Switzerland Used Car Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 25.69 Billion |

| Market Size (2026) | USD 26.48 Billion |

| Market Size (2031) | USD 30.82 Billion |

| Growth Rate (2026 - 2031) | 3.08% CAGR |

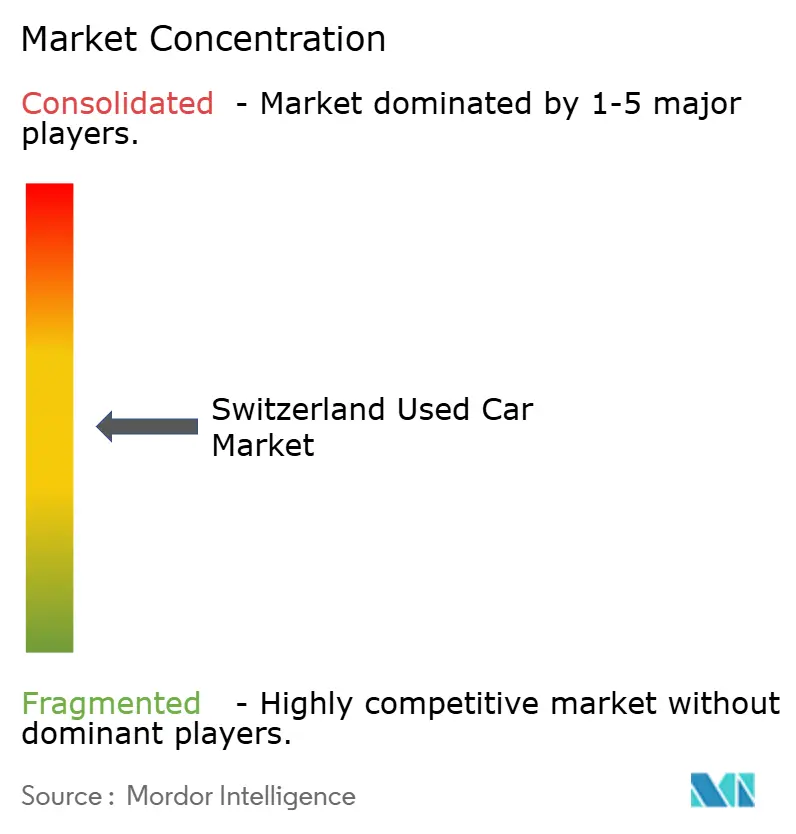

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Switzerland Used Car Market Analysis by Mordor Intelligence

The Switzerland used car market size is expected to grow from USD 25.69 billion in 2025 to USD 26.48 billion in 2026 and is forecast to reach USD 30.82 billion by 2031 at a 3.08% CAGR over 2026-2031. Cost-sensitive buyers are turning away from new models as transaction prices rise faster than disposable incomes, and digital platforms now enable cross-canton discovery and transparent pricing. A record low of 233,744 new-car registrations in 2025 redirected demand toward the secondary channel, lifting the average vehicle age to over 10 years[1]"New Registrations Switzerland 2025: Which Brands and Models Lead?", autoweg, autoweg.ch. Buyers increasingly value bundled warranties, inspection reports, and instant financing, so organized dealers and subscription providers are formalizing what was once a largely informal marketplace. Electrification is reshaping supply: near-new battery-electric vehicles from corporate fleets are enlarging inventory. At the same time, Chinese brands entering in 2026 will broaden the choice of affordable EVs by the end of this decade. Competitive strategies now revolve around owning the customer interface, controlling proprietary digital channels, and leveraging captive financing to lock in recurring revenue streams.

Key Report Takeaways

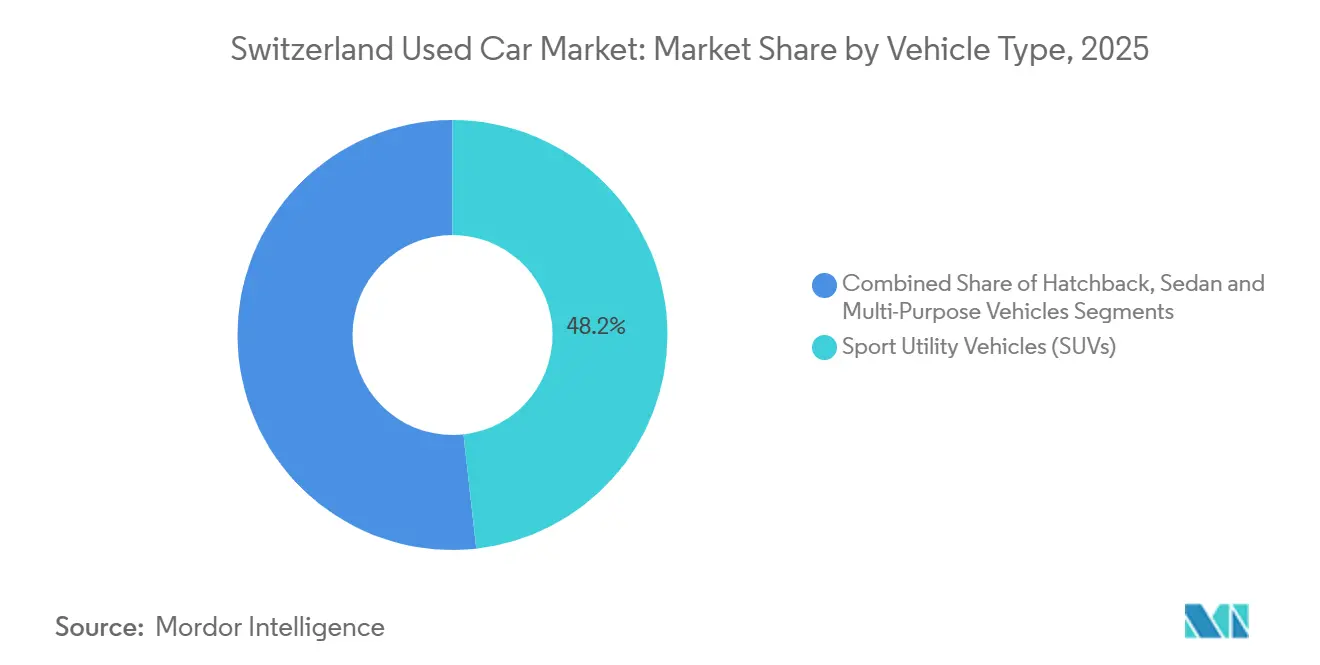

- By vehicle type, SUVs commanded a dominant 48.23% revenue share of Switzerland's used-car market in 2025, with projections indicating a 4.07% CAGR through 2031.

- By vendor type, the unorganized channel dominated Switzerland's used car market with a 59.68% share in 2025, while organized dealers are set to surge at a 5.11% CAGR through 2031.

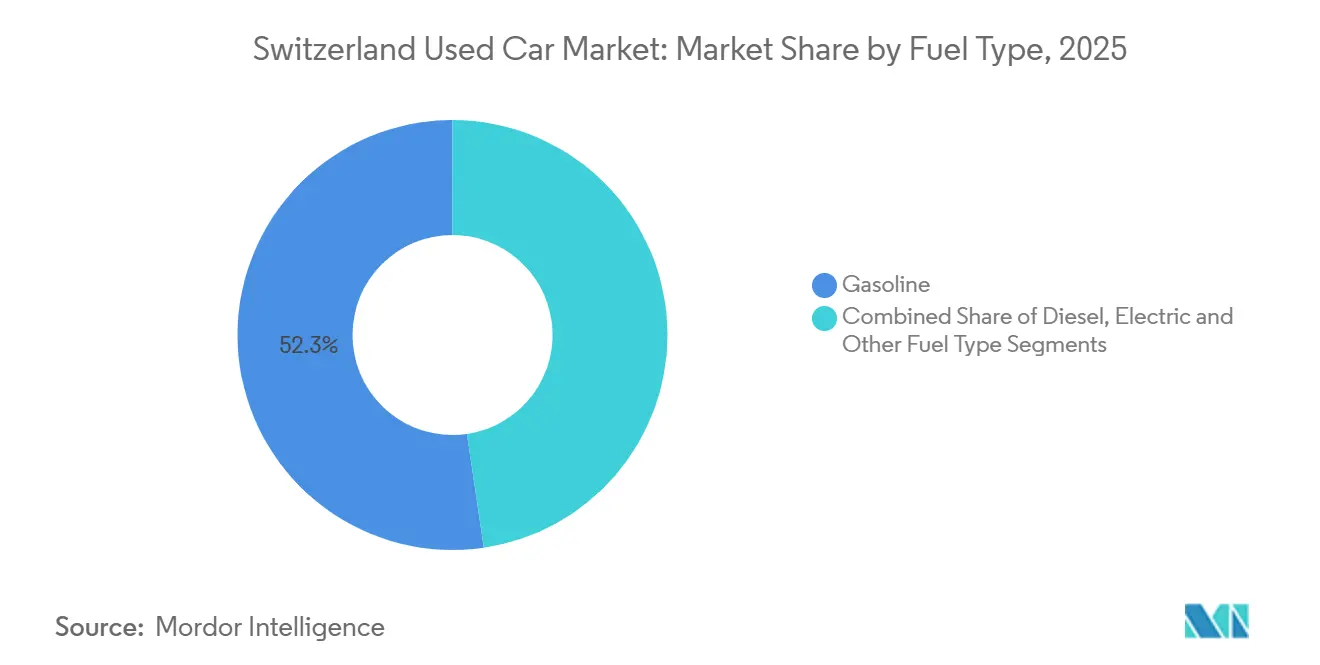

- By fuel type, gasoline vehicles accounted for 52.33% of Switzerland's used-car market in 2025, but electric cars are poised for the swiftest growth, projected at an 8.68% CAGR through 2031.

- By vehicle age, vehicles over 8 years old held a 41.42% share of Switzerland's used-car market in 2025, but the 0 to 3-year segment is anticipated to expand at a 5.86% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

National developments in Switzerland connect differently with activity unfolding across other parts of the world. In the global used car market coverage, Mordor Intelligence integrates these into a single analytical framework.

Switzerland Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prices of New Vehicles | +0.8% | Zurich, Geneva, Vaud, Bern, Basel-Stadt, Aargau | Short term (≤ 2 years) |

| Online Used-Car Platforms and Digital Retail | +0.6% | Zurich, Geneva, Vaud, Basel-Stadt, Zug | Medium term (2-4 years) |

| Corporate Fleet ESG Renewal Cycles | +0.5% | Zurich, Vaud, Geneva, Zug, Basel-Stadt | Medium term (2-4 years) |

| Affordable Chinese EVs | +0.4% | Zurich, Zug, Ticino, Geneva, Vaud | Long term (≥ 4 years) |

| Competitive Financing and Subscription Models | +0.4% | Zurich, Vaud, Geneva, Bern, Aargau | Medium term (2-4 years) |

| Decline in New-Car Sales | +0.3% | All cantons | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prices of New Vehicles and Cost-Sensitive Consumers

Average showroom prices for new cars climbed significantly in 2025, while ownership costs touched CHF 0.76 per kilometer, the steepest increase in more than a decade[2]"Kilometer costs to rise by four cents per kilometer in 2025", mobility-360.ch, mobility-360.ch . The affordability squeeze pushed middle-income households toward late-model used cars, typically sold at 30–40% discounts to their new equivalents, and heightened interest in fixed-price subscriptions that wrap insurance, maintenance, and taxes into a single monthly bill. Consumer surveys continue to show a 50% gap between perceived and actual total cost of ownership, a knowledge shortfall that organized dealers exploit by emphasizing predictable payments and manufacturer-backed warranties. The price gap between new EVs and comparable three-year-old units averages approximately CHF 13,000, strengthening residual values on battery-electric models and drawing first-time EV buyers into the secondary channel. Higher showroom sticker prices are therefore reinforcing the Swiss used car market as the default acquisition path for budget-constrained consumers.

Expansion of Online Used-Car Platforms and Digital Retail

AutoScout24 recorded a 6.2% increase in visitor traffic during H1-2024, accompanied by a robust surge in used-EV listings, proving that digital storefronts are the primary discovery engine for the modern buyer. AutoScout24 Direct’s instant-offer mechanism completed over 2,000 transactions in its inaugural year, illustrating appetite for low-touch, quick-liquidity exits among private sellers. Comparis acts as a nationwide pricing oracle; its algorithmic fair-value estimates reduce information asymmetry and compress negotiating spreads. Online-to-offline convergence is accelerating, with dealers deploying virtual walkarounds and click-to-reserve features to hold vehicles for 48 hours while remote buyers arrange financing. The Swiss used-car market is therefore moving toward an information-efficient equilibrium in which digital channels set transparent reference prices, and organized vendors capture value by adding reconditioning, warranty, and logistics layers.

Corporate Fleet ESG Renewal Cycles Increasing Near-New Supply

Corporate buyers account for most new registrations and typically defleet vehicles after 30–36 months, compared with more than 6 years for private owners. Upcoming European sustainability targets are shortening holding periods as companies race to electrify, boosting the flow of low-mileage cars into dealer auctions. Zurich, Vaud, and Geneva benefit disproportionately because fleet headquarters cluster in those cantons and the charging infrastructure is most dense there. Organized dealers exploit the steady inflow of well-documented ex-lease inventory to populate certified pre-owned programs that command price premiums and faster turns. Over the forecast window, these dynamics will raise the share of the 0-3 years cohort and keep warranty-backed deals at the forefront of consumer choice in the Switzerland used car market.

Influx of Affordable Chinese EVs Creating Future Supply Pipeline

BYD inaugurated Swiss operations in April 2025 with an entry price below CHF 43,000 (USD 52,527.5) for its SEAL U hybrid, capturing early adopters attracted by value-for-money propositions. Chinese brands already hold roughly 4% of total passenger-car registrations and 8% of the new-battery electric vehicle segment, indicating rapid acceptance beyond niche status. Lease contracts signed during the early adoption phase (2024-2026) are expected to mature between 2028 and 2031, releasing a wave of competitively priced battery-electric vehicles into the secondary channel. As these models age, they are expected to recalibrate consumer price anchors for used EVs, lowering entry thresholds and accelerating the transition away from internal-combustion units, especially in cantons offering full BEV tax exemptions. Over time, residual-value curves for incumbent European and Japanese models will likely flatten, pushing dealers to revise stocking strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vehicle-Tax Variations | -0.3% | All cantons, particularly Zurich, Geneva, Vaud, Bern | Medium term (2-4 years) |

| Trust and Transparency Challenges | -0.2% | All cantons | Short term (≤ 2 years) |

| Limited Public and Home Charging | -0.2% | Zurich, Geneva, Bern, Vaud, Basel-Stadt | Long term (≥ 4 years) |

| Stricter Lending Standards | -0.1% | All cantons | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cantonal Vehicle-Tax Variations Complicate Cross-Canton Sales

Vehicle-ownership taxes differ significantly, creating 26 micro-markets that distort price discovery and inventory allocation. Zurich, Geneva, and Basel-Stadt grant full BEV exemptions, whereas Schwyz offers minimal relief, encouraging arbitrage buyers to register vehicles in low-tax cantons. Dealers running multi-canton footprints face constant repricing headaches and must advise buyers of post-purchase tax liabilities, increasing transaction complexity. High-tax cantons exhibit softer residual values because buyers bake annual dues into discounted offers, a factor that slows inventory turns and curtails dealer appetite for stocking certain powertrains. Until federal harmonization emerges, tax dispersion will remain a structural drag on the Switzerland used car market’s overall growth rate.

Trust and Transparency Challenges for Buyers

Mandatory MFK technical inspections occur at five, eight, and every two subsequent years of a vehicle’s life, yet undisclosed defects are among the most common consumer grievances, according to national insurance claim files. Dealers can legally shorten statutory warranty coverage to 12 months, and private sellers can exclude it altogether, exposing buyers to repair costs that may exceed 10% of purchase value. Organized vendors attempt to close the trust gap with certified checks, digital service histories, and return policies, but uneven implementation allows isolated fraud incidents to taint broader market perception. The reputational overhang lengthens decision cycles and especially hurts the unorganized channel, where enforceable remedies are scarce. Greater transparency remains pivotal for unlocking latent demand, particularly among first-time buyers of used EVs, who are concerned about battery health and charging costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs Drive Market Expansion

Sport utility vehicles (SUVs) accounted for 48.23% of the 2025 volume, representing the most significant single slice of the Swiss used-car market share, and the segment is projected to grow at a 4.07% CAGR by 2031. Elevated seating, four-season traction, and adaptable cargo configurations align with alpine driving conditions, and corporate fleets increasingly favor compact crossovers that return to market after short lease terms. Electric versions such as the Tesla Model Y and Škoda Enyaq dominate search traffic, proving that battery-powered SUVs are fast becoming mainstream choices. Sedans, once the default format for private ownership, now trail SUVs and hatchbacks, with substitution most visible in German-speaking cantons where BMW 3-Series and Audi A4 listings spend longer on forecourts than equivalent Tiguan or Qashqai models.

Hatchbacks remain resilient in densely populated Geneva and Lausanne, where compact footprints ease parking and congestion charges. In contrast, MPVs are confined to large families and taxi fleets, a niche sustained mainly by the Volkswagen Multivan. The SUV electrification wave is set to translate into a richer pool of near-new BEVs from 2026 onwards, compressing price differentials with gasoline equivalents and expanding adoption beyond early enthusiasts. Dealers accordingly prioritize multi-brand SUV stocking strategies to capture high-velocity demand in urban and alpine markets. Because SUVs command the highest residuals among used body styles, they underpin dealer profitability and will continue to anchor transaction volumes in the Swiss used-car market.

By Vendor Type: Organized Players Consolidate Market Share

The unorganized space, private parties, and informal brokers accounted for 59.68% of the 2025 turnover, yet organized outlets are growing faster at a forecast 5.11% CAGR, as buyers gravitate toward institutional safeguards such as warranties and instant financing. EMIL FREY stores more than 30,000 used units nationally and has upgraded its e-commerce portal to enable 360-degree vehicle tours and click-to-reserve functionality. Unorganized sellers still attract value-driven buyers who can inspect mechanical condition themselves, but their price advantage is narrowing as platforms levy listing fees and organized players streamline cost structures.

Subscription models bridge the ownership-usage divide, monetizing vehicles through recurring revenues rather than one-off sales. This shift locks buyers into longer customer-lifetime cycles and hands organized vendors predictable cash flows that private sellers cannot rival. Regulatory tightening on consumer protection and warranty disclosure will further tilt the momentum toward formal actors, reinforcing the organized channel’s share-gaining trajectory in the Switzerland used car market.

By Fuel Type: Electric Vehicles Emerge Despite Infrastructure Challenges

Gasoline cars accounted for 52.33% of 2025 exchanges, reflecting the legacy fleet composition and the convenience of Switzerland’s dense refueling network. Yet battery-electric vehicles are the fastest-growing segment, with an 8.68% CAGR to 2031, buoyed by fleet electrification and cantonal tax holidays. BEVs captured over 15% of new registrations in 2024, setting the stage for a swelling secondary supply as early adopters offload three-year-old models. Diesel has receded to a single-digit share of new-car sales, and its appeal erodes further as Zurich and Geneva weigh emissions-zone restrictions.

Hybrids straddle the gap, sustaining robust residuals because they appeal to range-anxious drivers while sidestepping full-EV infrastructure dependence. Switzerland's used-car market for electric units is on a steep upward curve as buyers seek lower running costs, electricity per kilometer averages one-third that of gasoline, and corporates dump ICE assets ahead of fleet CO₂ thresholds. Dealers now integrate battery health diagnostics into listings, bolstering buyer confidence and reducing the average days-to-sell for used EVs.

By Vehicle Age: Near-New Vehicles Gain Momentum

Cars older than 8 years accounted for 41.42% of 2025 transfers, anchoring affordability for cost-conscious households. However, the 0-3 years bracket is expanding at a 5.86% CAGR as de-fleeted corporate and subscription units flood forecourts with low-mileage, warranty-eligible choices. Average national vehicle age climbed to over 10 years in 2024 as owners stretched replacement cycles amid new-car price inflation. Stricter periodic MFK inspections and higher parts costs weigh on maintenance budgets of legacy diesels and early-2000s gasoline models, nudging buyers toward younger, more efficient options.

Organized dealers capitalize on near-new inflows to promote certified pre-owned programs that bundle two-year warranties and subsidized financing. Subscription providers systematically retire vehicles before year four to preserve resale value, expanding supply even further. While the 8+ years segment will remain the largest by sheer count, its relative share is set to decline as ESG-driven fleet rotation intensifies and buyers seek vehicles compatible with evolving emissions and connectivity standards required for resale liquidity in the Switzerland used car market.

Geography Analysis

Zurich, a hub for vehicle registrations, leads in transaction counts due to its vibrant corporate leasing activity and a diverse dealer ecosystem spanning from luxury showrooms to high-volume auction houses. Urban electrification incentives and a well-established network of charging points contribute to the strong market performance of battery electric vehicles (BEVs). Additionally, Zurich stands out for its digital engagement, with platforms such as AutoScout24 and Comparis widely used by residents.

In the French-speaking regions, Geneva and Vaud are prominent for their high motorization rates and strong BEV adoption. Tax exemptions on zero-emission powertrains help reduce running costs for second owners and support the growing demand for used EVs. The regions also benefit from cross-border labor inflows, which drive demand for compact hatchbacks well-suited for urban commuting and limited parking.

Bern, Aargau, and Basel-Stadt represent the market's balanced core. With their mix of urban and rural areas, Bern and Aargau cater to a wide range of vehicle preferences, from affordable hatchbacks to premium SUVs. Basel-Stadt benefits from its position as a trade hub, bringing in vehicle imports from neighboring countries and enhancing model variety. In Ticino, cultural ties to Italy influence consumer preferences, with Fiat being a popular choice. However, in the alpine cantons, limited charging infrastructure hampers the growth of the used EV market, maintaining a steady demand for gasoline vehicles. Federal funding planned for the coming years could pave the way for new electrification opportunities in these regions.

Mordor Intelligence's coverage of the used car market extends across other regions including Africa, while country-specific intelligence is also available for Netherlands, Portugal, Nigeria, Belgium, Kenya, South Korea, Brazil, and Bangladesh, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The market is moderately concentrated. Emil Frey and AMAG, two key players in the organized tier, leverage nationwide service centers, captive leasing, and omnichannel sales to handle a significant volume of monthly trade-ins. AMAG’s lease contracts contribute to its certified pre-owned funnel, enhancing its advantages in reconditioning and logistics. In January 2026, Emil Frey expanded its portfolio with the acquisition of PJ Condellis SA, entering the light truck market. This move diversifies its offerings, mitigating risks associated with passenger-car cyclicality, and positions it favorably for the anticipated surge in demand for last-mile delivery fleets.

Digital platforms are reshaping buyer expectations. AutoScout24, for instance, aggregates listings from dealers and private sellers, enhancing its platform with financing calculators and automated valuation tools. Comparis serves as a price-benchmarking tool, nudging dealers to align with algorithmic fair values to ensure stock visibility. New entrants like Carvolution and Gowago, focusing on subscriptions, cater to millennials and expatriates who prioritize flexibility over ownership. This shift transforms traditional one-time sales into recurring annuity-style services.

In today's market, competitive edge is increasingly derived from data analytics, inventory algorithms, dynamic pricing, and predictive maintenance. While larger players harness AI to predict residuals and streamline stock rotation, smaller independents depend on human judgment, making them vulnerable to pricing inaccuracies and slower inventory turnover. The entry of Chinese OEMs, exemplified by BYD's direct sales approach, intensifies competition. BYD's strategy not only challenges entry-level ICE prices but also threatens to squeeze dealer margins in mainstream segments. The Swiss used-car market finds itself at a crossroads, balancing the scale-driven strategies of incumbents against the nimble approaches of digital newcomers, with neither commanding overwhelming market dominance.

Switzerland Used Car Industry Leaders

-

Emil Frey Ag

-

AMAG Automobil und Motoren AG

-

CAR FOR YOU AG

-

Auto Kunz AG

-

AutoScout24 AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: AutoScout24.ch introduced AutoScout24 Direct, a platform that enables private sellers to connect with its nationwide dealer network. AutoScout24 Direct has collaborated with CarAuktion, a privately owned e-auction platform, to facilitate this service.

- January 2024: Carvolution secured CHF 200 million in asset-backed financing from Barclays and Waterfall Asset Management to accelerate growth in the Swiss car subscription market.

Switzerland Used Car Market Report Scope

A used car is a pre-owned vehicle that has previously had one or more retail owners. These cars are sold through a variety of outlets through independent dealers, online sales channels, and others.

The Switzerland used car market is segmented by vehicle type, vendor type, fuel type, and vehicle age. By vehicle type, the market is segmented into Hatchbacks, Sedans, Sport Utility Vehicles (SUVs), and Multi-Purpose Vehicles (MUVs). By vendor type, the market is segmented into Organized and Unorganized. By fuel type, the market is segmented into Gasoline, Diesel, Electric, and Other Fuel Types. By vehicle age, the market is segmented into 0 to 3 Years, 4 to 8 Years, and More than 8 Years. The report provides market sizing and forecasts in terms of value (USD) and volume (units).

| Hatchback |

| Sedans |

| Sport Utility Vehicles (SUVs) |

| Multi-Purpose Vehicles (MUVs) |

| Organized |

| Unorganized |

| Gasoline |

| Diesel |

| Electric |

| Other Fuel Types |

| 0 to 3 Years |

| 4 to 7 Years |

| More than 8 Years |

| By Vehicle Type | Hatchback |

| Sedans | |

| Sport Utility Vehicles (SUVs) | |

| Multi-Purpose Vehicles (MUVs) | |

| By Vendor Type | Organized |

| Unorganized | |

| By Fuel Type | Gasoline |

| Diesel | |

| Electric | |

| Other Fuel Types | |

| By Vehicle Age | 0 to 3 Years |

| 4 to 7 Years | |

| More than 8 Years |

Key Questions Answered in the Report

How fast is the Switzerland used car market expected to grow to 2031?

Value is projected to increase from USD 26.48 billion in 2026 to USD 30.82 billion by 2031 at a 3.08% CAGR.

Which body style sells the most in Switzerland?

SUVs led with 48.23% share in 2025 and are forecasted to stay ahead through 2031.

Are electric vehicles gaining traction in the secondary channel?

Yes, used-EV transactions are growing at an 8.68% CAGR as corporate fleets de-fleet near-new battery-electric cars.

Why are organized dealers taking share from private sellers?

Buyers favor warranties, financing, and digital transparency that organized channels provide, driving their forecast 5.11% CAGR.

Page last updated on: