Terminal Block Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

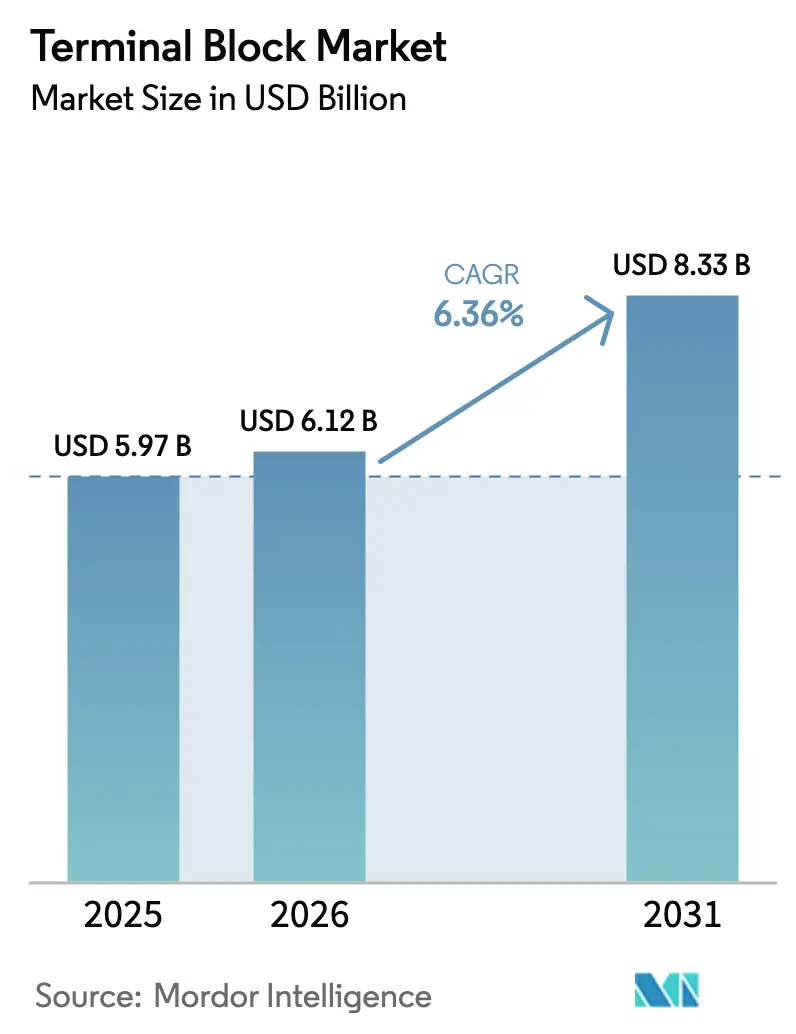

| Market Size (2026) | USD 6.12 Billion |

| Market Size (2031) | USD 8.33 Billion |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Terminal Block Market Analysis by Mordor Intelligence

The terminal block market size was valued at USD 5.97 billion in 2025 and estimated to grow from USD 6.12 billion in 2026 to reach USD 8.33 billion by 2031, at a CAGR of 6.36% during the forecast period (2026-2031). Beyond steady top-line expansion, vendors are pivoting toward intelligent, modular, and cyber-secure connection hardware as factories digitalize, renewable-energy installations proliferate, and electric-vehicle (EV) charging networks scale. Barrier and panel blocks still anchor brownfield control-panel retrofits, yet fuse-integrated and disconnect variants are gaining favor where rising power density and tighter regulatory oversight require embedded circuit protection. DIN-rail solutions dominate footprint-constrained enclosures, while PCB-mounted blocks ride electronics miniaturization. Asia Pacific is the demand epicenter as China, India, and Japan invest heavily in automation, clean energy, and robotics, but North America’s EV charger roll-out and Europe’s offshore-wind build also underpin incremental volumes. Competitive intensity remains high because no supplier controls more than 12% revenue, encouraging product differentiation through push-in mechanics, RFID tagging, and predictive-maintenance sensors.

Key Report Takeaways

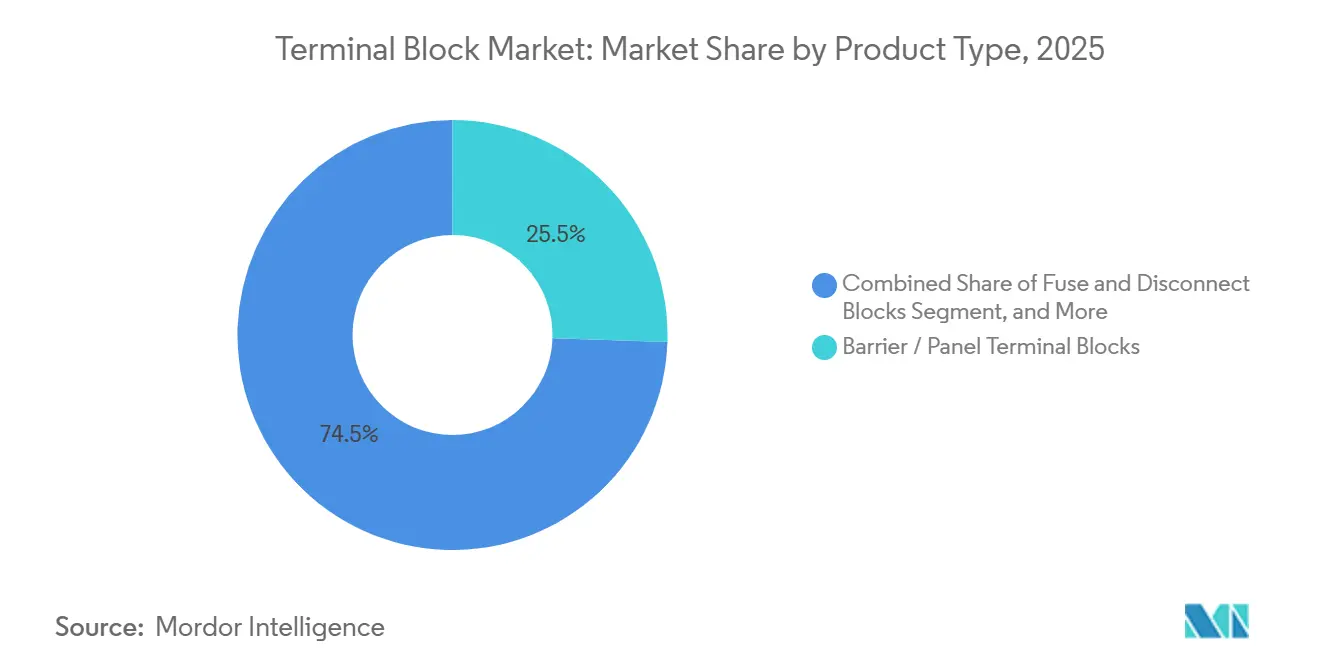

- By product type, barrier and panel blocks led with 25.52% of the terminal block market share in 2025, while fuse and disconnect blocks are projected to expand at a 6.57% CAGR through 2031.

- By mounting method, DIN-rail solutions captured 58.84% of the terminal block market size in 2025, whereas PCB-mounted blocks are forecast to grow at 6.84% CAGR between 2026-2031.

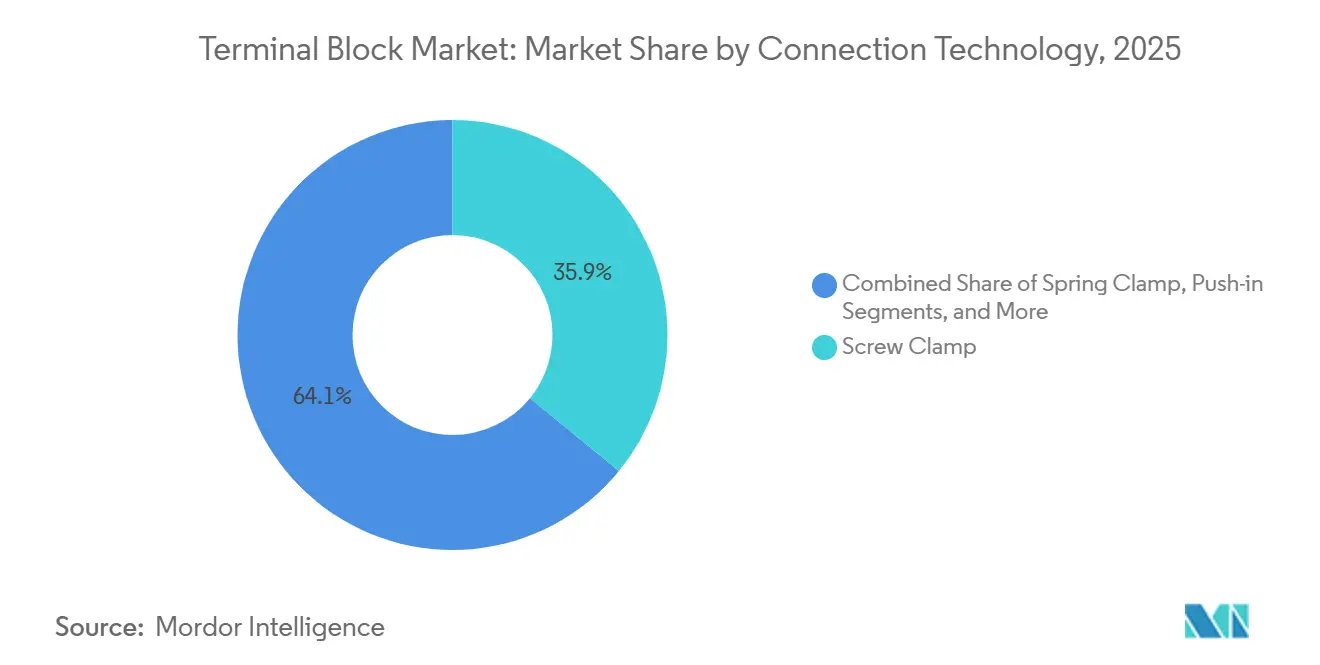

- By connection technology, screw-clamp designs retained 35.91% terminal block market share during 2025 and push-in or pluggable variants are advancing at a 7.08% CAGR to 2031.

- By end-user industry, industrial controls accounted for 33.57% of 2025 revenue, yet transportation is the fastest-growing vertical with a 7.13% CAGR to 2031..

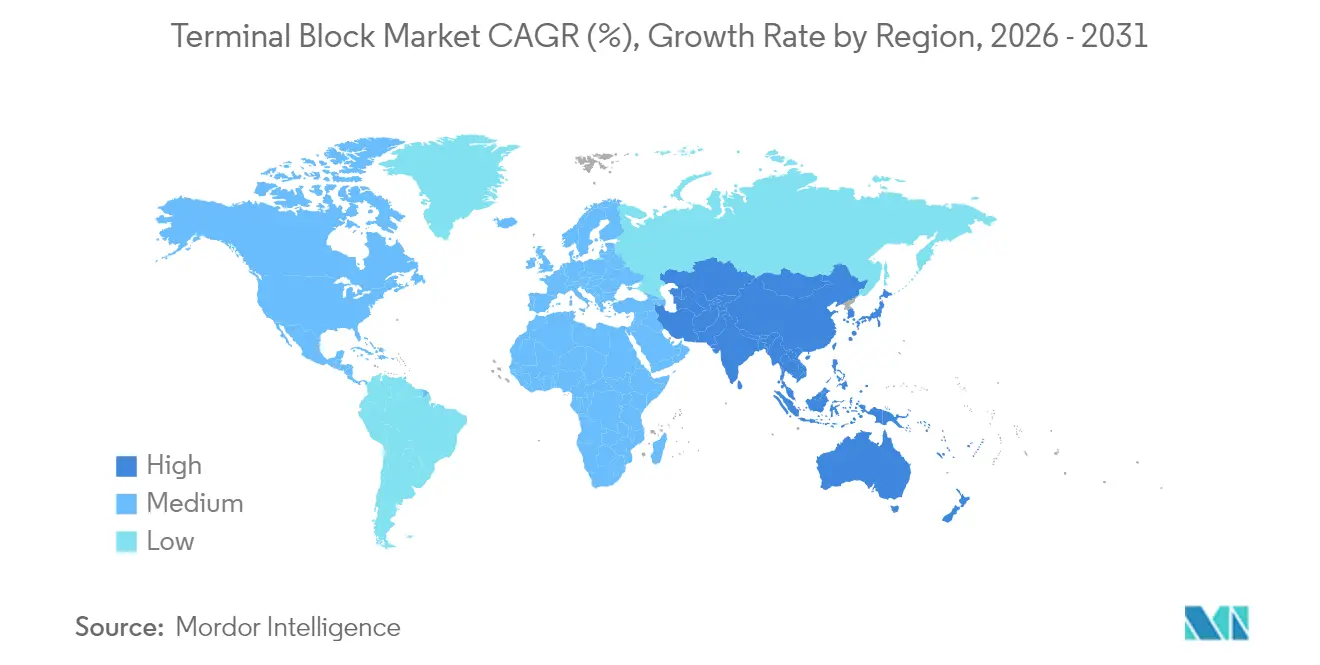

- By geography, Asia Pacific commanded 41.76% of 2025 revenue and is expanding at 7.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Terminal Block Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industry 4.0-driven demand for modular wiring | +1.2% | Global, concentrated in Germany, US, China | Medium term (2-4 years) |

| Renewable-energy build-out needs robust power distribution | +1.5% | Global, peak impact in EU, India, APAC | Long term (≥ 4 years) |

| Building-automation and HVAC retrofits in mature economies | +0.9% | North America, Western Europe | Medium term (2-4 years) |

| Preference for DIN-rail solutions for footprint and serviceability | +0.8% | Global, strongest in industrial automation hubs | Short term (≤ 2 years) |

| Miniaturised IoT devices require sub-3.5 mm PCB blocks | +0.7% | APAC core, spill-over to North America | Medium term (2-4 years) |

| EV fast-charger safety specs push high-amp blocks | +1.1% | North America, EU, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Industry 4.0-Driven Demand for Modular Wiring

Automotive, electronics, and consumer-goods factories increasingly reconfigure production cells every few weeks; push-in blocks with snap-on jumpers reduce panel-assembly labor by 25% and cut documentation errors by 40% when combined with embedded RFID tags. Labeling, color coding, and asset-registration automation help maintenance teams trace circuits in seconds, aligning with IEC 61439 segregation rules. U.S. guidelines for cyber-physical systems endorse modular wiring to isolate compromised zones, positioning smart terminal blocks as a frontline cybersecurity control. Demand is strongest where line changes must occur overnight, notably in German automotive plants and Chinese smartphone assembly lines. Consequently, suppliers that package terminal blocks with digital twins and commissioning scripts are building sticky ecosystems, locking in aftermarket revenue.

Renewable-energy Build-out Needs Robust Power Distribution

Global solar and wind additions hit 507 GW in 2024, yet grid upgrades lagged by 30%, forcing developers toward decentralized inverters that multiply DC and AC termination points.[1]International Energy Agency. “Renewable Energy Market Update – June 2025.” IEA.ORG Phoenix Contact’s 1,500-V DC photovoltaic blocks launched in 2025 address higher-string voltages that compress balance-of-system costs. IEC 60364-7-712 now requires 3,000-hour salt-spray testing and elevated pull-out forces for coastal or desert sites, driving adoption of gold-plated contacts and silicone seals. Offshore wind nacelles must survive 20-year service intervals, so block housings are vented to equalize pressure without ingesting condensation. Emerging hydrogen-electrolyzer farms add hundreds of amperes per cell stack, enlarging the addressable terminal block market and raising the premium on low-resistance, high-temperature materials.

Building-Automation and HVAC Retrofits in Mature Economies

Western commercial real estate owners face net-zero mandates, retrofitting HVAC with variable-frequency drives, CO₂ sensors, and smart dampers- each retrofit adds hundreds of low-voltage terminations. Spring-clamp blocks eliminate torque wrenches and speed field wiring by 35% on Schneider Electric projects. The EU’s requirement to renovate 3% of public buildings annually generates roughly 15 million new termination points per year. EN 60947-7-1 temperature-rise limits align with building codes, ensuring blocks do not become hidden ignition sources. Labor scarcity among electrical contractors amplifies the value of tool-free blocks, tilting specifications toward push-in designs across retrofit cycles.

Preference for DIN-rail Solutions for Footprint and Serviceability

DIN-rail mounting compresses cabinet footprints by up to 30%, critical where brownfield panels lack spare space.[2]International Electrotechnical Commission. “IEC 60364-7-712 Photovoltaic Installations.” IEC.CH WAGO’s TOPJOB S earned UL 508A listing in 2025 with a 10 kA short-circuit rating, reassuring motor-control center integrators. Integrating terminal blocks with Rittal TS 8 enclosures shaved 18 labor hours per cabinet, resulting in significant savings across multi-cabinet builds. Hot-swap capability lets technicians replace a block in ≤ 2 minutes without shutting down adjacent circuits, minimizing process downtime. Predictive-maintenance systems can now flag voltage drops across individual blocks, enabling condition-based replacement and reinforcing the value proposition of modular rails.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper and aluminium price volatility | -0.9% | Global, acute in regions without hedging | Short term (≤ 2 years) |

| Proliferation of low-cost counterfeits | -0.6% | APAC, Middle East, Africa | Medium term (2-4 years) |

| Cyber-security compliance delays "smart" blocks | -0.5% | North America, EU | Medium term (2-4 years) |

| Precision spring-steel shortages constrain capacity | -0.4% | Europe, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Copper and Aluminium Price Volatility

Copper spot prices touched USD 9,800 per t in Jan 2025, an 18% year-on-year jump, squeezing gross margins by up to 300 basis points for vendors without hedges.[3]London Metal Exchange. “Copper and Aluminium Price Data 2025.” LME.COM Aluminium followed a similar trajectory, rising to USD 2,650 per t amid Chinese smelter curtailments. Producers of high-current blocks, which rely on solid copper bus bars, consider substituting tin-plated copper-clad aluminium in non-critical SKUs, yet performance trade-offs threaten UL ratings. Europe’s Carbon Border Adjustment Mechanism adds another 5-8% cost on imported aluminium from 2026. Suppliers with captive metal-forming lines and multi-year procurement contracts gain a structural cost advantage, elevating consolidation risk for smaller competitors.

Proliferation of Low-cost Counterfeits

Underwriters Laboratories warned in 2025 that counterfeit low-voltage components represented 12% of shipments in certain channels, with terminal blocks high on the list. Copycat products often use recycled plastics and under-spec springs that pass visual inspection but fail under fault conditions, exposing OEMs to arc-flash liabilities. Phoenix Contact and Ningbo Degson embed QR-code tags linking to blockchain ledgers to verify provenance, yet field adoption varies. Counterfeits flourish in retrofit markets where price eclipses lifecycle risk, particularly across Southeast Asia and parts of Africa. As IEC and UL cannot effectively police gray imports, genuine manufacturers must shoulder the burden of education and inspection programs, increasing overhead and elongating sales cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fuse and Disconnect Blocks Gain as Power Densities Climb

Fuse and disconnect blocks are set to outpace all other product categories with a 6.57% CAGR through 2031, capturing incremental demand from high-density motor drives and utility-scale battery inverters. In contrast, barrier and panel variants retained 25.52% revenue in 2025 by serving legacy control-panel layouts where visual fuse access and finger-safe shutters remain essential. Eaton’s 6.2 mm DIN-rail block that combines a disconnect switch and 30 A fuse compresses the bill of materials by 40% and frees cabinet real estate for PLC expansions. Rising adoption of 1,500-V DC bus architectures in solar and commercial-vehicle traction systems places thermal stress on terminations; embedded fuse carriers reduce branch-circuit wiring and simplify selective coordination. Regulatory frameworks such as UL 1059 and UL 248 demand coordinated testing, nudging OEMs toward integrated solutions rather than discrete holders plus feed-through blocks.

Sensor and actuator blocks equipped with IO-Link or M12 connectors, while still niche, halve commissioning time by auto-registering device parameters in PLCs- WAGO clocked a 50% reduction in a 2025 electronics-assembly pilot. Grounding and earthing blocks remain indispensable for safety-integrity compliance under NEC Article 250 but grow more slowly because their functionality is mature. Overall, the terminal block market finds a sweet spot where integrating protection, switching, and diagnostics adds tangible panel-builder value without altering enclosure footprints.

By Mounting Method: PCB-Mounted Blocks Ride Electronics Miniaturization

DIN-rail blocks owned 58.84% of 2025 billings thanks to decades-old dominance in motor-control centers and process skids, yet PCB-mounted variants are poised for 6.84% CAGR growth as edge computers, IoT gateways, and LED drivers shrink enclosures below 100 cm³. TE Connectivity’s 2.54 mm pitch board block introduced in 2025 pushes 10 A at 300 V, a current density previously unattainable in surface-mount footprints. Asia Pacific electronics manufacturers embrace these components because they feed through automated pick-and-place lines, slashing hand-solder labor by 90% at an EMS pilot in Shenzhen. Panel- or chassis-mount blocks fill niche roles in marine and aerospace applications, where vibration dictates bolted terminations.

Industrial designers increasingly weigh labor savings from robotic assembly against field-service constraints; board-level blocks lack hot-swap convenience, so designs often blend PCB and DIN solutions. The terminal block market size for PCB variants is projected to grow steadily as automotive zone controller architectures shift power distribution to circuit boards, reinforcing long-term momentum despite DIN-rail incumbency.

By Connection Technology: Push-In and Pluggable Designs Compress Commissioning Time

Screw-clamp blocks still held 35.91% share in 2025 because torque verification satisfies NEC 110.14 and delivers vibration immunity in rail rolling stock. However, push-in and pluggable designs will grow at a 7.08% CAGR as panel shops battle skilled-labor shortages and seek tool-free wiring. Weidmüller’s OMNIMATE 4.0, UL 2459-certified in 2025, trims wiring time by 60% and removes torque-wrench recalibration costs. Spring-clamp technology occupies a functional middle ground yet faces competitive pressure from push-in mechanisms that now equal pull-out force requirements under IEC 60947-7-1.

Pluggable blocks enable pre-wired modules; Phoenix Contact’s COMBICON series withstands 500 mating cycles, minimizing outage during process-plant turnarounds. The terminal block market size in push-in and pluggable categories benefits from universal color coding and accessories such as test sockets, which accelerate troubleshooting. While screw terminals will persist in high-shock niches like mining shovels, new projects increasingly specify tool-less alternatives, signaling a generational shift.

By End-User Industry: Transportation Sector Electrification Drives Fastest Growth

Industrial automation accounted for 33.57% of 2025 demand across PLC racks, VFDs, and robotics controllers, but transportation- including rail electrification and EV fast chargers- will log a 7.13% CAGR through 2031. Rail Baltica alone ordered 12,000 high-voltage termination points for traction substations in 2025. Each 350 kW DC fast charger integrates 40-60 blocks for power and control circuits, and global charger installations topped 180,000 units in 2025, IEA.ORG. Power-and-energy verticals demand wide-creepage blocks for 1,500-V DC solar arrays and 40 kA fault levels in battery-energy-storage racks, sustaining steady growth.

Building-automation upgrades add steady volumes through HVAC retrofits, whereas telecom and datacom applications adopt surge-protected blocks for 5G base stations. Compliance spectra range from EN 50155 shock standards in passenger rail to UL 2202 ground-fault requirements in EV chargers. Net transportation electrification is driving outsized growth in the terminal block market, even though its current revenue base is smaller than that of industrial controls.

Geography Analysis

Asia Pacific generated 41.76% of 2025 revenue and will outpace every other region at 7.41% CAGR. China installed 330,000 industrial robots in 2025, each using 200-400 blocks for drives and safety circuits. India’s 2025 solar auctions under the National Solar Mission mandated 1,500-V DC-rated blocks, creating a multi-year pipeline. Japanese robotics density of 479 units per 10,000 workers drives demand for compact blocks, while South Korean fabs purchased USD 85 million of blocks for cleanrooms and lithography tools. Fast-design Asian vendors are challenging European incumbents on price and custom lead times, reshaping regional share dynamics in the terminal block market

North America accounted for roughly 24% of 2025 turnover. U.S. Inflation Reduction Act funding of USD 7.5 billion for EV chargers underwrote thousands of UL-listed blocks with arc-fault detection. Canada’s push to refine critical minerals triggered orders for explosion-proof Class I, Div 2 blocks. Mexico’s near-shoring boom added 18 manufacturing plants in 2025, each outfitted with multi-cabinet control panels requiring extensive terminal infrastructure. The region values Made-in-USA sourcing and UL certification, offering an anchor for domestic suppliers.

Europe generated around 22% of global revenue. Germany’s offshore wind capacity of 9.2 GW in 2025 embedded 800-1,200 blocks per turbine nacelle. The EU Machinery Regulation that comes into effect in 2027 obliges cybersecurity risk assessments, accelerating adoption of RFID-tagged blocks. The Middle East and Africa, though smaller, experience fast growth in desalination and oil-and-gas automation; Saudi Arabia’s NEOM calls for IP67 blocks handling desert sand and humidity. South America benefits from Brazil’s agribusiness automation and Argentina’s lithium projects, which need UV-resistant, wide-temperature housings.

Competitive Landscape

The terminal block market remains fragmented; the top five suppliers- Phoenix Contact, WAGO, Weidmüller, TE Connectivity, and Siemens- held only 38% combined share in 2025. Competitive levers include product breadth, delivery lead time, and total installed cost. European incumbents emphasize push-in innovation: Phoenix Contact’s XTV series and WAGO’s TOPJOB S cut wiring time by up to 60% for panel shops. Weidmüller and TE Connectivity bundle Ethernet interfaces and IO-Link masters with blocks, catering to machine builders seeking single-vendor wiring platforms. Siemens differentiates with RFID-tagged blocks that auto-populate digital twin asset registers, easing compliance with IEC 62443.

Regional specialists such as Dinkle and Ningbo Degson undercut pricing by 30-35% and offer four-week custom configurations, appealing to Asian OEMs with compressed design cycles. Strategic moves in 2025 included Schneider Electric’s acquisition of a German spring-steel supplier, shielding it from raw-material volatility. ABB patented blocks with built-in Hall-effect sensors, aiming to sell predictive-maintenance subscriptions rather than one-time hardware.

Start-ups like SwitchLab introduced Bluetooth-enabled fuse cartridges for solar-storage cabinets, illustrating how sensor integration is the next battleground. Given the sub-40% concentration, further M&A is plausible as vendors chase economies of scale and vertical integration into surge protection or cybersecurity firmware.

Terminal Block Industry Leaders

Phoenix Contact GmbH & Co. KG

WAGO Kontakttechnik GmbH & Co. KG

TE Connectivity Ltd.

ABB Ltd.

Weidmüller Interface GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Siemens completed beta trials of its 8WH9 RFID-enabled terminal blocks at three U.S. water-treatment plants, demonstrating encrypted asset tracking for critical infrastructure.

- December 2025: Phoenix Contact opened a 45,000 m² plant in Bangalore with annual capacity for 12 million blocks, integrating laser marking to deter counterfeits.

- November 2025: WAGO launched 2857 push-in blocks with Category III surge protection, certified under IEC 61643-11 for building-automation cabinets.

- October 2025: TE Connectivity pledged USD 120 million to expand PCB block capacity in Shenzhen, adding automated pick-and-place lines for automotive electronics.

- September 2025: Schneider Electric acquired Federspiel GmbH, securing spring-steel supply and reducing material-cost volatility by 15%.

Global Terminal Block Market Report Scope

The Terminal Block Market refers to the industry focused on the production, distribution, and use of terminal blocks, modular, insulated devices used to secure and connect multiple wires. These components are essential across industries, including industrial controls and automation, power and energy, building and construction, and transportation.

The Terminal Block Market Report is Segmented by Product Type (Feed-through Terminal Blocks, Barrier and Panel Terminal Blocks, Grounding and Earthing Blocks, Fuse and Disconnect Blocks, Sensor and Actuator and Other Types, and Other Product Types), Mounting Method (DIN-Rail Mounted, PCB-Mounted, Panel and Chassis Mounted, and Other Mounting Methods), Connection Technology (Screw Clamp, Spring Clamp, Push-in and Pluggable, and Other Connection Technologies), End-user Industry (Industrial Controls and Automation, Power and Energy, Building and Construction, Transportation, Telecom and Data-com, and Other End-user Industries), and Geography (North America, South America, Europe, APAC, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Feed-through Terminal Blocks |

| Barrier / Panel Terminal Blocks |

| Grounding / Earthing Blocks |

| Fuse and Disconnect Blocks |

| Sensor / Actuator and Other Types |

| Other Product Types |

| DIN-Rail Mounted |

| PCB-Mounted |

| Panel / Chassis Mounted |

| Other Mounting Methods |

| Screw Clamp |

| Spring Clamp |

| Push-in / Pluggable |

| Other Connection Technologies |

| Industrial Controls and Automation |

| Power and Energy |

| Building and Construction (HVAC / BMS) |

| Transportation (Rail, EV Charging) |

| Telecom and Data-com |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Feed-through Terminal Blocks | |

| Barrier / Panel Terminal Blocks | ||

| Grounding / Earthing Blocks | ||

| Fuse and Disconnect Blocks | ||

| Sensor / Actuator and Other Types | ||

| Other Product Types | ||

| By Mounting Method | DIN-Rail Mounted | |

| PCB-Mounted | ||

| Panel / Chassis Mounted | ||

| Other Mounting Methods | ||

| By Connection Technology | Screw Clamp | |

| Spring Clamp | ||

| Push-in / Pluggable | ||

| Other Connection Technologies | ||

| By End-user Industry | Industrial Controls and Automation | |

| Power and Energy | ||

| Building and Construction (HVAC / BMS) | ||

| Transportation (Rail, EV Charging) | ||

| Telecom and Data-com | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will global revenue from terminal blocks be in 2031?

Forecasts indicate the terminal block market size will reach USD 8.33 billion by 2031 on a 6.36% CAGR trajectory between 2026-2031.

Which product category is expanding fastest?

Fuse and disconnect blocks are projected to grow at 6.57% CAGR to 2031 as designers embed circuit protection inside the connection hardware.

Why are push-in blocks gaining share?

Tool-free push-in technology cuts wiring time by up to 60%, essential as panel shops confront labor shortages and stricter deadlines.

What drives Asia Pacific demand?

Massive investments in factory automation, solar and wind projects, and high-density electronics manufacturing push Asia Pacific to 7.41% CAGR through 2031.

How exposed are manufacturers to raw-material swings?

Copper prices rose 18% year-on-year in 2025, trimming margins by 200-300 bps for producers without hedging, making procurement strategy a key competitiveness lever.

Page last updated on: