Global Tardive Dyskinesia Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

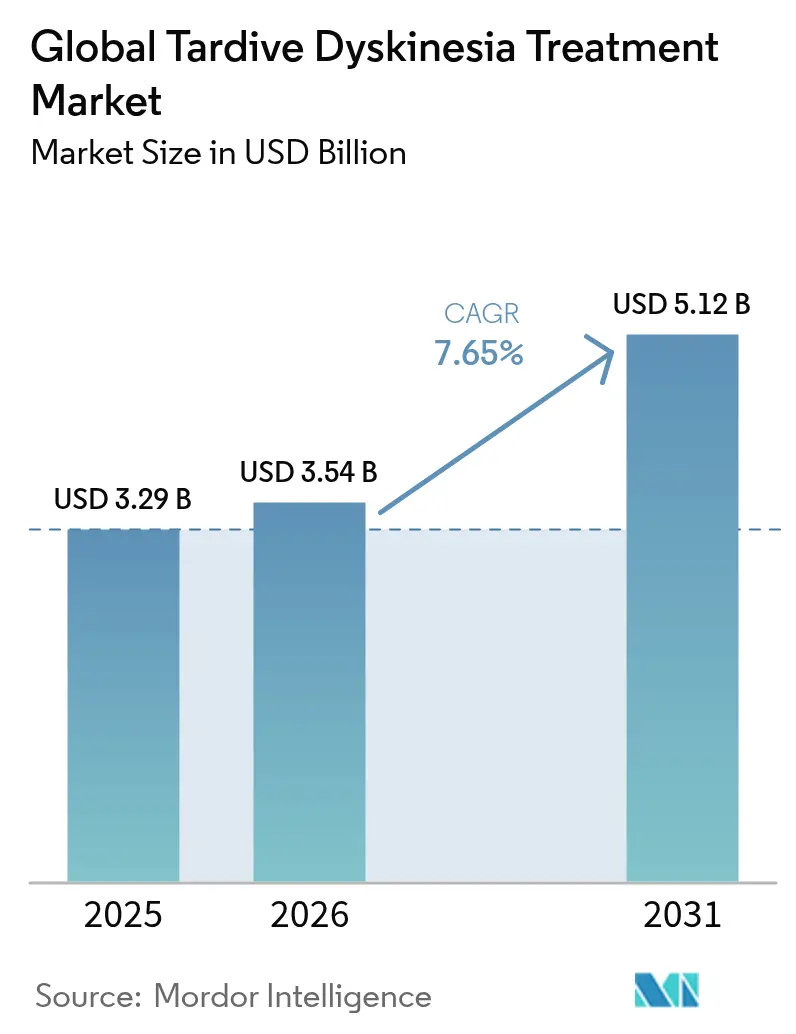

| Market Size (2026) | USD 3.54 Billion |

| Market Size (2031) | USD 5.12 Billion |

| Growth Rate (2026 - 2031) | 7.65% CAGR |

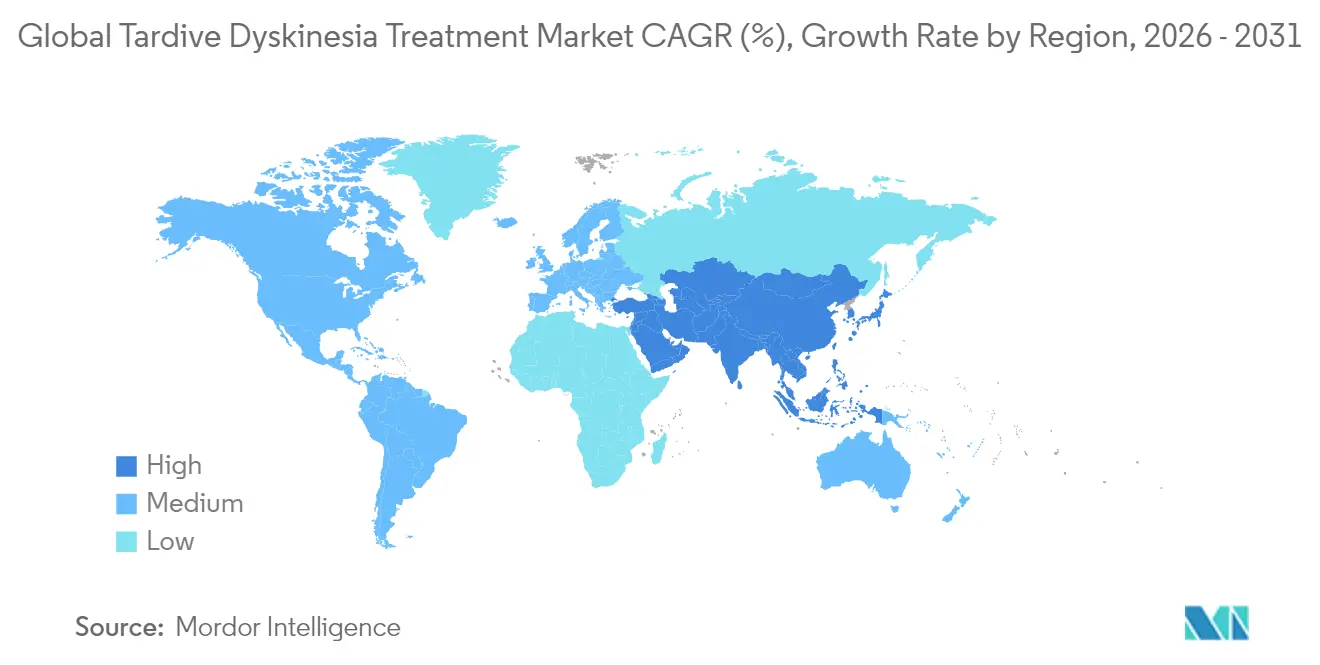

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Tardive Dyskinesia Treatment Market Analysis by Mordor Intelligence

The tardive dyskinesia treatment market size in 2026 is estimated at USD 3.54 billion, growing from 2025 value of USD 3.29 billion with 2031 projections showing USD 5.12 billion, growing at 7.65% CAGR over 2026-2031. Sustained growth springs from continued VMAT2 inhibitor uptake, expanding payer coverage, and systemic efforts to close the diagnostic gap that leaves 85% of affected patients without a formal diagnosis. Competitive intensity is rising as generic valbenazine launches in the United States while Asia-Pacific authorities add deutetrabenazine to essential-drug lists, hastening regional demand. Formulation innovation, notably Teva’s once-daily Austedo XR and Neurocrine’s Sprinkle capsules, improves adherence and widens candidate pools. The uptrend is further reinforced by digital phenotyping tools and AI-enabled screening platforms that reduce the median 5.5-year diagnostic lag.

Key Report Takeaways

- By drug class, VMAT2 inhibitors held 69.35% of the tardive dyskinesia treatment market share in 2025, while the “Others” segment is forecast to expand at 9.18% CAGR to 2031.

- By route of administration, oral products accounted for 59.45% share of the tardive dyskinesia treatment market size in 2025 and will expand at a 9.02% CAGR between 2026 and 2031 .

- By distribution channel, hospital pharmacies led with 53.30% of the tardive dyskinesia treatment market size in 2025, whereas online pharmacies are growing at 10.05% CAGR through 2031.

- North America contributed 41.70% of global revenue in 2025, but Asia-Pacific is the fastest-growing region at 10.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Global Tardive Dyskinesia Treatment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of antipsychotic-induced TD | +2.1% | Global | Medium term (2-4 years) |

| Approvals and reimbursement of VMAT2 inhibitors | +1.8% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Growing clinician awareness and screening mandates | +1.5% | Global, strongest in developed markets | Medium term (2-4 years) |

| Digital phenotyping tools enabling early diagnosis | +1.2% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Pipeline gene-expression modulators | +0.8% | Global, early focus North America | Long term (≥ 4 years) |

| Asia-Pacific essential-drug-list adoptions | +0.7% | APAC core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Antipsychotic-Induced TD

Global TD prevalence among antipsychotic users stands at 25.3%, with first-generation agents driving higher incidence than second-generation compounds. Pandemic-era telemedicine widened care access but masked subtle movement symptoms, reinforcing under-recognition challenges even as the at-risk population grew. Evidence from the IMPACT-TD study revealed a 5.5-year median diagnostic delay, underscoring a latent pool of untreated patients now reaching specialist care via mandated screening programs. The tardive dyskinesia treatment market consequently benefits from a steady flow of newly identified cases independent of fresh disease incidence.

Approvals & Reimbursement of VMAT2 Inhibitors

The American Psychiatric Association recommends VMAT2 inhibitors as first-line therapy for moderate-to-severe TD, cementing their role in clinical algorithms. Copay assistance keeps 90% of Austedo users’ out-of-pocket costs at USD 10 or less, stimulating adherence. Medicare price negotiations under the Inflation Reduction Act introduce looming margin pressure, yet enhanced formulations such as Austedo XR and Ingrezza Sprinkle widen clinical appeal. This blend of policy tailwinds and reimbursement uncertainty sparks strategic differentiation around dosing convenience and support services, sustaining growth but heightening competitive stakes.

Growing Clinician Awareness & Screening Mandates

The RE-KINECT study quantified quality-of-life burdens stemming from unrecognized TD and catalyzed hospital-based screening protocols. Smartphone video assessments and the Tardive Dyskinesia Impact Scale supply objective metrics that streamline case finding and monitoring. Expanded training for non-specialist physicians mitigates neurologist shortages, accelerating diagnosis in community settings. As a result, patient funnel conversion rises, reinforcing prescription volume for established VMAT2 inhibitors and supporting future entrants.

Digital Phenotyping Tools Enabling Early Dx

Machine-vision algorithms now analyze gait, speech, and hand kinetics captured via consumer devices, enabling decentralized TD screening. FDA guidelines for patient-focused digital health create a clear authorization pathway that encourages integration into routine psychiatric care. Early deployments suggest hybrid workflows where AI pre-screens and clinicians confirm, boosting diagnostic sensitivity without sacrificing oversight. These tools add a technology-driven growth layer to the tardive dyskinesia treatment market as payers recognize long-term cost savings from earlier intervention.

Restraints Impact Analysis of Global Tardive Dyskinesia Treatment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High drug costs & limited coverage in EMs | -1.4% | Emerging markets globally, with acute impact in Latin America & Africa | Medium term (2-4 years) |

| Safety-profile concerns (somnolence, QTc) | -0.9% | Global, with heightened scrutiny in EU regulatory environment | Short term (≤ 2 years) |

| EHR-coding & ethnic under-diagnosis gaps | -0.8% | Global, with pronounced impact in diverse urban centers | Medium term (2-4 years) |

| Shift toward non-dopaminergic psych meds | -0.6% | North America & EU core, gradual adoption in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Drug Costs & Limited Coverage in Emerging Markets

VMAT2 inhibitor list prices exceed many emerging-market reimbursement thresholds, dampening uptake despite rising clinical need. Specialty-pharmacy distribution forecloses generic substitution in most jurisdictions, tethering launch prices to U.S. benchmarks and constricting affordability. While patient-assistance programs bridge gaps, sustained manufacturer subsidies are necessary yet commercially unattractive in lower-income settings. Lupin’s generic valbenazine introduces a modest discount but still requires specialty handling, limiting broad-based price relief.

Safety-Profile Concerns (Somnolence, QTc)

Somnolence and QTc prolongation necessitate baseline and periodic monitoring, elevating treatment complexity in primary care and resource-constrained hospitals. The FDA boxed warning regarding depression and suicidal ideation compels psychiatric oversight, prompting cautious prescribing in multi-morbid populations. Interaction risks with CYP3A4 modulators further complicate medication management, potentially curbing expansion beyond specialist centers in the short run.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Global Tardive Dyskinesia Treatment Market Segment Analysis

By Disorder:

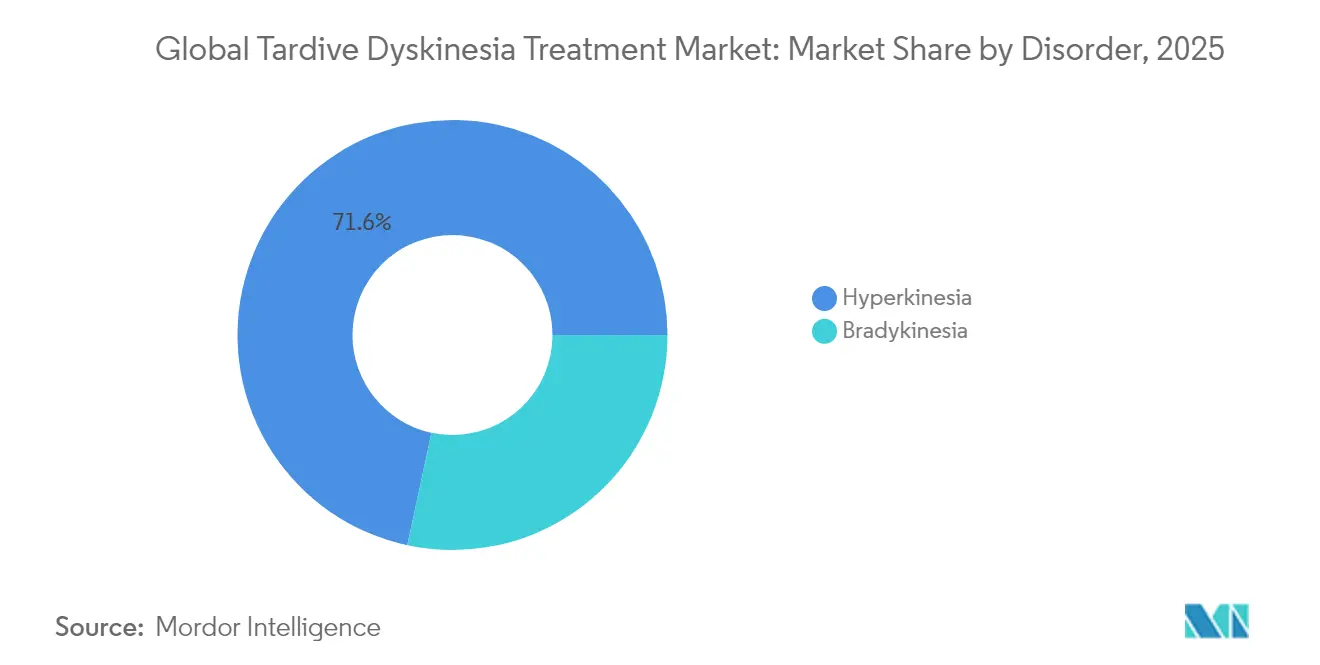

Hyperkinesia Drives Clinical InnovationHyperkinesia accounts for 71.63% of 2025 revenue and posts a 8.74% CAGR, underpinned by strong responsiveness to dopamine-depleting therapy. The tardive dyskinesia treatment market size for hyperkinetic presentations benefits from clear diagnostic criteria and objective movement-scale tools that enable timely intervention. Emerging gene-therapy research seeks durable modulation of dopaminergic signaling, aiming for disease modification rather than symptom suppression.

The hyperkinetic subtype’s predictability fosters prescriber confidence, reinforcing sustained demand. Bradykinesia remains clinically challenging since dopamine depletion can exacerbate symptoms, requiring nuanced dosing strategies. Nevertheless, real-world evidence from the KINECT-PRO study shows VMAT2 inhibitor benefits across psychiatric subgroups, encouraging broader adoption in mixed-phenotype patients.

By Drug Class:

VMAT2 Inhibitors Face Emerging CompetitionVMAT2 inhibitors captured 69.35% share in 2025 but confront brisk 9.18% CAGR growth in the “Others” category. Reformulated valbenazine and deutetrabenazine products sustain class leadership, yet non-dopaminergic agents such as TAAR1 agonists and glutamate modulators gather momentum.

Extended-release VMAT2 tablets ease adherence while gene-expression modulators target causal pathways, foreshadowing a shift from symptomatic to disease-altering strategies. Anticholinergic agents continue to fade, reflecting guideline contraindications and inferior risk-benefit profiles. The drug-class landscape therefore bifurcates into entrenched depletors versus innovative preventives, shaping future investment flows within the tardive dyskinesia treatment market.

By Route of Administration:

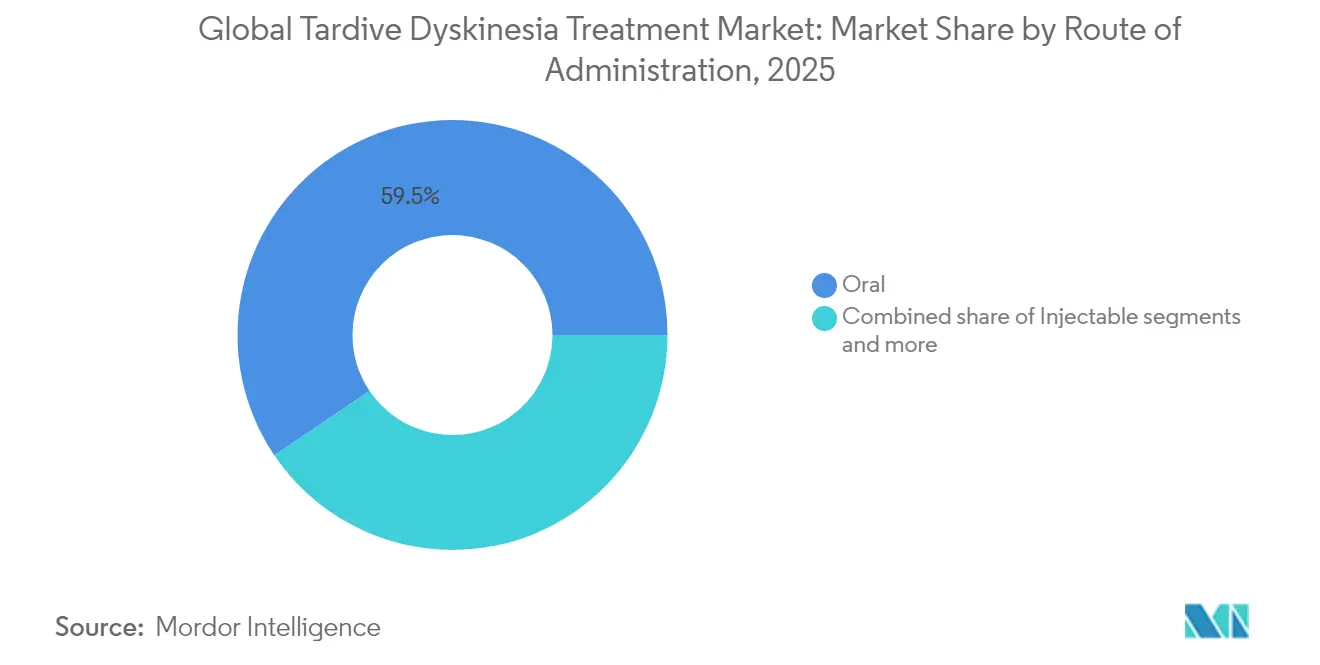

Oral Dominance Reinforced by InnovationOral formulations held 59.45% revenue in 2025 and will rise at 9.02% CAGR through 2031. The tardive dyskinesia treatment market size for oral products expands on the back of once-daily tablets and sprinkle capsules that address adherence and swallowing barriers.

Injectables remain niche, reserved for severe dysphagia cases, while pipeline transdermal systems aim to blend convenience with steady plasma levels. Digital adherence capsules—still investigational—could further entrench the oral route by integrating real-time ingestion tracking once regulatory pathways mature.

By Distribution Channel:

Specialty Pharmacy Model DominatesHospital pharmacies generated 53.30% of 2025 sales, reflecting initiation oversight needs, yet online pharmacies lead growth at 10.05% CAGR. The tardive dyskinesia treatment market size flowing through e-commerce channels benefits from telehealth expansion and direct-to-patient logistics that flourished during the pandemic.

Specialty pharmacies integrate nursing support, prior-authorization services, and adverse-event triage, adding value beyond mere dispensing. Retail outlets lag due to limited counseling capacity for complex neurologic therapies but may regain share if simplified formulations reduce monitoring burdens.

Geography Analysis

North America Tardive Dyskinesia Treatment Market

North America dominated with 41.70% share in 2025 thanks to FDA approvals, insurance penetration, and structured specialty-pharmacy networks. Sustained screening initiatives and payer support counterbalance looming Medicare price negotiations, sustaining volume momentum even as revenue per prescription moderates. Generic valbenazine’s April 2024 debut applies gentle price pressure but preserves specialist-channel margins due to distribution safeguards.

APAC Tardive Dyskinesia Treatment Market

Asia-Pacific races ahead at 10.41% CAGR, propelled by rising psychiatric drug usage and incremental policy wins such as Austedo’s China launch under the Teva–Jiangsu Nhwa alliance. Specialist shortages and out-of-pocket payment hurdles temper full-scale uptake, yet digital diagnostic tools bridge access gaps in markets like Japan and South Korea. Essential-drug-list additions and local manufacturing tie-ups could accelerate affordability, expanding the tardive dyskinesia treatment market base beyond premium urban centers.

EMEA and South America Tardive Dyskinesia Treatment Market

Europe delivers steady growth as HTA agencies demand cost-effectiveness evidence, nudging manufacturers toward patient-reported-outcome data and risk-sharing agreements. Safety scrutiny drives conservative prescribing, particularly around QTc monitoring, yet comprehensive insurance buffers patient affordability. South America and Middle East & Africa remain nascent, constrained by limited neurologist density and budget priorities, but represent upside for tiered-pricing models aligned with national income levels.

Regulatory Landscape

Regulatory landscape for tardive dyskinesia pharmacotherapy centers on VMAT2 inhibitors. In the United States, the FDA expanded labelable administration options with the April 2024 approval of Ingrezza Sprinkle (valbenazine) for adults with TD, expanding dosing flexibility and adherence options. In May 2024, the US FDA cleared Teva's Austedo XR (deutetrabenazine) for clinically therapeutic once-daily dosing, reinforcing formulation-led adherence strategies. In Europe, EMA activity in 2025 around deutetrabenazine (Austedo) informs national reimbursement and post-authorization pharmacovigilance requirements, while payer-led controls such as Department of Veterans Affairs formulary criteria shape real-world access alongside regulator approvals.

Value Chain Analysis

The tardive dyskinesia treatment value chain remains centered on branded VMAT2 inhibitors (valbenazine and deutetrabenazine), with commercialization anchored in regulatory-compliant manufacturing, specialized packaging networks, and rigorous pharmacovigilance oversight to support safety monitoring. Downstream, access and fulfillment rely on specialty pharmacy models with hub-based onboarding, prior authorization, and adherence support. Hospital pharmacies remain central for initiation and coordination of care, while online pharmacy growth aligns with telehealth-enabled follow-up within payer-network rules.

Competitive Landscape

Neurocrine and Teva together held roughly 85% share in 2024, translating into USD 3.9 billion combined sales. Ingrezza’s first-mover edge is reinforced by robust patient-support hubs, while Austedo capitalizes on once-daily dosing and expanding international reach. Formulation leap-frogging, not price cuts, remains the primary rivalry axis because specialty drug economics reward differentiation over discounting.

AbbVie’s USD 8.7 billion purchase of Cerevel Therapeutics injects fresh competition as tavapadon inches closer to TD trials, potentially introducing a new mechanism with less dopaminergic liability. Lupin’s generic entry opens the first budget alternative yet retains specialty-channel premiums, softening but not dismantling incumbent pricing power. Longer term, gene-therapy pioneers could upend the landscape if disease-modifying efficacy translates from Parkinson’s models to tardive dyskinesia.

Global Tardive Dyskinesia Treatment Industry Leaders

Neurocrine Biosciences, Inc

Teva Pharmaceutical Industries Ltd

Sun Pharmaceutical Industries Ltd

SteriMax Inc.

Lannett Co Inc

- *Disclaimer: Major Players sorted in no particular order

Global Tardive Dyskinesia Treatment Market Companies Covered in this Report

- Neurocrine Biosciences

- Teva Pharmaceutical Industries

- H. Lundbeck

- Supernus Pharmaceuticals*

- Sun Pharmaceuticals Industries

- Zydus Lifesciences

- Sandoz Group

- Adamas Pharma (legacy)

- Alkermes

- Cerevel Therapeutics

- Supernus Pharmaceuticals

- Acorda Therapeutics

- Enterin Inc.

- Theravance Biopharma

- Voyager Therapeutics

Read Analysis of Global Tardive Dyskinesia Treatment Companies

Market Opportunities and Future Outlook

A primary whitespace is diagnosis-to-treatment conversion, given a large under-diagnosed pool and diagnostic lag that limit timely initiation. Digital tools such as digital phenotyping and smartphone video assessments align with this gap, and regulatory clarity for patient-focused digital health tools creates a pathway for integration into psychiatric workflows where TD is often first observed. Evidence from 2024 approvals demonstrates practical expansion of eligibility through formulation variants such as Ingrezza Sprinkle and Austedo XR. The large under-diagnosed pool highlighted in-market and the ongoing development of next-generation options, including the January 2026 Phase 2 study of NBI-1065890 in adults with TD, illustrate ongoing investment in differentiated efficacy, tolerability, or durability beyond the core VMAT2 inhibitor franchises.

Recent Industry Developments in Global Tardive Dyskinesia Treatment Market

- June 2026: Teva presented new long-term clinical data on AUSTEDO and AUSTEDO XR at Psych Congress Elevate (June 3-6, 2026), highlighting outcomes relevant to symptom control in tardive dyskinesia. The update supports lifecycle value messaging for once-daily dosing and can strengthen payer and prescriber confidence in persistence-focused positioning.

- February 2025: Neurocrine reported positive quality-of-life findings from the KINECT-PRO Phase 4 study of Ingrezza (valbenazine). The readout adds real-world oriented evidence that supports differentiation beyond symptom score changes and reinforces the role of patient-reported outcomes in access discussions.

- May 2024: The US FDA approved Teva's AUSTEDO XR (deutetrabenazine) extended-release tablets as a one-pill, once-daily option for clinically therapeutic doses for tardive dyskinesia. The approval expanded available strengths (30, 36, 42, and 48 mg) and raised the competitive bar around adherence-centric formulation design within the VMAT2 inhibitor class.

Global Tardive Dyskinesia Treatment Market Report Scope and Research Methodology

Market Definition and Coverage

This market is defined as the revenue generated from therapies used to manage tardive dyskinesia, including prescription drug options used in routine clinical practice, across major care settings and geographies.

Scope exclusions: We exclude non-therapeutic wellness products and general neurology visits that are not linked to a tardive dyskinesia treatment decision.

Segments Covered in This Report

- By Disorder

- Bradykinesia

- Hyperkinesia

- By Drug Class

- VMAT2 Inhibitors

- Dopamine-Depleting Agents (non-VMAT2)

- Anticholinergics & Others

- By Route of Administration

- Oral

- Injectable

- Others

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the disease and treatment context, form realistic assumptions, and set guardrails for the model before interviews began. Public sources such as the US FDA label and safety communications, CDC and NIH background statistics, Centers for Medicare and Medicaid Services signals on access, and published articles indexed in PubMed helped us understand diagnosis patterns, switching behavior, and therapy persistence.

We also reviewed company annual reports, investor presentations, earnings transcripts, and credible healthcare press to track launches, label updates, and payer coverage shifts that can move demand quickly. When needed, we referenced paid database subscriptions for company financials and intelligence, and for patent databases to cross-check pipeline and formulation activity. The desk research sources listed here are not exhaustive, and additional public and paid references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on specialists involved in tardive dyskinesia management and stakeholders linked to treatment access, including prescribers, pharmacy channel participants, and market access roles. Since this is a global market, views were balanced across mature and emerging regions so assumptions on diagnosis uplift, adherence, and payer restrictions could be tested, then adjusted where regional practice differed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | APAC: 44% |

| Mid tier: 45% | Functional/Unit leaders: 38% | EMEA: 37% |

| Smaller Players: 17% | Managers: 48% | Americas: 19% |

Market-Sizing & Forecasting

The sizing model starts with a top-down demand pool build-up where treated patient counts are reconstructed from disease prevalence signals, diagnosis rates, and the share of patients that persist on therapy, then translated into annual revenues using therapy mix and average annual cost assumptions. To keep the outcome grounded, we corroborate results with selective bottom-up approximations, such as sampled price levels from public references, channel mix checks, and supplier-side sanity checks on exposure to this indication.

Inputs that materially move the numbers include VMAT2 inhibitor uptake within eligible patients, diagnosis and screening intensity in psychiatric care, prior authorization tightness and reimbursement breadth, therapy duration and discontinuation, and the shift between hospital, retail, and online pharmacy dispensing. Forecasts were extended using scenario analysis, where the base case is guided by expert consensus on diagnosis improvement, access changes, and competitive dynamics, then stress-tested for slower diagnosis conversion or faster adoption. When bottom-up visibility is limited in smaller countries, gaps are handled through region-level proxies that are scaled using population and healthcare access indicators, and then reviewed in follow-up calls.

Data Validation & Update Cycle

Outputs are validated through stepwise checks that compare implied treated patients, therapy mix, and pricing levels against independent clinical and access signals. Variances are investigated, assumptions are revisited, and any material mismatch triggers re-contact with selected respondents so the logic can be corrected before sign-off.

A multi-step analyst review is followed to catch calculation errors and inconsistent definitions early, and the final dataset is checked again right before delivery. Reports are refreshed annually, with interim updates when major events occur, such as label changes, meaningful pricing moves, or payer policy shifts that can change utilization in a short period.

Mordor Intelligence's Tardive Dyskinesia Treatment Market Size Measured Against Other Published Estimates

Published market sizes for tardive dyskinesia treatment can vary quite a bit, even when the same end condition is being discussed, because the counted therapies and the timing of the base year are not always aligned. Differences also come from how each model converts diagnosis into treated patients and then translates treatment mix into revenue.

By tracking treated patient progression, therapy duration, and the pharmacy channel mix, Mordor Intelligence keeps the estimate tied to what is actually treated in routine care, instead of blending in adjacent movement disorder care or loosely defined surgery revenue, which can widen totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.54 B (2026) | |

| Global Consultancy A | USD 3.88 B (2024) | Uses an earlier base year and a broader treatment bucket that explicitly includes surgery and a wider list of non-core options, which can lift totals when combined with generalized uptake assumptions. |

| Industry Publisher B | USD 3.60 B (2024) | Anchors the model on a 2024 base and groups the market mainly by a few branded drug categories, which can understate therapy mix shifts and channel effects when access and persistence change by region. |

The spread mainly reflects what gets counted as a tardive dyskinesia treatment and how the treated pool is constructed from diagnosis to ongoing therapy. Using clear inclusion rules and repeatable demand and pricing checks helps keep the market size traceable to practical variables that can be verified and updated each year.

Key Questions Answered in the Report

What is the current value of the tardive dyskinesia treatment market?

The global tardive dyskinesia treatment market is valued at USD 3.54 billion in 2026

Which segment holds the largest share of the tardive dyskinesia treatment market?

Hyperkinesia dominates with a 71.63% share in 2025

What is the expected growth rate of VMAT2 inhibitors?

VMAT2 inhibitors are projected to grow in line with the overall 7.65% CAGR, maintaining leadership while facing competition from novel mechanisms

Why is Asia-Pacific the fastest-growing region?

Rapid regulatory approvals, rising antipsychotic use, and partnerships such as Teva’s deal with Jiangsu Nhwa drive Asia-Pacific’s 10.41% CAGR

Page last updated on: