Medical Devices MLCC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

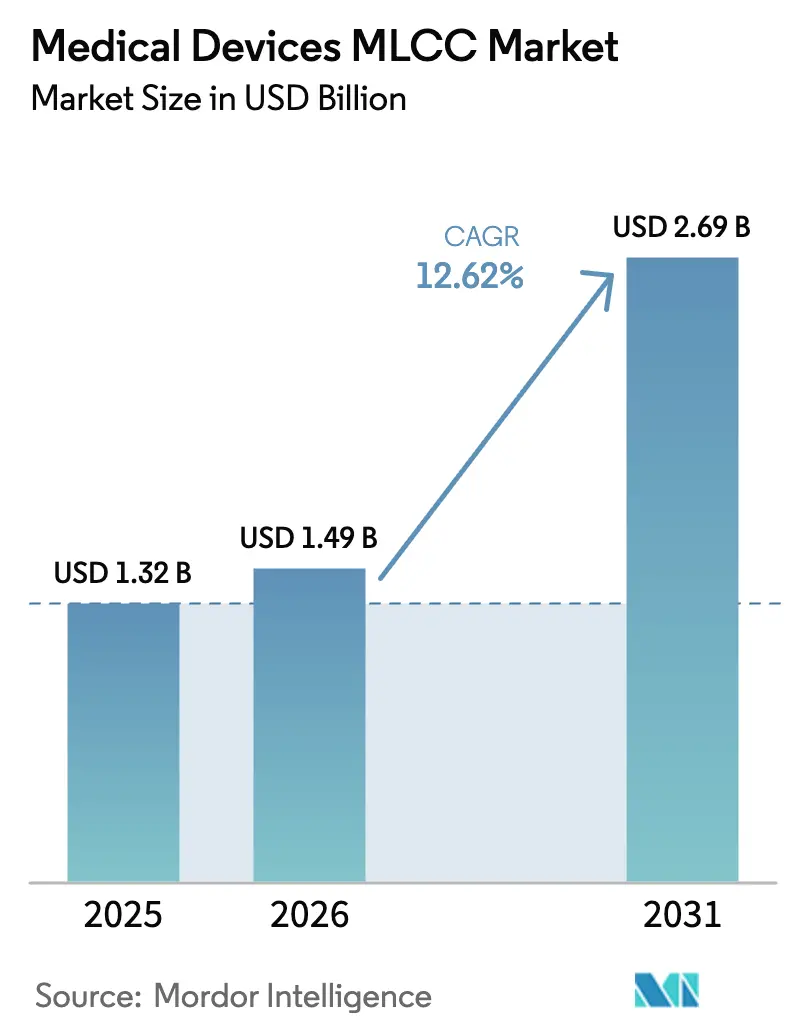

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 2.69 Billion |

| Growth Rate (2026 - 2031) | 12.62% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Devices MLCC Market Analysis by Mordor Intelligence

The medical devices MLCC market size is expected to grow from USD 1.32 billion in 2025 to USD 1.49 billion in 2026 and is forecast to reach USD 2.69 billion by 2031 at 12.62% CAGR over 2026-2031. Strong momentum is driven by the rapid adoption of miniaturized electronics in implantables, wearables, and diagnostic imaging systems, where multilayer ceramic capacitors (MLCCs) are essential for power regulation, signal filtering, and electromagnetic compatibility. The growing demand for connected health solutions, the convergence of artificial intelligence at the edge, and tightening global reliability standards are reinforcing supplier pricing power in specialty grades, even as commodity MLCC prices erode. Manufacturers are intensifying investments in high-capacitance Class 1 formulations, ultra-small 0402 and 0201 packages, and metal-cap mounts that withstand vibration in surgical robots. Regulatory frameworks such as ISO 13485 and IEC 60601 are increasing the requirements for traceability and biocompatibility, prompting OEMs to prefer established suppliers with vertically integrated supply chains that can certify powder chemistry, electrode metallurgy, and sterilization compatibility.

Key Report Takeaways

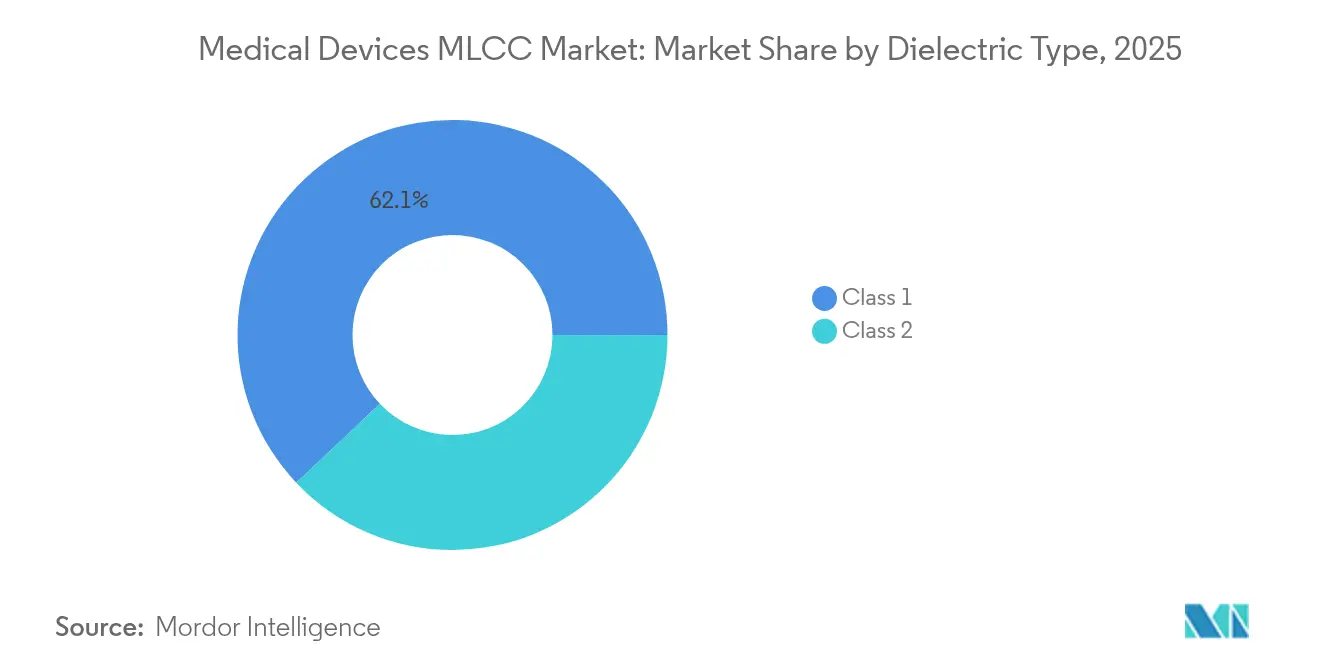

- By dielectric type, Class 1 MLCCs led with 62.05% medical devices MLCC market share in 2025, and Class 1 implantable-grade variants are projected to post the quickest 13.58% CAGR through 2031.

- By case size, the 201 format accounted for 56.02% of the medical devices MLCC market size in 2025, while the 402 format is forecast to advance at a 13.31% CAGR to 2031.

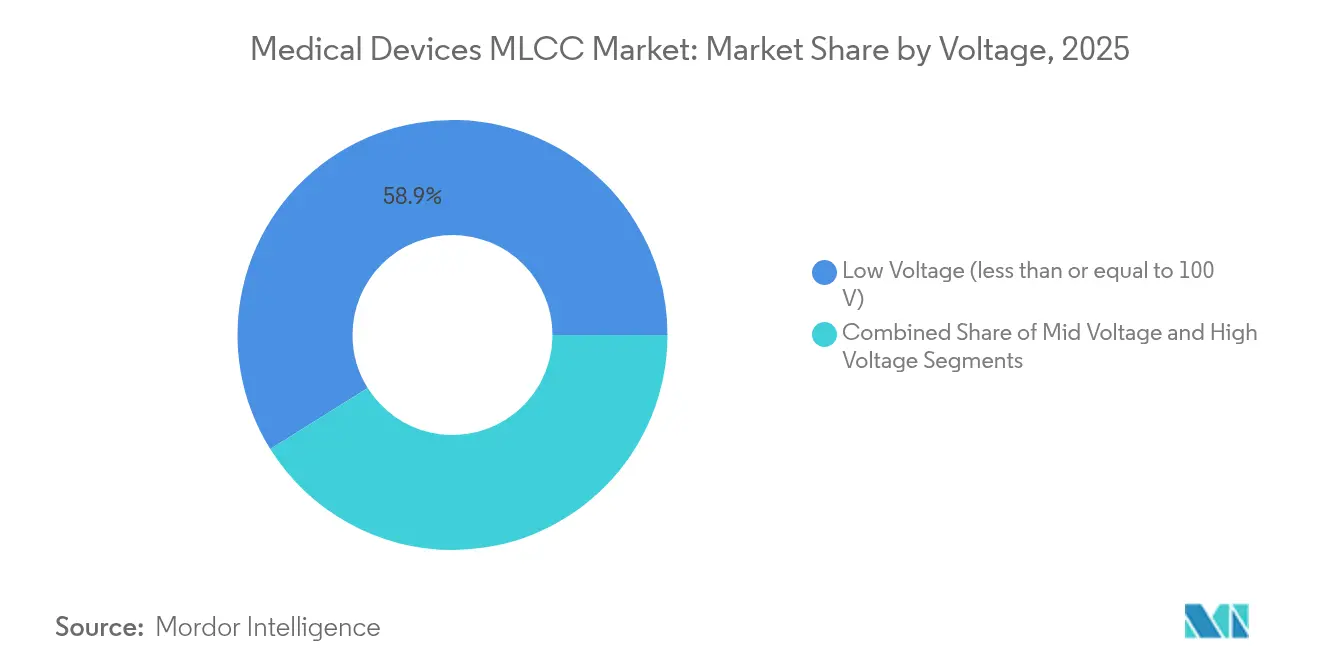

- By voltage rating, low-voltage (≤100 V) units captured 58.90% of the medical devices MLCC market size in 2025, whereas high-voltage (>500 V) grades are expected to climb at a 12.92% CAGR through 2031.

- By MLCC Mounting Type, surface-mount devices represented 41.25% of 2025 revenue, yet metal-cap versions are advancing at a 13.02% CAGR.

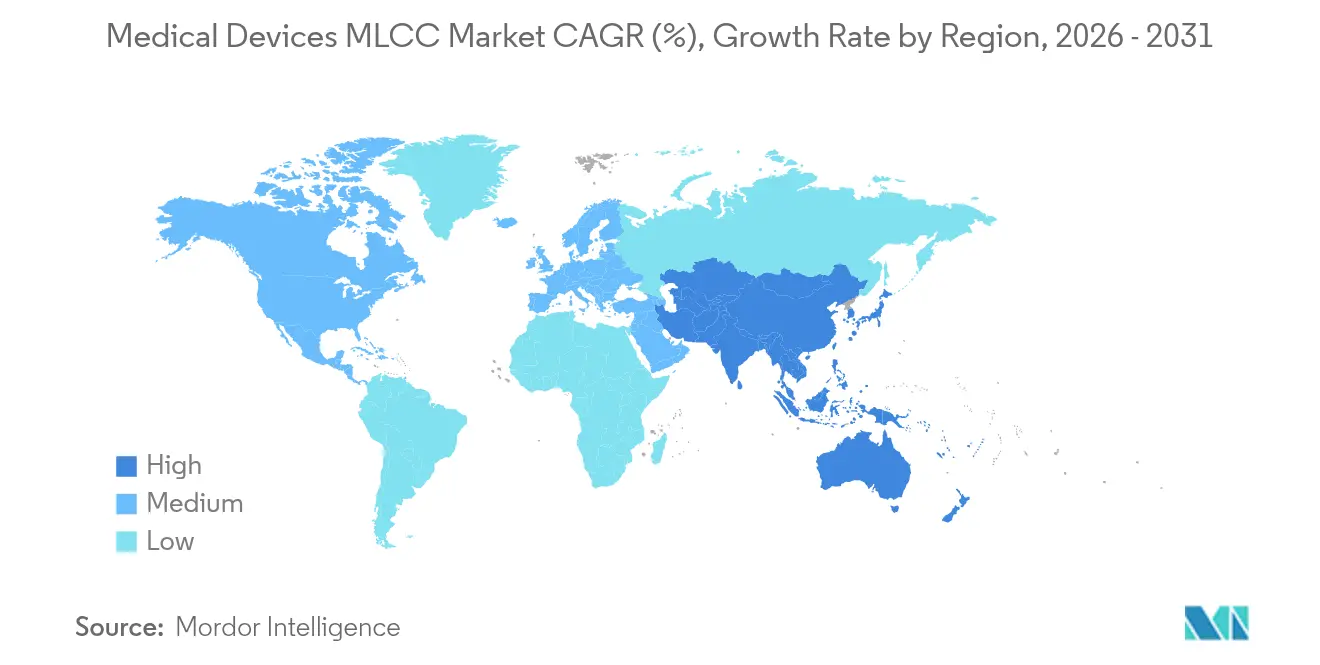

- By Geography, the Asia-Pacific region dominated with a 57.15% revenue share in 2025, while North America is expected to expand at a 13.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Devices MLCC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Miniaturization of implantable medical devices | +2.8% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Adoption surge in connected wearables and tele-health monitors | +3.2% | Global, led by Asia-Pacific consumer markets | Short term (≤ 2 years) |

| Regulatory push for higher-reliability passive components | +2.1% | North America and Europe, extending to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of home-care portable diagnostics | +2.4% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Integration into neuromodulation micro-stimulators | +1.8% | North America and Europe | Long term (≥ 4 years) |

| Shift to high-voltage MLCCs in robotic surgery systems | +1.3% | Global, concentrated in advanced healthcare markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Miniaturization of Implantable Medical Devices

Breakthrough 0402-size MLCCs offering 47 µF capacitance let pacemaker designers shrink enclosures by up to 30% while preserving energy density. [1]Murata Manufacturing, “Automotive MLCCs Balancing Reliability with Miniaturization,” murata.com Dielectric layers below 20 µm now embed directly into flexible polymer circuits for brain-computer interfaces, yet engineers must balance reduced thickness with voltage stability across the 25 °C to 42 °C body range. Class 1 C0G compositions remain preferred, despite their lower volumetric efficiency, because their ±30 ppm/°C drift safeguards therapy accuracy during decades-long implantation. Parallel work on hermetic encapsulation and barrier films guards against fluid ingress and prevents ionic leachates, helping suppliers meet ISO 10993 requirements.

Adoption Surge in Connected Wearables and Tele-Health Monitors

Global shipments of smart health wearables are expected to surpass 800 million units in 2025, each incorporating dozens of decoupling MLCCs that must exhibit ultra-low ESR to support on-device AI engines operating within a 1.5 W budget. High-frequency stability ensures clean sensor data for optical heart rate, blood glucose, and continuous blood pressure monitoring. FDA cybersecurity guidance is prompting device creators to specify components with tighter tolerances and longer aging stability, thereby eroding the viability of low-tier, commodity capacitors. Suppliers are responding with Class 1, low-aging MLCCs that sustain calibration for five-year service intervals under variable ambient conditions.

Regulatory Push for Higher-Reliability Passive Components

ISO 13485 revisions now require component-level process change notification and extended fault tree analysis, elevating automotive-grade AEC-Q200 tests to a de facto benchmark for critical medical electronics. Documentation must include extractables, leachables, and sterilization resilience for gamma, ethylene oxide, and autoclave cycles. MLCC vendors capable of disclosing powder provenance, sintering schedules, and electrode plating chemistry gain preferred-supplier status. The European MDR requires a clinical evaluation of passive parts in contact with bodily fluids, further favoring firms with long operating records and biocompatibility data.

Expansion of Home-Care Portable Diagnostics

Point-of-care analyzers used at home rely on MLCCs that limit leakage below microampere thresholds to maximize battery runtime in glucose meters and infusion pumps. Designers specify low-loss dielectrics that maintain capacitance over a temperature range of –10 °C to 45 °C, ensuring test accuracy remains within tight medical error bands. Regulatory guidance demands safeguards against drift during multi-year, unsupervised use, stimulating interest in MLCCs with built-in self-diagnostic impedance monitoring. Suppliers integrate metal-cap terminations to bolster mechanical integrity when devices are dropped or exposed to transport vibration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile BaTiO₃ raw-material supply chain | -1.9% | Global, with acute impact in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Price erosion of mainstream Class-2 MLCCs | -1.4% | Global, most severe in cost-sensitive segments | Medium term (2-4 years) |

| Biocompatibility concerns over nickel electrodes | -1.1% | North America and Europe regulatory markets | Long term (≥ 4 years) |

| Competition from ultra-thin polymer capacitors | -0.8% | Global, concentrated in miniaturized applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile BaTiO₃ Raw-Material Supply Chain

High-purity barium titanate powder shortages cause 40-60% cost swings within a year, as only a handful of mines meet the medical-grade stoichiometry and contamination specifications. Vertical integration shields large Japanese vendors; however, a disruption at a single chemical precursor plant can simultaneously idle multiple MLCC fabs. ISO 13485 change-control requirements slow cross-qualification of alternative powders, forcing OEMs to carry larger safety stocks that tie up working capital. [2]Murata Manufacturing, “Financial Highlights,” murata.com

Price Erosion of Mainstream Class-2 MLCCs

Commodity capacitors face annual double-digit price drops, prompting tier-one suppliers to prioritize higher-margin medical and automotive parts while downsizing standard Class-2 lines. Start-ups and niche device makers struggle to secure allocation for low-volume specialty builds, stretching design cycles and raising bill-of-materials costs. Market bifurcation widens between oversupplied consumer-grade parts and scarce, implantable-qualified parts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dielectric Type: Class 1 Dominates Stability-Critical Applications

Class 1 MLCCs captured 62.05% of 2025 revenue as designers prize their flat temperature coefficients in ECG, EEG, and implantable pulse generators. The medical devices MLCC market size for Class 1 is projected to advance at a 13.58% CAGR to 2031. Demand focuses on C0G/NP0 ceramics, maintaining a ±30 ppm/°C drift over the –55 °C to 125 °C test window. Class 2, while offering higher volumetric efficiency, experiences restricted uptake in life-support circuits because capacitance can decrease by 15-25% under bias, potentially compromising diagnostic accuracy.

Innovations focus on lead-free ferroelectric compositions that meet RoHS requirements without compromising the Q-factor. TDK’s 10 kV-rated X-ray capacitor series demonstrates how refined powder morphology and electrode plating enhance breakdown voltage without increasing footprint. Regulatory momentum favors Class 1 materials because their aging rate remains below 0.3% per decade, easing long-term calibration requirements in implantables.

By Case Size: Miniaturization Drives 201 and 402 Adoption

The 201 family accounted for 56.02% of the revenue in 2025, mirroring the medical devices MLCC market's preference for ultracompact components in drug-delivery pumps and cochlear implants. Component makers now pattern electrodes within 50 µm pitch while preserving insulation margins, maintaining yields above 98%. Meanwhile, the 402 size enjoys 13.31% CAGR as it balances miniaturization with manufacturing robustness for higher capacitance stacks that power edge-AI wearables.

Larger casings, ranging from 603 to 1210, persist in defibrillators and MRI gradient amplifiers, where designers require more than 500 V and ripple current endurance. Challenges for the tiniest sizes involve electrode alignment tolerance and solder-joint reliability on high-density PCBs-issues that metal-cap terminations and sintered copper barrier layers actively mitigate.

By Voltage: Low-Voltage Segments Lead Despite High-Voltage Growth

Low-voltage (≤100 V) capacitors dominated the market with a 58.90% share in 2025, as battery-operated devices proliferated. The segment is projected to climb 13.20% CAGR through 2031, in line with the adoption of continuous glucose monitors and smart patches. The medical devices MLCC market share for high-voltage grades remains modest yet lucrative; accelerated growth stems from the drive for robotic surgery, phototherapy systems, and compact ultrasound transducers now transitioning toward 800 V bus architectures. Suppliers integrate porcelain dielectric layers and interleaved copper screens to suppress partial discharge.

By MLCC Mounting Type: Surface-Mount Technology Leads Market

Surface-mount technology accounted for 41.25% of 2025 revenue, favored for automated reflow assembly. However, metal-cap devices log a 13.02% CAGR as surgical robots and portable analyzers seek shock resistance. Radial-lead packages persist in legacy infusion pumps, which require through-hole retention during sterilization cycles. KYOCERA AVX’s hermetic metal-cap MLCCs add glass-to-metal seals that block moisture in fully immersible implants.

Geography Analysis

Asia-Pacific commanded 57.15% of 2025 sales, reflecting the synergy of Japanese materials science, Korean production scale, and China’s cost-efficient fabs. Japan hosts over 65% of global MLCC capacity for medical-grade lines and remains the key hub for powder synthesis know-how. South Korea scales high-volume lines, while China ramps emerging producers in mainstream segments, yet lags in implantable-qualified grades. Governments across the region are streamlining approval pathways for digital health devices, thereby enhancing domestic MLCC uptake.

North America is the fastest-growing territory, with a 13.71% CAGR to 2031, driven by a robust startup scene and stringent FDA mandates that favor high-reliability components. U.S. device makers increasingly specify automotive-grade reliability for life-critical circuits, benefiting suppliers with legacy AEC-Q200 portfolios. Venture funding in neuromodulation, digital therapeutics, and AI-driven diagnostics sustains design wins for specialized MLCCs.

Europe maintains solid demand under the MDR framework, prioritizing lifecycle risk management. German OEMs integrate precision Class 1 capacitors into high-resolution CT scanners, while Nordic innovators leverage tiny 201 packages for next-gen continuous monitoring patches. The region’s sustainability focus accelerates the adoption of lead-free dielectrics despite incremental costs. Emerging markets in Latin America and the Middle East represent untapped potential as hospital modernization programs require advanced imaging and patient monitoring systems.

Competitive Landscape

Innovation and Compliance Drive Market Success

Six entrenched suppliers-Murata, Samsung Electro-Mechanics, KYOCERA AVX, TDK, Taiyo Yuden, and Vishay-collectively held almost 70% of shipments in 2024. Their dominance stems from vertically integrated control over ceramic powders, green-sheet casting, and termination metallurgy. Murata’s investment in AI-enabled defect inspection drives zero-ppm quality, a critical requirement for implantables. Samsung expands multilayer lines with spacers under 0.8 µm to boost capacitance density without sacrificing reliability. KYOCERA AVX courts medical OEMs through application-engineering centers that co-design capacitors to meet sterilization and biocompatibility tests.

Second-tier specialists carve niches in ultra-high voltage or flexible form factors. TDK’s 10 kV series addresses portable X-ray couplers. Vishay leverages medical-grade tantalum heritage to cross-sell pulse-stable MLCCs into defibrillators. Patent portfolios in doped BaTiO₃ compositions and nickel barrier layers reinforce entry barriers. Supply security considerations prompt OEMs to dual-source from at least two of the top six vendors, despite qualification costs, which anchors the high concentration ratio.

Medical Devices MLCC Industry Leaders

KYOCERA AVX Components Corporation

Maruwa Co., Ltd.

Murata Manufacturing Co., Ltd.

Nippon Chemi-Con Corporation

Samsung Electro-Mechanics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: KYOCERA AVX unveiled groundbreaking AI sensor technology and underwater communication systems at CES 2025, highlighting MLCCs with low parasitics and excellent EMI filtering capabilities positioned for medical, automotive, and IoT applications across multiple voltage ratings and package configurations StockTitan.

- November 2024: Pacific BioLabs updated ISO 10993 biocompatibility protocols, widening extractables targets for ceramic passives

- October 2024: Murata released its “Murata Value Report 2024,” confirming capital allocation for medical-grade MLCC expansion

- June 2024: TDK showcased 10 kV MLCCs for mobile X-ray ramps, enabling smaller resonant tanks

Global Medical Devices MLCC Market Report Scope

0 402, 0 603, 0 805, 1 206, 1 210, Others are covered as segments by Case Size. 100V to 500V, Above 500V, Less than 100V are covered as segments by Voltage. 10 μF to 100 μF, Less than 10 μF, More than 100 μF are covered as segments by Capacitance. Class 1, Class 2 are covered as segments by Dielectric Type. Asia-Pacific, Europe, North America are covered as segments by Region.| Class 1 |

| Class 2 |

| 201 |

| 402 |

| 603 |

| 1005 |

| 1210 |

| Other Case Sizes |

| Low Voltage (less than or equal to 100 V) |

| Mid Voltage (100 – 500 V) |

| High Voltage (above 500 V) |

| Metal-Cap |

| Radial-Lead |

| Surface-Mount |

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Dielectric Type | Class 1 | |

| Class 2 | ||

| By Case Size | 201 | |

| 402 | ||

| 603 | ||

| 1005 | ||

| 1210 | ||

| Other Case Sizes | ||

| By Voltage | Low Voltage (less than or equal to 100 V) | |

| Mid Voltage (100 – 500 V) | ||

| High Voltage (above 500 V) | ||

| By MLCC Mounting Type | Metal-Cap | |

| Radial-Lead | ||

| Surface-Mount | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Market Definition

- MLCC (Multilayer Ceramic Capacitor) - A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits.

- Voltage - The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V)

- Capacitance - The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor

- Case Size - The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height

| Keyword | Definition |

|---|---|

| MLCC (Multilayer Ceramic Capacitor) | A type of capacitor that consists of multiple layers of ceramic material, alternating with conductive layers, used for energy storage and filtering in electronic circuits. |

| Capacitance | The measure of a capacitor's ability to store electrical charge, expressed in farads (F). It determines the amount of energy that can be stored in the capacitor |

| Voltage Rating | The maximum voltage that a capacitor can safely withstand without experiencing breakdown or failure. It is typically expressed in volts (V) |

| ESR (Equivalent Series Resistance) | The total resistance of a capacitor, including its internal resistance and parasitic resistances. It affects the capacitor's ability to filter high-frequency noise and maintain stability in a circuit. |

| Dielectric Material | The insulating material used between the conductive layers of a capacitor. In MLCCs, commonly used dielectric materials include ceramic materials like barium titanate and ferroelectric materials |

| SMT (Surface Mount Technology) | A method of electronic component assembly that involves mounting components directly onto the surface of a printed circuit board (PCB) instead of through-hole mounting. |

| Solderability | The ability of a component, such as an MLCC, to form a reliable and durable solder joint when subjected to soldering processes. Good solderability is crucial for proper assembly and functionality of MLCCs on PCBs. |

| RoHS (Restriction of Hazardous Substances) | A directive that restricts the use of certain hazardous materials, such as lead, mercury, and cadmium, in electrical and electronic equipment. Compliance with RoHS is essential for automotive MLCCs due to environmental regulations |

| Case Size | The physical dimensions of an MLCC, typically expressed in codes or millimeters, indicating its length, width, and height |

| Flex Cracking | A phenomenon where MLCCs can develop cracks or fractures due to mechanical stress caused by bending or flexing of the PCB. Flex cracking can lead to electrical failures and should be avoided during PCB assembly and handling. |

| Aging | MLCCs can experience changes in their electrical properties over time due to factors like temperature, humidity, and applied voltage. Aging refers to the gradual alteration of MLCC characteristics, which can impact the performance of electronic circuits. |

| ASPs (Average Selling Prices) | The average price at which MLCCs are sold in the market, expressed in USD million. It reflects the average price per unit |

| Voltage | The electrical potential difference across an MLCC, often categorized into low-range voltage, mid-range voltage, and high-range voltage, indicating different voltage levels |

| MLCC RoHS Compliance | Compliance with the Restriction of Hazardous Substances (RoHS) directive, which restricts the use of certain hazardous substances, such as lead, mercury, cadmium, and others, in the manufacturing of MLCCs, promoting environmental protection and safety |

| Mounting Type | The method used to attach MLCCs to a circuit board, such as surface mount, metal cap, and radial lead, which indicates the different mounting configurations |

| Dielectric Type | The type of dielectric material used in MLCCs, often categorized into Class 1 and Class 2, representing different dielectric characteristics and performance |

| Low-Range Voltage | MLCCs designed for applications that require lower voltage levels, typically in the low voltage range |

| Mid-Range Voltage | MLCCs designed for applications that require moderate voltage levels, typically in the middle range of voltage requirements |

| High-Range Voltage | MLCCs designed for applications that require higher voltage levels, typically in the high voltage range |

| Low-Range Capacitance | MLCCs with lower capacitance values, suitable for applications that require smaller energy storage |

| Mid-Range Capacitance | MLCCs with moderate capacitance values, suitable for applications that require intermediate energy storage |

| High-Range Capacitance | MLCCs with higher capacitance values, suitable for applications that require larger energy storage |

| Surface Mount | MLCCs designed for direct surface mounting onto a printed circuit board (PCB), allowing for efficient space utilization and automated assembly |

| Class 1 Dielectric | MLCCs with Class 1 dielectric material, characterized by a high level of stability, low dissipation factor, and low capacitance change over temperature. They are suitable for applications requiring precise capacitance values and stability |

| Class 2 Dielectric | MLCCs with Class 2 dielectric material, characterized by a high capacitance value, high volumetric efficiency, and moderate stability. They are suitable for applications that require higher capacitance values and are less sensitive to capacitance changes over temperature |

| RF (Radio Frequency) | It refers to the range of electromagnetic frequencies used in wireless communication and other applications, typically from 3 kHz to 300 GHz, enabling the transmission and reception of radio signals for various wireless devices and systems. |

| Metal Cap | A protective metal cover used in certain MLCCs (Multilayer Ceramic Capacitors) to enhance durability and shield against external factors like moisture and mechanical stress |

| Radial Lead | A terminal configuration in specific MLCCs where electrical leads extend radially from the ceramic body, facilitating easy insertion and soldering in through-hole mounting applications. |

| Temperature Stability | The ability of MLCCs to maintain their capacitance values and performance characteristics across a range of temperatures, ensuring reliable operation in varying environmental conditions. |

| Low ESR (Equivalent Series Resistance) | MLCCs with low ESR values have minimal resistance to the flow of AC signals, allowing for efficient energy transfer and reduced power losses in high-frequency applications. |

Research Methodology

Mordor Intelligence has followed the following methodology in all our MLCC reports.

- Step 1: Identify Data Points: In this step, we identified key data points crucial for comprehending the MLCC market. This included historical and current production figures, as well as critical device metrics such as attachment rate, sales, production volume, and average selling price. Additionally, we estimated future production volumes and attachment rates for MLCCs in each device category. Lead times were also determined, aiding in forecasting market dynamics by understanding the time required for production and delivery, thereby enhancing the accuracy of our projections.

- Step 2: Identify Key Variables: In this step, we focused on identifying crucial variables essential for constructing a robust forecasting model for the MLCC market. These variables include lead times, trends in raw material prices used in MLCC manufacturing, automotive sales data, consumer electronics sales figures, and electric vehicle (EV) sales statistics. Through an iterative process, we determined the necessary variables for accurate market forecasting and proceeded to develop the forecasting model based on these identified variables.

- Step 3: Build a Market Model: In this step, we utilized production data and key industry trend variables, such as average pricing, attachment rate, and forecasted production data, to construct a comprehensive market estimation model. By integrating these critical variables, we developed a robust framework for accurately forecasting market trends and dynamics, thereby facilitating informed decision-making within the MLCC market landscape.

- Step 4: Validate and Finalize: In this crucial step, all market numbers and variables derived through an internal mathematical model were validated through an extensive network of primary research experts from all the markets studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 5: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platform