Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 15.04 Billion |

| Market Size (2026) | USD 15.61 Billion |

| Market Size (2031) | USD 18.57 Billion |

| Growth Rate (2026 - 2031) | 3.53% CAGR |

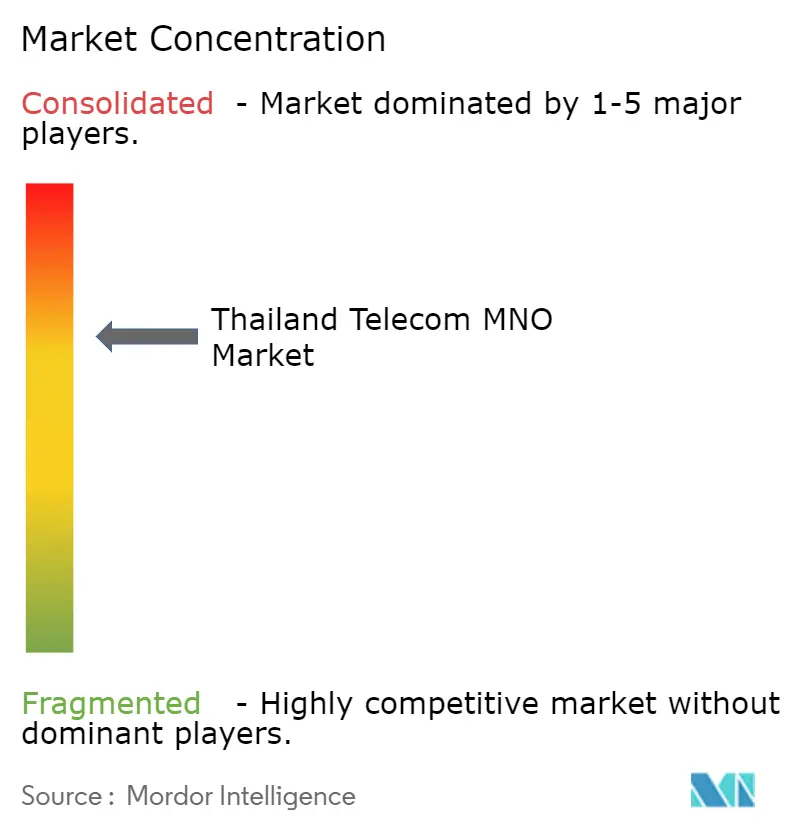

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Telecom MNO Market Analysis by Mordor Intelligence

The Thailand telecom MNO market size is projected to expand from USD 15.04 billion in 2025 and USD 15.61 billion in 2026 to USD 18.57 billion by 2031, registering a CAGR of 3.53% between 2026 and 2031. Voice services continue to decline, yet data monetization, enterprise 5G solutions, and inbound roaming packages are generating fresh revenue streams that moderate the topline drag. Operators are streamlining cost structures through tower consolidation and dynamic spectrum sharing, but capital intensity remains high because world-leading license fees and rural coverage targets still demand fresh spectrum purchases. The March 2023 True-dtac merger left the market with two private players and one state-owned challenger, amplifying price competition even as it improved spectrum depth. OTT traffic, 5G-enabled industrial automation, and digital-government services together underpin the next wave of subscriber value, while regulatory clarity on upcoming 850 MHz and 2100 MHz auctions will shape long-term network economics.

Key Report Takeaways

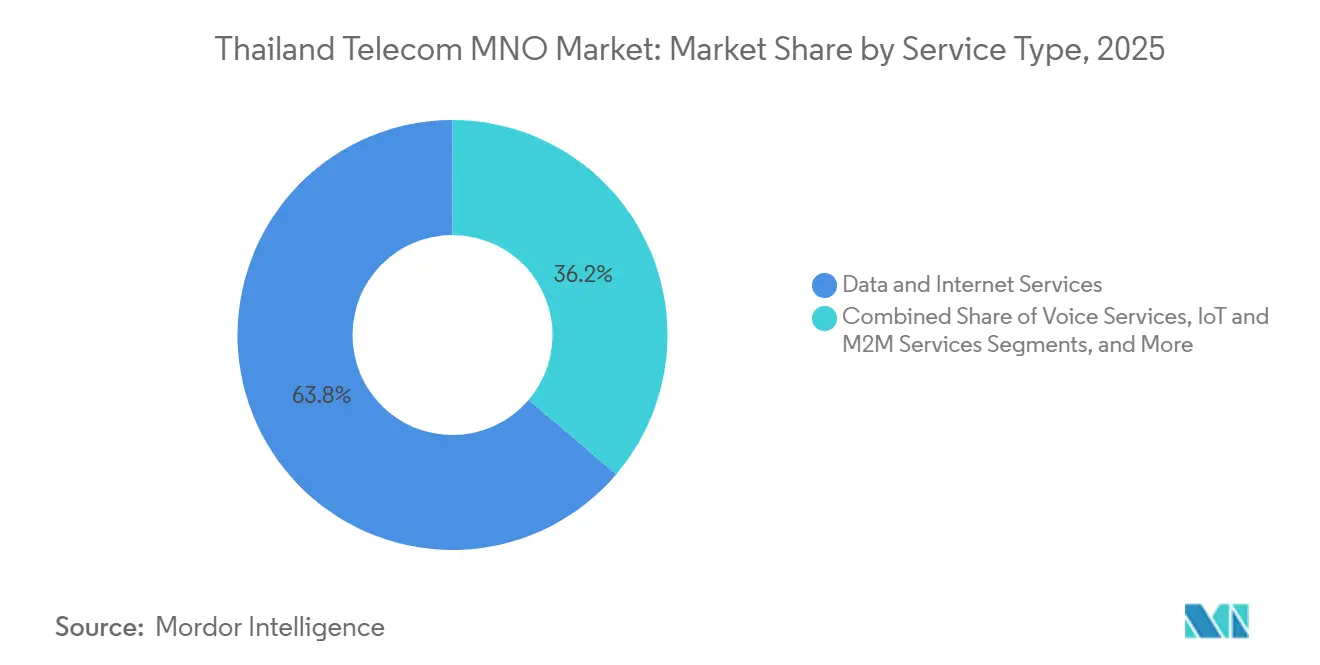

- By service type, data and internet services held 63.78% of Thailand telecom MNO market share in 2025, while IoT and M2M services are projected to advance at a 3.72% CAGR through 2031.

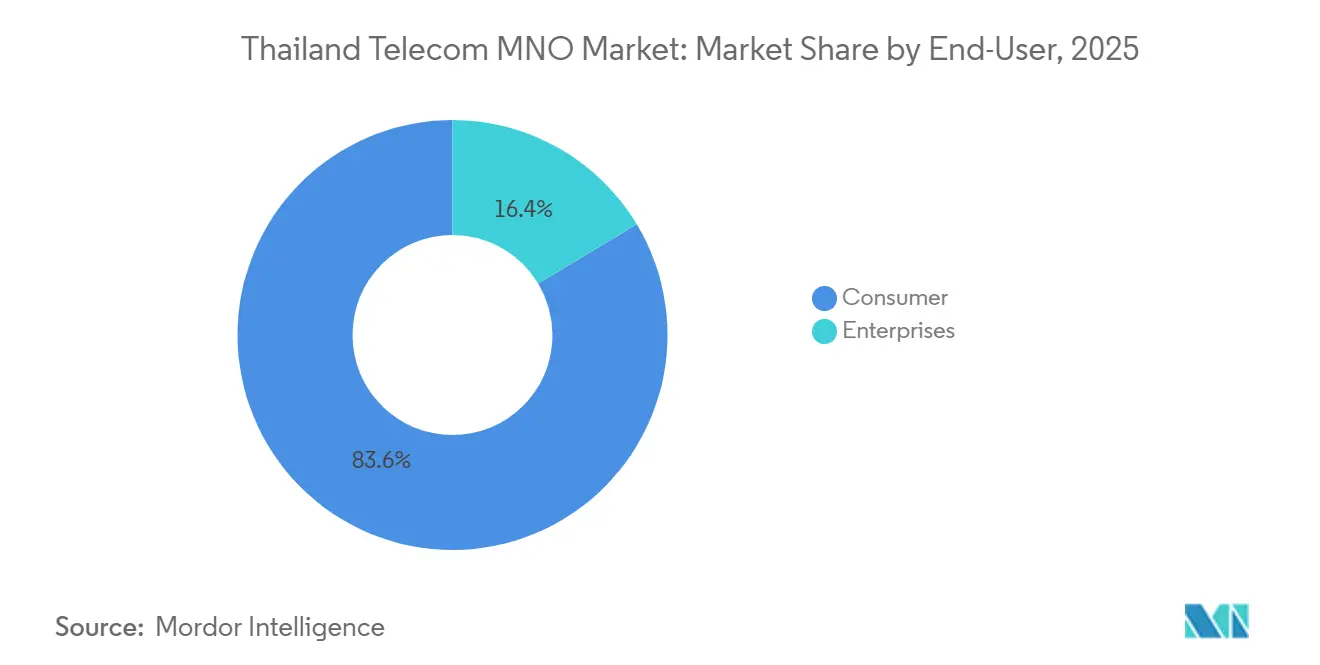

- By end-user, the consumer segment contributed 83.62% of 2025 revenue, yet the enterprise segment is forecast to expand at a 4.01% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide 5G rollout accelerating mobile data monetization | +1.2% | National, early gains in Bangkok, Chiang Mai, Phuket | Medium term (2-4 years) |

| Explosion in OTT video and gaming traffic driving ARPU uplift | +0.9% | National, concentrated in urban centers and tourist zones | Short term (≤ 2 years) |

| Enterprise digital-transformation boosting private-LTE and 5G SA demand | +0.8% | Industrial estates in Rayong, Chonburi, Samut Prakan | Medium term (2-4 years) |

| Soaring smartphone penetration in rural provinces | +0.6% | Northeastern and Northern provinces | Long term (≥ 4 years) |

| Rapid adoption of eSIM tourist packages increasing inbound roaming revenues | +0.4% | Phuket, Pattaya, Koh Samui, Bangkok | Short term (≤ 2 years) |

| NB-IoT smart-agriculture pilots backed by government grants | +0.3% | Nakhon Ratchasima, Ubon Ratchathani | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nationwide 5G Rollout Accelerating Mobile Data Monetization

Thailand’s three operators pushed 5G population coverage above 95% by December 2025, turning the country into one of only seven Asia-Pacific markets with a live standalone 5G core. AIS tested a quality-of-service add-on that lifted monthly spend per participating user by 22%, proving that tiered speed plans can offset the flattening of headline tariffs.[1]Advanced Info Service, “Q3 2025 Financial Results,” ais.co.th True consolidated more than 100,000 towers under its One Network program, then activated dynamic spectrum sharing on 2600 MHz to cut gigabyte delivery costs and free capacity for premium plans. Operators have spent roughly THB 500 billion (USD 15.6 billion) on 3G, 4G, and 5G spectrum since 2012, so each additional megabit now needs a clear revenue path. The early success of higher-priced 5G tiers suggests that coverage leadership will convert into margin defense as traffic climbs.

Explosion in OTT Video and Gaming Traffic Driving ARPU Uplift

Average mobile data use per Thai smartphone rose from 13 GB a month in 2023 toward a Southeast Asian trajectory of 59 GB by 2030, pushed by Netflix, Disney+, and TrueID securing exclusive local content.[2]GSMA Intelligence, “Mobile Economy Asia Pacific 2024,” gsmaintelligence.com Video now accounts for more than 70% of downstream traffic on AIS and True networks, prompting both to invest in edge caching that shortens start times and limits backhaul strain. Operators bundle unlimited plans with speed tiers rather than strict caps, letting heavy streamers pay more for guaranteed throughput during primetime. Sponsored-data deals also surface, such as True’s tourism bundle that paired roaming eSIMs with free streaming trials for 9.3 million visitors in Q1 2024. As ad-supported mobile video spending rises, carriers gain an indirect share by selling prioritized network slices to content platforms.

Enterprise Digital-Transformation Boosting Private-LTE and 5G SA Demand

The regulator cleared 4800-4900 MHz for private 5G, letting factories deploy on-premises wireless without relying on public cores.[3]National Broadcasting and Telecommunications Commission, “Spectrum Allocation Notice 2024,” nbtc.go.th NTT and Nokia immediately targeted the 3.2 million Thai businesses that need deterministic latency for machine vision and automated guided vehicles. In February 2026, TrueBusiness and SoftBank began bundling AI analytics with managed 5G to address predictive maintenance and real-time quality control in automotive plants. AIS validated Reduced Capability (RedCap) devices that lower module prices for wearables and industrial sensors, broadening the addressable device pool. Early pilots show throughput gains of 40-60 Mbps with sub-10 millisecond latency, confirming that enterprise demand can diversify revenue away from saturated consumer segments.

Soaring Smartphone Penetration in Rural Provinces

National smartphone ownership reached about 85% in 2025, yet Northeastern and Northern provinces still trail Bangkok’s 95-plus percent penetration.[4]Ministry of Digital Economy and Society, “Digital Economy and Society Statistics 2025,” mdes.go.th Universal Service Obligation rules now link license renewals to rural milestones, so operators partner with village chiefs and farm co-ops to sell bundles that include 4G handsets priced below THB 3,000 (USD 94). AIS and True deploy mobile agents who teach digital-literacy basics and activate SIMs on-site, converting first-time internet users into recurring data subscribers. Government e-wallets and telehealth apps further anchor usage, turning connectivity into a utility rather than a discretionary expense. As coverage gaps close, rural data volume is projected to grow faster than urban traffic, extending the market’s long-tail growth curve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| World-leading spectrum license fees straining operator balance sheets | -0.9% | National, policy set by NBTC | Long term (≥ 4 years) |

| Intensifying price wars following True-dtac merger remedies | -0.7% | National, prepaid and unlimited-data segments | Medium term (2–4 years) |

| Delay in location-based emergency number routing regulation | -0.2% | Tourist and heritage zones | Short term (≤ 2 years) |

| Municipal opposition to small-cell street furniture in heritage zones | -0.1% | Bangkok, Chiang Mai, Ayutthaya | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

World-Leading Spectrum License Fees Straining Operator Balance Sheets

Thailand’s spectrum cost-to-revenue ratio jumped from 2% in 2014 to 16% in 2023, making local licenses the most expensive worldwide on a per-MHz basis. The June 2025 auction forced AIS and True to spend THB 41 billion (USD 1.26 billion) for mid-band blocks, yet the 850 MHz lots went unsold because reserve prices exceeded operators’ debt capacity. True’s long-term borrowings ballooned to THB 339.66 billion (USD 10.5 billion), while National Telecom slid into loss after its lucrative wholesale deals expired. Empirical GSMA studies tie a 10-percentage-point rise in spectrum fees to 6-percentage-point lower 5G coverage, hinting that Thailand’s pricing model risks underfunding rural roll-outs. Unless reserve prices soften, network densification may slow despite surging traffic.

Intensifying Price Wars Following True-dtac Merger Remedies

Regulatory conditions attached to the March 2023 merger banned lock-in contracts and capped some wholesale rates, triggering a race to launch unlimited data plans that pushed blended ARPU from THB 235.5 (USD 7.3) in 2021 to THB 217.4 (USD 6.7) in 2023. AIS prepaid users now spend about THB 125 a month, while True’s prepaid base lingers near THB 103 (USD 3.2), leaving scant headroom to fund new capacity. Operators hope quality-of-service tiers will restore pricing power, yet AIS drew only 180,000 sign-ups to its paid 5G Mode option by February 2025. Churn remains volatile because number portability is free and SIM cards cost under THB 50 (USD 1.5) at convenience stores. Sustained margin compression may deter investment in off-grid rural sites and niche enterprise solutions that need long payback horizons.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Revenues Eclipse Voice Decline

Data and internet services captured 63.78% of 2025 operator revenue, giving the category the single-largest Thailand telecom MNO market share among all service lines. Voice and messaging continued to retreat as LINE, WhatsApp, and Facebook Messenger displaced circuit-switched calling, prompting operators to roll unlimited minutes into every data bundle so customers perceive calls as “free” add-ons. OTT and pay-TV subscriptions added incremental value; TrueID led local streaming sign-ups, while Netflix and Disney+ relied on telco billing deals that improve conversion among prepaid users.

Momentum now rests with IoT and M2M connectivity, forecast to expand at a 3.72% CAGR through 2031 after the regulator released 4800-4900 MHz for private enterprise networks. Manufacturing plants in Rayong and Chonburi have already installed on-premises 5G to link automated guided vehicles and quality-control cameras, while agriculture pilots in Ubon Ratchathani use narrowband IoT sensors for soil-moisture alerts. Operators are testing GSMA Open Gateway APIs that expose SIM-swap detection and number verification, signalling a shift toward platform revenues rather than pure transport fees. Even small tourist SIM packs now come with bundled video passes, proving that content partnerships can offset traffic costs by lifting average spend without raising headline tariffs.

By End-User: Enterprise Upswing Counters Consumer Saturation

Consumers produced 83.62% of 2025 revenue, yet enterprises are expected to grow at a 4.01% CAGR to 2031, positioning them as the fastest path to expand Thailand telecom MNO market size over the forecast horizon. Urban postpaid subscribers already average THB 416-446 (USD 13.7-12.8) in monthly spend, so incremental gains depend on premium 5G tiers that guarantee throughput during video streaming or mobile gaming peaks.

Enterprise demand is broadening as factories seek deterministic latency for machine vision and predictive maintenance; the February 2026 TrueBusiness-SoftBank alliance packages AI analytics with private 5G cores to serve that need. NTT and Nokia target 3.2 million Thai companies with managed spectrum and edge-cloud hosting, while AIS validated RedCap devices that lower the hardware cost for wearables and smart meters. National Telecom is chasing THB 10 billion (USD 308 million) in cloud revenue by 2027 to replace lost wholesale earnings, showing how every player is racing to bundle connectivity with software, storage, and security services. Early wins are surfacing in industrial estates, where private-network pilots already support autonomous forklifts and high-definition video inspection lines that were impossible on Wi-Fi alone.

Geography Analysis

Bangkok and its adjoining provinces account for the highest traffic density and record 5G coverage of 95-99%, making the capital the anchor that underwrites Provincial regions average 80-85%, constrained by affordability and patchy 4G backhaul. Thailand telecom MNO market size growth each year. Average revenue per user there tops THB 400 (USD 12.3) because subscribers readily pay for speed-tier plans, cloud gaming passes, and enterprise VPN add-ons.

Tourist destinations, Phuket, Pattaya, Koh Samui, and Krabi, punch above their population weight thanks to inbound roaming and eSIM onboarding; True’s partnership with the Tourism Authority delivered 65% penetration among 9.3 million visitors in Q1 2024. These regions also hosted Thailand’s first live cell-broadcast alerts, though engineers still grapple with a 200,000-device batch limit that must scale before nationwide roll-out. The Eastern Economic Corridor, covering Rayong, Chonburi, and Samut Prakan, attracts private 5G licenses for automotive welding robots and petrochemical safety monitoring, converting factory estates into steady high-margin enterprise accounts.

Rural Northeastern and Northern provinces remain the coverage frontier, with smartphone penetration near 80-85% and spotty 4G backhaul that suppresses data-plan usage. Universal Service Obligation funds now tie license renewals to remote-village milestones, pushing AIS and True to train village-level agents who sell bundles with discounted Chinese 4G handsets priced below THB 3,000 (USD 94). However, municipal heritage boards in Bangkok, Chiang Mai, and Ayutthaya still block small-cell poles that clash with historic aesthetics, delaying dense millimeter-wave deployment essential for indoor 5G in temples, museums, and colonial shopfronts.

Competitive Landscape

Advanced Info Service and True Corporation now control an estimated 90% of total revenue, giving them dominant scale yet exposing each to direct pricing stare-downs that keep prepaid ARPU near THB 100 (USD 3.1). AIS leans on Gulf Energy and Singtel to finance spectrum and tower upgrades, while also investing up to THB 8 billion (USD 0.25 billion) with Oracle Alloy to run Thailand’s first home-grown hyperscale cloud from Q1 2025, positioning the operator as a hybrid-cloud integrator for banks and state agencies.

True’s January 2026 ownership reshuffle saw Arise Digital Technology acquire Telenor’s 24.95% stake for THB 100 billion (USD 3.1 billion), freeing management to accelerate debt reduction and dividend restoration while deepening its Ascend Money fintech ecosystem that serves 34 million wallets. The company finished its One Network tower merger in October 2025, enabling dynamic spectrum sharing on 2600 MHz that cuts cost per gigabyte by double digits and opens room for 5G-exclusive speed tiers.

National Telecom, formed from TOT and CAT, lost two profitable spectrum partnerships in September 2025, slipping into net loss but still controlling a nationwide fiber backbone and the 126°E orbital slot it won in 2023 for future LEO services. The state carrier is courting AIS, True, and foreign vendors for joint ventures that could monetize stranded 700 MHz and satellite assets without heavy capex. Meanwhile, NTT-Nokia private-network sales, Thaicom-Globalstar LEO backhaul, and a looming June 2026 auction of 850 MHz, 2100 MHz, and 2300 MHz spectrum ensure competitive intrigue remains high even within a duopoly structure.

Thailand Telecom MNO Industry Leaders

Advanced Info Service (AIS)

True Corporation Public Company Limited

National Telecom (NT)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: TrueBusiness and SoftBank announced a partnership to deliver AI and 5G solutions for Thai enterprises, targeting manufacturing, logistics, and retail.

- February 2026: The NBTC said draft rules for the 850 MHz, 2100 MHz, and 2300 MHz auctions will be completed by June 2026.

- January 2026: Arise Digital Technology bought Telenor’s 24.95% stake in True Corporation for THB 100 billion (USD 3.1 billion).

- January 2026: Arise and True set a plan to cut net debt-to-EBITDA to 3.2× by 2027 and raise the dividend payout ratio to at least 50%.

Thailand Telecom MNO Market Report Scope

Telecom or Telecommunication is the long-range transmission of information by electromagnetic means. The Telecom MNO Market includes in-depth trend analysis based on connectivity like Fixed Networks, Mobile Networks, and Telecom Towers.

The Thailand Telecom MNO Market Report is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, IoT and M2M Services, OTT and PayTV Services, and Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, Rest of Service Type)), End-User (Enterprises, and Consumer), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services, Value-Added and Wholesale Services |

End-User

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services, Value-Added and Wholesale Services | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large will Thailand telecom MNO market be in 2031?

It is forecast to reach USD 18.57 billion by 2031, expanding at a 3.53% CAGR from 2026.

Which service type is growing fastest?

IoT and M2M services show the highest momentum, projected at a 3.72% CAGR through 2031.

Who holds the biggest share among operators?

Advanced Info Service captured about 49% of mobile revenue at end-2024.

Why are spectrum costs considered a restraint?

License fees consume 16% of operator revenue, limiting funds for rural 5G rollout.

What opportunity exists for enterprises?

Private 5G in industrial estates offers low-latency connectivity for automation and AI workloads.

How is tourism influencing revenue?

ESIM tourist packages drive inbound roaming, with True onboarding 65% of Q1 2024 visitors.

Page last updated on: