Telecom API Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

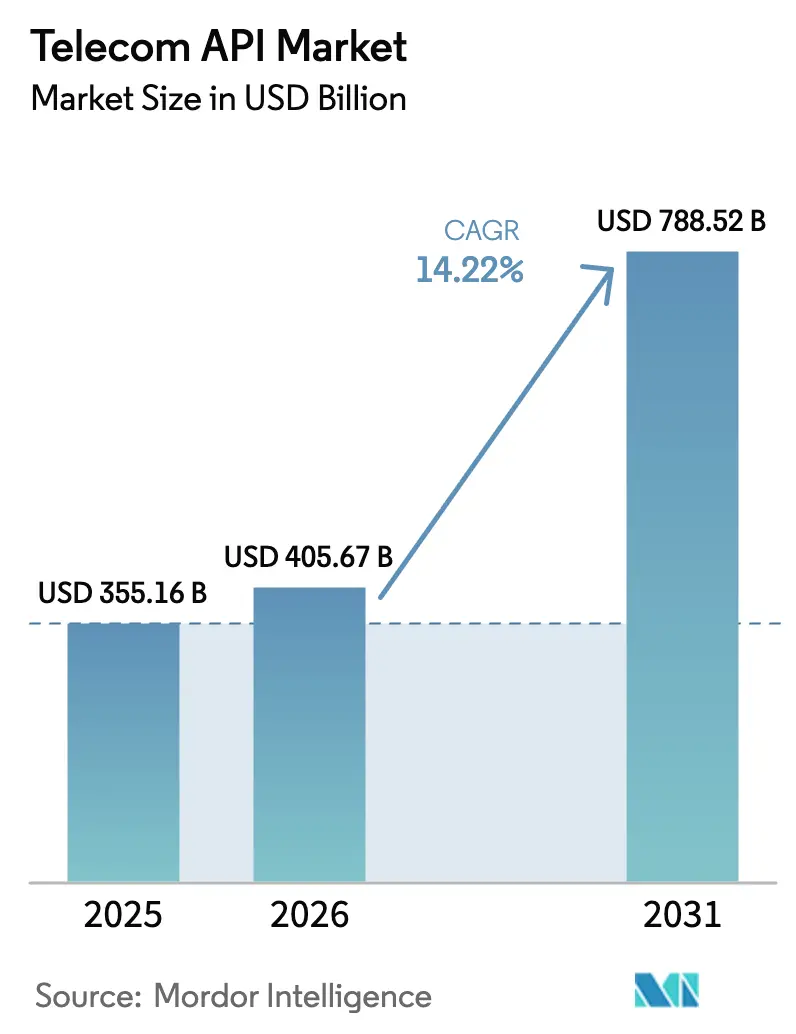

| Market Size (2026) | USD 405.67 Billion |

| Market Size (2031) | USD 788.52 Billion |

| Growth Rate (2026 - 2031) | 14.22% CAGR |

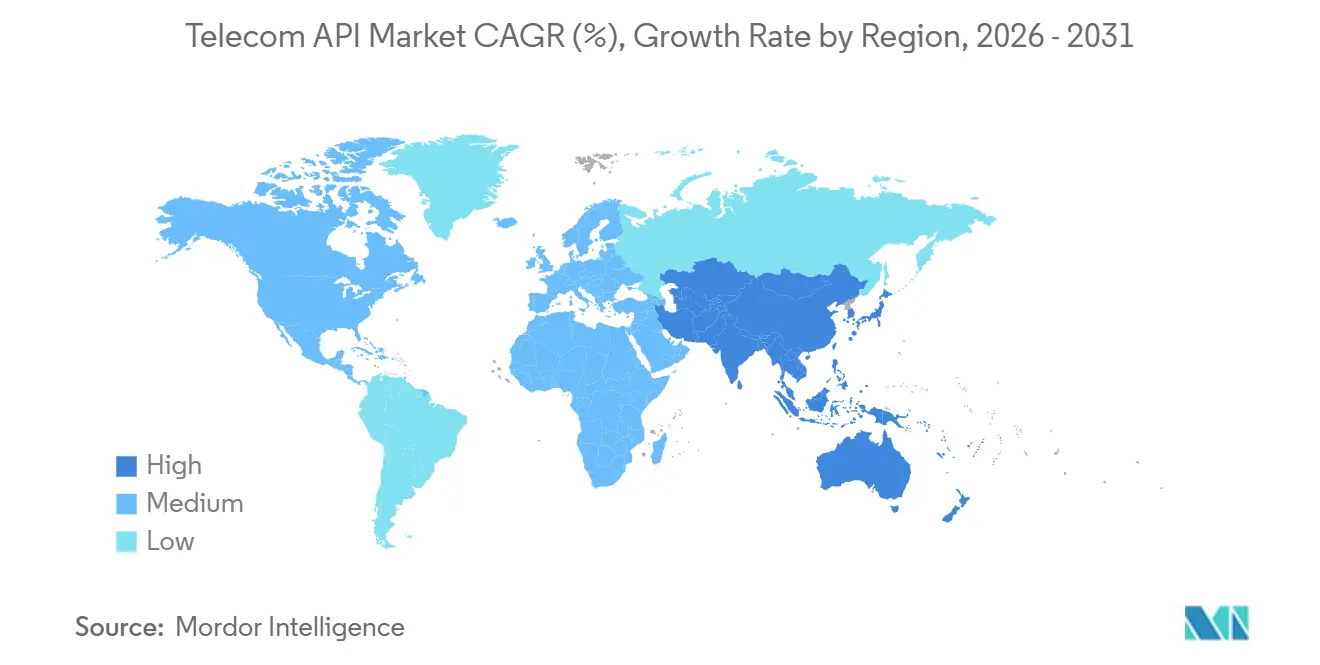

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

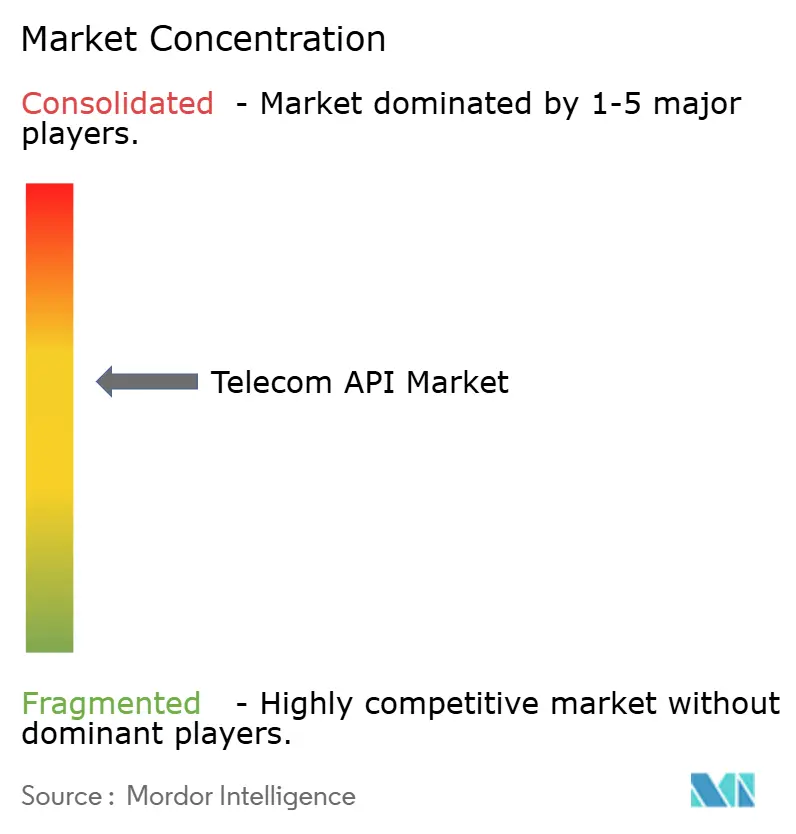

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telecom API Market Analysis by Mordor Intelligence

The telecom API market size reached USD 405.67 billion in 2026 from USD 355.16 billion in 2025, and is projected to register a 14.22% CAGR to touch USD 788.52 billion by 2031, underscoring a structural pivot from connectivity-only offerings toward platform business models that monetize network capabilities through standardized application programming interfaces. Operators now package location verification, network slicing, quality of service, carrier billing, and messaging functions as developer-ready services, accelerating time-to-market for enterprise and long-tail developers. The GSMA Open Gateway initiative, whose 72 operator groups cover 284 networks, removed bilateral integration friction by federating CAMARA-compliant APIs and OAuth 2.0 authentication. North America maintained technological leadership in 2025, yet Asia Pacific is expanding fastest as Reliance Jio and China Mobile expose edge-computing and network-slicing APIs to their vast 5G standalone subscriber bases. Payment, messaging and quality-on-demand APIs benefit from telco-fintech convergence, rich-communication upgrades on iOS and Android, and enterprise demand for low-latency edge services. Competitive intensity is rising because CPaaS aggregators, incumbent carriers, and hyperscalers all target the same developer wallet, simultaneously pressuring margins and stimulating innovation across marketplaces, security, and compliance.

Key Report Takeaways

- By service type, messaging held 37.82% of the telecom API market share in 2025, while payment APIs are forecast to expand at a 14.88% CAGR through 2031.

- By deployment type, hybrid architectures captured 56.82% of the telecom API market size in 2025, whereas multi-cloud implementations are advancing at a 15.34% CAGR to 2031.

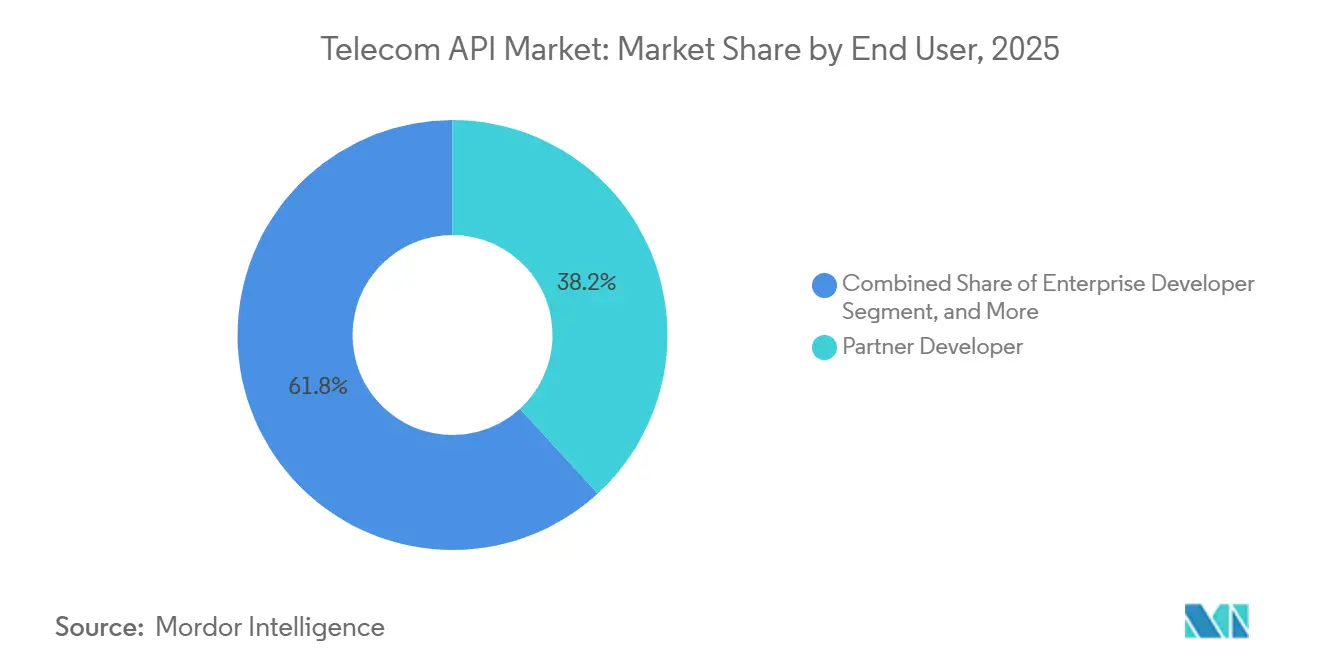

- By end-user, partner developers accounted for 38.2% share of the telecom API market size in 2025 and long-tail developers are projected to record the highest CAGR at 14.98% through 2031.

- By business model, aggregator-led CPaaS accounted for 46.72% share of the telecom API market size in 2025 and API marketplace / exchange record the highest projected CAGR at 15.22% through 2031.

- By geography, North America led with 38.73% revenue share in 2025 of the telecom API market; Asia Pacific is forecast to expand at a 15.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Telecom API Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in CPaaS adoption among enterprises | +2.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Open Gateway and CAMARA standardization of network APIs | +3.1% | Global, led by Europe and Asia Pacific | Medium term (2-4 years) |

| Monetization pressure on 5G driving QoS-on-demand APIs | +2.5% | Asia Pacific, North America, Middle East early adopters | Long term (≥ 4 years) |

| Edge-computing workloads need low-latency slicing APIs | +2.2% | North America and Asia Pacific core, spillover to Europe | Long term (≥ 4 years) |

| Gen-AI–assisted developer tools lowering entry barriers | +1.9% | Global, with early gains in North America and Europe | Short term (≤ 2 years) |

| Telco-fintech push catalyzing carrier-billing and payment APIs | +2.4% | Africa, Asia Pacific, South America emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Open Gateway and CAMARA Standardization of Network APIs

The GSMA Open Gateway enrollment of 72 operator groups created a single federated catalog of number-verification, SIM-swap, device-location and quality-on-demand APIs, enforceable through OAuth 2.0 tokens.[1]GSMA Staff, “Open Gateway Initiative,” GSMA, gsma.com Enterprises once forced to negotiate fifteen bilateral contracts now integrate once, shrinking procurement cycles from quarters to weeks. Vodafone and Telefonica commercial launches in the United Kingdom, Brazil, Spain and Germany proved commercial feasibility and aligned API request-response syntax with hyperscaler conventions, lowering cognitive overhead for cloud-native developers.[2]Vodafone Group, “Press Release: Network API Marketplace,” vodafone.com ETSI GS OPG 002 rules formalized JSON Web Token security and RESTful design, helping regulators treat core network capabilities as essential digital facilities. Operators have consequently shifted from passive bandwidth wholesalers to active platform orchestrators able to charge per-transaction fees. Although revenue-share disputes with AWS and Microsoft persist, standardized APIs have removed the primary inhibitor to global scalability.

Surge in CPaaS Adoption among Enterprises

Twilio, Sinch, and Infobip reported combined 2024 revenue above USD 3.5 billion, indicating that enterprises gravitate toward programmable communications rather than monolithic voice and SMS bundles. Retailers using WhatsApp Business API now route 40% of customer-service interactions through asynchronous channels, lowering call-center handle time by 18 minutes and labor cost by USD 12 per ticket. Twilio’s Segment integration bridges customer-data graphs with programmable APIs, enabling abandoned-cart outreach within 90 seconds of checkout drop-off. Infobip’s generative-AI bots parse natural language to automatically invoke payment or location APIs, thereby widening access for non-specialist developers. As privacy regulations tighten, enterprises favor CPaaS providers that embed consent management and encryption in the API layer rather than bolt-on compliance.

Monetization Pressure on 5G Driving QoS-on-Demand APIs

Operators invested more than USD 1 trillion in 5G spectrum and hardware between 2019-2024, yet ARPU stagnated, spurring them to monetize network differentiation. Verizon’s 5G Edge with AWS Wavelength sells 20-millisecond latency guarantees at USD 0.08 per gigabyte, demonstrating premium pricing for ultra-low-latency workloads.[3]Verizon Business Team, “5G Edge with AWS Wavelength,” verizon.com SK Telecom’s factory-floor slices achieve 99.999% uptime, priced 40% above consumer tariffs. 3GPP Release 17 standardized lifecycle management for slice orchestration, enabling third-party platforms to automate provisioning via RESTful calls. Early pilots with Siemens reduced German automotive downtime by 15% when predictive-maintenance telemetry received QoS priority.

Telco-Fintech Push Catalyzing Carrier-Billing and Payment APIs

Mobile money registrations hit 1.74 billion by December 2024, positioning operators as de facto payment rails in low-bank-penetration regions. Vodafone M-Pesa merchant APIs circumvented average 2.5% card-network interchange, letting e-commerce sites debit airtime or wallets directly. Orange Money and Mastercard enabled 60-second cross-border remittances in West Africa, a 90% speed gain over correspondent banking. Nigeria’s Payment Service Banks rules and India’s Unified Payments Interface require ISO 20022-compliant APIs, further entrenching telcos in digital payment flows. Carrier billing for digital content reached USD 8 billion in operator revenue during 2024, aided by frictionless network-identity verification that lifts conversion in emerging markets.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating API-security breaches and signaling fraud | -1.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Legacy OSS and BSS upgrade bottlenecks | -2.1% | Global, severe in Tier-2 and Tier-3 operators | Long term (≥ 4 years) |

| Margin compression from OTT CPaaS competitors | -1.5% | North America and Europe, spillover to Asia Pacific | Medium term (2-4 years) |

| Unclear revenue-share models with hyperscalers | -1.3% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy OSS and BSS Upgrade Bottlenecks

Cloud-native API exposure demands real-time billing and policy engines, yet migrating monolithic systems costs USD 50-200 million and takes three-to-five years. SOAP-based interfaces cannot relay per-millisecond usage data required for dynamic network-slicing. Only 22% of the 150 operators that adopted TM Forum Open APIs achieved full compliance because decades-old custom code complicates refactoring. Regional carriers lacking capex rely on CPaaS aggregators, effectively ceding API monetization. Containerized BSS microservices from Nokia and Huawei allow phased migration, yet dual-stack operations raise opex by up to 25% during transition.

Escalating API-Security Breaches and Signaling Fraud

The January 2024 AT&T breach that exposed call and text metadata for 73 million customers showcased SS7 weaknesses dating to the 1970s. ENISA logged EUR 180 million in SS7-based fraud across the European Union in 2024. The Federal Communications Commission will require SS7 and Diameter encryption, anomaly detection and message filtering by Q2 2026, with USD 10 million penalties per incident. Misconfigured OAuth scopes on new APIs risk violating the General Data Protection Regulation, which allows fines up to 4% of global revenue. Only 38% of operators have implemented all GSMA security guidelines owing to legacy authentication constraints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Payment APIs Rise on Fintech Convergence

Payment APIs are set to rise at a 14.88% CAGR from 2026-2031, outpacing the telecom API market. Messaging retained 37.82% of the telecom API market share in 2025 because Apple adopted RCS in iOS 18, enabling rich media across iPhone-Android exchanges. Voice, WebRTC, and location services complement omnichannel commerce, while subscriber identity APIs eliminate SMS one-time-password friction, cutting onboarding time to 90 seconds in Southeast Asian banking pilots.

MTN Mobile Money’s 200 million accounts and Vodafone M-Pesa’s merchant APIs prove that bypassing card rails can slash costs and broaden ecommerce. Orange Money-Mastercard integration accelerated 60-second remittances, and carrier billing generated USD 8 billion in 2024 revenue, lifting digital-content conversions by 30% in emerging regions. Interoperability mandates, such as Nigeria’s PSB and India’s UPI, require alignment with ISO 20022, pushing operators to modernize their settlement systems. IoT connectivity and fraud-detection APIs address smaller niches but add cross-sell potential.

By Deployment Type: Multi-Cloud Architectures Gain Momentum

Hybrid deployments owned 56.82% of telecom API market size in 2025 as carriers kept core authentication on-premises while placing developer gateways in public clouds. Multi-cloud, however, will expand at a 15.34% CAGR as Kubernetes-based service meshes route traffic across AWS Wavelength, Azure for Operators and Google Distributed Cloud Edge, avoiding lock-in and optimizing latency.

Downtime risk also drives diversification; AWS logged 14 hours of outages in 2024. Red Hat OpenShift abstracts multicloud complexity, letting Deutsche Telekom push APIs to new regions in days. Gaia-X inspired European-hosted marketplaces for data sovereignty, yet developers still gravitate toward U.S. hyperscalers for tooling breadth. Private-cloud and fully on-prem solutions linger in defense, health and critical-infrastructure sectors bound by residency mandates, though FedRAMP and ISO 27001 certifications shrink these holdouts.

By End-User: Long-Tail Developers Accelerate Consumption

Partner developers held 38.2% telecom API market share in 2025, integrating messaging and payment APIs into third-party commerce and CRM platforms. GitHub Copilot, adopted by 55% of enterprise coders in 2024, shortens API onboarding to minutes, thereby expanding usage among long-tail developers forecast to grow at a 14.98% CAGR.

Low-code suites such as Microsoft Power Platform and OutSystems added connectors to CAMARA APIs, enabling business analysts to drag-and-drop location verification without writing code. Infobip’s conversational-AI interface further abstracts JSON marshalling, democratizing telecom network capabilities for small merchants in Southeast Asia and Latin America. Mandatory consent and encryption baked into these platforms reassure SMEs lacking in-house privacy counsel.

By Business Model: Marketplaces Disintermediate Aggregators

CPaaS aggregators still command 46.72% revenue, but new telecom API marketplaces will rise at a 15.22% CAGR as carriers federate catalogs and remove 30-50% aggregator tolls. The joint venture of Deutsche Telekom, Orange and Telefonica covers 284 networks with unified OAuth sign-on. Vodafone’s marketplace cut enterprise procurement from 12 weeks to 48 hours, showcasing self-service speed.

Hyperscalers introduced telecom-API gateways inside cloud consoles, though carriers resist 70-30 revenue splits favoring cloud vendors. Direct carrier exposure serves mega-clients needing bespoke pricing, while turnkey PaaS bundles from Ericsson Vonage attract operators lacking development staff by merging compute, analytics and APIs into one license. Regulatory designations of telecom APIs as essential facilities require non-discriminatory marketplace access, supporting smaller developers.

Geography Analysis

North America contributed 38.73% of telecom API market size in 2025. Verizon ThingSpace enrolled 15,000 enterprise developers, AT&T Live Video APIs underpinned telehealth sessions in 42 states and T-Mobile commercialized 5G standalone slices in 12 metropolitan areas. FCC security mandates, estimated at USD 2-5 million per network, also enhance API trustworthiness. Rogers and Bell joined Open Gateway, and América Móvil piloted carrier-billing APIs across Mexico to monetize the unbanked.

Asia Pacific is forecast to post a 15.32% CAGR through 2031. Reliance Jio’s 5G standalone base exceeded 100 million users by September 2024, its edge-computing APIs enable AR retail and real-time translation. China Mobile reached 500 million 5G connections and signed USD 1.2 billion in smart-city contracts to deploy network-slicing APIs for traffic control. India’s TRAI mandated transparent API rate cards, while Singtel and Maxis exposed location and QoS APIs to logistics providers in Southeast Asia. NTT Docomo and SK Telecom monetize factory automation slices priced 40% above consumer rates, and Samsung-powered edge nodes enable 12-millisecond latency gaming streams.

Europe balances regulation and innovation. GDPR and the Digital Markets Act obligate privacy-by-design and nondiscriminatory API access, respectively, standardizing trust frameworks while raising compliance overhead. The Deutsche Telekom-Orange-Telefonica-Vodafone marketplace aims to recapture margin from CPaaS aggregators. Vodafone United Kingdom’s launch allowed developers to provision CAMARA APIs within 48 hours. Middle East operators deploy payment APIs for expatriate remittances, processing USD 4 billion in 2024 transactions. Africa’s MTN generated significant wallet activity, and South America’s Telefonica Brasil exposed messaging and location APIs to agritech startups, highlighting regional diversification.

Competitive Landscape

The telecom API market remains moderately concentrated as the top five CPaaS providers account for the majority of aggregator revenue, while more than 200 regional players focus on niche verticals. Incumbent carriers, including AT&T, Verizon, Deutsche Telekom and Vodafone, are pivoting to direct developer marketplaces to reclaim margins historically lost to aggregators. Hyperscalers bundle telecom APIs into compute portals yet clash with operators over 70-30 revenue splits.

Vendor strategies emphasize vertical integration. Twilio’s USD 3.2 billion Segment deal fused customer-data graphs with programmable messaging, letting brands trigger contextual outreach in real time. Ericsson paid EUR 6.2 billion (USD 6.70 billion) for Vonage to connect 5G core sales with CPaaS capabilities. Telnyx and Bandwidth undercut legacy CPaaS rates by 20-40% via software-defined networking. Technology differentiation now centers on generative-AI orchestration, edge-compute provisioning and zero-trust security, each raising the bar for smaller entrants.

Technology differentiation centers on generative-AI integration; Infobip's conversational bots parse natural-language queries and invoke payment or location APIs without explicit developer scripting, lowering the skill threshold for long-tail developers in Southeast Asia and South America. Regulatory compliance frameworks such as the General Data Protection Regulation and ISO 27001 certification raise barriers to entry, as vendors must implement audit trails, consent management, and encryption that smaller startups struggle to finance, consolidating share among established players with dedicated compliance teams.

Telecom API Industry Leaders

AT&T Inc.

Telefónica SA

Twilio Inc.

Infobip Ltd

Sinch AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Deutsche Telekom, Orange, Telefonica and partners finalized a joint GSMA Open Gateway marketplace covering 284 networks.

- November 2025: Vodafone expanded its Network API Marketplace to Germany, Spain and Italy, attracting 1,200 developers in the first month.

- October 2025: Infobip introduced generative-AI conversational bots that auto-invoke messaging APIs for Southeast Asian merchants.

- September 2025: The FCC proposed mandatory SS7 and Diameter hardening rules with USD 10 million non-compliance penalties.

Global Telecom API Market Report Scope

Telecom API is a set of standard software functions that an application can utilize to operate the networking architecture. The API bridges the combination between the application and the resources across the device. Telecom APIs are the medium for accessing telecom services and data for multiple communication-enabled applications. Telecom providers are leveraging APIs to create differentiated offerings. APIs enable providers to combine their services and systems with third parties, opening up more rapid partnership opportunities that produce innovative, high-quality services. The telecom API market is segmented by type of service (messaging API, IVR/voice store and voice control API, payment API, webrtc [real-time connection] API, location and map API, subscriber identity management and SSP API, and other types of services), deployment type (hybrid, multi-cloud, and other deployment types), end user (enterprise developer, internal telecom developer, partner developer, long tail developer), geography (North America, Europe, Asia-Pacific [China, South Korea, Australia, New Zealand, India, Thailand, Singapore, Malaysia, Rest of Asia-Pacific], Latin America, and Middle East and Africa). The impact of macroeconomic trends on the market is also covered under the scope of the study. Further, factors affecting the market's evolution in the near future, such as drivers and constraints, have been covered in the study. The market sizes and predictions are provided in terms of value (USD) for all the above segments.

| Messaging / SMS-MMS-RCS API |

| Voice / IVR and Voice Control API |

| Payment API |

| WebRTC API |

| Location and Mapping API |

| Subscriber ID Management and SSO API |

| Other Service Types |

| Hybrid |

| Multi-cloud |

| Other Deployment Modes |

| Enterprise Developer |

| Internal Telecom Developer |

| Partner Developer |

| Long-tail Developer |

| Direct Carrier Exposure |

| Aggregator-led CPaaS |

| Platform-as-a-Service (PaaS) |

| API Marketplace / Exchange |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Messaging / SMS-MMS-RCS API | ||

| Voice / IVR and Voice Control API | |||

| Payment API | |||

| WebRTC API | |||

| Location and Mapping API | |||

| Subscriber ID Management and SSO API | |||

| Other Service Types | |||

| By Deployment Type | Hybrid | ||

| Multi-cloud | |||

| Other Deployment Modes | |||

| By End-User | Enterprise Developer | ||

| Internal Telecom Developer | |||

| Partner Developer | |||

| Long-tail Developer | |||

| By Business Model | Direct Carrier Exposure | ||

| Aggregator-led CPaaS | |||

| Platform-as-a-Service (PaaS) | |||

| API Marketplace / Exchange | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast value for the telecom API market in 2031?

The telecom API market is expected to reach USD 788.52 billion by 2031, rising at a 14.22% CAGR.

Which service type grows fastest through 2031?

Payment APIs post the highest growth, with a 14.88% CAGR fueled by telco-fintech convergence and carrier-billing expansion.

Why are multi-cloud deployments gaining momentum?

Operators adopt Kubernetes-based service meshes to avoid vendor lock-in, reduce outage risk and meet latency targets for edge workloads.

How do Open Gateway APIs benefit developers?

They provide a single OAuth credential that unlocks standardized network-verification, location and QoS functions across 284 carrier networks.

What security requirements must U.S. carriers meet by 2026?

The FCC plans to mandate SS7 and Diameter encryption, message filtering and anomaly detection, with fines up to USD 10 million per breach.

Page last updated on: