Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

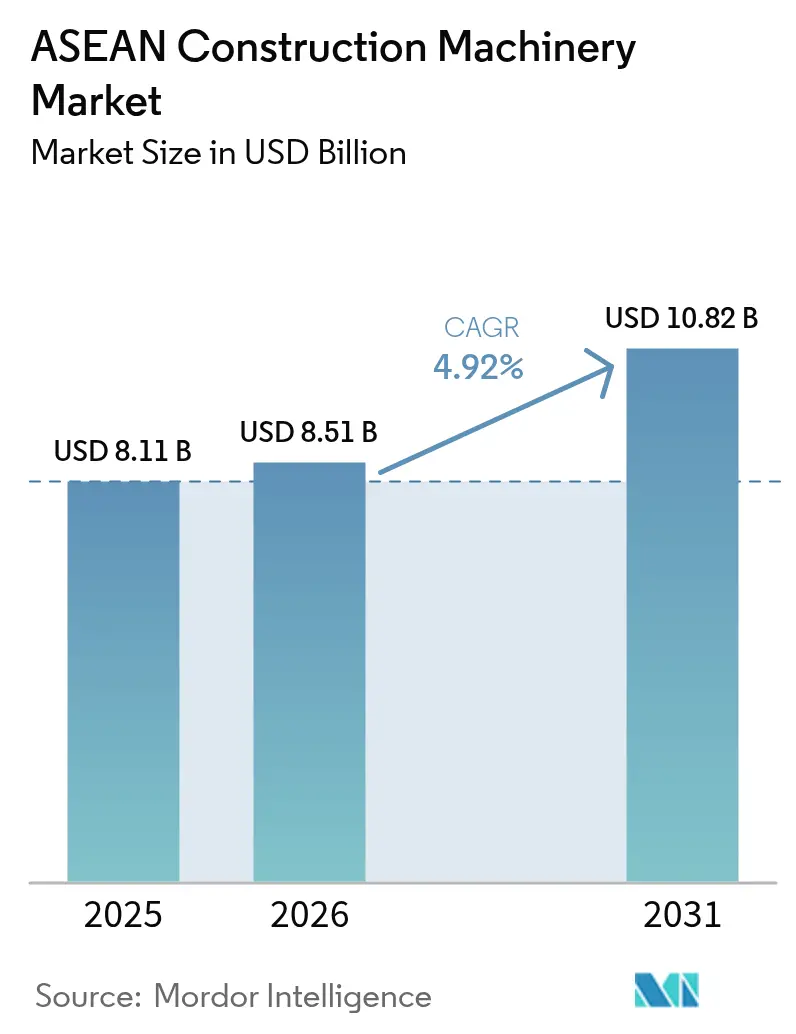

| Base Year Market Size (2025) | USD 8.11 Billion |

| Market Size (2026) | USD 8.51 Billion |

| Market Size (2031) | USD 10.82 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

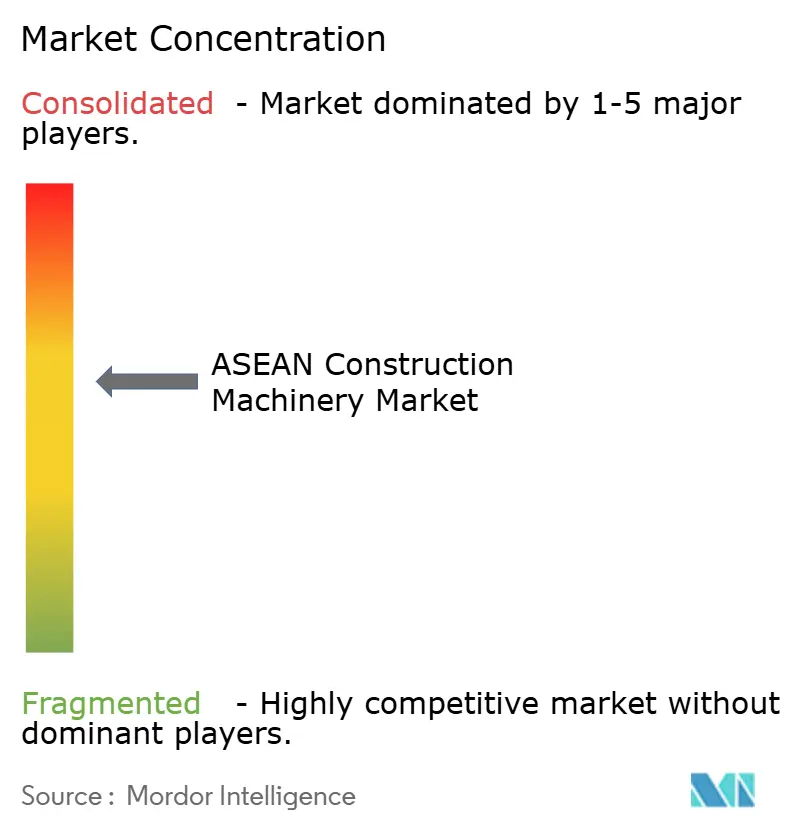

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Construction Machinery Market Analysis by Mordor Intelligence

The ASEAN Construction Machinery Market size was valued at USD 8.11 billion in 2025 and is estimated to grow from USD 8.51 billion in 2026 to reach USD 10.82 billion by 2031, at a CAGR of 4.92% during the forecast period (2026-2031). Indonesia's ambitious Nusantara capital-city project and the high-speed rail corridor linking Thailand and Vietnam are not just monumental undertakings; they're reshaping the landscape of equipment procurement. As these megaprojects unfold, equipment procurement cycles are stretching, and the pool of available machinery is expanding. Meanwhile, in the mineral-rich regions of Sulawesi and Maluku, expansions in nickel mining are driving a surge in demand for excavators, particularly those in the large-capacity range, extending beyond traditional infrastructure projects. Chinese OEMs, notably XCMG and Sany, are making significant inroads, thanks in part to the Belt and Road contractor-localization rules. They are leveraging their ability to deliver parts quickly, allowing them to undercut established Japanese suppliers by a notable margin. On job sites, the push for digitalization is evident. With mandates like BIM Level 2, the advent of 5G telematics, and the rise of semi-autonomous grade-control systems, fleet owners are increasingly leaning towards tech-driven renewals. This shift comes even as they navigate tighter project financing rates and a shortage of operators. While battery-electric models are still in their infancy, they stand to gain significantly. Singapore's mandate for zero-emission equipment in public contracts underscores the importance of sustainability and positions early adopters to tap into lucrative aftermarket charging-service revenues.

Key Report Takeaways

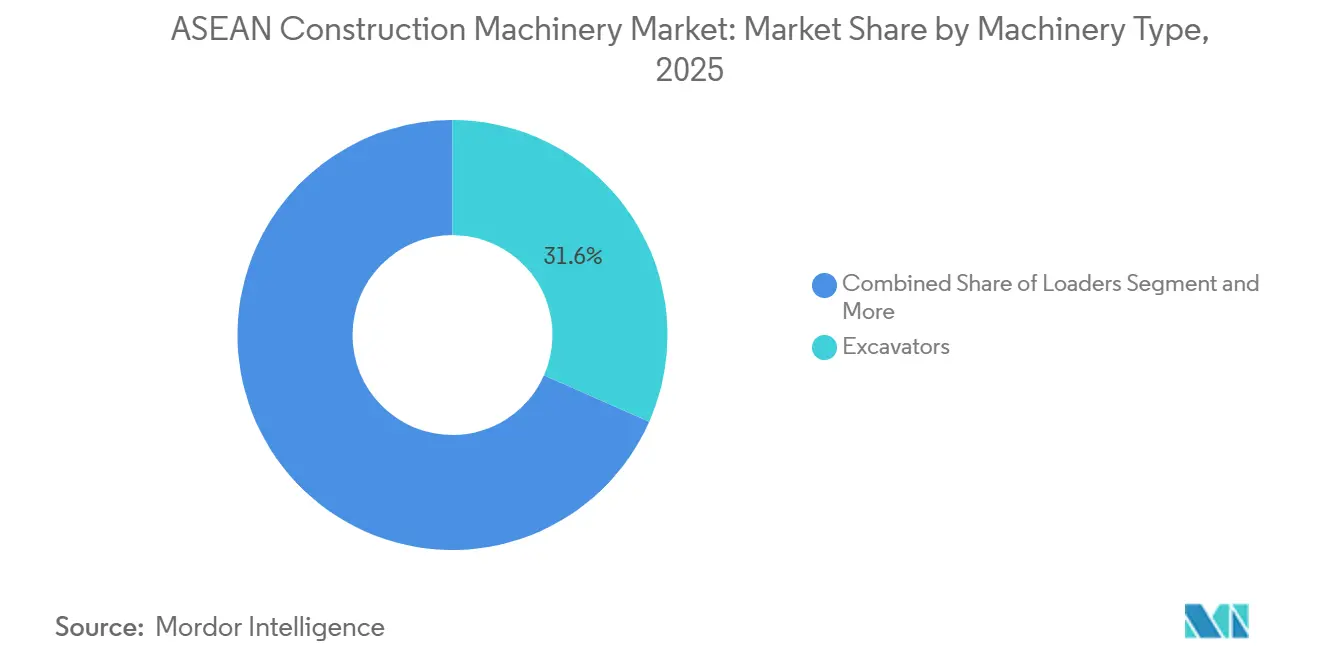

- By machinery type, excavators held 31.61% of the ASEAN construction machinery market share in 2025, while backhoe loaders are projected to post a 5.94% CAGR through 2031.

- By application, earth-moving captured 54.15% of the ASEAN construction machinery market in 2025; utilities installation is advancing at a 6.8% CAGR through 2031.

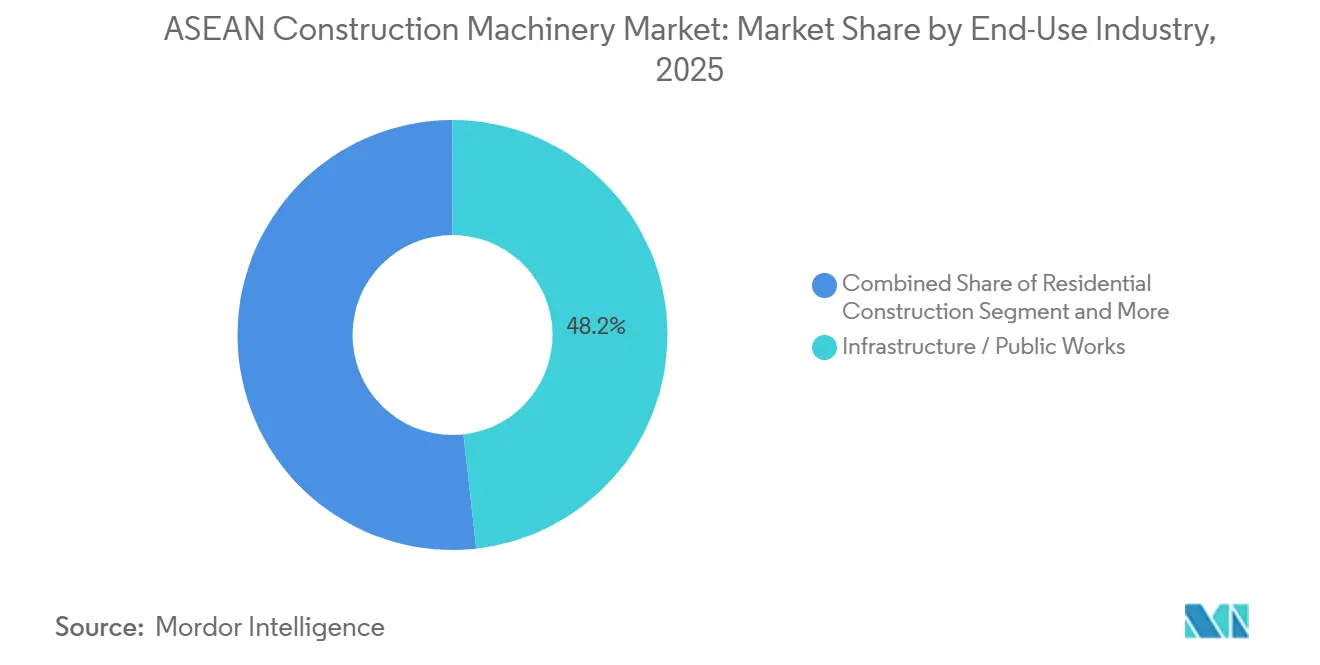

- By end-use industry, infrastructure and public works accounted for 42.23% of the ASEAN construction machinery market in 2025 and will expand at a 5.8% CAGR through 2031.

- By propulsion, diesel equipment retained a 61.39% share in 2025, whereas battery-electric units are forecast to grow at a 10.99% CAGR to 2031.

- By geography, Indonesia led with 39.62% of regional demand in 2025; Vietnam is set to register the fastest 5.61% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Construction Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Super-Cycle | +1.8% | Indonesia, East Kalimantan, Nusantara | Long term (≥ 4 years) |

| Nickel-Mine Boom | +1.5% | Indonesia, Sulawesi, Kalimantan | Medium term (2-4 years) |

| High-Speed Rail Corridor | +1.2% | Thailand, Vietnam, Mekong Delta | Medium term (2-4 years) |

| Strong FDI Inflows | +1.0% | Vietnam, Indonesia, Thailand, Malaysia | Short term (≤ 2 years) |

| Belt and Road Contractor-Localization | +0.8% | Indonesia, Thailand, Malaysia, Philippines | Medium term (2-4 years) |

| Job-Site Digitalization | +0.6% | Singapore, Malaysia, Thailand, Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Super-Cycle Driven by Indonesia’s IKN Capital-City Build

Indonesia’s relocation of its administrative center to Nusantara has unleashed a ~ USD 32 billion multi-year construction wave spanning 256,000 hectares [1]“IKN Earthworks Schedule,”, Jakarta Post Staff, thejakartapost.co. The first phase requires extensive earthworks and enforces local-content thresholds for machinery, prompting joint ventures between global OEMs and local assemblers. Hitachi has increased production of its ZAXIS-7G excavators at its Karawang facility. At the same time, XCMG has opened a parts hub in Jakarta, which has notably decreased contractor downtime. In Samarinda and Balikpapan, the growing need for worker housing and logistics parks is driving equipment usage beyond just the primary sites. Although land-acquisition delays have slowed procurement, the construction program maintains a steady pipeline for the foreseeable future.

Nickel-Mine Boom Fuelling Demand for Ultra-Large Excavators

Production of battery-grade nickel is expected to grow significantly, leading to higher strip ratios at Sulawesi's laterite deposits. This shift has made it essential to employ hydraulic excavators equipped with six-cubic-meter buckets. In a strategic move, Hitachi commenced local assembly of its equipment, effectively reducing lead times and sidestepping hefty import duties. While Caterpillar and Komatsu continue to lead the market, competitors Sany and XCMG are making waves by offering discounts and ensuring rapid parts logistics through their localized hubs. Under Indonesia’s Mining Law, the introduction of telematics-based dust-suppression packages has increased unit capital expenditure, but this move ensures fleets are in line with ESG audits. However, a potential dip in global EV demand might temper orders in the forecast period.

Thailand–Vietnam High-Speed Rail Corridor Boosting Cross-Border Equipment Demand

Vietnam's North-South railway, with an investment of USD 67 billion, and Thailand's Bangkok-Nong Khai railway are set to consume substantial amounts of ballast and concrete. This underscores sustained demand for graders, pavers, and rollers over a vast stretch. In Thailand's Eastern Economic Corridor, Komatsu's semi-autonomous excavators have reduced operator hours and enhanced grade accuracy. In Laos and Cambodia, the logistics of prefabricated bridge segments are driving up crane and telehandler rental rates due to undersized domestic fleets. However, challenges loom as Vietnam grapples with a high debt-to-GDP ratio, raising concerns over potential shifts in sovereign ratings and subsequent disbursement delays.

Strong FDI Inflows into ASEAN Industrial Parks and Sezs

ASEAN attracted a significant share of manufacturing and logistics foreign direct investment (FDI). Leading the region, Vietnam secured a notable portion, followed by Malaysia. Johor’s Special Economic Zone (SEZ) attracted substantial investments, allocated to semiconductor and data center sites, each requiring extensive floor space. The ASEAN construction machinery market experienced strong growth, driven by the popularity of backhoe loaders, particularly for trenching and drainage tasks on greenfield estates. JCB’s 3DX Xtra ecoXcellence offers a considerable reduction in fuel consumption. Meanwhile, in Vietnam, competitive lease rates for excavators, significantly lower than ownership costs, are driving increased rental adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Finance Rates | -1.2% | Indonesia, Thailand, Philippines, Malaysia | Short term (≤ 2 years) |

| Certified Operator Shortage | -0.8% | Indonesia, Thailand, Vietnam, Philippines | Medium term (2-4 years) |

| Sparse Charging / Hydrogen Refuelling Network | -0.6% | Singapore, Malaysia, Thailand, Vietnam | Long term (≥ 4 years) |

| China–US Trade Volatility | -0.4% | Indonesia, Thailand, Malaysia, Singapore | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex and Tightening Project-Finance Rates

In Thailand, leasing rates for a standard 20-ton excavator priced within a specific range are now higher. In Indonesia, the rate is also higher. This marks an increase from the previous rates. A hike in basis points translates into an additional cost in the net present value of a five-unit fleet, putting pressure on contractors with fixed-price bids. Delays in disbursements from the Maharlika Investment Fund have already pushed back equipment orders for the North-South Railway. While rental options provide some relief—Vietnam's daily excavator rental rate often proves more economical than ownership for projects lasting under a year—credit-approval ratios have declined, reflecting a significant drop from the previous period.

Shortage of Certified Operators Inflating OPEX

ASEAN faces a significant operator shortfall, with certifications growing slowly each year. Operator wages in Vietnam have increased substantially, while only a small percentage of operators in the Philippines have met the new TESDA standards. Inexperienced crews are contributing to higher repair costs and increased downtime. Additionally, Malaysia's freeze on Bangladeshi labor work permits has further tightened supply. However, semi-autonomous systems are helping to mitigate the shortages. For example, Komatsu's PC200i-12 allows operators, with minimal training, to achieve grade tolerances that previously required extensive experience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Backhoe Loaders’ Versatility Spurs Growth

Excavators are commanding 31.61% of the 2025 ASEAN construction machinery market share. Backhoe loaders posted a 5.94% CAGR, surpassing excavators. Emerging municipal-utilities work in secondary Vietnamese and Philippine cities values one machine that both digs and loads. Loaders hold a significant share of the ASEAN construction machinery market, driven by port expansions and increasing material-handling demands. Cranes also maintain a notable share, supported by the rise in high-rise constructions in Bangkok and Ho Chi Minh City.

Rental trends bolster this momentum: contractors frequently rent backhoe loaders, surpassing the rental rate for excavators. This approach helps mitigate capital pressures, particularly in a high-interest-rate environment. JCB’s 3DX Xtra, featuring a Tier 4 Final engine, highlights the industry's focus on fuel-efficient, multifunctional equipment, especially in Build-Operate-Transfer water projects. Komatsu’s semi-autonomous PC200i-12, equipped with intelligent controls, reduces grade times and accelerates operator training, signaling a technological shift in fleet dynamics across the ASEAN construction machinery landscape.

By Application: Earth-Moving Dominance, Utilities Installation Acceleration

Earth-moving remained the largest slice of the ASEAN construction machinery market, accounting for 54.15% in 2025, underpinned by land reclamation and flood-control embankments in Indonesia, Vietnam, and the Philippines. Utilities installation, however, will grow fastest at a 6.8% CAGR as 5G rollouts and aging water networks in dense metros demand narrow-trench precision that favors compact equipment.

Concrete and road construction, holding a significant share, aligns closely with high-speed rail and MRT projects. Meanwhile, mining support sees a boost from surging nickel-ore outputs. In Singapore, the demolition-and-recycling sector, despite its modest share of demand, is expanding rapidly. This growth is driven by a waste-recycling mandate, necessitating specialized crushers and sorters. Such diverse applications not only mitigate cyclicality but also underscore their significance in maintaining revenue streams across the ASEAN construction machinery market.

By End-Use Industry: Infrastructure Pipeline Sustains Equipment Demand

Infrastructure and public works accounted for 42.23% of the ASEAN construction machinery market in 2025 and should post the highest 5.8% CAGR, as metro rail, expressway, and port projects exceed USD 320 billion through 2030. Residential construction accounted for a significant share, driven by affordable housing initiatives, though higher mortgage costs cast a note of caution.

Commercial construction benefits from the expansion of data centers and logistics warehouses, while mining rides the tailwinds of Indonesia's nickel boom. The infrastructure sector, with its longer utilization cycle, influences OEM parts strategies. Komatsu’s expanded Malaysian and Singaporean distribution centers aim to capture downstream service revenue, reinforcing brand stickiness in the ASEAN construction machinery market.

By Propulsion: Diesel Retains Majority as Battery-Electric Gains Traction

Diesel equipment still held 61.39% of the ASEAN construction machinery market share in 2025, owing to energy density and rapid refueling. Battery-electric machines, however, are expected to grow at a 10.99% CAGR through 2031, catalyzed by Singapore’s 2030 zero-emission public project rule and Malaysia’s tariff waivers. Hybrid models are bridging the gap, harnessing energy in swing cycles without the need for charging infrastructure.

While charge times and duty windows pose challenges for electric adoption in remote megaprojects, they align well with urban tunneling and indoor logistics. Although diesel's dominance is set to wane—thanks to a drop in lithium-ion pack costs—fleet owners still favor the well-established diesel-service network. In contrast, the electric-service network boasts limited points across the ASEAN construction machinery market.

Geography Analysis

Indonesia anchored 39.62% of 2025 demand, bolstered by the Nusantara program and nickel mine expansions that together require 200 million m³ of earthworks and continuous deployment of ultra-large excavators. Hitachi’s local assembly reduced delivery cycles to 10 months and muted rupiah-driven import price spikes, while currency depreciation pushed contractors toward domestically assembled units [2]“Karawang Plant Milestone,”, Hitachi Construction Machinery, hitachicm.com. Vale Indonesia’s HPAL plants further extend overburden removal demand, keeping the ASEAN construction machinery market firmly weighted toward the archipelago.

Vietnam will log the region’s fastest CAGR of 5.61%, backed by significant investments in high-speed railway projects and foreign direct investment in electronics and EV battery parks. Vietnam is witnessing a surge in backhoe-loader and compactor rentals. While swift site-preparation timelines fuel this demand, rising operator wages and potential shifts in sovereign ratings pose challenges. Notably, with a high rental penetration for compact gear, the Vietnamese segment of the ASEAN construction machinery market is demonstrating a quick adaptability to capital-cost pressures.

Thailand, with a substantial market share, is driven by projects such as significant rail developments, industrial estates, and trials of autonomous equipment. While Chinese OEMs, exemplified by locally built cranes, are making their mark, Japanese brands are holding their ground with offerings such as semi-autonomous controls and attractive finance packages. Although leasing rates have risen slightly, dampening contractor enthusiasm, these concerns are mitigated by productivity boosts from Smart Construction.

The Philippines, which accounts for a notable share of demand and projects steady growth, faced delays in equipment orders due to funding bottlenecks. While mandatory operator certifications have led to wage inflation, reforms in the mining sector are carving out opportunities for medium-sized excavators. Malaysia, with a significant market share, is riding high on the nearing completion of primary rail links and commitments to special economic zones. Furthermore, tariff concessions on electric machines are positioning Kuala Lumpur as a pioneering ground for zero-emission fleets. Singapore, contributing a smaller share to the market, is experiencing modest growth. While land scarcity limits absolute volumes, mandates for BIM and zero-emission vehicles are creating lucrative demand pockets. The remaining members of ASEAN, together holding a minor share, are leaning on developments such as rail extensions and port upgrades, though instability in Myanmar is curbing wider adoption.

Competitive Landscape

In the ASEAN construction machinery market, competition remains fragmented, with no OEM holding more than a minimal stake. Localization 2.0 has emerged as the strategic frontier: Hitachi has set up an ultra-large excavator assembly in Indonesia. At the same time, Komatsu's expansion at Bangkok Motor Works not only shortens lead times but also helps avoid import duties. This move bolsters the reputation of these Japanese incumbents for ensuring uptime. Furthermore, Komatsu's PC200i and PC220LCi models now feature cloud-based grade controls, streamlining operator training and boosting lifecycle economics.

Chinese firms are capitalizing on Belt and Road content regulations to expand rapidly. XCMG has secured a significant crane contract in Thailand, and its expedited logistics for parts in Jakarta highlight the maturity of its service network. Meanwhile, Sany is eyeing a Southeast Asian production boost, aiming to generate a substantial portion of its revenue from overseas, thanks to its planned IPO. Despite aggressive pricing strategies, with significant price gaps and extended payment terms, clinching initial equipment deals, brand loyalty remains tethered to the long-term availability of parts.

Opportunities abound in battery-electric offerings and predictive maintenance solutions. Volvo's New Generation electric excavators, equipped with ActiveCare Direct, boast a notable reduction in downtime. However, with only a limited number of service points for electric equipment scattered across ASEAN, growth is hampered. In the aftermarket, financing plays a pivotal role: Komatsu Financial offers competitive lease rates, alleviating capital pressures. At the same time, Caterpillar's extensive network of diesel-service centers fosters loyalty among long-time fleet owners. Meanwhile, niche players like JCB, specializing in backhoe loaders, and Doosan, focusing on compact excavators, are carving out their space by emphasizing versatility and lower capital expenditure.

ASEAN Construction Machinery Industry Leaders

Hitachi Construction Machinery Co

Caterpillar Inc.

Mitsubishi Corporation

Komatsu Ltd.

Xuzhou Construction Machinery Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SDLG inaugurated PT SDLG Indonesia Machinery in Jakarta, signing agreements for more than 1,100 machines.

- January 2025: Volvo Construction Equipment launched its New Generation excavators in Southeast Asia, featuring hydraulics that cut fuel use by up to 15% and standard rear-view cameras.

ASEAN Construction Machinery Market Report Scope

The ASEAN construction machinery market report is segmented by machinery type (excavators, loaders, cranes, backhoe loaders, motor graders, pavers and compactors, and others), application (earth-moving, concrete and road construction, material handling and logistics, mining support, demolition and recycling, utilities installation, and others), end-use industry (residential construction, commercial construction, infrastructure/public works, mining, oil and gas, industrial manufacturing, and others), propulsion (diesel, hybrid, battery-electric, hydrogen fuel-cell, and others), and Geography (Indonesia, Thailand, Vietnam, Philippines, Malaysia, Singapore, and Rest of ASEAN). The market forecasts are provided in terms of value (USD) and volume (units).

By Machinery Type

| Excavators |

| Loaders |

| Cranes |

| Backhoe Loaders |

| Motor Graders |

| Pavers and Compactors |

| Others (Telehandlers, Dump Trucks, etc.) |

By Application

| Earth-Moving |

| Concrete and Road Construction |

| Material Handling and Logistics |

| Mining Support |

| Demolition and Recycling |

| Utilities Installation |

| Others |

By End-Use Industry

| Residential Construction |

| Commercial Construction |

| Infrastructure / Public Works |

| Mining |

| Oil and Gas |

| Industrial Manufacturing |

| Others |

By Propulsion

| Diesel |

| Hybrid |

| Battery-Electric |

| Hydrogen Fuel-Cell |

| Others |

By Country

| Indonesia |

| Thailand |

| Vietnam |

| Philippines |

| Malaysia |

| Singapore |

| Rest of ASEAN (Myanmar, Laos, Cambodia, Brunei) |

| By Machinery Type | Excavators |

| Loaders | |

| Cranes | |

| Backhoe Loaders | |

| Motor Graders | |

| Pavers and Compactors | |

| Others (Telehandlers, Dump Trucks, etc.) | |

| By Application | Earth-Moving |

| Concrete and Road Construction | |

| Material Handling and Logistics | |

| Mining Support | |

| Demolition and Recycling | |

| Utilities Installation | |

| Others | |

| By End-Use Industry | Residential Construction |

| Commercial Construction | |

| Infrastructure / Public Works | |

| Mining | |

| Oil and Gas | |

| Industrial Manufacturing | |

| Others | |

| By Propulsion | Diesel |

| Hybrid | |

| Battery-Electric | |

| Hydrogen Fuel-Cell | |

| Others | |

| By Country | Indonesia |

| Thailand | |

| Vietnam | |

| Philippines | |

| Malaysia | |

| Singapore | |

| Rest of ASEAN (Myanmar, Laos, Cambodia, Brunei) |

Key Questions Answered in the Report

How big is ASEAN construction machinery market demand today and where is it heading?

The market stands at USD 8.51 billion in 2026 and is forecast to reach USD 10.82 billion by 2031 at a 4.92% CAGR.

Which country accounts for the largest share of equipment sales?

Indonesia leads with 39.62% of regional demand thanks to the Nusantara capital city build and nickel-mine expansions.

What equipment segment is growing fastest across Southeast Asia?

Backhoe loaders are projected to rise at a 5.94% CAGR through 2031, outpacing excavators due to municipal utilities and residential site-prep demand.

Which OEM strategies are proving most successful in the region?

Localization 2.0—assembling equipment in-country and shortening parts lead times—combined with semi-autonomous and telematics features is helping brands like Hitachi, Komatsu, XCMG, and Volvo CE gain share.

What are the main risks contractors face when procuring machinery?

Higher borrowing costs, a shortage of certified operators, sparse charging networks for green equipment, and supply-chain volatility stemming from China–US trade tensions all pressure total cost of ownership.

Page last updated on: