Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

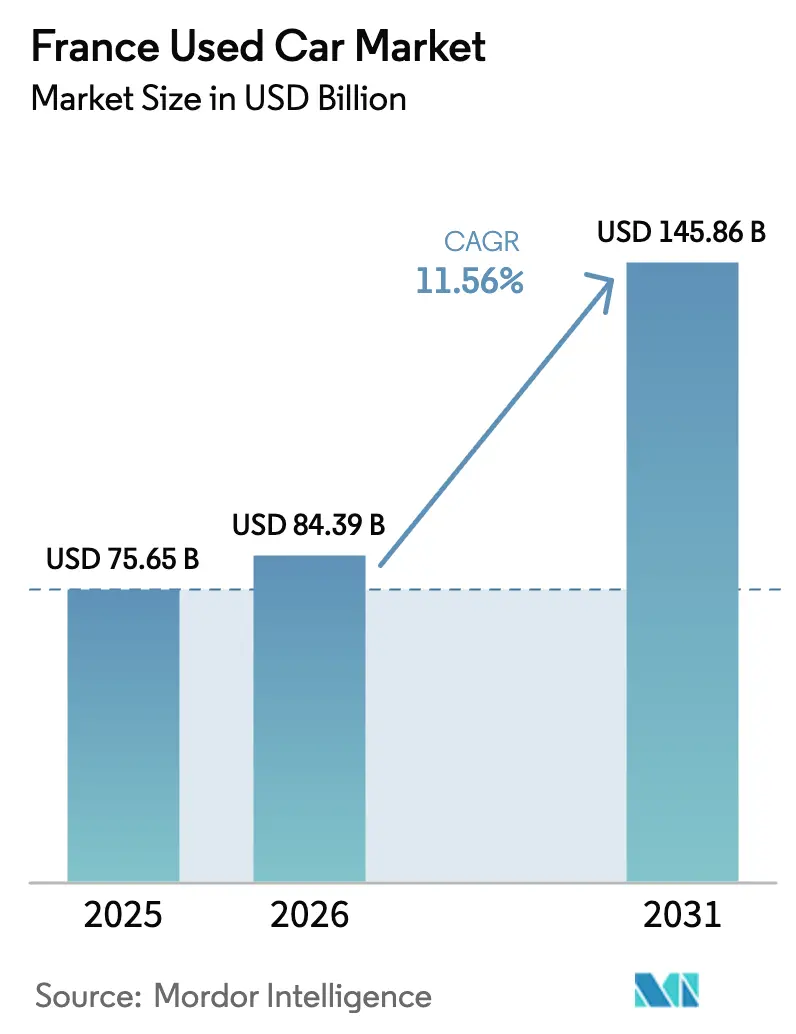

| Base Year Market Size (2025) | USD 75.65 Billion |

| Market Size (2026) | USD 84.39 Billion |

| Market Size (2031) | USD 145.86 Billion |

| Growth Rate (2026 - 2031) | 11.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Used Car Market Analysis by Mordor Intelligence

France used car market size in 2026 is estimated at USD 84.39 billion, growing from 2025 value of USD 75.65 billion with 2031 projections showing USD 145.86 billion, growing at 11.56% CAGR over 2026-2031.

France is now the second-largest pre-owned vehicle arena in Europe, trailing only Germany, because regulatory action, widening new-to-used price gaps, and rapid digital adoption are reshaping demand. New-car sticker prices have risen 15% faster than used-car values since 2024, pushing cost-conscious buyers toward the secondary channel and reinforcing the structural appeal of the France used car market. On the supply side, the coming wave of 2–3-year-old lease and subscription returns, especially electric compact SUVs, will refresh inventory depth while moderating price inflation. Parallel growth in certified-pre-owned (CPO) programmes enhances consumer confidence, allowing organised retail networks to monetise refurbishing know-how and warranty extensions. Finally, the roll-out of France’s CO₂/weight tax in 2026 tilts shopper preference toward lighter, lower-emission models, deepening the pivot to electrified powertrains and accelerating fleet turnover in the France used car market.

Key Report Takeaways

- By vehicle type, SUVs led with 38.10% of France used car market share in 2025.

- By vendor type, unorganised dealers controlled 56.40% of the France used car market size in 2025, while organised dealers delivered the fastest 13.35% CAGR through 2031.

- By fuel type, petrol retains 43.70% share of the France used car market size in 2025.

- By vehicle age, the 3-5-year bucket accounts for 48.00% of France used car market share in 2025.

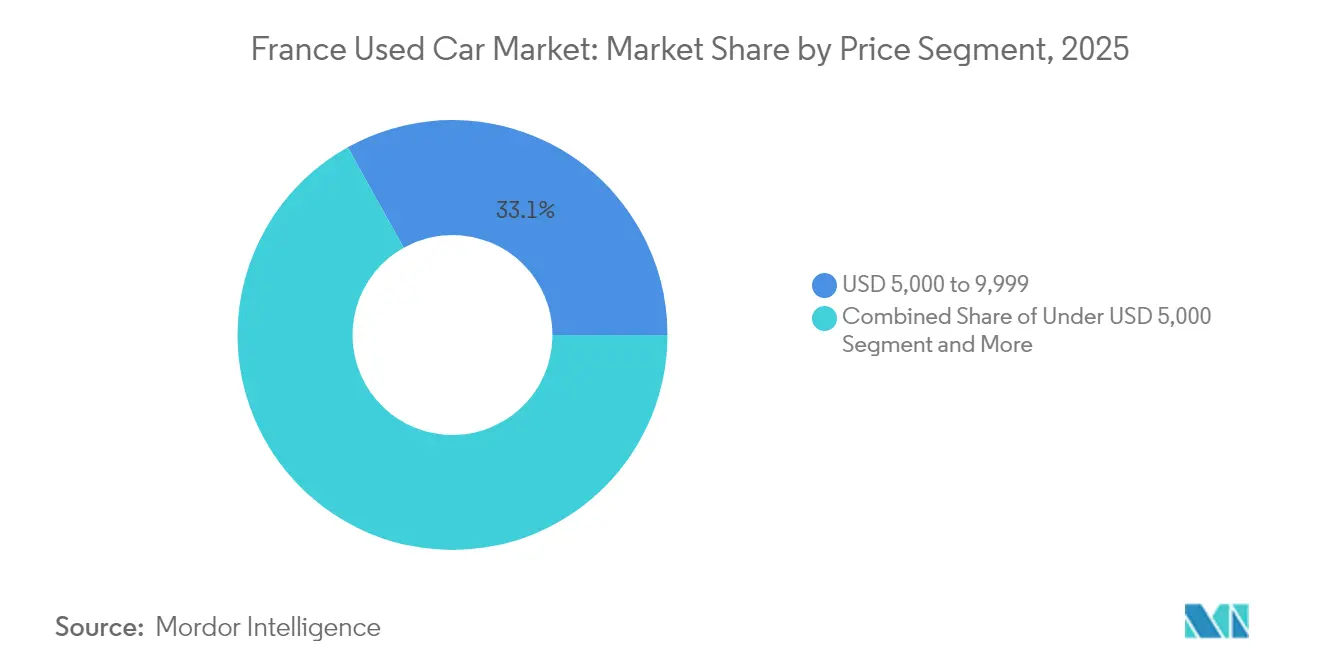

- By price band, the USD 5,000-9,999 bracket holds 33.10% of the France used car market size in 2025.

- By sales channel, online transactions grow at 17.30% CAGR while offline outlets keep an 86.20% revenue share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | Qualitative Impact | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|---|

| Rising new-car prices widening the value gap | Strong | +3.2% | Île-de-France, Provence-Alpes-Côte d'Azur, Auvergne-Rhône-Alpes | Short term (≤ 2 years) |

| Expansion of online used-car platforms | Strong | +2.8% | Île-de-France, Hauts-de-France, Grand Est | Medium term (2-4 years) |

| Short-term subscription & lease fleet returns surge | Strong | +2.1% | Île-de-France, Provence-Alpes-Côte d'Azur, Occitanie | Medium term (2-4 years) |

| Growth of certified-pre-owned (CPO) programmes | Moderate | +1.9% | Île-de-France, Auvergne-Rhône-Alpes, Nouvelle-Aquitaine | Medium term (2-4 years) |

| 2025 French CO₂/weight tax | Moderate | +1.4% | All French regions | Short term (≤ 2 years) |

| AI-driven reconditioning cuts refurb costs | Weak | +0.8% | Île-de-France, Auvergne-Rhône-Alpes, Hauts-de-France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | ||||

Rising New-Car Prices Widen the Value Gap to Used Cars

New-car registrations fell 7% year-on-year through April 2025, while pre-owned transactions climbed 3.1%, underscoring a structural shift toward the France used car market. The average price premium for a new vehicle over a comparable three-year-old model widened from 45% in 2024 to 52% by December 2025. Dealers that scale sourcing and refurbishing pipelines capture this arbitrage, especially within warranty-backed CPO stock that still undercuts new-car outlays by roughly 30%.

Expansion of Online Used-Car Platforms & Digital Showrooms

Online channels, fuelled by AI inspection kiosks and end-to-end finance integration, are compounding at 17.75% through 2030 even though click-to-buy makes up only 13.11% of current turnover. Players deploying ProovStation’s automated scanning cut appraisal time to seconds and issue instant binding offers, lowering friction for urban millennials increasingly steering activity within the France used car market[1]“Automated Vehicle Inspection Solutions,” ProovStation, proovstation.com.

Short-Term Subscription & Lease Fleet Returns Surge From 2026

France’s social EV leasing scheme restarts in 2025 and is expected to dispatch tens of thousands of compact electric SUVs back into circulation by 2027, dovetailing with corporate fleet swaps initiated in 2024–2025. The resulting influx of 2–3-year-old, low-mileage units will extend model choice and ease price spikes, yet may compress dealer margins without agile pricing tools.

Growth of Certified-Pre-Owned (CPO) Programmes

CPO schemes bridge trust gaps by providing multi-point inspections, factory-grade refurbishment, and extended warranties of up to 10 years/175,000 km, as seen in Stellantis’ Spoticar roll-out. Such guarantees feed growing consumer appetite for reliability, allowing organised retailers to lift average selling price while sustaining faster stock turns.

Restraints Impact Analysis*

| Restraint | Qualitative Impact | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|---|

| Highly fragmented dealer landscape | Strong | -2.1% | All French regions | Short term (≤ 2 years) |

| Falling BEV residual values | Strong | -1.8% | Île-de-France, Provence-Alpes-Côte d'Azur, Auvergne-Rhône-Alpes | Medium term (2-4 years) |

| Extended 3-year statutory warranty | Moderate | -1.2% | All French regions | Medium term (2-4 years) |

| EU battery end-of-life rules add compliance cost | Weak | -0.7% | All French regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | ||||

Highly Fragmented Dealer Landscape Compresses Margins

More than 15,000 small-scale dealerships operate nationwide, limiting purchasing leverage and curtailing economies of scale. With unorganised vendors still commanding 57.08% share, pricing wars erode gross margins and delay technology upgrades critical for the next phase of growth in the France used car market.

Falling BEV Residual Values Create Stock-Value Risk

Five-year projected depreciation for battery-electric models averages 49.1%, outpacing ICE counterparts and forcing cautious stocking strategies. Dealers must adopt battery-health analytics to mitigate valuation errors, particularly as aggressive OEM price cuts can shock residual models mid-cycle[2]Philippe Borremans et al., “Residual Value Trajectories of Battery-Electric Vehicles in Europe,” MDPI, mdpi.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs Drive Market Expansion

SUVs held 38.10% of the French used car market share in 2025 and are expanding the French used car market size for this body style at a 12.05% CAGR to 2031, fuelled by consumer preference for elevated seating and the influx of compact electric crossovers from leasing schemes. The segment’s depth lets organised retailers optimise stocking plans, while hatchbacks retain inner-city loyalty but face weight-tax headwinds favouring lighter platforms. Rural territories lean toward larger SUVs for versatility, whereas Parisian districts gravitate to sub-compact variants apt for tight parking zones.

Higher transaction velocity in SUVs boosts data availability for dynamic pricing, supporting AI-assisted analytics that refine inventory turns. Conversely, sedans and MPVs cede mindshare, with sedan resale values dipping as buyers gravitate to multi-purpose silhouettes. MPVs still address family mobility but battle SUV substitutes offering comparable boot volume and better residuals. Lifestyle categories, convertibles, and coupes remain low in volume yet enjoy resilient margins driven by enthusiast appetite.

By Vendor Type: Organised Players Gain Ground

Unorganised outlets retained 56.40% of France used car market size in 2025, but organised networks are compounding at 13.35%, signalling a gradual re-balancing. Scale advantages allow nationwide chains to standardise refurbishment, extend warranties, and unify digital storefronts. Franchise groups employ centralised remarketing hubs to shave reconditioning cycles by double-digit percentages, reinforcing margin differential.

Small independents maintain agility through local rapport and lower overhead; yet opaque pricing is steadily penalised as comparison engines proliferate across the French used car market. Capital constraints limit their investment in omnichannel tech and battery diagnostics for EV stock, widening the capability gap. A coexistence equilibrium is likely, but shared drift favours branded networks leveraging CPO credibility.

By Fuel Type: Electric Surge Reshapes Dynamics

Electric vehicles are steering an 18.20% CAGR, outpacing all legacy fuels, while petrol units still own 43.70% of the French used car market share in 2025. Government weight-based malus exemptions and expanding fast-charge corridors underpin the pivot, particularly in Île-de-France, where EV penetration reached 19.4% in January 2025. Diesel inventory declines on looming urban access limits and residual value uncertainties.

Hybrid models serve risk-averse adopters who want combustion back-up but cleaner profiles, while LPG/CNG fleets cater to commercial mileage disciplines. Dealers adopting certified battery-health reports accelerate consumer trust and mitigate price haggling. Infrastructure gaps outside metro areas decelerate rural EV rotation, but 2026 lease-return surpluses will catalyse affordability.

By Vehicle Age: Young Vehicles Command Premium Growth

Units aged 0-2 years are advancing at 15.90% CAGR as buyers chase near-new tech with remaining factory cover. Yet the 3-5-year tranche retains 48.00% of France's used car market share, balancing affordability and quality in the French used car market. Lease maturities and corporate fleet renewals ensure a steady supply of both cohorts, sustaining broad inventory health.

Older categories-6-8 years and 9-12 years-anchor value-driven segments but attract stricter financing terms that can curb demand. Vehicles exceeding 12 years confront ever-tighter environmental controls, such as expanded technical inspection regimes legislated in 2022 that escalate compliance costs. Dealers segment inventory by age to align warranty packages and credit tenors to consumer affordability ceilings.

By Price Segment: Mid-Market Drives Growth

The USD15,000-19,999 bracket is the fastest-growing at 13.75% CAGR, appealing to middle-income households seeking modern safety tech without new-car premiums. Below USD 10,000, older stock still holds 33.10% of France used car market size as cash buyers and micro-enterprises look for budget transport. Premium tiers above USD 30,000 cater to aspirational or corporate perks, but account for limited volume.

Weight-related taxation from 2026 incentivises lighter configurations across all price bands, potentially compressing large-engine premium values. Financiers extend six- to seven-year loan durations on mid-market vehicles, supporting affordability and sustaining the French used car market’s resilience amid macro uncertainty.

By Sales Channel: Digital Transformation Accelerates

Although offline showrooms commanded 86.20% revenue share in 2025, online channels are growing at 17.30% CAGR as millennials normalise click-to-buy behaviour. Digital classified portals funnel lead volume, while pure-play e-retailers differentiate through home delivery and money-back guarantees. OEM-branded sites integrate CPO warranties for brand loyalists.

Hybrid models are emerging: shoppers shortlist vehicles digitally, then finalise test drives and paperwork in satellite hubs. Offline incumbents retrofit augmented-reality walk-rounds and live-chat finance approvals to keep pace, cementing omnichannel expectations across the French used car market.

Geography Analysis

Île-de-France contributes roughly one-quarter of national pre-owned transactions and showcases the highest digital-purchase ratios, underpinned by superior broadband penetration and dense charging infrastructure. Only 33% of Paris households own a car versus 81.4% nationally, catalysing churn for shared-mobility-aligned compact EVs. Stringent low-emission zones fast-track ICE scrappage and lift residuals for compliant hybrids.

Provence-Alpes-Côte d’Azur and Auvergne-Rhône-Alpes form a second tier, combining tourism-driven seasonal spikes with proximity to manufacturing clusters that streamline stock sourcing. Warm coastal climates curb corrosion, preserving bodywork and elevating resale premiums. Lyon hosts multiple automotive tech start-ups, becoming a testbed for AI-assisted inspection rigs that ripple efficiency across the French used car market.

Rural corridors, Nouvelle-Aquitaine, Occitanie, Grand Est, display ownership ratios exceeding 90%, given sparse public transport. Demand skews toward SUVs and light commercials, while EV adoption lags amid limited charger density. The government’s social leasing incentives specifically target these regions, promising a future pipeline of used electric hatchbacks that will progressively diversify rural forecourts.

Competitive Landscape

Leboncoin holds a significant share, leveraging high-traffic classifieds reach, while AutoScout24 gains via cross-border inventory draw. Aramis Group, through centralised refurb hubs, demonstrates the scalability of CPO-led e-commerce. Competitive levers are shifting from sheer stock volume to data analytics and omnichannel convenience.

AI pricing engines refine offer accuracy, and battery-health certificates reduce EV appraisal volatility. Stellantis’ Spoticar integrates factory warranties, boosting trust equity, whereas ProovStation kiosks truncate inspection time from 30 minutes to under 5. Partnerships with fintech lenders deliver instant credit decisions, bolstering consumer conversion.

Fragmentation nevertheless endures: thousands of independents sustain hyper-localised supply, especially in peri-urban belts where personal rapport still trumps digital clicks. Consolidation is expected to proceed steadily as capital-rich networks absorb under-invested peers, riding the scale economics vital to compete within the expanding France used car market.

France Used Car Industry Leaders

Leboncoin

Aramis Group

AutoScout24 (SMG Swiss Marketplace Group)

Stellantis Spoticar

Auto1 Group (Autohero)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: ProovStation expanded AI vehicle-scanning units to 130 service stations across 13 countries, offering automated inspection and valuation for used-car transactions.

- February 2024: Stellantis subsidiary Ayvens signed a frame agreement to acquire up to 500,000 vehicles by 2026 to accelerate sustainable-mobility roll-out.

France Used Car Market Report Scope

A used car/pre-owned vehicle is a vehicle that previously had one or more retail owners. A certified pre-owned (CPO) vehicle, on the other hand, is a pre-owned vehicle that has been extensively inspected (pre-purchase inspection) and expertly reconditioned. The used car market consists of a wide range of companies involved in purchasing and selling pre-owned vehicles through online or offline sales channels.

The French used car market is segmented by vehicle type, vendor type, fuel type, and sales channel. By vehicle type, the market is segmented into hatchbacks, sedans, sports utility vehicles (SUVs), and multi-purpose vehicles (MPVs). By vendor type, the market is segmented into organized and unorganized. By fuel type, the market is segmented into petrol, diesel, electric, and other fuel types (liquefied petroleum gas, compressed natural gas, etc.). By sales channel, the market is segmented into online and offline.

The report offers market size and forecasts for used cars in value (USD) for all the above segments.

By Vehicle Type

| Hatchbacks |

| Sedans |

| SUVs |

| MPVs |

| Others (convertibles, coupes, crossovers, sports cars) |

By Vendor Type

| Organized |

| Unorganized |

By Fuel Type

| Petrol |

| Diesel |

| Hybrid |

| Electric |

| LPG / CNG / Others |

By Vehicle Age

| 0 - 2 Years |

| 3 - 5 Years |

| 6 - 8 Years |

| 9 - 12 Years |

| Above 12 Years |

By Price Segment

| Under USD 5,000 |

| USD 5,000 - 9,999 |

| USD 10,000 - 14,999 |

| USD 15,000 - 19,999 |

| USD 20,000 - 29,999 |

| USD 30,000 and Above |

By Sales Channel

| Online | Digital Classifieds Portals |

| Pure-play e-Retailers | |

| OEM-Certified Online Stores | |

| Offline | OEM-Franchised Dealers |

| Multi-brand Independent Dealers | |

| Physical Auction Houses |

| By Vehicle Type | Hatchbacks | |

| Sedans | ||

| SUVs | ||

| MPVs | ||

| Others (convertibles, coupes, crossovers, sports cars) | ||

| By Vendor Type | Organized | |

| Unorganized | ||

| By Fuel Type | Petrol | |

| Diesel | ||

| Hybrid | ||

| Electric | ||

| LPG / CNG / Others | ||

| By Vehicle Age | 0 - 2 Years | |

| 3 - 5 Years | ||

| 6 - 8 Years | ||

| 9 - 12 Years | ||

| Above 12 Years | ||

| By Price Segment | Under USD 5,000 | |

| USD 5,000 - 9,999 | ||

| USD 10,000 - 14,999 | ||

| USD 15,000 - 19,999 | ||

| USD 20,000 - 29,999 | ||

| USD 30,000 and Above | ||

| By Sales Channel | Online | Digital Classifieds Portals |

| Pure-play e-Retailers | ||

| OEM-Certified Online Stores | ||

| Offline | OEM-Franchised Dealers | |

| Multi-brand Independent Dealers | ||

| Physical Auction Houses | ||

Key Questions Answered in the Report

What is the current size of the France used car market?

The market stands at USD 84.39 billion in 2026 and is projected to reach USD 145.86 billion by 2031.

How fast is the market expected to grow?

It is forecast to expand at an 11.56% CAGR from 2026 to 2031.

Which vehicle type holds the largest share today?

SUVs lead with 38.10% France used car market share in 2025 and also post the fastest 12.05% CAGR.

Which fuel segment is growing quickest?

Electric vehicles record the highest 18.20% CAGR while petrol maintains the largest share.

How significant is online retail in this market?

Online channels currently capture 13.80% of sales but are growing at 17.30% CAGR, signalling a rapid digital shift.

Page last updated on: