Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

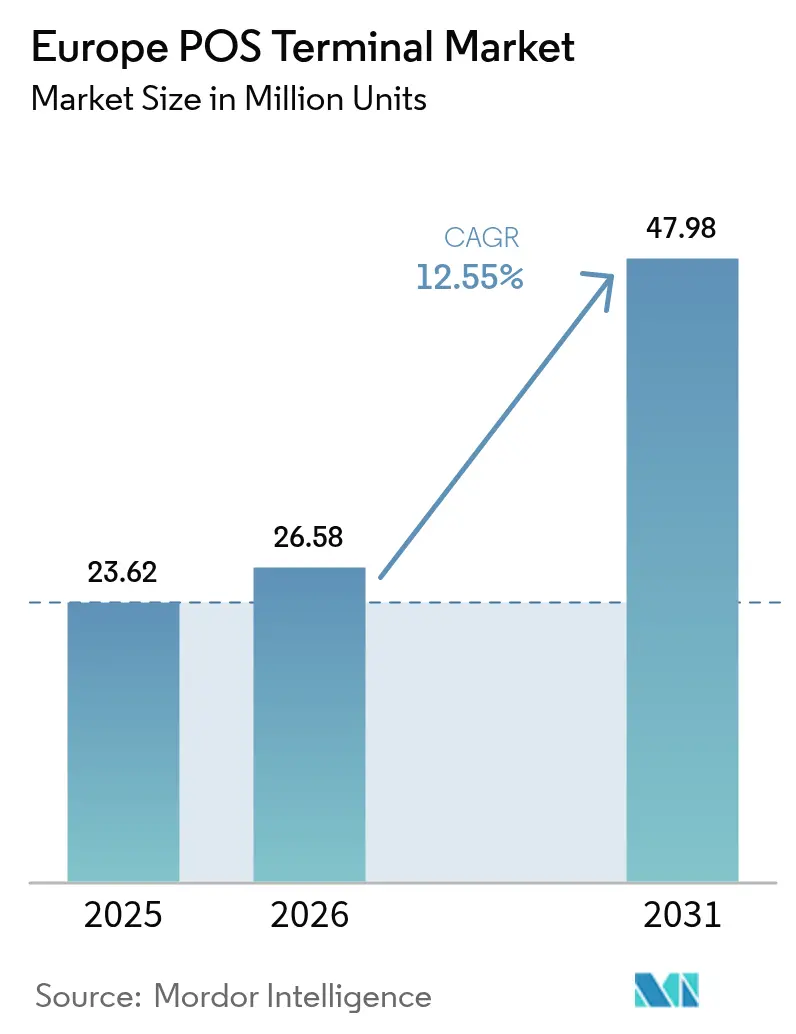

| Base Year Market Size (2025) | 23.62 Million units |

| Market Volume (2026) | 26.58 Million units |

| Market Volume (2031) | 47.98 Million units |

| Growth Rate (2026 - 2031) | 12.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe POS Terminal Market Analysis by Mordor Intelligence

The Europe POS terminal market size was valued at USD 23.62 million units in 2025 and estimated to grow from USD 26.58 million units in 2026 to reach USD 47.98 million units by 2031, at a CAGR of 12.55% during the forecast period (2026-2031). The expansion has been underpinned by accelerated contactless adoption, regulatory mandates that force periodic hardware refresh, and merchants’ search for unified payment infrastructure that lowers total cost of ownership. Strong consumer preference for tap-to-pay, transit system digitization, and subsidy-backed roll-outs in smaller cities have collectively pushed shipment volumes higher in Western and Central Europe. Vendors that combine Android-based terminals, cloud analytics, and subscription billing have captured wallet share as merchants prioritize ROI. Meanwhile, SoftPOS introductions have broadened the addressable base by turning smartphones into certified acceptance points, challenging legacy fixed units but also enlarging overall payment acceptance capacity.

Key Report Takeaways

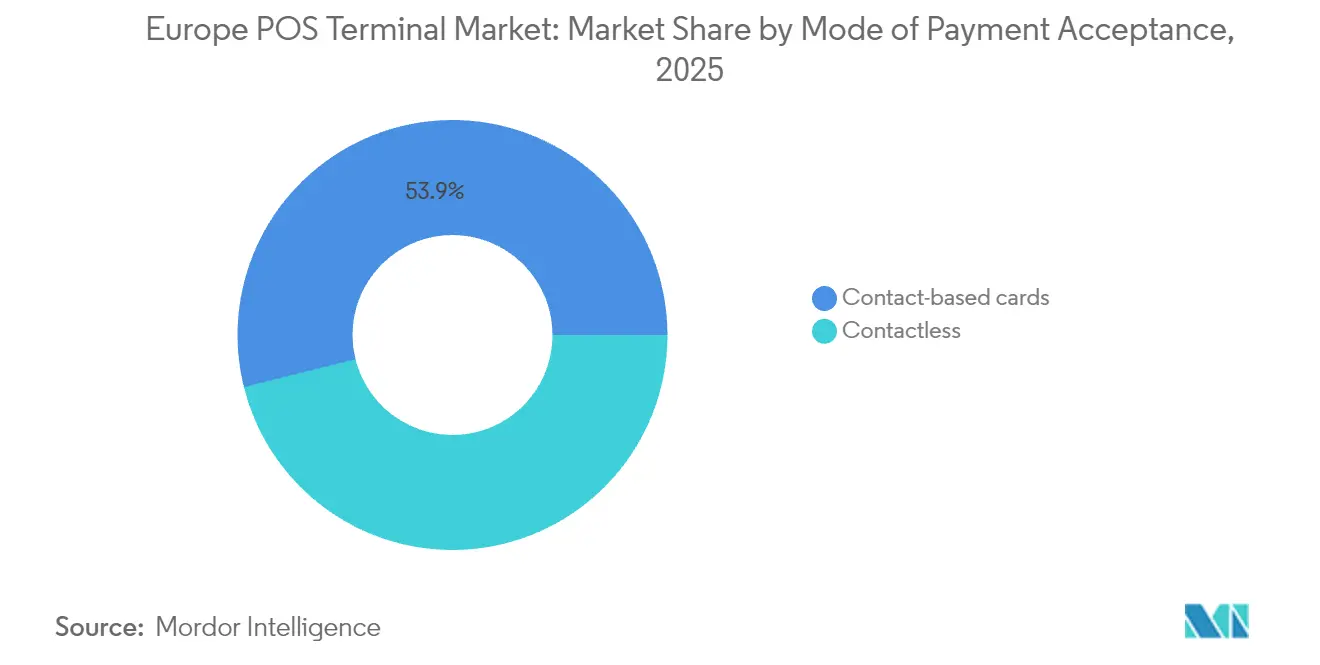

- By mode of payment acceptance, contact-based solutions held 53.90% of Europe POS terminal market share in 2025, while contactless devices are projected to register a 12.65% CAGR through 2031.

- By POS type, fixed systems dominated with 58.20% share of the Europe POS terminal market size in 2025; mobile and portable units are advancing at a 13.05% CAGR to 2031.

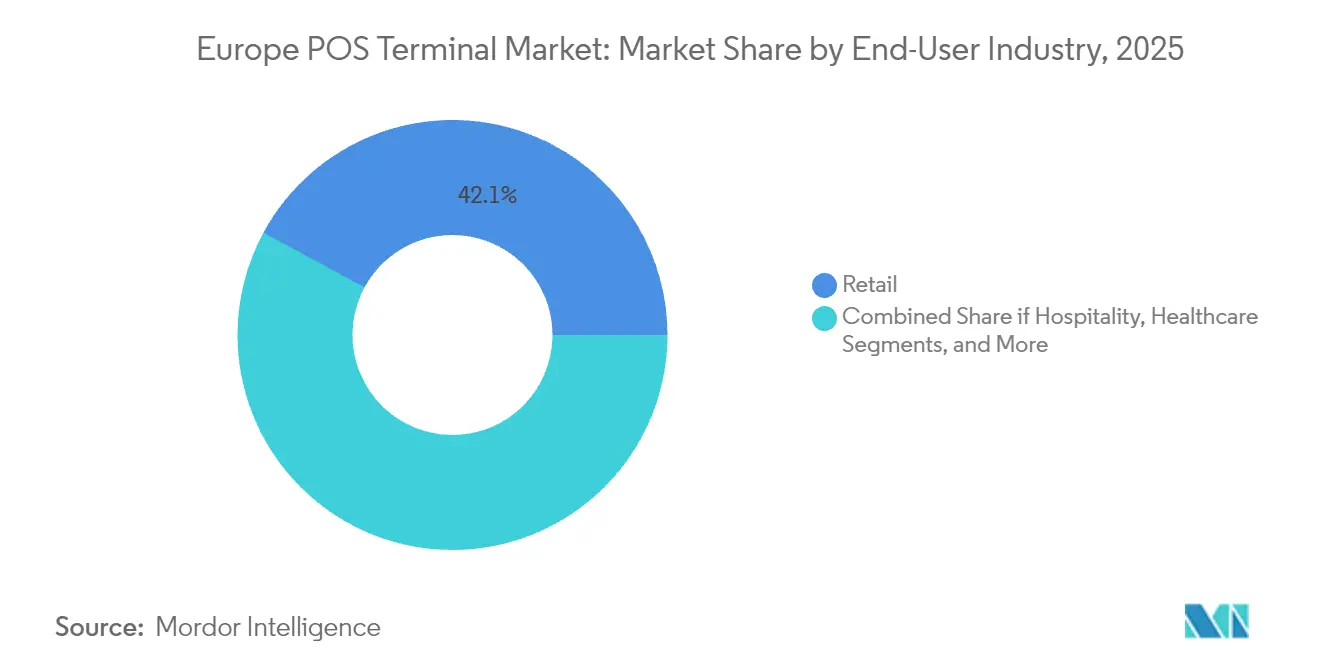

- By end-user, retail led with 42.10% revenue share in 2025; transportation and logistics is forecast to expand at a 13.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe POS Terminal Market Trends and Insights

Drivers Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PIDF subsidies accelerating Tier-3-Tier-6 roll-outs | +2.1% | Western Europe, Central Europe | Medium term (2-4 years) |

| Surging credit-card base (>100 million) lifts card-swipe volumes | +3.2% | EU-wide, UK | Short term (≤ 2 years) |

| Omni-payment Android POS integration | +2.8% | Nordics, DACH | Medium term (2-4 years) |

| GST e-invoice compliance driving real-time POS upgrades | +1.9% | Italy, France | Long term (≥ 4 years) |

| Smart-mall boom in Tier-2/3 cities raises fixed-POS demand | +1.7% | Germany, Spain, Poland | Medium term (2-4 years) |

| Advanced analytics/AI add-ons boosting retailer ROI | +1.3% | EU-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PIDF subsidies accelerating Tier-3-Tier-6 roll-outs

Payment Infrastructure Development Fund programs lowered merchant on-boarding cost and spurred shipments into previously under-served rural districts. Worldline alone enrolled 6,300 micro-merchants on its Tap on Mobile platform during H1 2024, signaling how subsidy alignment quickly converts latent demand into active transaction volumes.[1]Worldline, “Q1 2025 Revenue,” worldline.com The subsidy window created a new recurring revenue stream as newly digitized merchants required value-added services such as analytics and inventory modules.

Surging credit-card base lifts card-swipe volumes

The European card base surpassed 100 million active cards in 2024, feeding higher card-present volumes and reinforcing merchant economics for upgrading POS estates.[2]Shift4, “Shift4 Acquires Majority Stake in Vectron Systems AG,” shift4.com Higher swipe density improved acquirer margins, encouraged loyalty-program integration, and strengthened the business case for contactless limits expansion.

Omni-payment Android POS integration

Ingenico, Verifone, and PAX Global released Android devices that combine EMV cards, QR, and BNPL acceptance in one unit, trimming counter clutter and support costs. Retailers in the Nordics adopted these terminals early, finding that unified interfaces cut average checkout time by 12 seconds per customer. Vendors consequently bundled subscription software, tilting revenue mix toward recurring income.

GST e-invoice compliance driving real-time POS upgrades

Italy’s mandate that fiscal registers and POS report VAT invoices in real time from January 2026 prompted merchants to replace non-compliant hardware. Pilot migrations in Milan and Rome in late 2024 proved that compliant endpoints reduced tax-filing labor by 15 hours per month and increased vendor service calls, benefitting after-sales revenue streams. Vendors with certified fiscal printers gained deterministic demand forecasting over the next four years.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zero-MDR UPI erodes small-merchant economics | -2.4% | EU markets adopting instant payments | Short term (≤ 2 years) |

| QR-code ubiquity dampens new POS demand | -1.8% | Urban EU | Medium term (2-4 years) |

| High total cost of ownership for micro-merchants | -1.1% | Southern and Eastern Europe | Long term (≥ 4 years) |

| Draft PA-Offline rules raise compliance cost | -0.7% | Harmonized EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Zero-MDR UPI erodes small-merchant economics

When regulators capped merchant discount at zero for instant payments, micro-merchants pivoted toward fee-free QR alternatives, slashing hardware rentals. Acquirers saw service fee compression, and POS suppliers lost first-unit sales in the café and kiosk segment.[3]Modern Treasury, “QR Codes for Payments Guide,” moderntreasury.com Larger chains, however, continued to rely on card rails because of richer data capture and chargeback management, tempering the downside.

QR-code ubiquity dampens new POS demand

Public transport and quick-service restaurants rolled out dynamic QR check-out flows that avoid EMV terminals altogether. In Amsterdam, OVpay’s open-loop QR code captured 15.2% of single-ride payments by June 2024, demonstrating consumer willingness to bypass traditional terminals. POS vendors responded by embedding QR modules into displays, but entry-level hardware sales still decelerated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment Acceptance: Contactless Surge Reshapes Infrastructure

Contactless units delivered 12.65% CAGR through 2031 even though contact-based devices held a 53.90% Europe POS terminal market share in 2025. The higher limit for tap-to-pay without PIN in the EEA trimmed checkout friction, and transit systems such as Brussels STIB recorded 57% contactless adoption for single rides in 2024. Europe POS terminal market size expansion within this segment was further propelled by wallet providers like Apple Pay and Google Pay adding loyalty receipt delivery, raising merchant acceptance incentives.

Legacy contact-based terminals remained indispensable for high-ticket transactions and markets with older banking cards. Nonetheless, multi-interface devices such as Verifone’s P400 allowed merchants to replace dual hardware with one converged pinpad, moderating the cannibalization rate. As payment security upgrades migrate toward biometric user verification by 2028, contactless share is projected to edge past the 60% threshold, cementing its role as the principal growth engine of the Europe POS terminal market.

By POS Type: Mobile Solutions Drive Deployment Flexibility

Fixed systems controlled 58.20% of Europe POS terminal market share in 2025, but mobile and portable models are forecast to log a 13.05% CAGR, mirroring the continent’s shift toward service-anywhere commerce. Hospitality chains in Spain piloted PAX A50 Android handhelds linked to cloud back-office suites and reported a 9% sales uplift due to faster table-side ordering. The Europe POS terminal market size in mobile sub-segments is thus scaling disproportionately to transaction volumes as service providers bundle SaaS.

Fixed lanes continued to dominate grocery and fashion anchors thanks to wide peripheral support-scales, scanners, and fiscal printers. Retailers converted investment into predictive analytics by routing SKU-level data to AI engines, enabling shrinkage detection and price-elasticity modeling. Consequently, vendors that fused high-performance fixed units with cloud dashboards insulated their install base from mobile substitution, keeping replacement revenue steady.

By End-User Industry: Transportation Leads Digital Transformation

Retail captured 42.10% of 2025 revenue; still, transportation and logistics is expected to expand at 13.35% CAGR to 2031 as operators digitize fare collection. Netherlands’ nationwide EMV open-loop rollout, OVpay, validated passenger readiness by securing 15.2% share of transit transactions in the first six months of 2024. Europe POS terminal market size in this vertical is forecast to nearly triple by 2031 as metro, rail, and ferry systems converge on account-based ticketing.

Retailers grappled with shrinking margins amid e-commerce competition, driving them to demand integrated loyalty, mixed-basket analytics, and BNPL support from terminals. Logistics hubs adopted ruggedized Android POS for proof-of-delivery and real-time invoicing, compressing accounts-receivable cycles by two days. Healthcare followed, deploying PCI P2PE-certified pinpads that interface with patient record systems to speed insurance co-payment processing.

Geography Analysis

Western Europe led deployment density, anchored by Germany, France, and the Netherlands, where PSD2 rules and mature acquirer networks accelerated hardware refresh. Germany’s tier-2 city smart-mall projects installed fixed lanes with centralized loyalty and energy-management integration in late 2024, boosting demand for enterprise-grade devices. France’s Banque de France incentives for small merchants adopting contactless hardware in 2024 broadened acceptance in rural communes.

Central and Eastern Europe exhibited faster shipment growth from a lower base. Italy’s regulation mandating POS-fiscal register integration from January 2026 ensured a significant uptick in compliant terminals, with pilot programs in Lombardy driving 18% quarter-on-quarter growth in Q2 2025. Poland’s cashless program reimbursed up to PLN 1,000 (USD 250) of terminal cost in 2024, catalyzing micro-merchant uptake.

Nordic markets sustained virtually cashless ecosystems, leading SoftPOS penetration. Sweden trialed biometric fingerprints on Android devices in early 2025, trimming fraud rates by 0.03 percentage points. The United Kingdom, buoyed by fintech innovation, blended SoftPOS and legacy chip-and-PIN, while tourism-heavy Spain and Portugal reinstated 2019 visitor volumes, reviving hospitality terminal installations. Collectively, heterogeneity in regulatory cadence ensures that the Europe POS terminal market remains a multi-speed arena where vendor localization capability dictates share gains.

Competitive Landscape

Competition remained moderately concentrated: the top five vendors accounted for 52% of 2024 shipments. Worldline’s merchant services revenue reached EUR 1,658 million (USD 1,953 Million) in H1 2024, illustrating the scale required to bundle acquiring, hardware, and analytics. Shift4’s acquisition of Vectron Systems AG in 2024 brought 65,000 food-service terminals onto its omnichannel cloud, signaling a trend toward geographic bolt-ons.

Verifone secured USD 235 million in preferred equity in April 2025, channeling funds toward biometric pinpad R&D and SMB vertical SaaS, which is expected to lift its cloud attachment rate from 22% to 35% by 2027. PAX Global diversified revenue by adding PagoBANCOMAT and SIBS certifications, enabling pan-regional hardware supply without bespoke SKUs.

Emerging challengers exploited SoftPOS to bypass traditional certification overhead; yet, stringent PCI MPoC guidelines effective 2025 imposed security compliance that favored incumbents with established audit processes. Hardware makers therefore repositioned as platform orchestrators, bundling device management, remote key injection, and micro-lending to capture lifetime value rather than one-time margin.

Europe POS Terminal Industry Leaders

Ingenico S.A.

Worldline S.A.

Verifone Systems, Inc.

PAX Technology Limited

NCR Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: PAX Global reported 2024 annual results highlighting expanded European certifications, including new PagoBANCOMAT approvals in Italy and SIBS in Portugal.

- April 2025: Verifone raised USD 235 million in preferred equity to finance European SMB product launches with biometric authentication.

- April 2025: Worldline posted Q1 2025 revenue of EUR 1,068 million and disclosed 6,300 new Tap on Mobile merchants.

- February 2025: myPOS acquired UTP (UK) and Toporder (France), enlarging its European merchant base.

Europe POS Terminal Market Report Scope

A POS system is computer hardware and software that manages transactions while selling products or services. It helps to store, capture, share, and report data related to sales transactions. It helps to expedite the checkout process, resulting in customer satisfaction. Inventory management, stock in hand, availability of a product, and pricing information are primary data acquired from the systems.

The European POS terminal market is segmented by type (fixed point-of-sale systems and mobile/portable point-of-sale-systems), end-user vertical (retail, entertainment, healthcare, hospitality, and other end-user industries), and country (Italy, United Kingdom, France, Spain, Germany, Netherlands, Portugal, Poland, Greece, Hungary, Czech Republic, Romania, Ukraine, Slovakia, and Rest of Europe [Croatia and Slovenia]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Mode of Payment Acceptance

| Contact-based |

| Contactless |

By POS Type

| Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems |

By End-User Industry

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-user Industries |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Mode of Payment Acceptance | Contact-based |

| Contactless | |

| By POS Type | Fixed Point-of-Sale Systems |

| Mobile / Portable Point-of-Sale Systems | |

| By End-User Industry | Retail |

| Hospitality | |

| Healthcare | |

| Transportation and Logistics | |

| Other End-user Industries | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large was the Europe POS terminal market in 2026?

It was valued at USD 26.58 million units in 2026.

What CAGR is forecast for Europe POS terminal shipments between 2026 and 2031?

Shipments are projected to grow at a 12.55% CAGR over the period.

Which POS type is recording the fastest growth?

Mobile and portable devices are advancing at a 13.05% CAGR through 2031.

Which end-user vertical shows the strongest upside?

Transportation and logistics is forecast to expand at a 13.35% CAGR, outpacing other sectors.

What regulatory shift will shape Italian demand after 2026?

Mandatory POS-fiscal register integration beginning January 2026 will trigger hardware refresh cycles.

Which vendors lead the competitive field?

Worldline, Ingenico, and Verifone together accounted for 38% of 2024 shipments.

Page last updated on: