Pyrrolidone Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

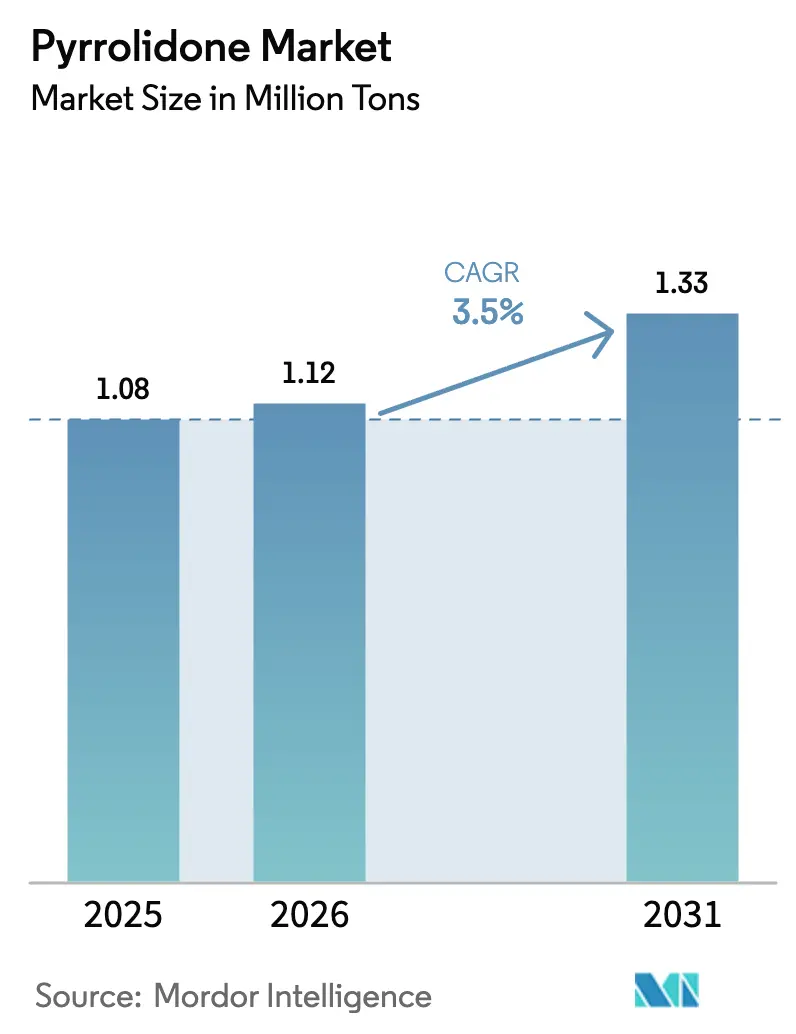

| Market Volume (2026) | 1.12 Million tons |

| Market Volume (2031) | 1.33 Million tons |

| Growth Rate (2026 - 2031) | 3.50% CAGR |

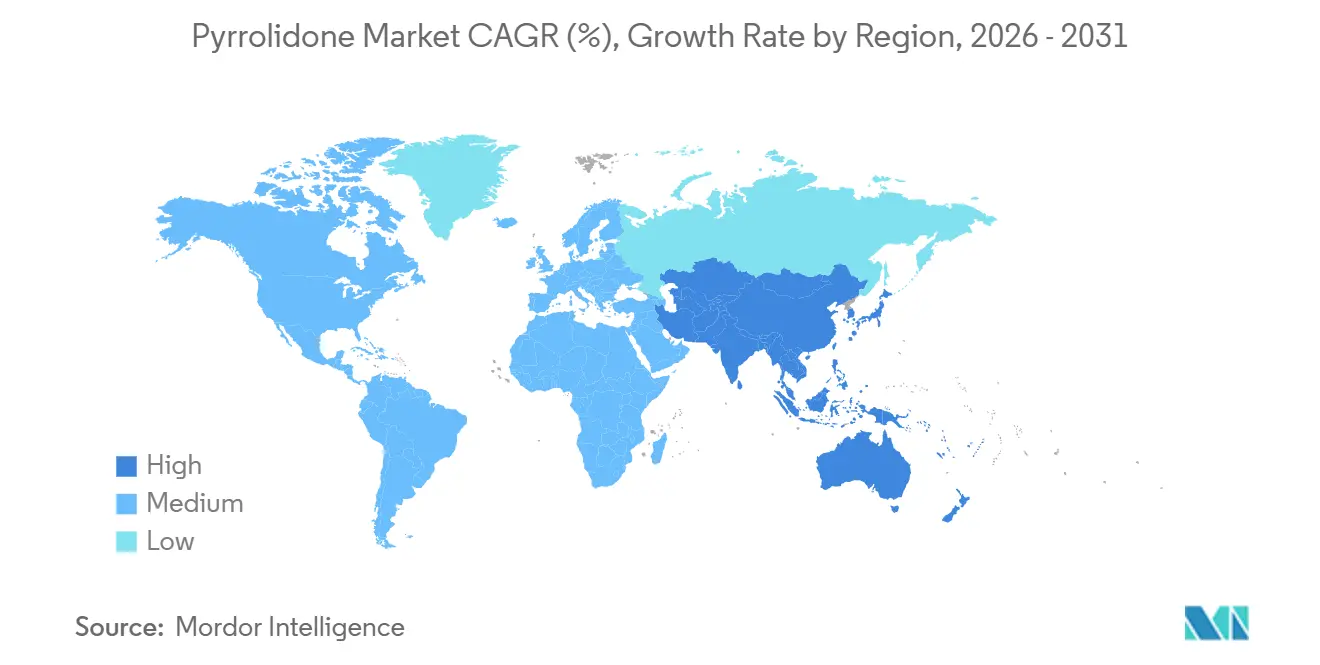

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

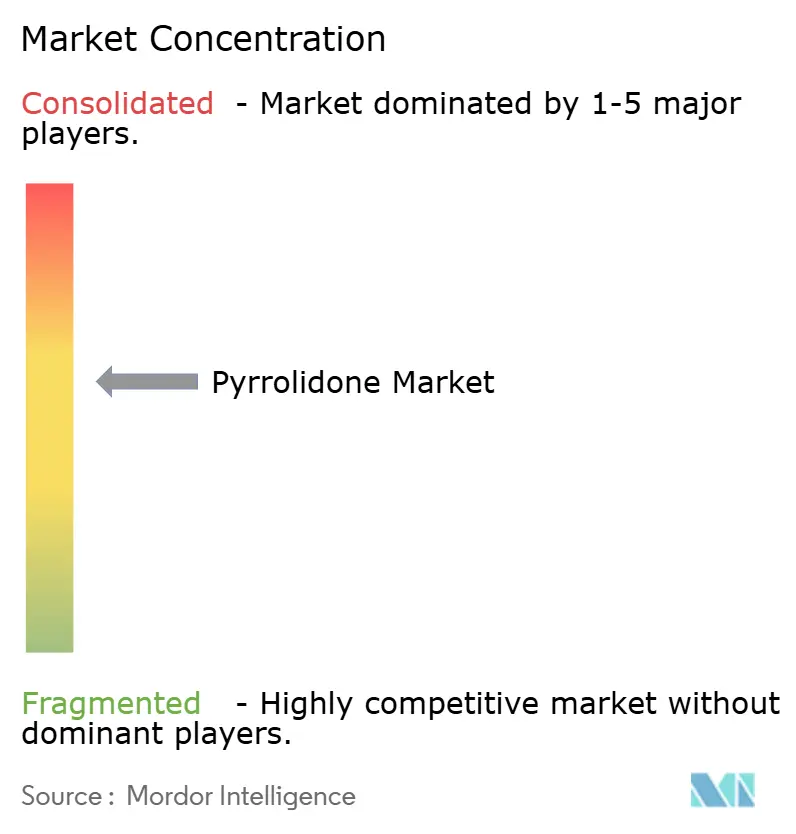

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pyrrolidone Market Analysis by Mordor Intelligence

The Pyrrolidone Market size is projected to be 1.08 million tons in 2025, 1.12 million tons in 2026, and reach 1.33 million tons by 2031, growing at a CAGR of 3.5% from 2026 to 2031. Steady headline growth hides a structural shift toward semiconductor-grade and battery-grade purity, both of which require ultra-low-metal recovery circuits and drive capital-expenditure cycles at most incumbent plants. Producers are also contending with stricter toxicity thresholds in the European Union and the United States, which create a two-speed market: Asian suppliers race to add electronic-grade capacity, while European formulators pivot to bio-based blends that stay below the 0.3% weight-by-weight limit set by REACH Annex XVII. At the same time, lithium-ion battery expansion keeps Asia-Pacific solvent demand rising even as per-cell consumption falls thanks to closed-loop recovery units. Competitive pressure is intensifying because Chinese entrants can undercut delivered cost by double-digit percentages, forcing Western incumbents to differentiate through purity, recovery efficiency, and ESG credentials.

Key Report Takeaways

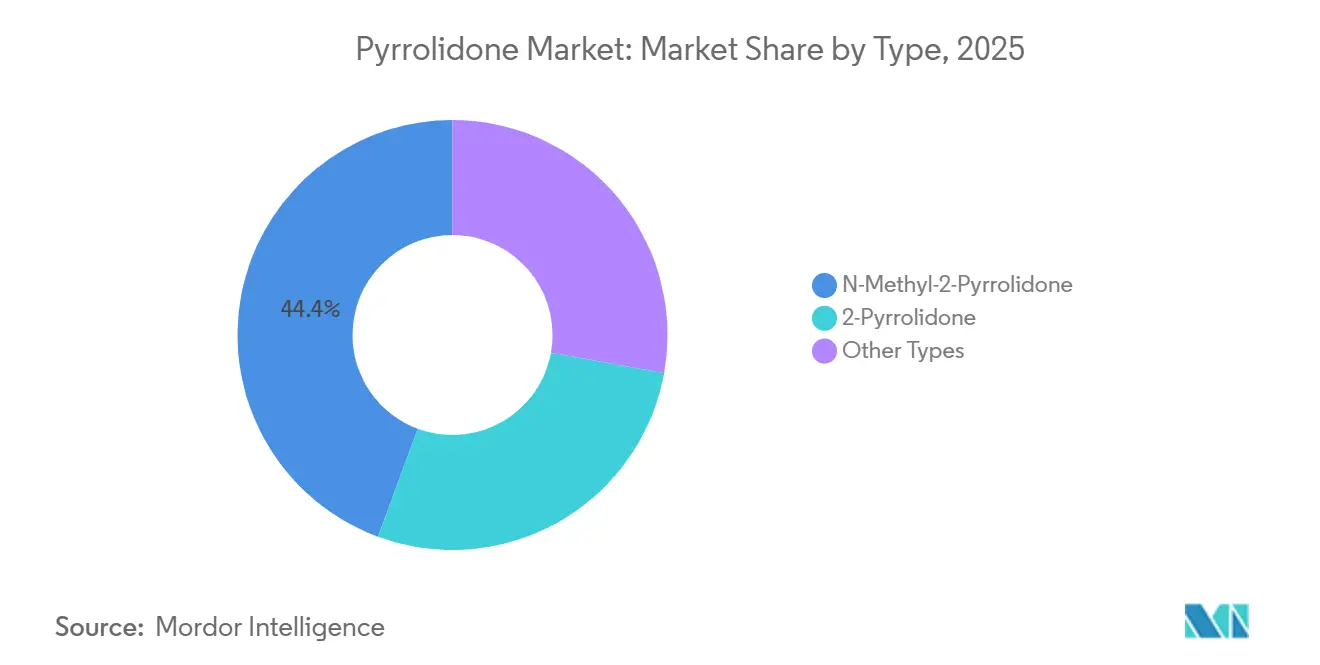

- By type, N-Methyl-2-Pyrrolidone held 44.36% pyrrolidone market share in 2025 while 2-Pyrrolidone posted the fastest growth at a 4.18% CAGR through 2031.

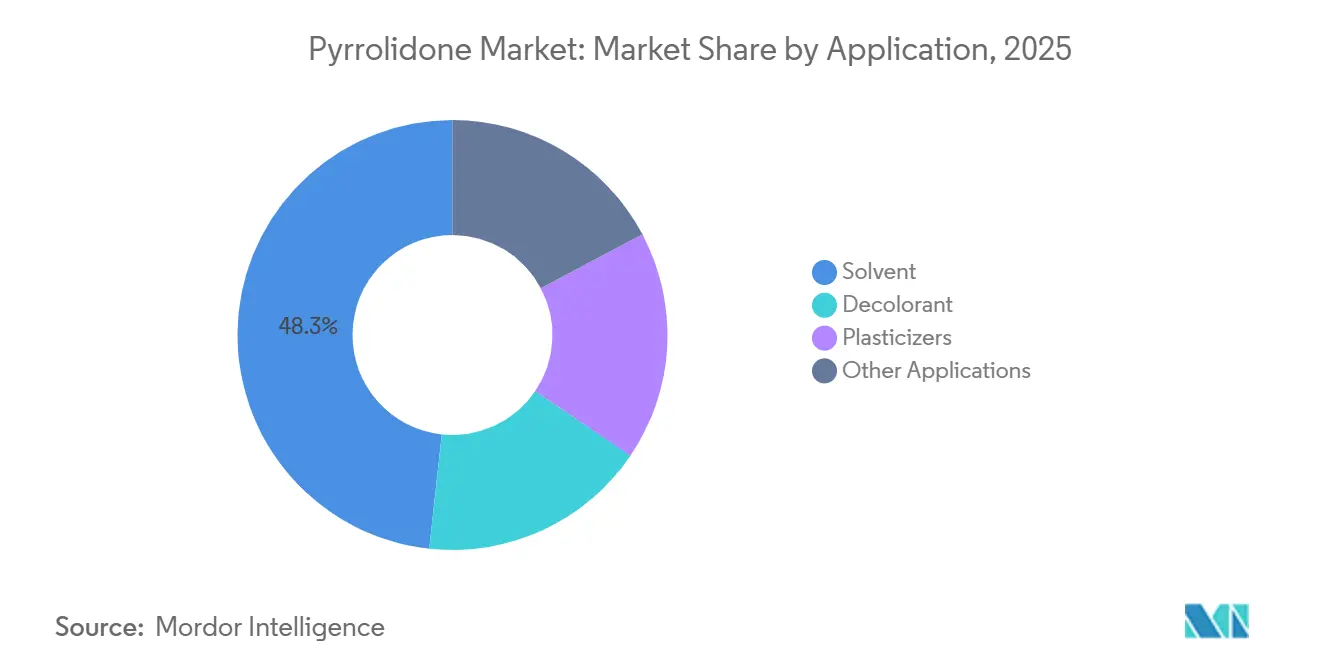

- By application, solvent accounted for 48.27% of the pyrrolidone market size in 2025, yet plasticizers are forecast to expand at 4.24% CAGR through 2031.

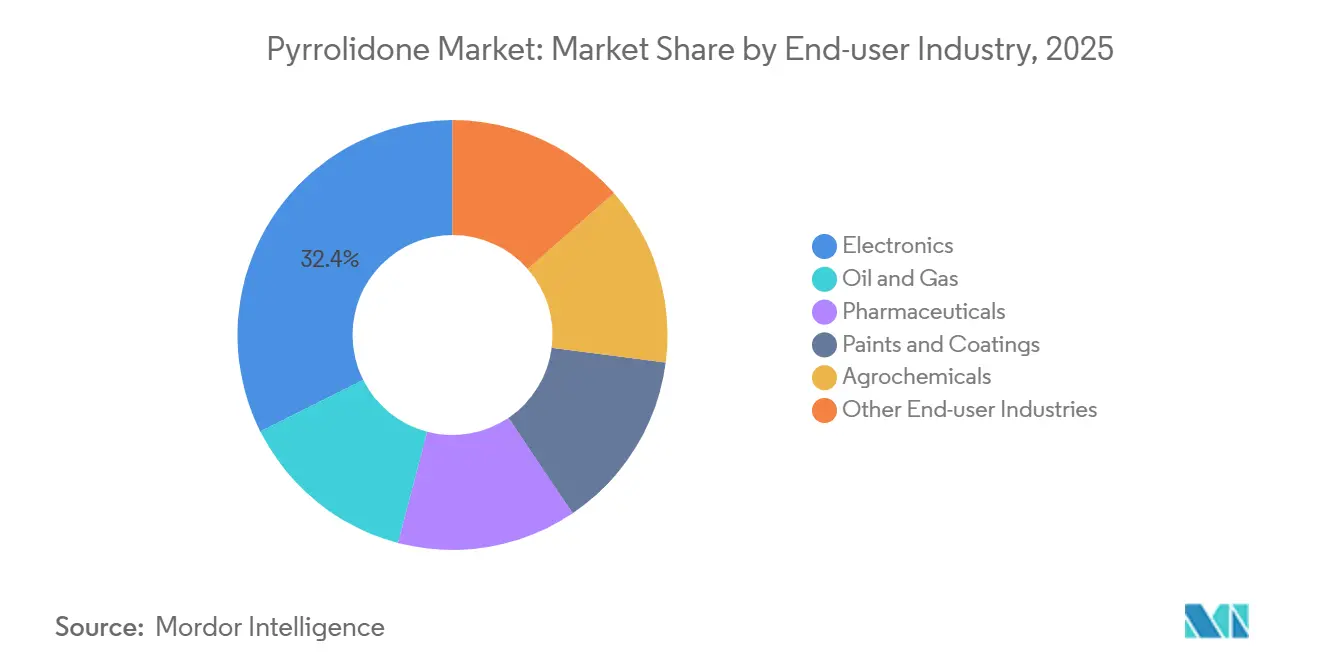

- By end-user industry, electronics led with a 32.41% share of the pyrrolidone market size in 2025 and are advancing at a 4.31% CAGR through 2031.

- By geography, Asia-Pacific controlled 48.89% of volume in 2025 and is projected to expand at 3.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pyrrolidone Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring demand for Li-ion battery cathode manufacturing | +1.4% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Expanding use as high-purity stripping solvent in semiconductor fabs | +0.9% | Asia-Pacific (South Korea, Taiwan, Japan), North America (Arizona, Texas) | Long term (≥ 4 years) |

| Strong uptake in pharmaceutical synthesis of 2-P derivatives | +0.6% | North America, Europe, India | Medium term (2-4 years) |

| Bio-based NMP commercialization gaining regulatory traction | +0.3% | Europe, North America | Long term (≥ 4 years) |

| Premium pricing for ultra-low-metal grades (less than 10 ppb) | +0.4% | Global, concentrated in electronics hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Soaring Demand for Li-Ion Battery Cathode Manufacturing

Lithium-ion battery lines consumed 180,000 tons of NMP in 2025, and gigafactory build-outs continue despite falling per-cell solvent intensity. Chinese, South Korean, and Japanese cell plants are co-locating distillation units that recover 95%–98% of solvent, shrinking consumption per kilowatt-hour from 1.2 kg to 0.05 kg. Stable spot pricing in 2025, despite a 22% rise in cathode output, shows that recovery rather than virgin demand absorbs much of the growth. Capital expenditure for closed-loop systems now sits at roughly USD 8 million–USD 12 million per 50 GWh plant, yet the lower energy cost per kilogram—down from 3.5 kWh to below 2 kWh—improves both margins and ESG scores. These dynamics keep battery producers locked into the pyrrolidone market even as regulatory pressure rises elsewhere.

Expanding Use as High-Purity Stripping Solvent in Semiconductor Fabs

Advanced-node fabs need NMP that meets SEMI C33-0213 Grade 4 purity, capping each metallic element at 100 ppt. Achieving this threshold requires multi-stage distillation, ion-exchange polishing, and inline ICP-MS monitoring, boosting production cost by up to 60% but allowing 15%–20% higher selling prices. Fujifilm’s 2024 EUV photoresist developer shows how material suppliers integrate solvent purification into value-added blends that improve wafer yield. Newly commissioned fabs in Arizona and Texas already specify electronic-grade NMP, signaling that North American demand will align with Asian purity standards within two years. The result is a profitability corridor that rewards suppliers who can guarantee sub-10 ppb impurity levels.

Strong Uptake in Pharmaceutical Synthesis of 2-P Derivatives

The U.S. FDA’s 2024 excipient update categorized pyrrolidones as safe for topical use up to 10% weight-by-weight, clearing a path for wider adoption in transdermal patches[1]U.S. Food and Drug Administration, “Inactive Ingredient Database Update 2024,” fda.gov . Ashland’s Pharmasolve NMP now appears in a dozen FDA filings for nicotine-replacement, hormone-replacement, and analgesic patches, each of which pays a 60%–80% premium over industrial-grade solvent. Pharmaceutical batch sizes are small, so producers can dedicate reactors and purification loops without stranding capacity. The margin uplift keeps the pyrrolidone market attractive to specialty-chemical firms even as commodity demand softens in coatings.

Bio-Based NMP Commercialization Gaining Regulatory Traction

BASF’s biomass-balance NMP, launched in May 2024, uses renewable γ-butyrolactone to cut Scope 3 carbon emissions by up to 35% for European battery manufacturers. Although bio-based feedstock adds a 25%–35% price premium, EU battery regulations and automaker sustainability scorecards favor low-carbon materials. Pilot capacity sits at 15,000 tons per year, but multi-year offtake agreements suggest scale-up to 50,000 tons by 2028. The divergence between cost-sensitive Asian buyers and premium European customers is creating a bifurcated supply chain within the pyrrolidone industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| REACH and US EPA toxicity restrictions on NMP | -0.8% | Europe, North America | Short term (≤ 2 years) |

| Feed-stock γ-butyrolactone price volatility | -0.4% | Global | Medium term (2-4 years) |

| Investor ESG screens on VOC-intensive recovery units | -0.2% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

REACH and US EPA Toxicity Restrictions on NMP

REACH Annex XVII prohibits mixtures with ≥0.3% NMP, and the US EPA’s June 2024 rule proposes similar limits for consumer paint removers[2]European Chemicals Agency, “REACH Annex XVII Entry 71,” echa.europa.eu . Roughly 35,000 tons of annual demand disappeared from European paints between 2020 and 2025 as formulators switched to propylene carbonate and dimethyl sulfoxide. Industrial users remain, but compliance costs—including closed-system handling and revised safety data sheets—favor vertically integrated producers such as BASF and Ashland. Smaller blenders, particularly in Southern Europe, have exited the pyrrolidone market entirely, consolidating supply and modestly increasing margins for surviving incumbents.

Feed-Stock γ-Butyrolactone Price Volatility

GBL spot prices jumped 45% in 2024 after Chinese inspections curtailed 1,4-butanediol output, squeezing NMP margins by 15–20 points. Battery customers often lock in annual contracts, limiting pass-through flexibility, so Western suppliers are backward-integrating into GBL to stabilize costs. BASF’s patent on reactive-distillation NMP production underscores the capital intensity required to weather feedstock swings. Chinese plants near Shandong BDO hubs retain a cost advantage, widening regional price differentials inside the pyrrolidone market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: NMP Anchors Volume, 2-Pyrrolidone Captures Pharma Growth

N-Methyl-2-Pyrrolidone commanded 44.36% of volume in 2025, reflecting its indispensability in battery slurries and photoresist stripping. While NMP keeps dominance, 2-Pyrrolidone is expanding at a 4.18% CAGR as formulators exploit its lower toxicity profile in transdermal patches. Ashland’s Pharmasolve 2-Pyrrolidone gives patch makers a penetration enhancer free of reproductive-hazard labeling, supporting premium pricing. Other variants—N-ethyl-2-pyrrolidone and N-vinyl-2-pyrrolidone—remain niche, mainly for specialty-polymer synthesis.

Purity stratification is now the primary competitive lever. Semiconductor-grade product commands USD 4,500–USD 5,200 per ton versus USD 2,800–USD 3,200 for battery-grade and USD 2,200–USD 2,800 for industrial solvent. Inline ion-chromatography and ICP-MS add USD 0.15–USD 0.25 per kilogram but protect margins. As a result, producers differentiate less on molecule and more on purification depth, a dynamic that reshapes pricing in the pyrrolidone market.

By Application: Solvent Dominance Masks Plasticizers’ Structural Shift

Solvent held 48.27% of volume in 2025, led by electronics and petrochemicals. Asia-Pacific accounts for most of the solvent growth, rising at a 4.1% CAGR as battery and semiconductor capacity builds out. Europe moves in the opposite direction because REACH restrictions remove NMP from consumer paints. Plasticizers are growing at 4.24% CAGR through 2031 as compounders integrate pyrrolidone-containing polyamides into flame-retardant TPU. BASF’s 2024 patent shows that 8%–12% pyrrolidone-PA loading achieves UL 94 V-0 ratings without halogens. Margin dispersion is evident: electronics solvents deliver 18%–22% EBITDA, whereas decolorant sales in petrochemicals hover at 8%–12%, confirming a distinct profitability hierarchy in the pyrrolidone market.

By End-user Industry: Electronics Pulls Ahead on Purity, Pharma Pivots to 2-P

Electronics absorbed 32.41% of volume in 2025 and is advancing at 4.31% CAGR through 2031, the fastest of any segment. Battery demand alone may climb further by 2031 as EV penetration accelerates. Semiconductor fabs added demand in 2025, with each advanced node requiring more stripping solvent per wafer. Pharmaceuticals benefit mainly from 2-Pyrrolidone penetration enhancers that avoid REACH hazard labels. Oil and gas stays stable but niche, while paints and coatings drop in Europe yet grow in Asia. Agrochemicals remain constrained by solvent-substitution pressure. Vertical integration into recovery loops and purification is now commonplace among electronics majors, altering procurement patterns inside the pyrrolidone market.

Geography Analysis

Asia-Pacific controlled 48.89% of volume in 2025 and will grow at 3.92% CAGR through 2031, anchored by MYJ Chemical’s 60,000-ton electronic-grade facility in Henan and South Korean gigafactories run by LG Energy Solution, Samsung SDI, and SK On. China benefits from low-cost γ-butyrolactone in Shandong, undercutting Western suppliers by up to 20% delivered cost. Japan continues as a high-purity stronghold, yet total tonnage is flat because automotive OEMs offshore battery production. India’s agrochemical and coatings sectors add 8,000–10,000 tons of new demand, mostly met by Chinese imports. Regionalization is evident: Chinese plants focus on volume, Korean operations on battery-grade purity, and Japanese units on pharma-grade niche volumes.

In North America, semiconductor investment in Arizona and Texas drives electronic-grade demand, while pharmaceutical adoption of 2-Pyrrolidone underpins specialty growth. The US EPA’s 2024 draft rule removed 12,000–15,000 tons from consumer paint removers, but industrial exemptions keep electronics and pharma users active. Eastman’s Kingsport plant satisfies domestic security needs despite a 10%–12% price premium over imports.

Europe is shrinking due to REACH Annex XVII. Germany still hosts 40,000 tons of BASF capacity, largely exported to Poland and Hungary gigafactories. Bio-based NMP helps European producers protect margins, but paints and coatings have largely switched to safer solvents. South America and the Middle East and Africa shares are fueled by Brazilian agrochemicals and Saudi refinery projects, yet they remain net importers, reinforcing Asia’s dominance in the pyrrolidone market.

Regulatory Landscape

Pyrrolidone regulation is tightening around worker exposure and product concentration limits, with the most direct impact on N-methyl-2-pyrrolidone (NMP) in Europe and the United States. In the European Union, REACH Annex XVII (Entry 71) caps NMP in mixtures at 0.3% w/w for many uses and is complemented by occupational exposure controls that have already accelerated reformulation in coatings; ECHA also published updated guidance for aprotic solvents in March 2026 covering NMP and related solvents (DMF, DMAC, NEP). In the United States, the EPA published a proposed TSCA risk management rule in June 2024 targeting restrictions across manufacture, processing, distribution, and use of NMP, including stricter workplace controls that elevate compliance costs for downstream formulators and toll processors.

Beyond NMP, classification activity adds additional constraints for pyrrolidone derivatives used in specialty applications. ECHA's Risk Assessment Committee issued a final opinion in December 2024 supporting a harmonized classification proposal for 2-pyrrolidone (CAS 616-45-5) as Repr. 1B (H360D), which can cascade into tighter handling requirements, labeling, and customer qualification in pharma and electronics supply chains. Staggered EU compliance timelines for certain aprotic solvents (notably DMAC and NEP) extend through December 2026, reinforcing a compliance-driven shift toward closed systems, solvent recovery, and documentation discipline among European importers and distributors.

Value Chain Analysis

The pyrrolidone value chain starts with petrochemical feedstocks, led by gamma-butyrolactone (GBL), followed by synthesis into NMP, 2-pyrrolidone, and niche derivatives, then purification and blending into application-specific grades. Electronics and battery supply chains increasingly pull higher-purity material (including semiconductor-grade specifications such as SEMI C33-0213 Grade 4 purity requirements cited by fabs) and require multi-stage distillation, polishing, and inline analytics (e.g., ICP-MS), shifting value capture from commodity production to purification, QA, and documentation. Distribution splits between bulk industrial channels (solvents, decolorants) and specialty channels serving electronics and pharmaceuticals, where qualification, traceability, and impurity guarantees drive recurring business.

Compliance and recovery infrastructure now sit inside the chain as core process steps rather than add-ons. REACH Annex XVII restrictions in the EU and the US EPA's proposed TSCA risk management rule (June 2024) increase the need for closed handling, worker exposure controls, and solvent recovery, pushing downstream users (battery cathode plants and some semiconductor lines) to install high-recovery units and favor suppliers that can provide compliant SDS packages and support audits. In parallel, feedstock volatility and regional cost advantages encourage backward integration into GBL and siting near upstream BDO/GBL hubs, while downstream battery and semiconductor customers move procurement closer to producers for security of supply and consistent purity.

Competitive Landscape

The pyrrolidone market shows moderate concentration: BASF, LyondellBasell, Ashland, Shandong Zhishang Chemical, and Mitsubishi Chemical jointly control 63% of capacity. Chinese makers such as Puyang Guangming, Zhejiang Realsun, and MYJ Chemical are gaining volume by selling electronic-grade NMP 15%–20% below Western prices. BASF’s October 2025 Nanjing expansion added a 98% recovery loop, cutting operating cost from USD 1.80 to USD 1.15 per kilogram and trimming energy use to below 2 kWh, a key ESG metric. Ashland’s Micropure and Pharmasolve portfolios target electronic and pharmaceutical niches, fetching 50%–70% price premiums through guaranteed low amine content. Mitsubishi Chemical markets carbon-neutral roadmaps that aim for bio-based NMP by 2028. Indian contract manufacturers like Chemex Organochem are looking to fill gaps in pharma-grade 2-Pyrrolidone by leveraging low labor costs. Technology remains the decisive lever: inline ICP-MS monitoring lets suppliers hit sub-10 ppb purity, thereby commanding premiums that offset feedstock and compliance costs.

Pyrrolidone Industry Leaders

Ashland

Mitsubishi Chemical Group Corporation

LyondellBasell Industries Holdings B.V.

SHANDONG ZHISHANG CHEMICAL CO.LTD.

BASF

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are concentrating in differentiated grades and lower-footprint offerings as regulatory limits squeeze traditional solvent uses. BASF introduced reduced product carbon footprint (rPCF) variants including NMP at its Ludwigshafen Verbund site in March 2026, giving battery and electronics customers a drop-in pathway to meet procurement scorecards without changing process chemistry. Bio-based pathways broaden the addressable customer set in Europe, where REACH-driven reformulation pressures are strongest and where buyers pay for verified footprint reductions; this supports a bifurcated market in which commodity volumes compete on delivered cost while premium segments compete on purity, recovery efficiency, and carbon accounting.

A second white-space area sits at the intersection of regulation and electronic chemicals, where concentration limits and use restrictions reshape product design and supply options. The European Commission opened a public consultation in June 2026 on a proposed REACH Annex XVII amendment that would tighten NMP concentration limits for integrated circuit cleaning solvents, and in July 2026 implemented green tariff arrangements for IC cleaning solvents containing NMP (including a surtax above a stated NMP content threshold). These moves create room for suppliers to expand compliant low-concentration formulations, high-purity alternatives, and recovery-centered service models that help fabs maintain yield while meeting documentation and import requirements. Parallel innovation in bio-based pyrrolidone intermediates is also emerging, highlighted by Toray's technology development to produce bio-based 2-pyrrolidone from biomass (announced in 2026), which can support downstream derivatives where customers are screening for renewable carbon content and reduced hazard labeling.

Recent Industry Developments

- March 2026: BASF introduced reduced product carbon footprint (rPCF) variants of N-methylpyrrolidone (NMP) produced at its Ludwigshafen Verbund site. The move aligns pyrrolidone supply with customer decarbonization scorecards in batteries and electronic chemicals without forcing immediate process redesign. It also raises the bar for competing suppliers on footprint documentation and integrated-site efficiency.

- June 2025: Wanhua and ElevenEs Ltd. signed an MoU to establish a supply and technical partnership for NMP solvents for the new energy industry. The agreement signals tighter producer-to-battery-maker linkages and more emphasis on qualification support and supply assurance rather than spot buying through distributors. It also highlights Europe-focused sourcing strategies for battery materials amid compliance and sustainability requirements.

- June 2024: The US Environmental Protection Agency (EPA) proposed a TSCA risk management rule for NMP that would restrict certain uses and impose stronger workplace controls, including for consumer paint removers. This regulatory push accelerates solvent substitution and increases compliance costs for downstream formulators, changing product mix toward industrial, electronics, and pharma-grade demand where controls and closed systems are more common.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the global demand for pyrrolidone family chemicals sold into industrial and specialty uses, counted at the point where product volumes are supplied to end-use applications across major regions.

Scope exclusions: We exclude internal transfers within integrated plants, lab-scale and R&D-only usage, and downstream finished goods where pyrrolidone is only a minor ingredient and cannot be traced to a clear consumption volume.

Segmentation Overview

- By Type

- N-Methyl-2-Pyrrolidone

- 2-Pyrrolidone

- Other Types

- By Application

- Solvent

- Decolorant

- Plasticizers

- Other Applications

- By End-user Industry

- Electronics

- Oil and Gas

- Pharmaceuticals

- Paints and Coatings

- Agrochemicals

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Egypt

- Nigeria

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand context for pyrrolidone and its linked end uses, then checking supply and trade signals that can be matched back to market volumes. We lean on public sources such as chemical safety and restriction documents from agencies like the US EPA and ECHA, UN Comtrade trade statistics, and peer-reviewed chemistry and process journals that discuss capacity additions and manufacturing routes.

After that, company annual reports, investor presentations, and product technical data sheets are used to confirm typical grades, purity cues, and key application pull, especially for solvent and electronics related demand. We also use paid subscriptions for company financials and intelligence, patent databases, and shipment-level import-export data to cross-check producer footprints and trade flows when public disclosures are thin. The examples listed here are illustrative and not exhaustive, and we referred to additional public and subscription sources for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focuses on validating which pyrrolidone volumes are actually moving into key applications, and how fast substitution, regulation, and pricing changes are shifting usage patterns. We speak with producers, distributors, and large end users across APAC, EMEA, and the Americas so assumptions on grade mix, trade dependency, and demand cycles can be corrected when desk sources do not provide enough detail for specific application categories.

table heading must remain fixed for respondent distribution capture.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 42% |

| Mid tier: 51% | Functional/Unit leaders: 40% | EMEA: 33% |

| Smaller Players: 21% | Managers: 47% | Americas: 25% |

Market-Sizing & Forecasting

Our sizing logic uses the top-down and bottom-up approach, where production, capacity utilization, and trade data are reconstructed into apparent consumption by region, then checked against application-level demand signals. Since public capacity numbers can be uneven by country, results are corroborated with selective bottom-up approximations like sampled producer volume ranges, distributor channel checks, and a few volume-to-demand ratios tied to end-use output.

Key inputs used in the model include announced plant capacity and debottlenecking timelines, import-export trends for relevant chemical categories, the share of pyrrolidone used as a solvent versus other functions, regulatory restriction points that change allowable use in sensitive applications, and regional growth in electronics, pharmaceuticals, and coatings output. Where data gaps exist for smaller producing countries, we fill them with trade-led proxies, then re-check implied consumption against interview feedback so the final totals stay realistic.

For forecasting, we rely on scenario analysis supported by leading indicators such as downstream industrial production, regional chemical output trends, and the expected pace of substitution in regulated uses. Assumptions are kept simple and are updated when primary respondents flag changes in sourcing behavior, inventory cycles, or pricing that could shift short-term volumes.

Data Validation & Update Cycle

Validation is handled through several checks so that single-source errors do not flow into the final market size. We compare the modeled totals with independent signals like trade balances, utilization swings, and regional end-use output trends, then investigate outliers before the numbers are finalized.

A second analyst reviews the model logic, input ranges, and the reasonableness of growth steps by region and application, followed by a final review pass prior to publication. The report is refreshed annually, and interim updates are triggered when material events occur, such as major capacity announcements, regulatory changes, or sharp demand disruptions. Before delivery, we do a fresh check so clients receive the latest updated view.

Mordor Intelligence's Pyrrolidone Market Size Compared Against Other Published Estimates

Published estimates for pyrrolidone often do not line up because the unit of measurement and the counted scope are not consistent across sources, and that quickly changes the headline number. Some studies describe the market in revenue terms, while others build it in physical volume, and the conversion between the two depends on grade mix and regional pricing.

The main gap comes from mixing revenue-based totals with tonnage-based demand, where Mordor Intelligence keeps the market size in million tons and avoids applying an implied average price that can swing widely by grade and by region.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.08 M (2025) | |

| Global Consultancy A | USD 1.95 B (2024) | Reported in revenue terms, which typically relies on an assumed average selling price across grades and regions, and the total can shift materially when the mix moves toward higher purity material. |

| Industry Publisher B | USD 3.42 B (2025) | Uses a revenue model over a longer horizon, and the total may reflect a broader monetized chain where derivatives or formulated end products are counted beyond the core pyrrolidone volume. |

Looking at the three figures together, the spread is explained mostly by unit choice and what is being monetized versus what is being consumed. When outputs are tied back to transparent variables like trade movement, utilization changes, and end-use activity, the results become easier for clients to follow and sanity-check year to year.

Key Questions Answered in the Report

How big is the pyrrolidone market in 2026?

The pyrrolidone market size totals 1.12 million tons in 2026 and is projected to reach 1.33 million tons by 2031.

Which application is growing fastest for pyrrolidone?

Plasticizers are the fastest-growing application, expanding at 4.24% CAGR due to flame-retardant TPU adoption.

Why is electronic-grade NMP priced at a premium?

Electronic-grade NMP must meet sub-10 ppb metallic-impurity limits, requiring costly purification that supports a 60%–80% price premium.

How do REACH rules affect pyrrolidone demand in Europe?

REACH Annex XVII caps NMP content in consumer products, eliminating significant paint and coating demand and shifting focus to bio-based blends below 0.3% weight.

Page last updated on: