Dispatch Console Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2025) | USD 2.16 Billion |

| Market Size (2031) | USD 2.70 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

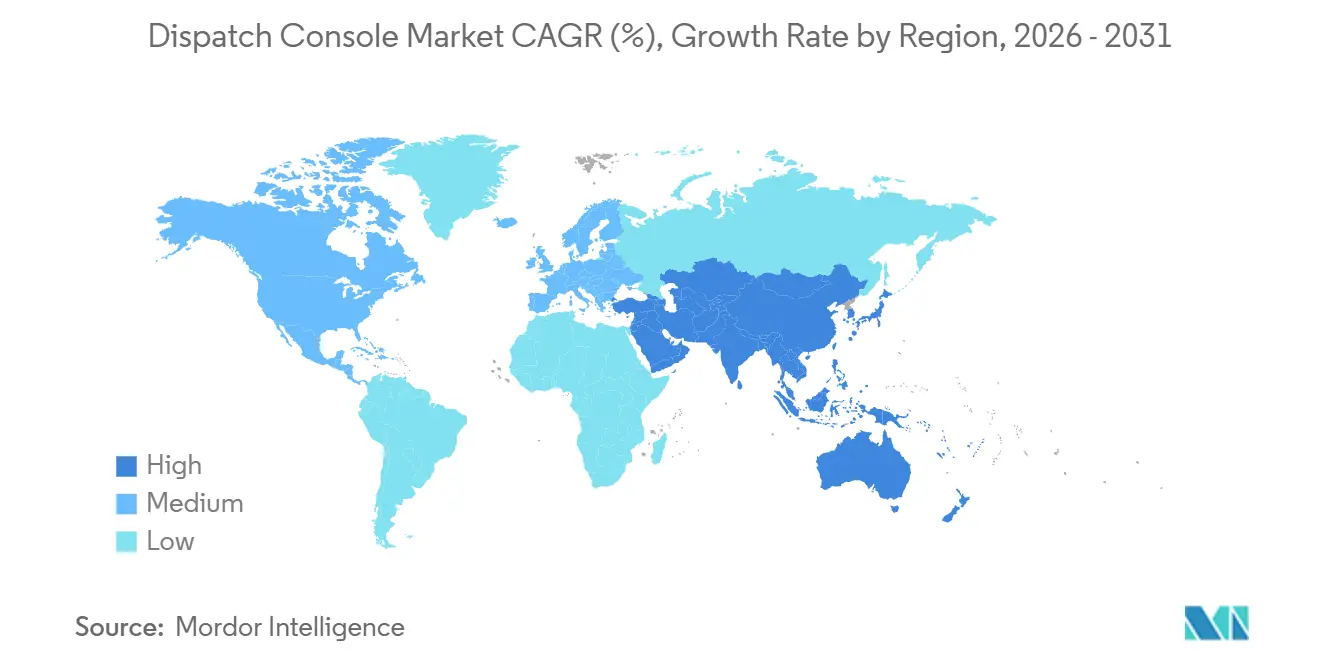

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

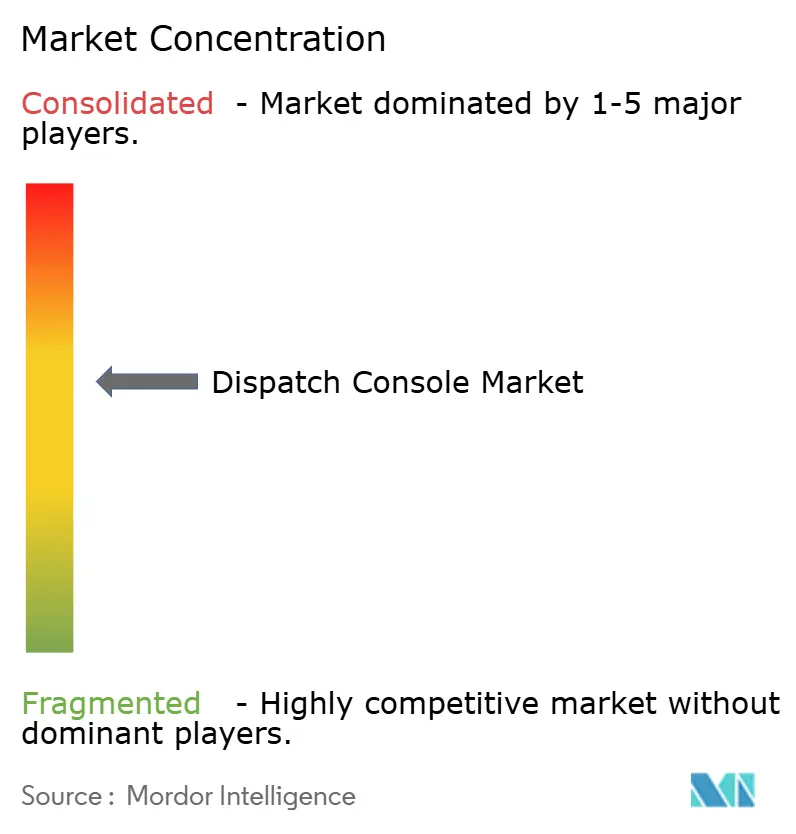

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dispatch Console Market Analysis by Mordor Intelligence

The dispatch console market size is projected to expand from USD 2.07 billion in 2025, USD 2.16 billion in 2026, to USD 2.70 billion by 2031, registering a 4.55% CAGR over 2026-2031. As legacy time-division multiplexing systems age out, public safety, utility, and transportation operators are accelerating the move to Internet Protocol platforms that blend voice, data, and live video. Agencies in North America and Europe are replacing consoles installed during the mid-2000s to comply with Next Generation 911 and European Electronic Communications Code rules, while Asia-Pacific smart-city programs are leapfrogging straight to cloud-native command centers. Vendors are responding with subscription-based software, artificial intelligence modules that triage incidents automatically, and open Application Programming Interfaces that simplify integration with broadband networks. However, stretched procurement cycles, tight municipal budgets, and growing cybersecurity compliance costs limit the short-term speed of replacements, causing a lumpy demand pattern that rewards suppliers able to finance long delivery schedules and guarantee backward compatibility.

Key Report Takeaways

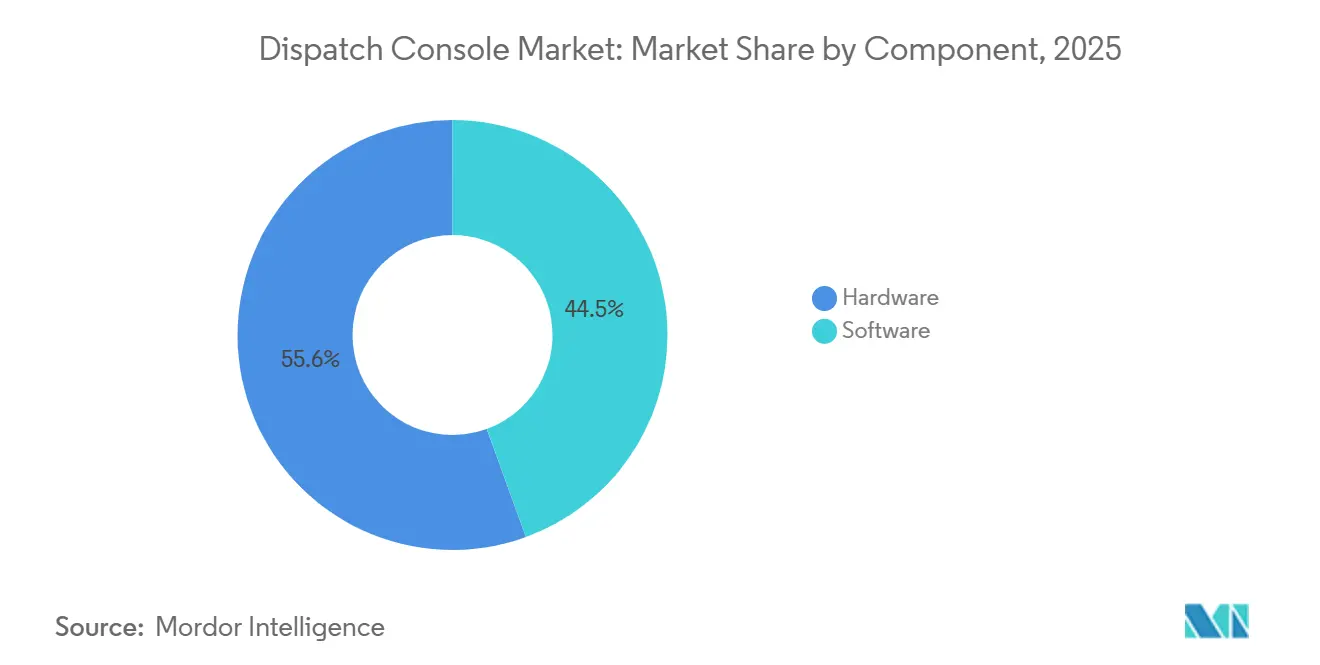

- By component, hardware accounted for 55.55% of revenue in 2025, while software is forecast to grow at a 4.63% CAGR through 2031.

- By type, IP-based platforms led with 67.75% of the dispatch console market share in 2025, whereas circuit-switched systems are expected to register a faster 5.05% growth rate through 2031.

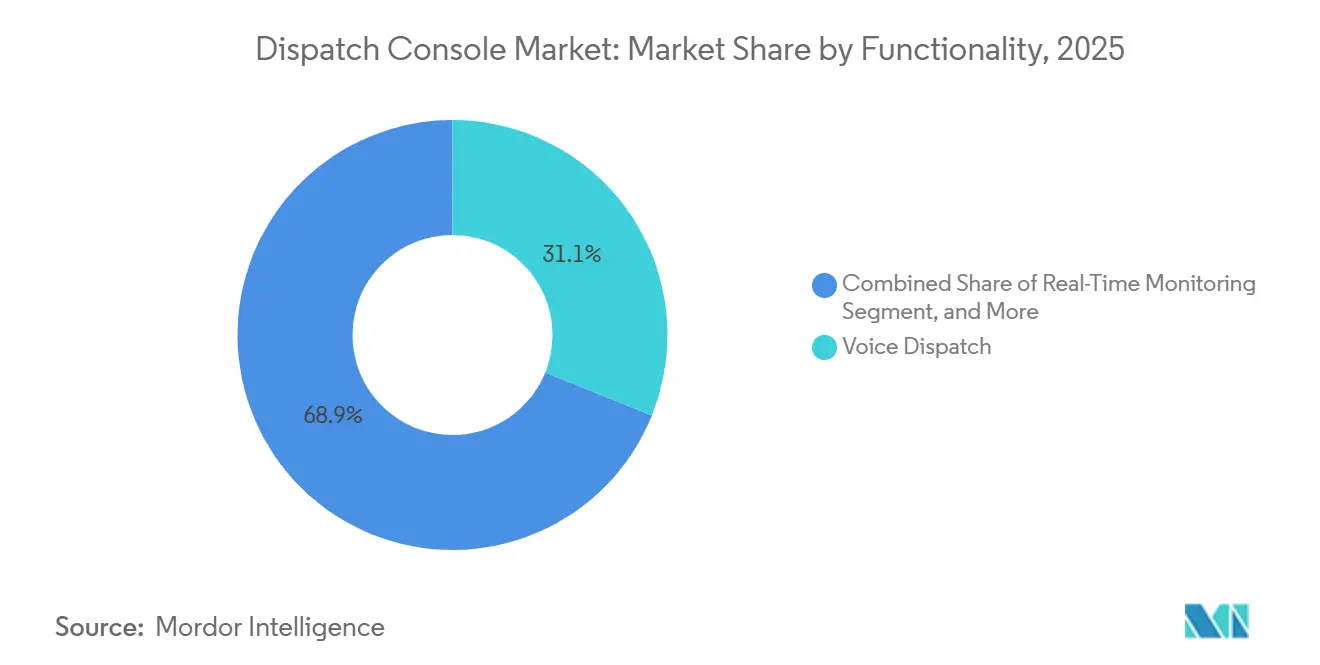

- By functionality, voice dispatch represented 31.10% of the dispatch console market size in 2025, and real-time monitoring is advancing at a 4.64% CAGR to 2031.

- By end-user, transportation and logistics held 33.10% revenue share in 2025, while public safety agencies are projected to expand at a 5.45% CAGR over 2026-2031.

- By geography, North America captured 36.67% revenue share in 2025, and Asia-Pacific is projected to post the fastest 4.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dispatch Console Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NG9‑1‑1 Deployments Speeding Up Console Upgrades | +1.2% | North America, Europe, Asia‑Pacific early adopters | Medium term (2-4 years) |

| Cloud‑Native CAD and Dispatch Adoption in Logistics | +0.9% | Global, especially North America and Europe | Short term (≤ 2 years) |

| Grid Modernization Boosting Demand from Utilities | +0.7% | North America, Europe, parts of Asia‑Pacific | Long term (≥ 4 years) |

| Roll‑Out of Public‑Safety Broadband Networks | +0.8% | North America, Europe, Middle East pilots | Medium term (2-4 years) |

| AI‑Assisted Dispatch Optimizing Response Workflows | +0.6% | North America, Middle East smart‑city initiatives | Short term (≤ 2 years) |

| Private 5G Pilots in Industrial Campuses Enabling IP Dispatch | +0.4% | Industrial zones worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

NG9-1-1 Deployments Speeding Up Console Upgrades

Federal and state mandates require call centers to accept voice, text, image, and video, prompting public safety agencies to scrap consoles incapable of multimedia Session Initiation Protocol feeds. Kansas, Oklahoma, and other early movers brought Emergency Services IP Networks online in 2026, validating that centrally funded programs can meet the 2026 federal target. Cost overruns in California, where spending already exceeds USD 450 million, underscore the budget risk when procurement is fragmented. Alongside hardware refreshes, agencies must modernize recording systems and training curricula, creating a bundled multi-year capital cycle. Vendors that certify equipment quickly and support phased cutovers gain an early-mover advantage.

Cloud-Native CAD and Dispatch Adoption in Logistics

Fleet operators increasingly subscribe to cloud dispatch suites that eliminate on-premises servers and allow supervisors to manage operations from any device. Requests for proposals in Georgia and Wisconsin call explicitly for near-zero downtime, browser-based interfaces, and analytics dashboards. Monthly fees convert capital outlays into operating expenses, shortening internal approval cycles and making solutions attractive to small and mid-sized fleets. Downtime risk shifts from local hardware to wide-area connectivity, so suppliers must bundle redundant telecommunications and rigorous Service Level Agreements to satisfy safety-critical use cases.

Grid Modernization Boosting Demand from Utilities

Transmission and distribution operators are consolidating control rooms as they integrate rooftop solar, battery storage, and electric vehicle chargers that create bidirectional power flows. Projects such as the Tennessee Valley Authority’s USD 300 million System Operations Center and Australia’s AUD 179.2 million (USD 119 million) Transgrid upgrade emphasize real-time situational awareness and automated fault isolation. Historically, utility consoles remained in service for up to two decades, but renewable integration and wildfire risk are trimming lifetimes closer to 12-15 years. Suppliers that can ingest supervisory control and data acquisition messages at millisecond latency and run predictive algorithms on feeder health win follow-on analytics revenue.

Roll-Out of Public-Safety Broadband Networks

Dedicated nationwide 700 MHz services, typified by FirstNet in the United States, enable consoles to pull live body-worn camera streams and biometric telemetry from responders. Certification requires rigorous interoperability and quality-of-service testing, giving incumbents with large engineering teams an advantage. High-capacity backhaul opens doors for artificial intelligence video analytics, but it also widens the threat surface. Dispatch centers now budget for encryption key management, continuous penetration testing, and redundant broadband links.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slow Public Procurement and Budget Hurdles | −0.9% | Global, pronounced in U.S. localities and South America | Medium term (2-4 years) |

| High Cost of Cyber‑Security Upgrades | −0.6% | North America, Europe, Asia‑Pacific compliance‑heavy markets | Short term (≤ 2 years) |

| Vendor Lock‑In Risks in Integrated Suites | −0.4% | Mature markets worldwide | Long term (≥ 4 years) |

| Scarcity of Dispatch‑Ready Spectrum Bands Below 1 GHz | −0.3% | North America, Europe, Asia‑Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Slow Public Procurement and Budget Hurdles

Public safety agencies navigate multi-step approval chains, public hearings, and potential bid protests that can stretch contract awards to 18-36 months. Illinois surcharge revenue funds barely cover half of operational costs, forcing departments to defer console refreshes until state grants materialize.[1]Illinois Association of Public-Safety Communications Officials, “Funding Gap White Paper,” ilapco.org Similar delays in Argentina, where funding for a ARS 23 billion (USD 23 million) 911 upgrade is split across two budget cycles, illustrate how macro-economic swings derail even approved projects. Vendors must provide bridge warranties and flexible payment schedules to remain competitive.

High Cost of Cyber-Security Upgrades

Migrating to Internet Protocol exposes call centers to ransomware, distributed denial-of-service, and insider threats that never existed on isolated circuit-switched networks. Federal guidelines urge segmentation, multi-factor authentication, and 24×7 monitoring, but mid-sized centers report implementation costs of USD 500,000-2 million. Insurance carriers increasingly demand proof of zero-trust architecture before underwriting cyber policies, turning security from optional to mandatory capital expenditure. Budget diverted to firewalls and intrusion detection leaves fewer dollars for new dispatch consoles, slowing refresh cycles and compressing margins on hardware.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Anchors Long Depreciation Cycles, Software Drives Recurring Revenue

Hardware contributed 55.55% of 2025 sales as agencies continued to amortize consoles, radio gateways, and adjustable furniture over 7-10 years. A statewide contract in Oklahoma and county-level approvals in Kansas affirmed that purpose-built ergonomic desks still command a premium over generic office fixtures. Growth in software revenue outpaces hardware at 4.63% annually because cloud subscriptions, mapping extensions, and analytics modules transform one-time licenses into predictable monthly recurring charges. Where servers once required forklifts, new deployments spin up virtual machines in minutes, and updates push automatically after midnight. This shift cuts total cost of ownership yet locks agencies into vendor roadmaps, making exit switches expensive. As artificial intelligence workloads rise, hardware refreshes will require additional graphics processing, higher-resolution monitors, and 10 gigabit network uplinks, fueling incremental hardware sales even in a SaaS world.

The bundling trend continues: more than 60% of 2026 solicitations require a single integrator to supply furniture, radio interface, and software. Bundled deals simplify governance but put price pressure on smaller specialists that cannot finance multi-year warranties. Best-of-breed buyers insist on standards-based APIs and object-level data export so future migrations remain possible, but those clauses rarely appear in municipal RFP templates, perpetuating supplier lock-in.

By Type: IP Platforms Dominate but Niche TDM Demand Persists

IP-based consoles accounted for 67.75% revenue in 2025, yet the dispatch console market still sold thousands of TDM positions to mines, oil rigs, and rural utilities where deterministic latency and standalone reliability trump features. IP systems integrate seamlessly with broadband networks, support multimedia calls, and enable virtualized disaster-recovery positions, all compelling perks for urban agencies. Conversely, a 5.05% growth rate for TDM reflects emerging-market utilities laying new copper or microwave links where fiber is scarce. Interoperability gateways that translate between Session Initiation Protocol and circuit-switched signaling remain a thriving subsegment, as agencies avoid flash-cut migrations. The dispatch console market size for gateways is projected to reach USD 270 million by 2031, rising alongside hybrid architectures.

Vendor roadmaps suggest the inflection point will arrive as carriers sunset narrowband private lines in the late 2020s. Once service providers roll over to all-IP backbones, replacement demand will spike, compressing a decade of upgrades into a three-year window. Suppliers with field-swappable IP interface cards and pay-as-you-grow licensing will be positioned to capture the surge.

By Functionality: Voice is Foundational, Situational Intelligence Gains Ground

Voice dispatch remained the single-largest function with 31.10% of 2025 revenue. The dispatch console market continues to value instant push-to-talk, selective calling, and patching across disparate radio systems. Real-time monitoring, a composite of Automatic Vehicle Location, geofencing, and sensor dashboards, is the quickest riser, climbing at 4.64% CAGR. Integrators embed live traffic overlays, historical incident heatmaps, and machine-learning-based demand forecasts directly into dispatcher screens. Text dispatch adoption rises as states mandate two-way short message handling, but staffing models lag: centers still roster positions based on voice call volumes, not parallel text sessions. Geo-location accuracy improvements, using hybrid GPS, cellular, and Wi-Fi positioning, trim search radii to under 10 meters in urban canyons, slashing unit arrival times.

Data analytics modules that crunch call durations, queue lengths, and on-scene intervals help chiefs justify overtime budgets and identify training gaps. Yet, only 40% of buyers activate advanced dashboards within the first year, citing limited analyst headcount. Vendors who pre-package dashboards and automate exception alerts reduce the configuration burden, boosting adoption.

By End-User Industry: Logistics Commands Spending, Public Safety Accelerates Adoption

Transportation and logistics operators dominated with a 33.10% share in 2025, reflecting fleets of delivery vans, long-haul trucks, and passenger coaches that rely on real-time route adjustments to trim fuel and stretch driver hours-of-service. Consolidation across third-party logistics means a single buyer can outfit hundreds of depots, giving sellers economies of scale. Public safety agencies, however, are adding positions faster than any other group thanks to federal and state infrastructure funds that unlock capital for Next Generation 911 consoles, incident management, and call-taking software.

Utility, mining, and energy firms integrate dispatch with supervisory control and data acquisition to coordinate field crews restoring power after extreme weather or rerouting ore conveyance belts when predictive alarms fire. Defense agencies refresh command-and-control rooms to support multi-domain operations and plug into classified networks, demanding air-gapped variants of commercial consoles. Healthcare emergency medical services deploy dispatcher-to-hospital interfaces that feed patient vitals ahead of ambulance arrival, reducing emergency department congestion. Although education and hospitality segments represent under 5% of revenue, campus safety units increasingly pool budgets with facilities and IT to procure shared dispatch and access-control consoles, adding incremental demand.

Geography Analysis

North America represented 36.67% of the dispatch console market in 2025. Multi-state contracts, such as Washington’s USD 48 million statewide Emergency Services IP Network extension and New York’s USD 85 million county grant program, underpin a visible pipeline through 2031. Canada mandated Next Generation 911 functionality nation-wide by 2027, releasing CAD 25 million (USD 18 million) funding tranches that accelerate console orders. Nonetheless, the removal of federal matching funds from the 2025 U.S. budget shifted financial burden to states, elongating procurement for smaller jurisdictions. FirstNet integration obliges additional certification, increasing deployment planning from six to nine months but, once complete, enabling high-bandwidth video and drone feeds to flow directly into consoles.

Asia-Pacific offers the fastest 4.76% CAGR. India’s 100-city smart-city initiative rolled out Integrated Command and Control Centers that monitor 142,000-plus cameras, evidence of large orders for IP positions with advanced video analytics. China’s megacity clusters replicate this at even larger scales, though domestic procurement policies favor local suppliers. Dubai’s Enterprise Command and Control Center coordinates 28,000 vehicles and ingests 4.4 billion daily data points, showcasing the Middle Eastern appetite for high-throughput, AI-enabled consoles.[2]Media Office - Government of Dubai, “Enterprise Command and Control Centre Tour,” mediaoffice.ae Japan and South Korea focus on incremental upgrades, ensuring existing investments interface with 5G and autonomous vehicle trials without wholesale rip-and-replace.

Europe modernizes to meet Electronic Communications Code requirements. Contracts in the United Kingdom for Guardian Hub and 10-year mobile policing suites demonstrate willingness to commit long-term operating budgets. Hexagon’s EUR 10 million (USD 11.3 million) acquisition of a European recording solutions provider strengthens interoperability offerings that fit EU data residency mandates. South America’s opportunity is real but fragmented; provincial buyers in Argentina and Brazil publish sizable tenders yet face unpredictable foreign-exchange swings and constrained federal transfers. Middle East mega-projects such as Saudi Arabia’s Qiddiya Smart Command Center create lighthouse references that vendors cite globally. Africa remains nascent but selected metros in South Africa, Nigeria, and Egypt are starting feasibility studies, hinting at a potential wave of greenfield IP console deployments late in the forecast horizon.

Competitive Landscape

The dispatch console market is moderately concentrated. Motorola Solutions, Hexagon, and CentralSquare leverage decades-long maintenance contracts and proprietary data models that hamper agency switching. Motorola’s April 2026 purchase of HyperYou for agentic AI plus its CAD 675 million (USD 487 million) buyout of Bell Canada’s land-mobile-radio unit signal a strategy to package end-to-end voice, data, and AI into one invoice, squeezing room for mid-tier rivals.[3]Motorola Solutions Investor Relations, “HyperYou Acquisition Announcement,” motorolasolutions.com Hexagon fortified its portfolio by adding voice recording and quality management through a EUR 10 million (USD 11.3 million) acquisition, enabling bundled bids across Europe’s police and fire services. CentralSquare nudges customers toward Software-as-a-Service by sunsetting legacy on-premises lines, leaving agencies a choice between costly re-platforming or exit migration.

Challengers such as RapidDeploy, First Arriving, and Carbyne exploit cloud elasticity to spin up proof-of-concept instances inside days, cutting sales cycles to under six months when cooperative purchasing contracts are in place. Their go-to-market model appeals to counties lacking procurement staff, but they must still certify under Criminal Justice Information Services policies and pass tough scalability tests before winning statewide deals. White-space remains among mid-sized utilities and private-sector control rooms that need robust voice patching yet cannot afford premium integrated suites. Vendors offering modular licensing, web-based interfaces, and open data pipelines stand to expand here.

Mergers and acquisitions will likely continue as incumbents buy niche artificial intelligence or cybersecurity specialists to fill feature gaps. Product roadmaps indicate a pivot toward role-based user interfaces that hide complexity, enabling agencies to upskill new dispatchers amid labor shortages. At the same time, buyer concerns about multi-year, single-vendor lock-in foster a secondary market for middleware and interoperability gateways that de-risk future migrations.

Dispatch Console Industry Leaders

Motorola Solutions, Inc.

Airbus SE

ZERTON

Cisco Systems, Inc.

L3Harris Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Motorola Solutions acquired HyperYou to embed agentic AI that automates call triage and recommends unit dispatch.

- March 2026: Motorola Solutions purchased Bell Canada’s land-mobile-radio business for CAD 675 million (USD 487 million) to bundle nationwide infrastructure with console software.

- March 2026: Hexagon won a contract from Kitsap 911, Washington, to deploy HxGN OnCall Dispatch with live mapping and mobile apps.

- March 2026: First Arriving secured a National Cooperative Purchasing Alliance contract that lets U.S. agencies buy its real-time platform without issuing individual RFPs.

Global Dispatch Console Market Report Scope

The dispatch console market pertains to the industry segment focused on providing software and hardware solutions essential for real-time communication, coordination, and resource management in critical operations such as public safety, transportation, utilities, and emergency response. Dispatch consoles function as centralized platforms that integrate voice, data, and radio communications, enabling dispatchers to effectively monitor activities, allocate resources, and ensure seamless connectivity between field personnel and command centers.

The Dispatch Console Market Report is Segmented by Component (Hardware, Software), Type (IP-Based Dispatch Console, TDM-Based Dispatch Console), Functionality (Voice Dispatch, Text Dispatch, Geo-Location Services, Real-Time Monitoring, Data Analytics and Reporting), End-User Industry (Public Safety Agencies, Government and Defense, Transportation and Logistics, Healthcare, Manufacturing, Mining, Energy, and Utilities, Other End-User Industries), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| IP-Based Dispatch Console |

| TDM-Based Dispatch Console |

| Voice Dispatch |

| Text Dispatch |

| Geo-Location Services |

| Real-Time Monitoring |

| Data Analytics and Reporting |

| Public Safety Agencies |

| Government and Defense |

| Transportation and Logistics |

| Healthcare |

| Manufacturing |

| Mining, Energy, and Utilities |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Kuwait | |

| Bahrain | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| By Type | IP-Based Dispatch Console | |

| TDM-Based Dispatch Console | ||

| By Functionality | Voice Dispatch | |

| Text Dispatch | ||

| Geo-Location Services | ||

| Real-Time Monitoring | ||

| Data Analytics and Reporting | ||

| By End-User Industry | Public Safety Agencies | |

| Government and Defense | ||

| Transportation and Logistics | ||

| Healthcare | ||

| Manufacturing | ||

| Mining, Energy, and Utilities | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Kuwait | ||

| Bahrain | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the dispatch console market today?

The dispatch console market reached USD 2.16 billion in 2026 and is projected to grow to USD 2.70 billion by 2031, reflecting a 4.55% CAGR.

Which segment grows fastest within dispatch consoles?

Real-time monitoring functionality is expanding the fastest, advancing at a 4.64% CAGR as agencies integrate geo-location, sensor data, and predictive analytics alongside voice communications.

What drives console upgrades for 911 centers?

Next Generation 911 (NG9-1-1) mandates require call centers to support text, images, and video, forcing replacement of legacy consoles that cannot process multimedia communications.

Why are utilities investing in new dispatch consoles?

Grid modernization initiatives are consolidating control rooms and integrating distributed energy resources, driving demand for consoles capable of near-real-time situational awareness and advanced analytics.

Who are the leading vendors in dispatch consoles?

Motorola Solutions, Hexagon, and CentralSquare hold the largest market shares, supported by long-term maintenance contracts and proprietary integration ecosystems.

Which region is the fastest-growing market for dispatch consoles?

Asia-Pacific is the fastest-growing region, forecast to expand at a 4.76% CAGR through 2031, driven by large-scale smart-city command-center deployments in India, China, and parts of the Middle East.

Page last updated on: