Temperature Data Logger Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

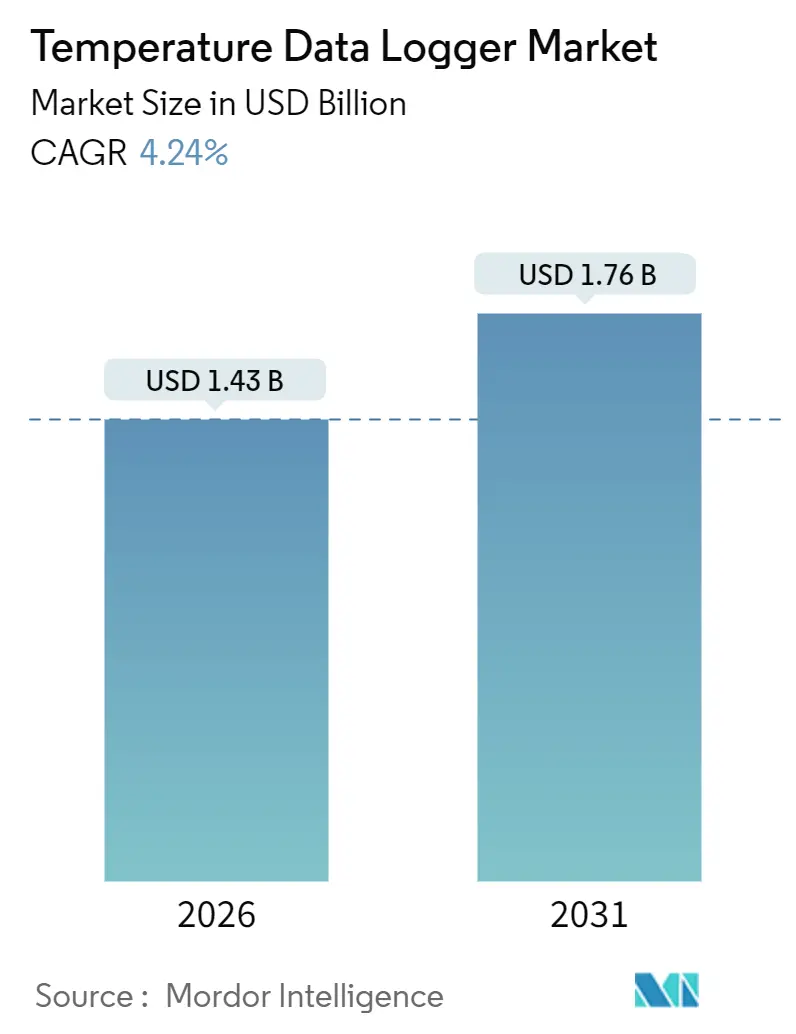

| Market Size (2026) | USD 1.43 Billion |

| Market Size (2031) | USD 1.76 Billion |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

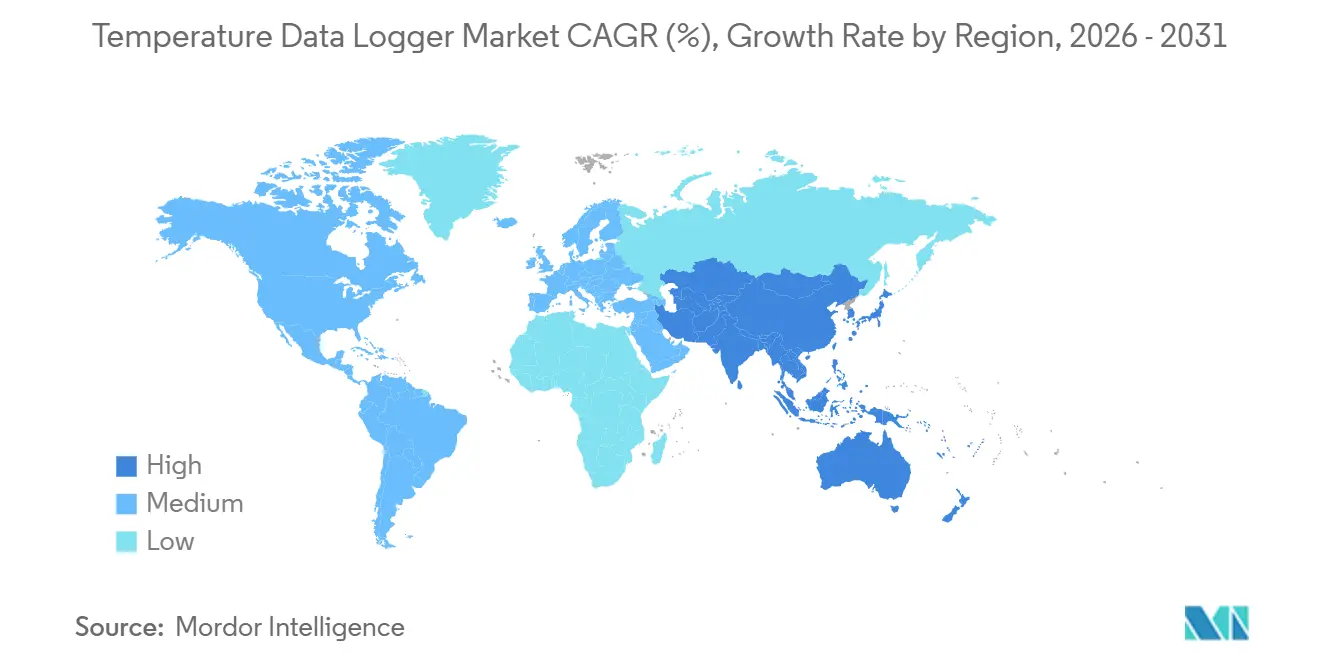

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Temperature Data Logger Market Analysis by Mordor Intelligence

The Temperature Data Logger Market size is estimated at USD 1.43 billion in 2026, and is expected to reach USD 1.76 billion by 2031, at a CAGR of 4.24% during the forecast period (2026-2031).

Demand is shifting toward cellular and IoT-connected devices, which are growing 7.06% annually, while Wi-Fi loggers that held 41.68% share in 2025 face battery-life and interoperability pressures. Regulatory mandates for digital cold-chain compliance in emerging economies, the rapid scale-up of mRNA vaccine pipelines that require ultra-cold tracking, and the expansion of hyper-local grocery fulfillment centers are widening the application base. Competition is intensifying as IoT-platform specialists bundle hardware at cost and monetize analytics subscriptions, forcing traditional instrument makers to add over-the-air updates and encrypted transmission. Lithium battery price volatility and connectivity fragmentation in Europe continue to weigh on margins, yet long-life sensors and miniaturized electronics are lowering ownership costs and extending device cycles, supporting steady growth across sectors.

Key Report Takeaways

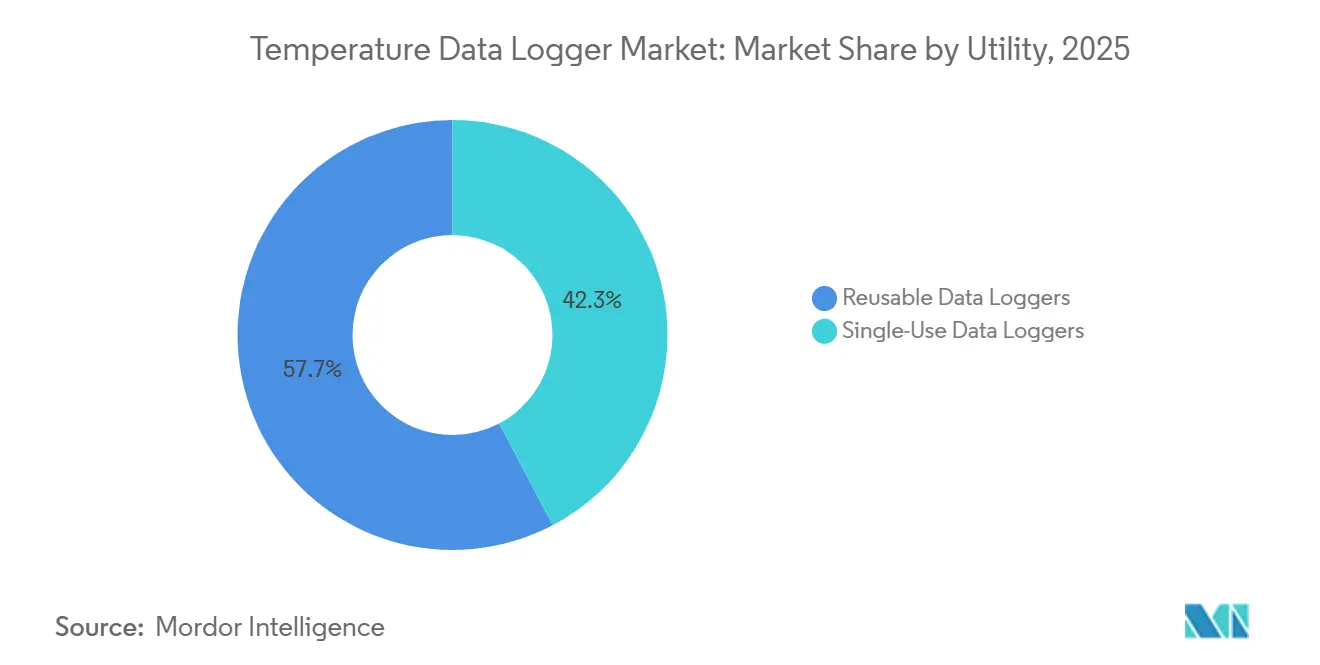

- By utility, reusable loggers led with 57.73% revenue share in 2025, while single-use devices are advancing at a 4.71% CAGR through 2031.

- By type, USB devices accounted for 34.91% of the temperature data logger market share in 2025, whereas Bluetooth Low Energy loggers are set to expand at a 5.23% CAGR to 2031.

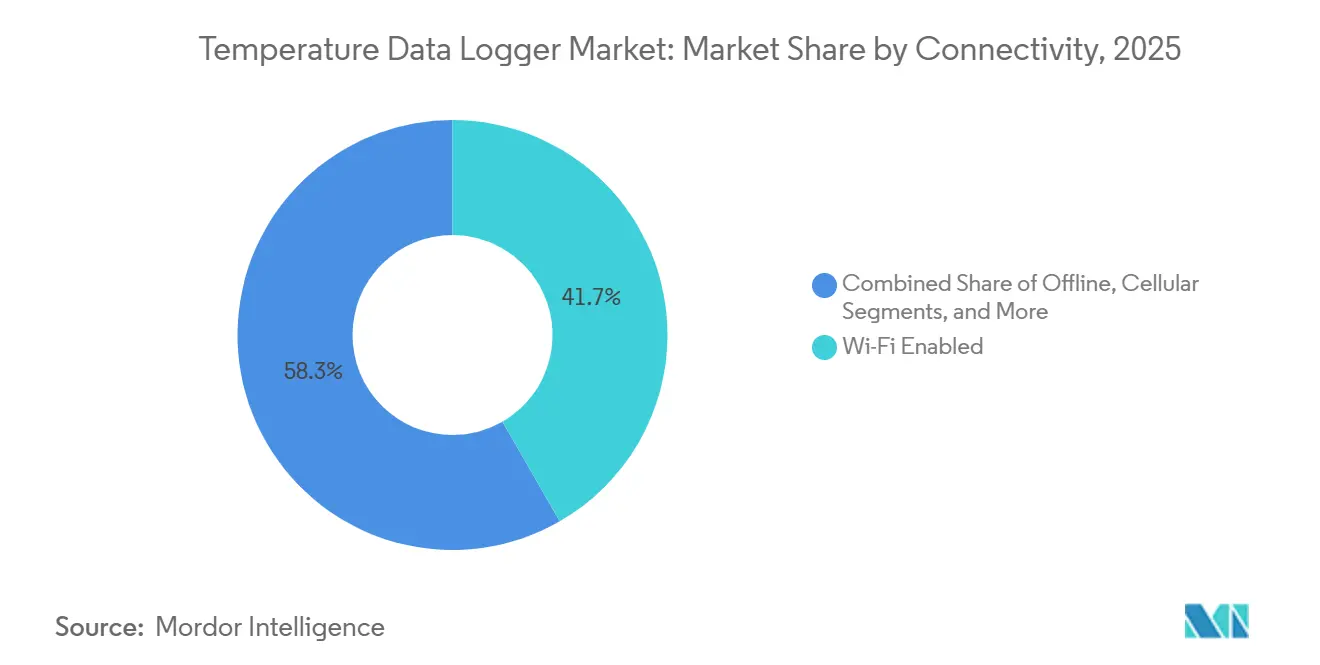

- By connectivity, Wi-Fi systems commanded 41.68% share in 2025, yet cellular and IoT-connected units are on course for a 7.06% CAGR over the same horizon.

- By application, life sciences and healthcare held 34.19% share in 2025, while cold-storage logistics remain the fastest climber at a 5.47% CAGR.

- By geography, North America dominated with 37.26% share in 2025, but Asia-Pacific is forecast to post a 5.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Temperature Data Logger Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandated Digital Cold-Chain Compliance in Emerging Economies | +1.2% | Asia-Pacific, Middle East and Africa, South America | Medium term (2-4 years) |

| Proliferation of mRNA Vaccine Pipelines Requiring Ultra-Cold Monitoring | +0.9% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| IoT-Enabled Asset Visibility Platforms Driving Logger Bundling | +0.8% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Miniaturization of Low-Power Sensors Extending Battery Life Beyond 5 Years | +0.6% | Global | Long term (≥ 4 years) |

| Expansion of Hyper-Local Fulfillment Centers Boosting Ambient Logger Demand | +0.5% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Real-Time AI Analytics Unlocking Predictive Maintenance of Cold Storage | +0.4% | North America, Europe, select Asia-Pacific hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandated Digital Cold-Chain Compliance in Emerging Economies

Regulators in India, Kenya, and South Africa began enforcing real-time temperature logging between 2024 and 2025, pushing distributors to retrofit fleets with cellular loggers that broadcast every 15 minutes.[1]India Central Drugs Standard Control Organisation, “Guidelines for Electronic Temperature Monitoring of Schedule X Drugs,” cdsco.gov.in Compressed implementation windows have replaced manual USB retrieval with always-connected units, accelerating hardware replacement cycles. Single-use shipments to sub-Saharan Africa rose 34% year over year in 2025 as distributors opted for tamper-evident devices that simplify audits. Vendors offering turnkey dashboards and local-language interfaces are gaining early footholds. The rising compliance bar is expected to cascade to other emerging markets, creating a secular pull for the temperature data logger market. Even regional food regulators are adopting the same digital templates, broadening the rule’s impact beyond pharmaceuticals.

Proliferation of mRNA Vaccine Pipelines Requiring Ultra-Cold Monitoring

World Health Organization guidance issued in 2024 cemented −70 °C to −80 °C as the storage benchmark for next-generation mRNA products.[2]World Health Organization, “Technical Specifications for Automated Temperature Monitoring Devices for Vaccine Cold Chain Equipment,” who.int Maintaining this band reduced potency loss to below 2%, compelling manufacturers to specify loggers with ±0.5 °C accuracy and one-minute sampling. Ultra-cold freezer makers now bundle calibrated loggers by default, turning an aftermarket accessory into standard equipment. Twelve CEPI-funded mRNA candidates under development each consume thousands of single-use loggers during validation trials. North American and European distributors fast-tracked upgrades, spurring above-market growth for ultra-cold-capable models. This dynamic positions the temperature data logger market as an essential enabler of mRNA supply chains over the next decade.

IoT-Enabled Asset-Visibility Platforms Driving Logger Bundling

Logistics operators are migrating from temperature-only monitoring to multi-sensor dashboards that merge location, shock, humidity, and thermal data. The 2024 Sensitech-Qualcomm collaboration embedded 5G modems into loggers, delivering geofencing alerts that cut claim rates by 23% for early adopters. Subscription pricing of USD 8-15 per shipment is replacing capital purchases, lowering barriers for smaller shippers. Retailers such as Walmart require platform-compatible loggers for preferred-vendor status, forcing suppliers to standardize. Device vendors lacking cloud ecosystems risk commoditization, while analytics-first players monetize long-tail data. The resulting shift concentrates value in software even as hardware volumes climb.

Miniaturization of Low-Power Sensors Extending Battery Life Beyond 5 Years

New sensor and timer chips launched in 2024 shaved power draw to microampere levels. Reusable loggers equipped with these components can operate for 7 years on a coin cell, eliminating the need for annual battery swaps. NOAA field deployments in 2025 validated the maintenance savings, and pharmaceutical protocols now accept reusable devices with documented five-year stability. Extended life reduces e-waste and total cost per shipment, prompting buyers to consider reusable units even in previously disposable-only scenarios. The innovation cycle supports gradual margin recovery for premium devices within the temperature data logger market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Connectivity Standards Hindering Interoperability | -0.7% | Global, acute in Europe and Asia-Pacific | Medium term (2-4 years) |

| Rising Lithium Supply Constraints Increasing Battery Costs | -0.5% | Global | Short term (≤ 2 years) |

| Cyber-Security Vulnerabilities Undermining Data Integrity Trust | -0.4% | Global, concentrated in regulated sectors | Medium term (2-4 years) |

| End-User Skill Gaps in Data Analytics Slowing Full Deployment | -0.3% | Emerging markets in Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Connectivity Standards Hindering Interoperability

Europe’s patchwork of LTE-M, NB-IoT, and LoRaWAN forces shippers to maintain parallel logger fleets or tolerate data blackouts when crossing borders.[3]European Telecommunications Standards Institute, “NB-IoT and LTE-M Interoperability Report,” etsi.org Integration testing stretched DHL’s 2025 pilot across 18 countries over 14 months, delaying rollouts. Cloud gateways add another layer of complexity as AWS, Azure, and Google Cloud require distinct provisioning flows. The resulting friction nudges smaller importers back to offline USB models, limiting real-time visibility gains. Although 3GPP Release 18 introduced RedCap to harmonize IoT radios, adoption remained below 5% of new logger shipments in late 2025.

Rising Lithium Supply Constraints Increasing Battery Costs

Lithium carbonate prices peaked at USD 28,000 per metric ton in early 2025 as electric-vehicle packs soaked up supply. Single-use logger makers dependent on lithium-thionyl chloride cells saw unit costs jump 54%, squeezing margins they could not pass on to price-sensitive pharmaceutical distributors. Berlinger disclosed a 320-basis-point margin erosion in its 2024 report. Sodium-ion pilots offer hope but lack low-temperature performance, leaving ambient-only niches for substitution. Until new mines ramp up, battery inflation will cap profitability despite healthy volume growth in the temperature data logger market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Utility: Single-Use Devices Capture Clinical-Trial Shipments

Single-use loggers expanded at a 4.71% CAGR through 2031, yet reusable devices retained 57.73% share in 2025. The single-use value proposition resonates with pharmaceutical sponsors that prioritize NIST-traceable calibration and zero cross-contamination between trials. Pfizer’s 2024 protocol update made disposable units mandatory for investigational products, a policy Merck mirrored within a year. Reusable loggers continue to dominate environmental monitoring and food processing, where multi-year calibration cycles dovetail with plant maintenance. The cost crossover occurs after 8-10 uses, above which reusable devices with swap-out battery packs, such as DicksonOne units introduced in 2025, become economical.

Longer life sensors and over-the-air recalibration are tipping the calculus in favor of reusable models for warehouse fleets. However, accelerated clinical pipelines and strict chain-of-custody rules in emerging markets keep disposable demand robust. The temperature data logger market thus supports dual tracks: high-end reusable systems for stationary facilities and scalable single-use units for point-to-point logistics. Vendors that offer unified dashboards spanning both formats are gaining preferred-supplier status, reinforcing the ecosystem play.

By Type: Bluetooth Low Energy Loggers Outpace USB Mainstays

Bluetooth Low Energy units are on track for a 5.23% CAGR through 2031, while USB devices that held 34.91% share in 2025 continue to decline. BLE’s appeal lies in its frictionless pairing with smartphones, enabling instant data sync without Wi-Fi or cables. Testo’s Saveris 2 gateway architecture cuts connectivity costs by 70% compared with direct cellular, supporting scale-up in multi-room cold stores.[4]Testo SE and Co. KGaA, “Saveris 2 Wireless Monitoring System,” testo.com USB models such as Lascar’s EL-USB-TC persist where air-gapped security is paramount, including defense and nuclear medicine labs. Web-based Ethernet loggers occupy a niche in fixed hospital pharmacies already wired for LAN access.

Hardware consolidation around BLE 5.2 simplifies firmware maintenance and accelerates adoption. As corporates deploy hybrid fleets, data harmonization becomes critical, spurring demand for cloud connectors that normalize USB CSV dumps and BLE real-time feeds. The temperature data logger market, therefore, balances legacy inertia with mobile-first innovation, a dynamic that shapes vendor roadmaps through the forecast period.

By Connectivity: Cellular IoT Leads Real-Time Visibility

Cellular and IoT-connected devices are expanding at 7.06% CAGR, the highest among connectivity types, as cross-border shippers demand uninterrupted telemetry. Wi-Fi loggers, which held a 41.68% share in 2025, remain entrenched in laboratories and retail pharmacies where access points are stable. Rotronic’s dual-radio HL-NT3 mitigates roaming losses by switching between LTE-M and NB-IoT within 30 seconds, covering 120 countries without manual SIM updates. Wi-Fi systems face network security hurdles that slow provisioning, though Vaisala’s on-premises servers help navigate strict compliance regimes.

RFID and NFC tags fill serialization niches, with Avery Dennison integrating blockchain to seal audit trails. Offline stand-alone units survive in expeditionary science and remote agriculture where power and coverage remain absent. As operators evaluate the total cost of cellular data versus Wi-Fi infrastructure, hybrid architectures that pool logger traffic through gateways are gaining attention. This coexistence underpins steady diversification inside the temperature data logger market.

By Application: Cold-Storage Logistics Become Fastest-Growing Use Case

Life sciences and healthcare commanded 34.19% of 2025 demand, but cold-storage logistics are growing at 5.47% CAGR as e-grocery chains roll out hyper-local hubs. Amazon Fresh runs 200-plus ambient loggers per micro-fulfillment center, integrating location and thermal alerts into routing algorithms. The U.S. Department of Agriculture’s 8 °C, 20-minute dairy threshold serves as the anchor for alert logic. High-value biologics now pair cellular telemetry with shock sensors, whereas lower-priced vaccines migrate to BLE devices that download data on arrival, balancing cost and compliance.

Food processing remains price-sensitive, favoring USD 50–80 USB models to cover HACCP checkpoints. Industrial environmental monitoring is moving toward wireless sensor networks that consolidate pressure and humidity measurements, trimming installation costs by 40% compared with discrete loggers. Museums, horticulture, and specialty manufacturing together contribute 12% of shipments, expanding in line with the broader temperature data logger market. Vendors that tailor firmware profiles to vertical-specific alarm thresholds gain traction as buyers prioritize plug-and-play validation.

Geography Analysis

Asia-Pacific delivers the fastest regional trajectory at a 5.67% CAGR to 2031, propelled by China’s cold-chain guidelines and India’s real-time vaccine mandate. China added 14 million m³ of refrigerated capacity in tier-2 cities in 2024, each new warehouse requiring 500-800 compliant loggers. India’s Food Safety and Standards Authority ordered live temperature feeds for every vaccine lane in 2025, triggering the replacement of 180,000 legacy USB units. Japan shortened calibration intervals to six months, steering hospitals toward reusable loggers with cloud certificates. These synchronized rules are expanding the temperature data logger market across the region, despite price sensitivity in lower-income economies.

North America retained a 37.26% share in 2025, supported by robust Food Safety Modernization Act enforcement and stringent good distribution practice audits. Platform adoption is mature; 62% of U.S. pharmaceutical distributors already use IoT-enabled loggers, evidencing the market’s pivot toward analytics. Hyper-local grocery expansion further boosts ambient logger volumes, while federal agencies advance cybersecurity baselines that favor vendors offering over-the-air patching. Stable regulatory clarity cushions demand against economic swings.

Europe’s adoption pace is tempered by connectivity fragmentation, even though good distribution practice updates issued in 2024 created a retrofit wave. Logistics providers juggle LTE-M, NB-IoT, and LoRa fleets, raising ownership costs and slowing device turnover. Nevertheless, GDP compliance still drives 40% of regional purchases, and subsidy programs in Germany and France offset part of the hardware upgrade costs. South America, the Middle East, and Africa remain sub-scale but invest in solar-powered cellular loggers for off-grid depots financed by Gavi grants. These long-tail markets offer attractive growth runways as digital cold-chain standards globalize.

Competitive Landscape

The temperature data logger market is moderately fragmented; the top five suppliers (Vaisala, Testo, Sensitech, Rotronic, and Onset) controlled a fair share of market revenue in 2025. Traditional instrument makers defend turf with ISO 17025 calibration and high-accuracy probes, while IoT specialists bundle devices at cost and monetize data subscriptions. Carrier’s 2024 purchase of Sensitech folded logger telemetry into the Lynx Fleet refrigeration suite, forging an end-to-end cold-chain platform that locks in trucking fleets. Startups such as Roambee deploy zero-upfront pricing, charging per shipment to lure cash-constrained regional distributors.

Technology differentiation now centers on firmware updateability and security compliance, following NIST's 2024 baseline update. Vendors can patch devices remotely, without retrieving devices, lowering total costs and liability for pharmaceutical clients. Patent filings cluster around low-power radio and battery algorithms, with Texas Instruments securing 14 new patents in 2024. Regional specialists remain relevant by localizing dashboards and offering 24-hour field support, but cross-border trade increasingly favors global platforms. Strategic moves in 2025 included Testo’s partnership with Siemens for HVAC predictive maintenance and Rotronic’s rollout of its dual-radio logger, underscoring the convergence between building automation and cold-chain telemetry. Competitive intensity is therefore poised to rise as service-centric models gain ground.

Temperature Data Logger Industry Leaders

OMEGA Engineering Inc. (Spectrics)

Sensitech Inc.

Testo SE & CO. KGaA

ELPRO-BUCHS AG

Onset Computer Engineering

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Milesight IoT launched the TS60x LoRaWAN sensor series with 10-year battery life and IP67 housing for outdoor cold-chain deployments.

- October 2025: Vaisala unveiled the HumiGuard HG3 reusable logger with integrated dew-point analytics and seven-year battery life.

- August 2025: Rotronic introduced the HL-NT4 cellular logger featuring dual LTE-M and NB-IoT radios across 140 countries.

- June 2025: Testo partnered with Siemens Building Technologies to connect Saveris 2 loggers to Desigo CC for predictive HVAC alerts.

- March 2025: Onset released the InTemp CX450 cellular logger with embedded GPS and accelerometer for pharma shipments.

Global Temperature Data Logger Market Report Scope

The Temperature Data Logger Market Report is Segmented by Utility (Single-Use Data Loggers, Reusable Data Loggers), Type (USB Data Loggers, Bluetooth Low Energy-Enabled Loggers, Web-Based Data Loggers, Wireless Data Loggers), Connectivity (Offline/Stand-Alone, Wi-Fi Enabled, Cellular/IoT-Connected, RFID/NFC-Enabled), Application (Life Sciences and Healthcare, Food Processing, Industrial, Cold Storage and Transportation, Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Single-use Data Loggers |

| Reusable Data Loggers |

| USB Data Loggers |

| Bluetooth Low Energy (BLE) Enabled Data Loggers |

| Web-Based Data Loggers |

| Wireless Data Loggers |

| Offline / Stand-Alone |

| Wi-Fi Enabled |

| Cellular / IoT-Connected |

| RFID / NFC-Enabled |

| Life Sciences and Healthcare (Hospitals, Laboratories, Pharmaceutical) |

| Food Processing |

| Industrial (Environmental Data Logging) |

| Cold Storage and Transportation (Logistics) |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Utility | Single-use Data Loggers | |

| Reusable Data Loggers | ||

| By Type | USB Data Loggers | |

| Bluetooth Low Energy (BLE) Enabled Data Loggers | ||

| Web-Based Data Loggers | ||

| Wireless Data Loggers | ||

| By Connectivity | Offline / Stand-Alone | |

| Wi-Fi Enabled | ||

| Cellular / IoT-Connected | ||

| RFID / NFC-Enabled | ||

| By Application | Life Sciences and Healthcare (Hospitals, Laboratories, Pharmaceutical) | |

| Food Processing | ||

| Industrial (Environmental Data Logging) | ||

| Cold Storage and Transportation (Logistics) | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the temperature data logger market in 2026?

The temperature data logger market size reached USD 1.43 billion in 2026 and is forecast to climb steadily through 2031.

Which segment is growing fastest within temperature data logging?

Cellular and IoT-connected loggers post the highest growth, advancing at a 7.06% CAGR driven by real-time visibility needs.

Why are single-use loggers still in demand?

Pharmaceutical sponsors prefer factory-calibrated, tamper-evident single-use devices for clinical-trial shipments, keeping disposable volumes high despite reusable gains.

What regional market shows the strongest growth outlook?

Asia-Pacific leads with a projected 5.67% CAGR as China and India tighten digital cold-chain mandates and expand refrigerated infrastructure.

How are vendors addressing battery cost inflation?

Suppliers mitigate lithium price spikes by adopting ultra-low-power sensors that stretch battery life to seven years and by piloting sodium-ion alternatives for ambient monitoring.

What is driving the shift toward subscription pricing?

IoT-enabled asset-visibility platforms bundle low-cost hardware with analytics services, turning one-time device sales into recurring per-shipment fees.

Page last updated on: