Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Thailand Data Center Storage Market Report Segments the Industry Into Storage Technology (Network Attached Storage (NAS), Storage Area Network (SAN) and More), Storage Type (Traditional Storage, and More), Data Center Type (Colocation Facilities and More), Form Factor(Rack-Mounted and More), Interface(sas / SATA, and More)and End User (IT and Telecommunication, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

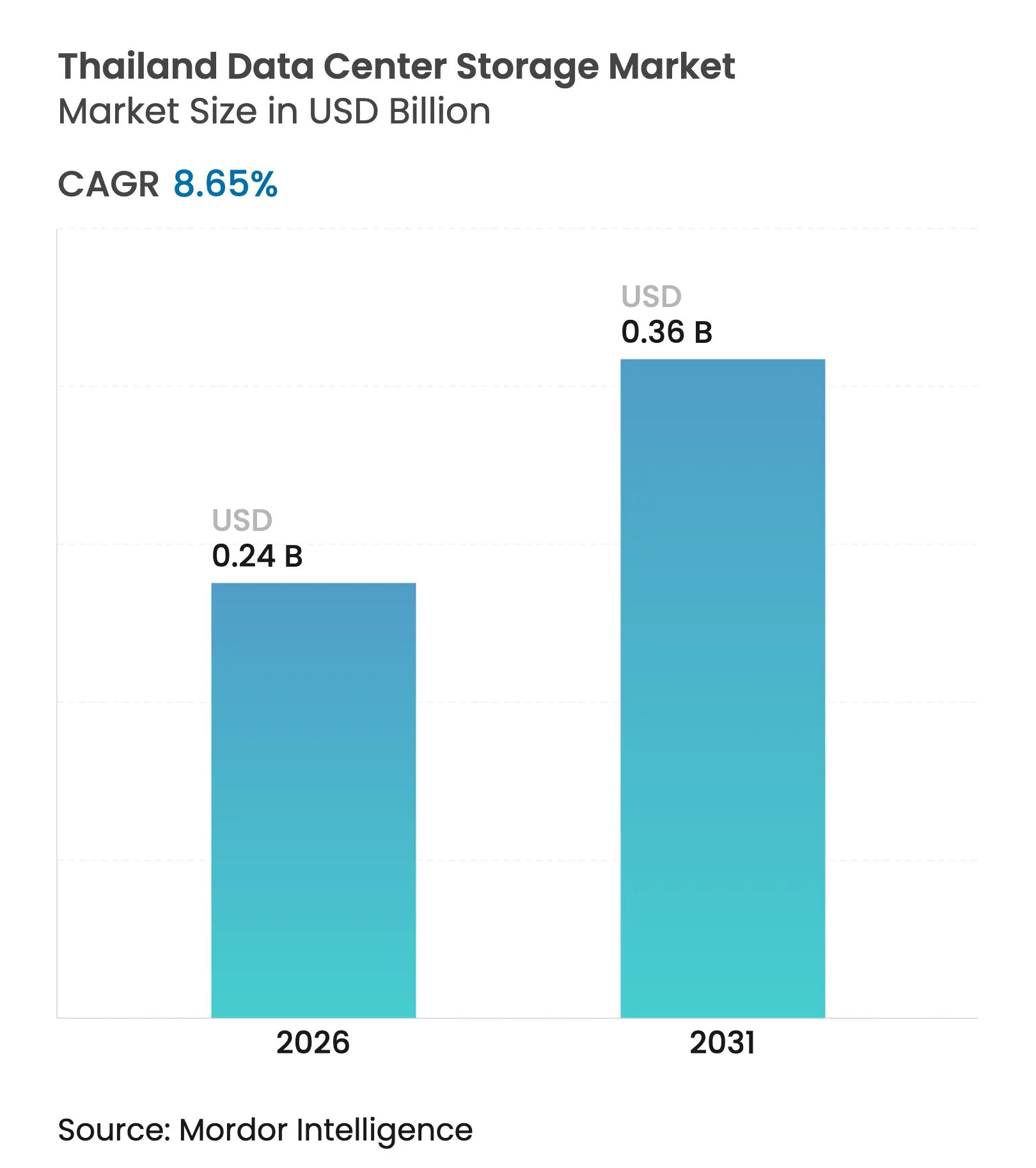

| Market Size (2026) | USD 0.24 Billion |

| Market Size (2031) | USD 0.36 Billion |

| Growth Rate (2026 - 2031) | 8.65 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Thailand data center storage market size is expected to grow from USD 220 million in 2025 to USD 240 million in 2026 and is forecast to reach USD 360 million by 2031 at 8.65% CAGR over 2026-2031. Hyperscale capital expenditure, nationwide 5G deployment, and Board of Investment (BOI) incentives together underpin brisk uptake of high-density flash arrays and scalable object platforms. Google, AWS, and TikTok have each announced multi-billion-dollar builds that reposition the nation from a manufacturing center toward an AI-ready digital hub. Thailand’s strong domestic HDD manufacturing base keeps legacy capacity solutions price-competitive, while falling NAND prices progressively erase the total-cost-of-ownership gap for flash. The Personal Data Protection Act introduces in-country storage mandates that favor both colocation and hyperscale operators. Elevated electricity tariffs and talent scarcity weigh on margins but do not alter the upward trajectory of infrastructure deployments.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Hyperscale and cloud provider capex boom Hyperscale and cloud provider capex boom | +2.8% | National, concentrated in Bangkok, Chonburi, Rayong | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.8% |

Geographic Relevance

:

National, concentrated in Bangkok, Chonburi, Rayong

|

Impact Timeline

:

Medium term (2-4 years)

|

5G rollout and edge nodes intensifying storage

demand 5G rollout and edge nodes intensifying storage

demand | +1.5% | National, with early gains in Bangkok, Pattaya, Chiang Mai | Medium term (2-4 years) | |||

BOI incentives and Thailand 4.0 digital policy BOI incentives and Thailand 4.0 digital policy | +1.2% | National, focused on Eastern Economic Corridor | Long term (≥ 4 years) | |||

AI-centric workloads driving high-density flash

arrays

AI-centric workloads driving high-density flash

arrays

| +2.1% | National, concentrated in hyperscale facilities | Short term (≤ 2 years) | |||

PDPA compliance spurring in-country data residency

PDPA compliance spurring in-country data residency

| +0.8% | National, with emphasis on financial and healthcare sectors | Medium term (2-4 years) | |||

Shift to renewable-powered "green" data

centers

Shift to renewable-powered "green" data

centers

| +0.6% | National, with pilot projects in industrial estates | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Hyperscale and Cloud Provider Capex Boom

Foreign hyperscalers have pledged multi-billion-dollar outlays that immediately lift the Thailand data center storage market. AWS opened its local region in January 2025 following a USD 5 billion commitment, unlocking near-term orders for petabyte-scale SAN and object clusters.[1]Amazon Web Services, “AWS launches Asia Pacific (Thailand) Region,” aws.amazon.com Google’s USD 1 billion facility in Chonburi and TikTok’s enlarged USD 8.8 billion plan confirm rising confidence in the regulatory environment. Hyperscalers favor disaggregated architectures that pool flash and HDD to balance cost and performance. Their arrival steers domestic enterprises toward local cloud zones, spawning secondary demand for backup and tier-2 storage. Collectively, these builds position Thailand as a sovereign-cloud alternative to Singapore.

5G Rollout and Edge Nodes Intensifying Storage Demand

Nationwide 5G coverage multiplies data creation inside factories, hospitals, and smart-city intersections. AIS demonstrated millimeter-wave throughput in manufacturing trials, prompting deployment of NVMe all-flash nodes at edge sites for real-time analytics. Edge storage absorbs sensor bursts locally before funneling refined data to Bangkok core data centers, yielding a two-tier architecture. Automotive and electronics plants along the Eastern Economic Corridor require millisecond-level responses for predictive maintenance, pushing modest capacity but extremely high IOPS. Storage vendors now bundle compact flash systems with orchestration software to fit these constrained edge racks. Early adopters report trimmed WAN bandwidth costs and shorter quality-control cycles, fueling broader industrial adoption.

AI-Centric Workloads Driving High-Density Flash Arrays

AI model training needs sustained throughput and rapid checkpoints, so hyperscale halls are swapping vast HDD pools for dense NVMe drives. STT GDC is designing AI clusters that draw 15-20 MW per hall, roughly triple a standard cloud hall, which elevates the value of flash that reduces rack count.[2]Bangkok Post Business Desk, “STT GDC builds AI-ready data centres,” bangkokpost.com Western Digital introduced a 64 TB eSSD aimed at large AI data lakes, aligning with inference clusters that rely on low-latency reads. Thai universities consequently request shared flash namespaces to support Thai-language models, widening flash adoption across academia and the public sector.

BOI Incentives and Thailand 4.0 Digital Policy

The BOI grants tax holidays and accelerated depreciation on data infrastructure, rendering Thailand cost-competitive inside ASEAN. Forty-seven projects totaling USD 5.1 billion had been approved by March 2025, with storage hardware representing roughly one-quarter of that bill. Thailand 4.0 promotes e-government, digital health, and smart logistics, each of which requires secure domestic data pools. New Digital Park zones come pre-wired with fiber and redundant power, easing entry barriers. Incentives include lower import duties on HDDs and SSDs assembled locally, nudging multinationals to favor Thai factories over Vietnam. These policies stabilize demand during global IT spending slowdowns.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capex for flash SAN platforms High capex for flash SAN platforms | -1.8% | National, affecting enterprise and SME segments | Short term (≤ 2 years) | (~)% Impact on CAGR Forecast:

-1.8%

|

Geographic Relevance

:

National, affecting enterprise and SME segments

|

Impact Timeline

:

Short term (≤ 2 years)

|

Rising electricity prices power-supply limits Rising electricity prices power-supply limits | -1.4% | National, concentrated in industrial estates | Medium term (2-4 years) | |||

Limited submarine-cable diversity elevates latency

risk

Limited submarine-cable diversity elevates latency

risk

| -0.9% | National, affecting international connectivity | Long term (≥ 4 years) | |||

Shortage of advanced storage-management talent

Shortage of advanced storage-management talent

| -1.1% | National, concentrated in Bangkok metropolitan area | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Capex for Flash and SAN Platforms

Mid-market budgets often struggle with the upfront costs of enterprise all-flash arrays, which are three to five times pricier than their hybrid counterparts. While industrial SSD pricing hovers around USD 0.25 per GB, substantially more than consumer drives, many firms in Thailand's data center storage market are prolonging HDD refresh cycles. This delay is pushing back the industry's transition to flash storage. However, TMBThanachart, after implementing Huawei's comprehensive NVMe solution, gained a notable 60% drop in latency.

Rising Electricity Prices and Power-Supply Limits

Power charges can account for up to 50% of data center OPEX, and tariffs rose again in early 2025 despite government relief efforts SolarQuarter.[3] SolarQuarter Editorial, “Thailand data centres seek lower power tariffs,” solarquarter.com High-density AI racks heighten cooling loads, pushing operators to reserve HDD for cold tiers to cut watt-per-terabyte. Industrial estates outside Bangkok face grid caps that postpone expansion plans. Operators now pursue renewable PPAs in Rayong and Chachoengsao to lock energy rates. Renewable deals improve the carbon footprint, yet interconnection delays can stall storage rollouts.

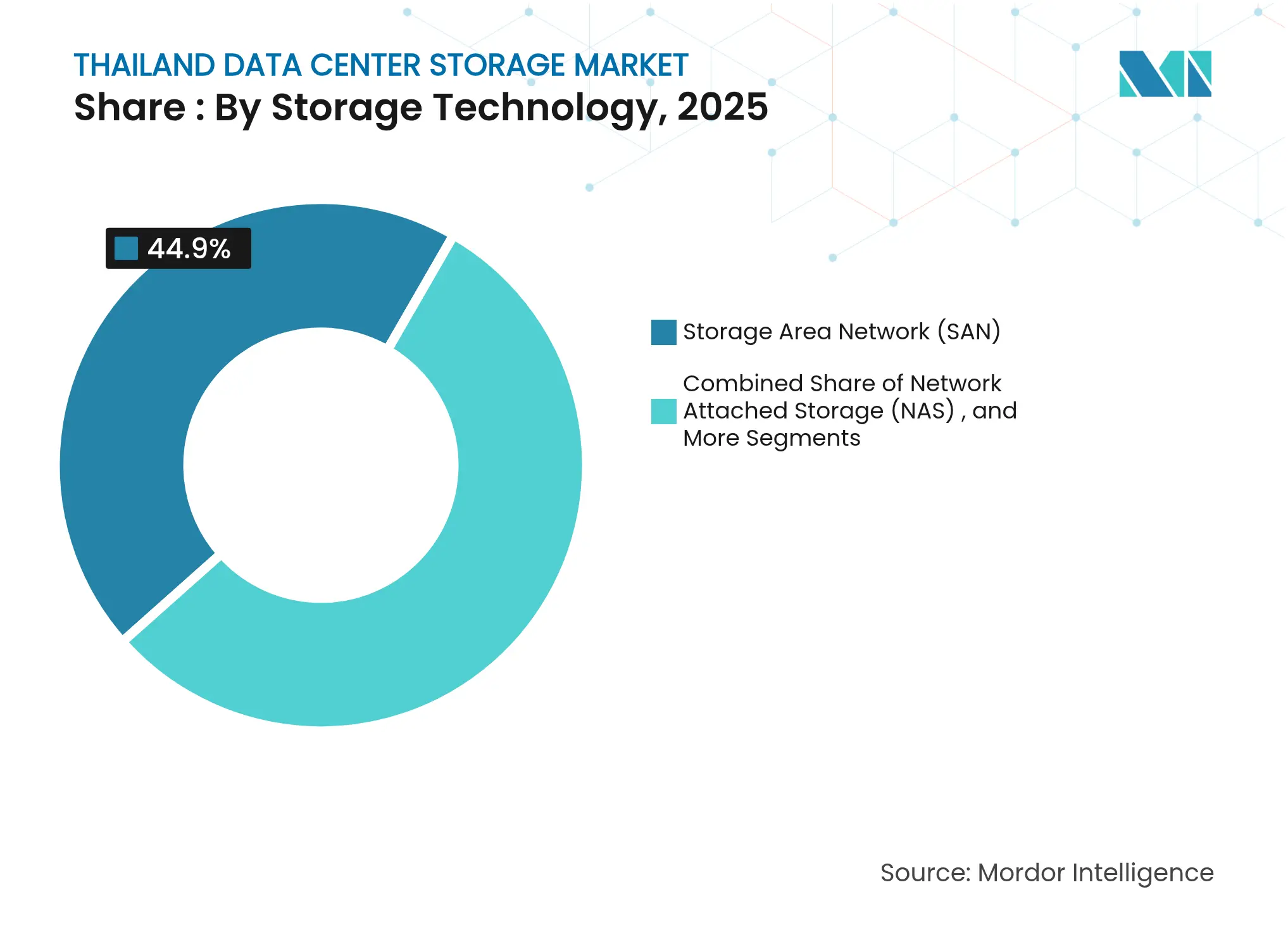

By Storage Technology: SAN Remains Core While Object Platforms Surge

SAN delivered 44.90% of 2025 revenue because banks and telecom carriers still rely on deterministic latency and proven Fibre Channel tooling. Most enterprises continue to allocate tier-1 databases and virtual machine clusters to these arrays, confirming the technology’s foundational role in the Thailand data center storage market. Object and tape storage, however, is on course for a 9.05% CAGR as hyperscalers add petabyte-scale data lakes for AI training sets. Object systems scale nearly linearly and align with Thailand data center storage market size projections for long-tail unstructured data growth.

NVMe-over-Fabric extensions now enter mainstream SAN portfolios to protect relevance, yet cost sensitivity nudges secondary workloads toward software-defined object clusters built on commodity x86 nodes. LTO-9 tape revival satisfies long-term compliance for health records governed by the PDPA. Vendors bundle tiering engines that shift cold datasets from flash to tape automatically, trimming OPEX. Across edge deployments, small SAN appliances yield to lightweight object gateways that replicate back to Bangkok regions, marking a pivot toward scale-out design principles in the Thailand data center storage market.

Note: Segment shares of all individual segments available upon report purchase

By Storage Type: HDD Dominance Faces Flash Inflection

HDD arrays supplied 44.60% of total capacity in 2025 because Thailand manufactures more than 80% of the world’s drives, translating into local cost advantages. This position continues to satisfy surveillance, media archive, and backup workloads that prize dollars-per-terabyte economics. Flash, nonetheless, is advancing at a 10.05% CAGR as AI and analytics workloads strain HDD throughput ceilings. Rack-scale NVMe systems reduce floor space, which is critical in Bangkok’s premium colocation halls, raising Thailand data center storage market size for solid-state arrays.

Hybrid systems function as a bridge, combining nearline HDD with TLC flash caches for tiering. Western Digital forecasts 44 TB HAMR drives by 2026, which extends HDD viability, yet hyperscalers increasingly weigh total cost that includes power and staffing. Flash endurance gains and improving QLC economics narrow the price gap every quarter. Enterprises performing SAP HANA or fraud analytics already default to flash, signalling an approaching tipping point in the Thailand data center storage market share held by spinning media.

By Data Center Type: Colocation Leads, Hyperscale Accelerates

Colocation operators owned 55.00% share in 2025 because enterprises favor carrier-neutral space connected by fiber triangles linking Bangkok, Ayutthaya, and Chonburi. Renting racks avoids hefty capital outlays, broadening Thailand data center storage market reach across multinationals with modest footprints. Facilities such as NTT Bangkok 2 provide 3,800 m² of white space and 5 MW IT load alongside SLA-based uptime guarantees.

Hyperscaler footprints, however, are rising at an 10.95% CAGR. AWS, Google, and Microsoft choose greenfield sites in the Eastern Economic Corridor, where 20-MW hall modules are feasible. Hyperscalers standardize on disaggregated architectures that pool storage over RDMA fabrics, shifting vendor engagement toward component-level supply. Their spending spills into local supply chains for racks, batteries, and network gear, adding indirect lift to the Thailand data center storage market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End User: IT-Telecom Governs, Healthcare Scales Fast

IT and telecommunications delivered 36.60% share in 2025, driven by internal cloud, streaming, and 5G service traffic. Operators such as AIS and True IDC run regional clouds to keep data local, reinforcing demand for secure SAN plus scalable object stores. Stable upgrade cycles provide a baseline for the Thailand data center storage market.

Healthcare and life sciences is growing at a 10.08% CAGR as e-health mandates spur PACS imaging and genomic research. Bangkok Dusit Medical Services now manages 5 million patient records on MongoDB Atlas, generating terabytes of new data daily MongoDB. Regulations that require seven-year record retention push hospitals toward tape vaults and immutable snapshots. Vendors supply out-of-the-box encryption and audit trails to align with PDPA, thereby enlarging the Thailand data center storage industry footprint in medical hubs.

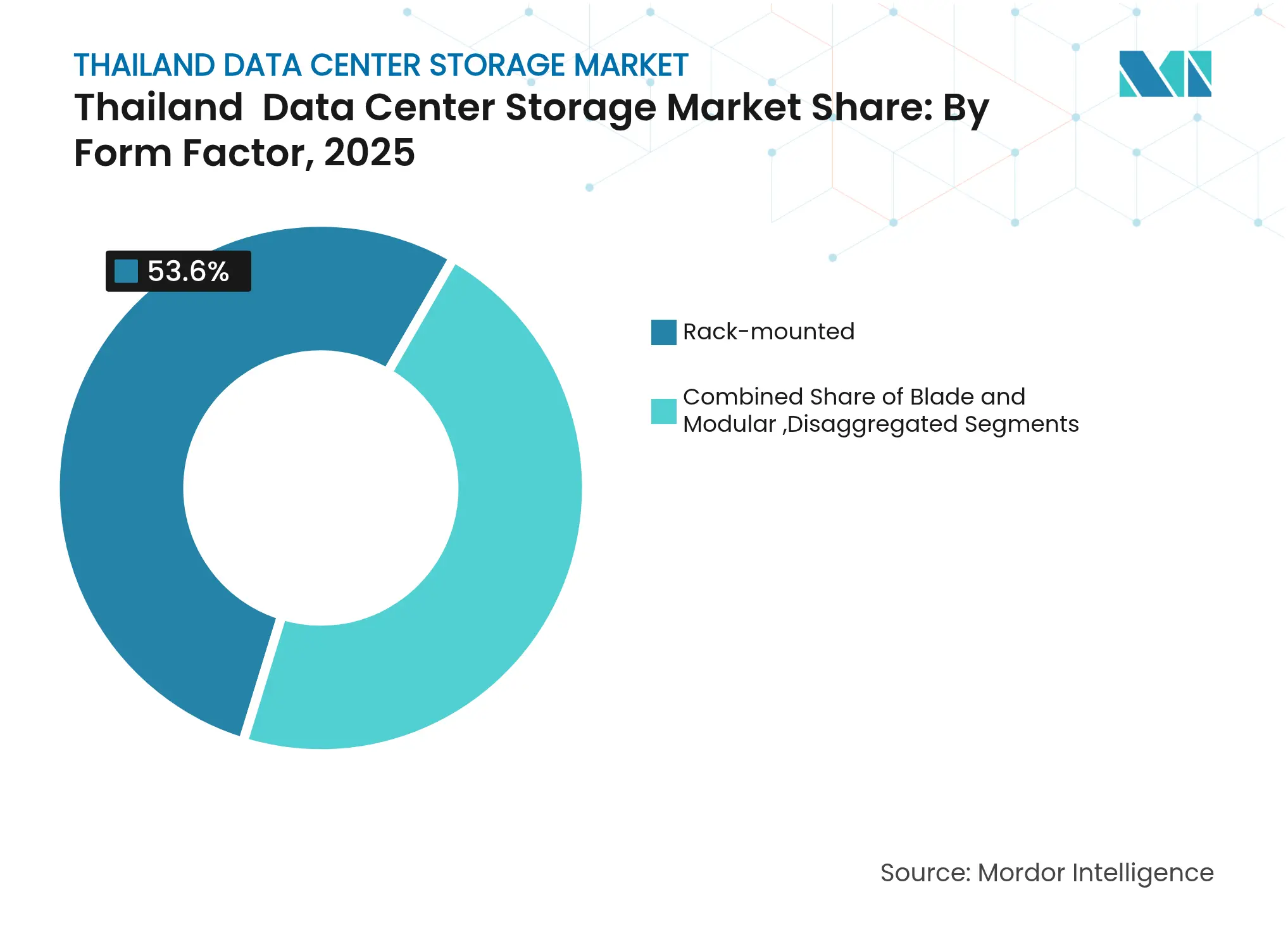

By Form Factor: Rack Stability Meets Composable Momentum

Rack-mounted enclosures retained 53.60% share in 2025 because predictable deployment and compatibility with existing cooling systems remain important to enterprises. Pre-cabled racks also cut installation time in high-cost Bangkok metros.

Composable architectures, however, are progressing at an 11.02% CAGR as software detaches drive pools from compute sleds. Western Digital’s RapidFlex Ethernet interposers place NVMe drives on fabric, reducing stranded capacity and boosting utilization. Composable stacks allocate shared flash volumes dynamically, serving bursty AI workloads for fintechs and media studios. As halls densify, operators adopt chassis-level liquid cooling that pairs well with composable flash, signalling broader uptake inside the Thailand data center storage market.

Note: Segment shares of all individual segments available upon report purchase

By Interface: SAS/SATA Legacy Gives Ground to NVMe

SAS and SATA still carry 57.10% of Thai enterprise blocks because of proven reliability and mature management tools. Fibre Channel preserves footholds in tier-1 banking but shows flat growth. NVMe is expanding at a 12.35% CAGR, propelled by AI, real-time analytics, and high-frequency trading that require sub-millisecond response times. TMBThanachart documented shorter query times after migrating to end-to-end NVMe, demonstrating clear ROI.

NVMe-over-TCP accelerates adoption by exploiting existing Ethernet fabrics. Vendors now include utilities that clone SAS volumes to NVMe pools with minimal downtime, simplifying migration. With NAND costs falling and controller maturity rising, NVMe is projected to exceed one-third of the Thailand data center storage market size by 2028.

Thailand’s central ASEAN location cuts latency to Hong Kong and Shanghai by more than 20 milliseconds, positioning Bangkok as a connectivity hub. Dense metro fiber rings and proximity to Suvarnabhumi Airport facilitate rapid parts logistics, supporting the Thailand data center storage market. The Eastern Economic Corridor—covering Chonburi and Rayong—attracts hyperscale projects due to land availability and dual-feed substations, while import-duty waivers on IT equipment further entice operators.

Submarine cable projects strengthen international bandwidth. A THB 5 billion subsidy supports new landing stations linked to the AAE-1 cable, reducing Bangkok-to-Tokyo distance. Carrier-neutral nodes such as CAT Neutral Gateway lower last-mile costs, making it feasible for smaller SaaS vendors to localize workloads. Expanding 5G coverage into Chiang Mai and Khon Kaen lifts regional demand for edge caches, broadening the Thailand data center storage market beyond the capital. Competition with Singapore and Malaysia is intense, yet Thailand leverages its HDD manufacturing ecosystem and bilingual workforce. Wage levels sit between high-cost Singapore and low-cost Vietnam, striking an attractive balance for multinationals seeking skilled technicians. Political stability since the 2024 election has reassured investors. As a result, geographic and policy factors converge to consolidate Thailand’s role as an AI-ready infrastructure gateway for ASEAN.

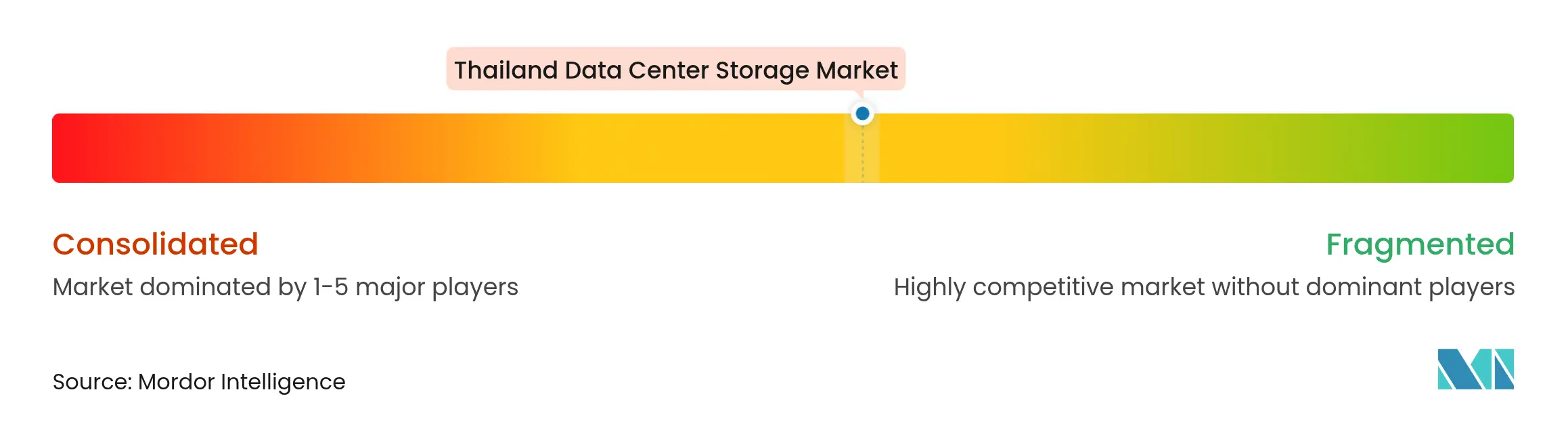

Market Concentration

Thailand’s data center storage arena shows moderate concentration. Global suppliers—Dell Technologies, Hewlett Packard Enterprise, NetApp, Huawei, and Western Digital—win large enterprise and hyperscale contracts through global service guarantees and broad product portfolios. Local providers such as True IDC, TCC Technology, NTT, and SUPERNAP Thailand focus on domestic firms needing Thai-language support and flexible pricing. This dual structure nurtures variety inside the Thailand data center storage market.

Strategic alliances influence competition. NetApp teams with Google Cloud for turnkey hybrid bundles, while Dell cooperates with Nvidia on AI-tuned flash nodes. Western Digital promotes an AI Data Cycle framework that positions its 64 TB eSSD as the backbone for training clusters Western Digital. Local integrators embed these drives into container platforms to offer “AI-as-a-Service” for universities and media houses.

Sustainability now differentiates bids. NTT operates Bangkok 2 on a 100% renewable PPA, winning ESG-minded clients. STT GDC uses chilled water cooling to push PUE below 1.3, while vendors recommend tiering cold data to HDD and tape to curb power per terabyte. As electricity tariffs continue to climb, efficiency stands beside performance on procurement scorecards, favoring suppliers with clear energy roadmaps.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. Market Size and Growth Forecasts (Value)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES and FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study defines Thailand's data-center storage market as domestic revenue from purpose-built hardware and associated software that capture, protect, and retrieve digital information inside colocation, hyperscale, enterprise, and edge halls. Covered technologies include network-attached storage, storage-area networks, direct-attached arrays, object libraries, tape systems, and the management layers that enable them.

Scope Exclusion: Consumer external drives, personal cloud boxes, and ad-hoc server disk upgrades installed outside data centers are excluded.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Interviews with infrastructure architects, colocation managers, and value-added resellers across Bangkok, Chonburi, and Chiang Mai revealed rack-level utilization and discount structures.

Short surveys of IT heads in BFSI and healthcare validated storage-to-compute ratios and planned migrations, allowing us to reconcile desk findings with field realities.

Desk Research

Our team began with open datasets from the Ministry of Digital Economy and Society, National Statistical Office, customs declarations, and Board of Investment filings to map imports and local assembly of disk arrays and flash modules. White papers from the Thai Data Center Association, ASEAN Data Center Alliance, and IEEE journals clarified technology mix and refresh cycles, while 10-Ks, investor decks, and reputable press refined pricing curves.

Paid sources, D&B Hoovers for vendor splits, Dow Jones Factiva for deal flow, and Questel for patent momentum, deepened insight. These references are illustrative; many additional materials informed checks and context building.

Market-Sizing & Forecasting

A top-down model reconstructed annual spend from import, production, and trade data, then was sense-checked bottom-up by multiplying sampled average selling prices with installed petabyte additions reported by key suppliers. Core variables, rack count growth, usable capacity per rack, flash share shifts, hyperscaler capex, and PDPA-driven data-residency needs, anchor the model. Multivariate regression with ARIMA overlays links spend to national IT investment, e-commerce transaction value, and 5G subscriber growth; scenario analysis tests currency swings and rollout delays. Expert-agreed factors bridge any residual gaps.

Data Validation & Update Cycle

Outputs pass variance checks, peer review, and senior sign-off. Figures refresh annually, with mid-cycle updates triggered by large facility announcements or policy shifts. Before release, an analyst reruns inputs so clients receive the latest view.

Why Our Thailand Data Center Storage Baseline Commands Reliability

Benchmark comparison

Published figures differ because firms fold in varying assets, pricing ladders, and refresh cadences. By focusing strictly on in-facility storage revenue and applying consistent currency conversion, Mordor's baseline avoids inflation from construction capex or network services. Differences elsewhere often stem from broader scopes, spot-rate conversions, or aggressive hyperscale extrapolations; our dual-model cross-checks and annual refresh keep totals dependable.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 0.20 B (2024) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 1.56 B (2024) | Regional Consultancy A | Counts full data-center investments, not just storage | ||

USD 0.65 B (2023) | Trade Journal B | Includes servers and network gear; earlier base year | ||

USD 0.22 B (2023) | Industry Association C | Uses spot THB conversion and a partial facility list |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.