Tetraacetylethylenediamine (TAED) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 755.05 Million |

| Market Size (2031) | USD 867.44 Million |

| Growth Rate (2026 - 2031) | 2.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tetraacetylethylenediamine (TAED) Market Analysis by Mordor Intelligence

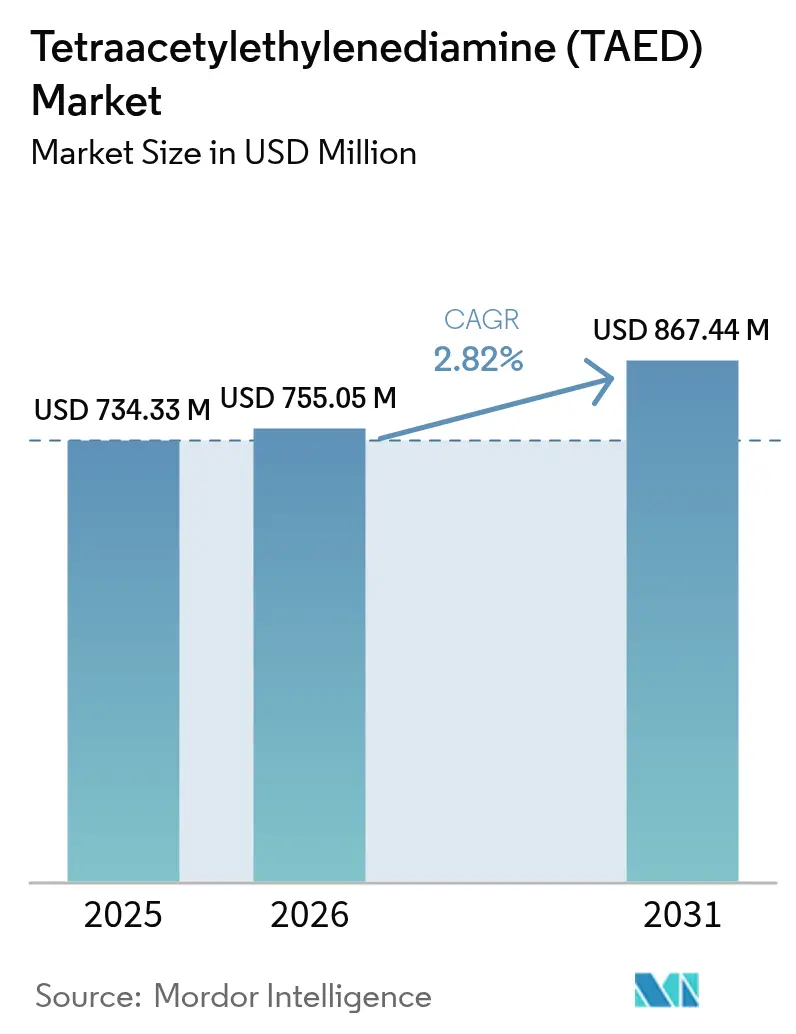

The Tetraacetylethylenediamine Market size is expected to grow from USD 734.33 million in 2025 to USD 755.05 million in 2026 and is forecast to reach USD 867.44 million by 2031 at 2.82% CAGR over 2026-2031. Widespread use of the bleach activator in powder detergents, where it generates peracetic acid and enables effective cleaning at 30–60 °C, anchors current demand. Growth remains slower than the broader laundry detergents sector because TAED is already well-entrenched in mature formulations and faces competition from newer low-temperature activators. Energy-efficiency mandates, the rise of on-premise industrial laundries in Asia, and heightened post-pandemic hygiene standards create steady replacement and upgrade cycles. At the same time, the shift from powder to liquid formats in North America and Europe, along with the emergence of manganese-based catalysts in automatic dishwashing, constrains upside potential.

Key Report Takeaways

- By product type, granular grades held 70.65% of TAED market share in 2025, while encapsulated/co-granulated grades are projected to expand at a 3.52% CAGR through 2031.

- By distribution channel, direct supply captured 60.90% of TAED market share in 2025, whereas chemical distributors record a 3.10% CAGR to 2031.

- By application, household laundry detergents led with 68.55% revenue share in 2025; industrial & institutional laundry is forecast to grow fastest at 3.32% CAGR to 2031.

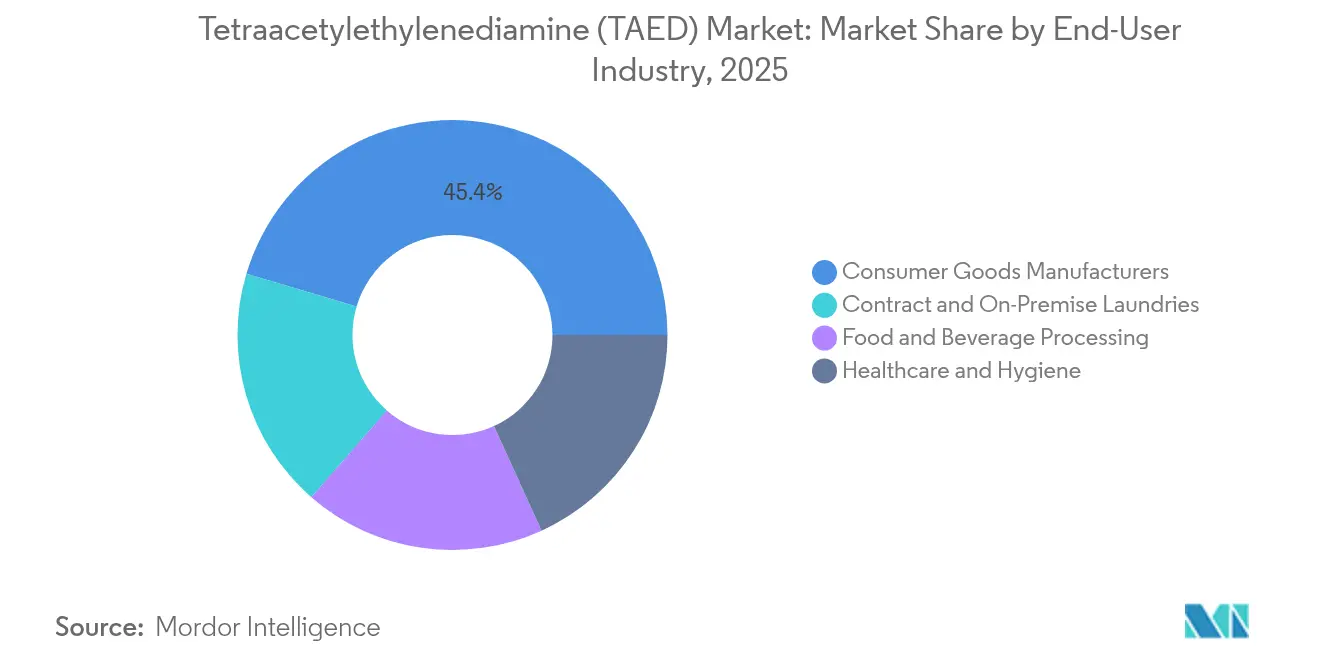

- By end-user industry, consumer goods manufacturers accounted for 45.40% share of the TAED market size in 2025; the healthcare & hygiene segment is advancing at a 3.38% CAGR through 2031.

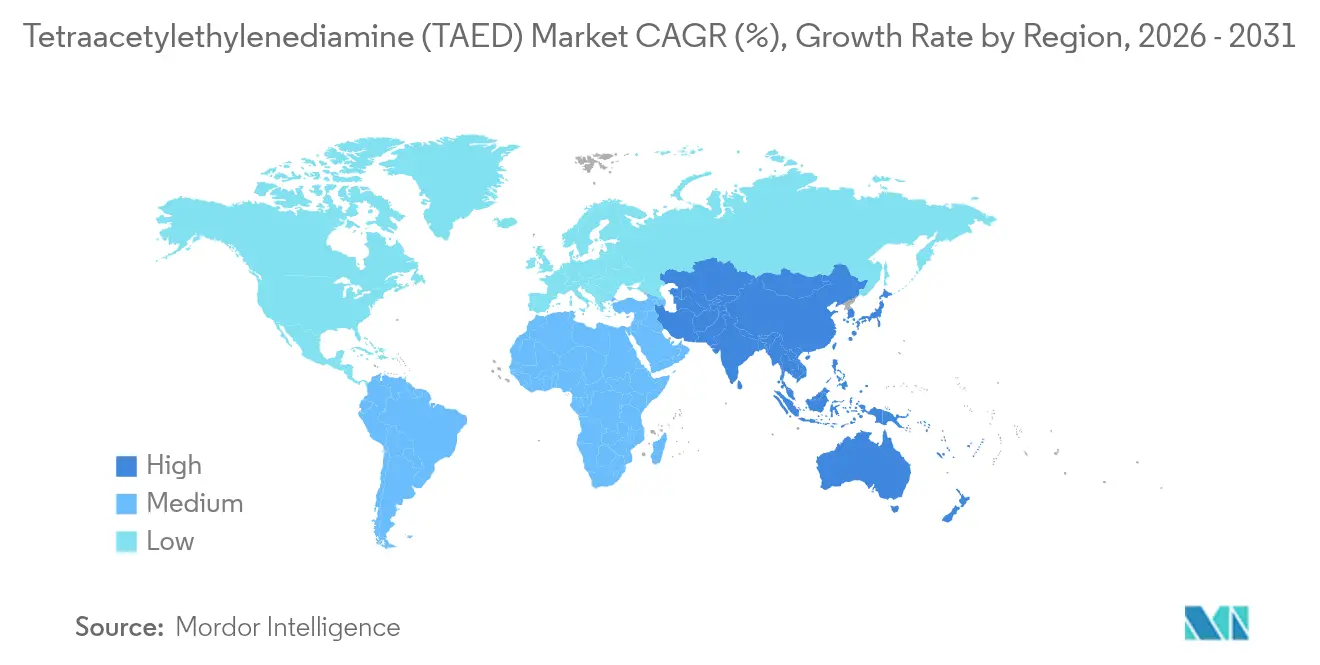

- By region, Europe retained 39.85% of global revenue in 2025; Asia-Pacific is the fastest-growing geography at a 3.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tetraacetylethylenediamine (TAED) Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising shift to low-temperature detergent formulations | +0.8% | Global, with stronger adoption in Europe and North America | Medium term (2-4 years) |

| Growth of on-premise & industrial laundry services in Asia Pacific | +0.6% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Consumer move toward phosphate-free, eco-labels in Europe and North America | +0.5% | Europe & North America | Short term (≤ 2 years) |

| Energy-saving mandates for commercial washers | +0.4% | Global, with regulatory focus in developed markets | Medium term (2-4 years) |

| Emergence of enzyme-TAED hybrid bleach systems | +0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising shift to low-temperature wash cycles

Cold-water adoption can curb laundry-related CO₂ emissions by 27 million t over a decade, making low-temperature activators such as TAED integral to sustainability goals. By enabling effective cleaning at lower temperatures, TAED reduces the reliance on energy-intensive hot water cycles, directly contributing to energy conservation and emission reduction. Tide Professional Coldwater shows commercial viability by lowering wash temperatures to 90 °F and cutting energy costs up to 75%. This significant cost-saving potential makes it an attractive option for both residential and commercial users. Appliance makers and detergent formulators therefore align around chemistry that works without hot water, reinforcing near-term demand for TAED. This alignment highlights the growing importance of sustainable solutions in the detergent market.

Expansion of industrial laundry services in APAC

Rapid urbanization and stricter hygiene codes in hospitals and hotels push Asia-Pacific laundries toward professional detergent systems that guarantee consistent bleaching across variable water quality. The increasing population and urban migration in the region have led to a surge in demand for industrial laundry services, particularly in sectors like healthcare and hospitality, where hygiene is critical. With commercial loads ranging 20–80 lb, chemical cost per cycle becomes a critical metric, as businesses aim to optimize operational costs while maintaining high standards of cleanliness. TAED’s predictable performance at mid-range temperatures offers a cost-effective solution, ensuring consistent results regardless of water quality variations. India’s textile output growth illustrates the scale of downstream demand where reliable commercial laundering is essential[1]Ministry of Textiles India, “Indian Textile Industry Statistics 2025,” texmin.nic.in . The expanding textile industry further amplifies the need for efficient and dependable laundry solutions, positioning TAED as a key component in meeting these demands.

Consumer preference for phosphate-free eco-labels

The European Union’s Detergent Regulation and parallel North American eco-label criteria favor biodegradable activators over phosphorus-based chemistries, bolstering TAED uptake[2]Ecomundo, “EU Detergent Regulation Revision 2025,” ecomundo.eu. These regulations reflect a broader consumer shift towards environmentally friendly products, driven by growing awareness of the environmental impact of traditional detergents. Inclusion of TAED on the U.S. EPA Safer Choice list further signals regulatory endorsement, providing consumers with confidence in its safety and sustainability. This regulatory backing not only supports the adoption of TAED but also aligns with the increasing demand for eco-labeled products, which are becoming a significant factor in purchasing decisions.

Energy-saving mandates for commercial washers

The U.S. Department of Energy’s 2025–2028 efficiency standards target 0.67 quads energy savings across the installed base of commercial washers, incentivizing detergent reformulations that clean effectively at lower temperatures and shorter cycles. These mandates aim to reduce energy consumption in commercial laundry operations, which are traditionally energy-intensive. By encouraging the development of detergents that perform well under these constraints, the standards drive innovation in the detergent market. TAED, with its ability to activate at lower temperatures, aligns perfectly with these requirements, making it a preferred choice for manufacturers looking to comply with energy-saving regulations while maintaining cleaning efficacy.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competitive threat from liquid bleach activators | -0.7% | Global, with stronger impact in North America | Medium term (2-4 years) |

| Decline in powder detergents share in mature markets | -0.5% | North America & Europe | Short term (≤ 2 years) |

| Thermal instability issues in high-humidity tropical storage | -0.3% | Tropical regions in APAC, MEA, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competitive threat from liquid bleach activators

Manganese-based catalysts, such as MnTACN, have demonstrated superior performance compared to TAED in automatic dishwashing applications, particularly at temperatures below 60 °C. This performance advantage is becoming increasingly relevant as energy efficiency standards drive dishwashing cycles to operate at lower temperatures. Additionally, Nonanoyloxybenzene sulfonate (NOBS) has established a strong foothold in the U.S. laundry capsule market. Its dominance is prompting formulators to explore switching to NOBS, especially in scenarios where dosage flexibility or compatibility with liquid formulations is a critical requirement. These shifts are gradually eroding TAED's market share in these segments.

Decline of powder detergents in mature markets

The retail landscape in mature markets is undergoing a significant transformation, with shelf space increasingly being allocated to liquid detergents and single-dose formats, such as capsules. This trend poses significant challenges for TAED, particularly in terms of encapsulation and maintaining shelf-life stability. In 2024, detergent capsules surpassed powder detergents in grocery sales within the U.K., marking a pivotal moment in the ongoing decline of powder detergents. This shift underscores the growing consumer preference for convenience and ease of use, which single-dose formats offer over traditional powders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Granular dominance faces encapsulation innovation

Granular grades retained 70.65% TAED market share in 2025, underpinning the largest portion of the TAED market size because conventional powder detergents rely on this free-flowing form. Their established production economics and compatibility with spray-dry towers make them the default choice for mass-market brands. Yet the segment’s mid-single-digit growth lags because powder volumes plateau in mature regions.

Encapsulated or co-granulated TAED, advancing at a 3.52% CAGR, addresses heat-humidity sensitivity and allows incorporation into liquid pods or compressed tablets. This technology mixes TAED with sodium percarbonate, carbonate buffers, or polymer shells to delay hydrolysis until immersion, safeguarding performance in tropical climates. Patent activity on multi-compartment pouches illustrates how dosage precision and ingredient separation enhance consumer convenience while extending TAED penetration into premium formats.

By Distribution Channel: Direct supply dominates amid distributor growth

Direct contracts between TAED producers and detergent plants controlled 60.90% of 2025 revenue, driven by high-volume powder lines that demand supply assurance and lot-specific technical support. Continuous improvement projects, such as optimizing percarbonate molar ratios, occur most efficiently under direct collaboration.

Distributor sales are rising 3.10% annually as niche formulators and regional contract blenders seek smaller pack sizes and just-in-time deliveries. Full-line chemical distributors leverage diversified warehouses to amortize inventory risk and offer formulation labs for application troubleshooting. This channel is gaining particular traction in Southeast Asia, Latin America, and Eastern Europe where local brands lack scale for direct importation.

By Application: Household laundry leads despite industrial growth

Household detergents commanded 68.55% revenue in 2025 and remain the anchor of the TAED market. Multiple European brands continue to advertise low-temperature whitening at 30 °C, a claim still tied to TAED chemistry. However, volume gains in this channel plateau as demographic trends flatten wash loads per capita in Western markets.

Conversely, the industrial & institutional laundry segment is growing 3.32% annually. Hospitals, hotels, and urban on-premise laundries in China, India, and Southeast Asia adopt mechanical wash extractors calibrated for 40–50 °C cycles, conditions that favor TAED over chlorinated bleaches. Equipment suppliers highlight water recycle loops and energy recovery, reinforcing mid-temperature wash chemistry as a purchasing criterion.

By End-User Industry: Consumer goods manufacturers drive demand

Consumer goods manufacturers consumed 45.40% of global volumes in 2025, reflecting the integrated sourcing strategies of multinational detergent producers that prefer direct, long-term supply contracts. Their central R&D teams also dictate global formulation standards, locking in TAED specifications for legacy powder brands.

Healthcare & hygiene facilities represent the fastest-growing end user at 3.38% CAGR as infection-control protocols tighten after COVID-19. Hospital laundries cite TAED’s broad-spectrum antimicrobial efficacy and fabric safety versus hypochlorite, enabling higher turnover of linens with lower replacement rates. EPA exemption from food-contact tolerance further supports uptake in the food & beverage processing industry where on-site cleaning regimes now mirror pharma hygiene norms.

Geography Analysis

Europe accounted for 39.85% of global demand in 2025 thanks to decades-old phosphate bans that pushed manufacturers to TAED-centred oxygen bleach systems. Germany and the United Kingdom constitute the largest national markets because retailers emphasize eco-labels and cold-wash performance on pack messaging. The renewed EU Detergent Regulation, effective 2025, tightens biodegradability tests and fragrance disclosures, indirectly reinforcing TAED compliance advantage. Consumers continue to pay a premium for sustainable claims, with 72% citing eco profile when selecting detergents.

Asia-Pacific registers the highest regional growth at a 3.41% CAGR to 2031. China gains from vertically integrated TAED supply, while India’s textile finishing sector and its expanding health-care infrastructure lift institutional wash volumes. Local suppliers such as Shanghai Deborn and JINKE ramp capacity to back regional contract detergent plants, shortening lead times and lowering duty costs. Authorities in Japan and South Korea incentivize lower energy use in laundry services, further aligning with TAED adoption.

North America is mature yet stable. The California Cleaning Product Right-to-Know Act compels disclosure of each ingredient at ≥0.01% concentration, leading multinational brands to stick with familiar, well-documented activators like TAED. However, liquid formats dominate retail channels, which constrains powder-based TAED volumes unless encapsulation or capsule technology bridges the gap. In Latin America, Middle East, and Africa, hygiene modernization in healthcare and hospitality sparks greenfield laundry projects, but summer-peak warehouse temperatures necessitate barrier films and desiccant liners, adding landed-cost headwinds.

Competitive Landscape

TAED production is highly concentrated, with the top five companies accounting for roughly 70% of global output. European producers Warwick Chemicals (Lubrizol), WeylChem International, and Henkel leverage long-standing relationships with powder detergent brands and maintain robust technical service teams. Warwick, for example, commercialized a next-generation co-granulated TAED that improves storage stability by 15 °C compared with legacy blends.

Asian entrants such as Shanghai Deborn and JINKE Company compete on cost and proximity to high-growth APAC customers, often offering toll-manufacturing and private-label packs. These suppliers gradually secure REACH registrations to target European imports and broaden their footprint. Technology partnerships with enzyme companies have emerged: in 2024 Novozymes signed a memorandum with an unnamed Chinese TAED producer to co-develop hybrid granules for low-temperature capsules.

Strategic responses include capacity debottlenecking in Germany and the United States, vertical integration into sodium percarbonate production, and patent filings on multi-compartment pouches that isolate TAED until dispense. The market has also witnessed distributor realignment; in 2024 Wego Chemical inked a pan-ASEAN distribution deal bringing technical field staff under its Performance Chemicals unit.

Tetraacetylethylenediamine (TAED) Industry Leaders

AK Chemtech Co., Ltd

Henkel AG and Co. KGaA

JINKE Company Limited

Shanghai Deborn Co. Ltd

WeylChem International GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: The Environmental Protection Agency established an exemption from tolerance requirements for TAED residues on food contact surfaces, facilitating adoption in food processing applications and expanding market opportunities in regulated environments.

- February 2024: Henkel's 2023 Annual Report stated that its Adhesive Technologies segment achieved sales of EUR 10,790 million. Henkel's focus on sustainable, high-performance chemical solutions reinforces its key role in the TAED supply chain for detergent and cleaning applications.

Global Tetraacetylethylenediamine (TAED) Market Report Scope

The Tetraacetylethylenediamine Market report include:

| Granular TAED |

| Tablet/Compressed TAED |

| Encapsulated/Co-granulated TAED |

| Liquid Dispersion TAED |

| Direct (Captive to Detergent Plants) |

| Chemical Distributors |

| Household Laundry Detergents |

| Automatic Dishwashing |

| Industrial and Institutional Laundry |

| Pulp and Paper Bleaching |

| Textile Processing |

| Consumer Goods Manufacturers |

| Contract and On-Premise Laundries |

| Food and Beverage Processing |

| Healthcare and Hygiene |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Granular TAED | |

| Tablet/Compressed TAED | ||

| Encapsulated/Co-granulated TAED | ||

| Liquid Dispersion TAED | ||

| By Distribution Channel | Direct (Captive to Detergent Plants) | |

| Chemical Distributors | ||

| By Application | Household Laundry Detergents | |

| Automatic Dishwashing | ||

| Industrial and Institutional Laundry | ||

| Pulp and Paper Bleaching | ||

| Textile Processing | ||

| By End-user Industry | Consumer Goods Manufacturers | |

| Contract and On-Premise Laundries | ||

| Food and Beverage Processing | ||

| Healthcare and Hygiene | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Tetraacetylethylenediamine (TAED) Market size?

The TAED market size stands at USD 755.05 million in 2026 and is projected to reach USD 867.44 million by 2031, posting a 2.82% CAGR.

Why is TAED preferred in low-temperature laundry detergents?

TAED generates peracetic acid when in contact with peroxide sources, delivering whitening performance at 30–60 °C and supporting energy-saving cold-wash cycles.

Which application segment is growing fastest for TAED?

Industrial & institutional laundry leads growth at a 3.32% CAGR as hospitals and hotels in Asia-Pacific expand professional wash capacity.

What competitive technologies challenge TAED?

Liquid bleach activators such as MnTACN catalysts and NOBS offer higher reactivity below 60 °C in dishwashing and capsule formats, pressuring TAED in certain niches.

Page last updated on: