”fpt.vn

PUE targets and rising electricity tariffs drive efficiency upgrades

EVN’s tariff adjustments, coupled with corporate net-zero pledges, are prompting widespread retrofits. Viettel’s Hoa Lac green data center saved 3 million kWh in 2024 through high-efficiency UPS and optimized airflow, cutting CO₂ by about 2,100 tons.[3]Trần Bình. "Viettel khai trương trung tâm dữ liệu lớn nhất Việt Nam." Sài Gòn Giải Phóng, sggp.org

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | Restraint |

|---|---|---|---|---|

| High capex for Tier III/IV electrical redundancy | -1.2% | National, with higher impact in emerging data center locations | Medium term (2-4 years) | High capex for Tier III/IV electrical redundancy |

| Skilled-labour shortage in critical-power O&M | -0.8% | National, with acute impact in rapidly growing regions | Short term (≤ 2 years) | Skilled-labour shortage in critical-power O&M |

| Grid frequency jitter from clustered Data Center trips | -0.6% | Concentrated in high-density data center clusters in HCMC and Hanoi | Medium term (2-4 years) | Grid frequency jitter from clustered Data Center trips |

| Grid-frequency jitter from simultaneous data-center disconnection/re-sync events forces Easy Virtual Network to impose curtailment protocols | -0.4% | Concentrated in high-density data center clusters in HCMC and Hanoi | Medium term (2-4 years) | Grid-frequency jitter from simultaneous data-center disconnection/re-sync events forces Easy Virtual Network to impose curtailment protocols |

| Source: Mordor Intelligence | ||||

High capex for Tier III/IV electrical redundancy

Average build costs reached USD 6.94 million per MW in 2025, 3.5% higher than 2024, adding pressure to balance reliability against economics. Smaller domestic firms often adopt modified Tier III+ designs to avoid the 30-40% premium associated with fully redundant Tier IV pathways.

Skilled-labour shortage in critical-power O&M

Rapid market growth has outpaced talent supply. Leading operators now run in-house academies to develop local expertise in UPS tuning, power-quality analytics, and lithium-ion battery management. These programs increase costs yet are vital for sustainable expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: UPS Systems Lead While PDUs Surge

UPS Systems controlled 37.62% of the Vietnam data center power market in 2025. Adoption of modular, lithium-ion UPS enables incremental scaling that aligns with unpredictable AI cloud loads while maintaining 97% energy efficiency. Vertiv’s Liebert EXL S1 deployments in new Tier III plants illustrate the transition toward space-saving, high-efficiency topologies. At the same time, intelligent PDUs are on an 8.38% CAGR trajectory through 2031, reflecting a sharper focus on rack-level telemetry and remote energy governance. The generator subsegment is shifting as HVO-ready sets replace conventional diesel, and Cummins’ Centum series now ships with Data Center Continuous ratings that support unlimited runtime.

Power Distribution Units attract heightened interest because AI racks exceeding 40 kW require granular load balancing and thermal mapping. Operators in the Vietnam data center power market deploy metered PDUs with circuit-breaker trip alarms to improve uptime and enable dynamic capacity planning. Switchgear and transfer switches capture additional spend as enterprises adopt N+1 redundancy, while battery energy-storage systems play a complementary role in smoothing grid volatility. Together, these trends signal an ecosystem that prizes agility, efficiency, and digitized power monitoring.

By Data Center Type: Colocation Dominance Challenged by Hyperscale Growth

Colocation operators held 36.18% of the Vietnam data center power market size in 2025. CMC Telecom commands about 40% of banking workloads and supports more than 60% of OTT players with 3,000 racks across three venues, demonstrating the attraction of pay-as-you-grow models for enterprise clients. However, hyperscale facilities register the fastest 7.78% CAGR through 2031 as global cloud majors evaluate campuses near Ho Chi Minh City that could draw power comparable to a small municipality.

Edge and enterprise data centers continue to serve regulated verticals that require physical segregation and low latency. A large Vietnamese bank recently migrated to a split estate, housing core systems in a Tier III colocation hall while deploying edge nodes for customer-facing apps. This hybrid adoption pattern broadens the addressable base for advanced power gear and reinforces demand for modular UPS blocks tailored to partial loads.

By Data Center Size: Large Centers Dominate While Massive Facilities Accelerate

Large-sized data center facilities account for 40.35% of 2025 revenue, reflecting the historic focus on domestic enterprise demand. Nonetheless, massive builds surpassing 20 MW will grow 8.57% annually to 2031, fueled by Viettel’s 140 MW design that features 10,000 racks and up to 60 kW per cabinet. Small sites continue to meet specific edge cases, while medium halls cater to regional SaaS providers needing moderate capacity with localized service. Mega-scale campuses, still nascent, are poised to emerge as foreign investors gain full ownership rights under the amended Telecommunications Law.

The Vietnam data center power market benefits as large operators consolidate multiple small rooms into single sites, reducing overhead and elevating UPS utilization. One e-commerce leader achieved 15% energy savings and cut management headcount by transitioning from eight micro rooms to a single 12 MW facility equipped with bus-duct power rails and hot-aisle containment.

By Tier Level: Tier III Standardization with Tier IV Growth

Tier III facilities accounted for 61.25% of 2025 revenue and remain the default specification because they deliver 99.982% uptime at competitive cost. QTSC’s dual certification for design and construction highlights industry maturity. Government policy further incentivizes Tier III builds for national data centers to align resilience with fiscal discipline.

Tier IV venues rise 8.96% per year as financial institutions, hyperscale cloud providers, and AI research labs demand fault-tolerant design. CMC Telecom’s Tan Thuan facility set a precedent by meeting Level 4 Information Security and deploying dual active power paths that eliminate single points of failure. The Vietnam data center power industry now sees premium buyers willing to pay extra for zero-downtime contracts and strict compliance profiles.

Geography Analysis

A legacy of telecom infrastructure, diverse enterprise tenants, and strong subsea connectivity continues to attract build-to-suit and colocation projects. Viettel is constructing a 140 MW hyperscale plant that targets PUE below 1.4 and hosts AI racks up to 60 kW. Municipal authorities budgeted VND 4.4 trillion (USD 173 million) for digital infrastructure in the 2021-2030 master plan, signalling policy support for further clusters

Foreign direct investment reached USD 24.8 billion during the first nine months of 2024, 63% flowing into manufacturing and processing that require robust digital infrastructure. Viettel’s 30 MW Hoa Lac green data center demonstrates the region’s commitment to renewable sourcing and high-density compute.

Central Vietnam remains early-stage yet presents future upside for edge deployments that improve content delivery to coastal cities. Limited international bandwidth and grid constraints temper short-term growth, but national roadmaps include sub-transmission upgrades and new cable landings. Local carriers are piloting standard power modules that can be trucked to regional exchanges, shortening deployment cycles and ensuring uniform maintenance procedures.

Competitive Landscape

Domestic telecom operators dominate ownership, with Viettel, VNPT, FPT Telecom, CMC Telecom, and VNG. These firms leverage national fiber backbones, tower real estate, and long-standing regulatory relationships to secure prime land and quick approvals. International power-equipment specialists such as ABB, Schneider Electric, Vertiv, and Eaton compete for UPS, bus-duct, and generator contracts, usually by aligning with local operators on joint bids. Schneider Electric’s 2025 partnership with NVIDIA to design AI-ready facilities shows the strategic use of co-innovation to gain share

Product differentiation now centers on supporting AI workloads that triple rack densities relative to legacy rooms. Emerging suppliers offer lithium-ion battery cabinets, dynamic busways, and solid-state transfer switches that reduce failover time. Hydrogen fuel cells, exemplified by Hitachi Energy’s HyFlex prototype, gain mindshare as operators explore diesel alternatives that meet net-zero goals

Vietnam Data Center Power Industry Leaders

-

ABB Ltd

-

Schneider Electric SE

-

Eaton Corporation plc

-

Caterpillar Inc.

-

Vertiv Group Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Viettel broke ground on a 140 MW hyperscale data center in Ho Chi Minh City targeting PUE < 1.4

- March 2025: Saigon Asset Management unveiled a USD 1.5 billion, 150 MW campus in Binh Duong Province.

- January 2025: Schneider Electric and NVIDIA agreed to co-develop AI-ready, sustainable data centers in Vietnam.

- November 2024: QTSC Data Center secured Uptime Tier III Certification

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Vietnam data center power market as annual spending on electrical gear (UPS systems, generator sets, diesel, gas, fuel-cell, switchgear, transfer switches, power distribution units, remote power panels, and battery storage) installed inside hyperscale, colocation, and enterprise facilities to keep servers running without interruption.

Scope exclusions: We exclude cooling systems and on-site renewables from scope.

Segmentation Overview

-

By Component

-

Electrical Solutions

- UPS Systems

-

Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

-

Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

-

Electrical Solutions

-

By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

-

By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

-

By Tier Level

- Tier I and II

- Tier III

- Tier IV

Detailed Research Methodology and Data Validation

Primary Research

We spoke with facility engineers at colocation operators, design consultants, UPS channel partners, and procurement heads in Ho Chi Minh City, Hanoi, and rising secondary cities. Their insights confirmed installed density, redundancy choices, and price moves, filling gaps documents alone could not.

Desk Research

Mordor analysts began with open data from the General Statistics Office, Ministry of Industry & Trade, World Bank, and IEA to frame macro load growth. Trade bodies supplied rack-density norms and expansion pipelines. Filings, investor decks, and Dow Jones Factiva clips then helped us clarify vendor shipments, ASP shifts, and upcoming campus capacities. The sources named are illustrative; many additional public and subscription references were consulted.

Market-Sizing & Forecasting

A top-down model starts from operational IT load published by regulators and utilities. We convert that load to required electrical capacity using standard PUE and redundancy factors, then validate totals with a bottom-up roll-up of site counts and blended equipment ASP. Key inputs include rack additions, Tier III-IV share, average UPS kVA per rack, and utility tariff trends. Multivariate regression projects these drivers and expert consensus caps extremes.

Data Validation & Update Cycle

Outputs face variance checks against shipment logs and customs codes before senior sign-off. Models refresh yearly with interim updates after major capacity or tariff moves.

Why Mordor's Vietnam Data Center Power Baseline Stands Firm

Published estimates often diverge because firms adopt different scopes, units, and refresh cadences.

Key gap drivers include whether construction capex or only equipment revenue is counted, if colocation alone or all facility types are covered, and whether redundancy overhead is folded into MW-to-dollar conversions. We see Mordor's disciplined scope, variable selection, and yearly refresh narrowing these gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 424.26 million (2025) | Mordor Intelligence | |

| USD 790 million (2024) | Global Consultancy A | Counts full data-center construction capex, inflating power value |

| USD 148 million (2024) | Industry Association B | Focuses on colocation facilities, excludes enterprise and edge sites |

| USD 25.79 million (2024) | Trade Journal C | Tracks UPS sales only, omitting generators and distribution gear |

Taken together, the comparison shows that, because Mordor ties spend to clear equipment boundaries and triangulates with load factors and shipment checks, our baseline offers a balanced, transparent foundation for decision making.

Key Questions Answered in the Report

What is the current value of the Vietnam data center power market?

The market is valued at USD 452.97 million in 2026 with a forecast to reach USD 628.4 million by 2031.

Why are UPS Systems so important in Vietnamese data centers?

Frequent grid disturbances drive demand for high-efficiency, modular UPS that secure uptime and cut operating costs.

How fast are hyperscale facilities growing in Vietnam?

Capacity is expected to expand from 80 MW in 2025 to more than 200 MW by 2028, translating to an 7.78% CAGR for hyperscale power demand.

What role does the Data-Localization Law play?

The law requires critical data to be stored domestically, prompting enterprises to shift workloads to local facilities and accelerating new builds that meet Tier III standards.

Page last updated on: