AI In Aerospace And Defense Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

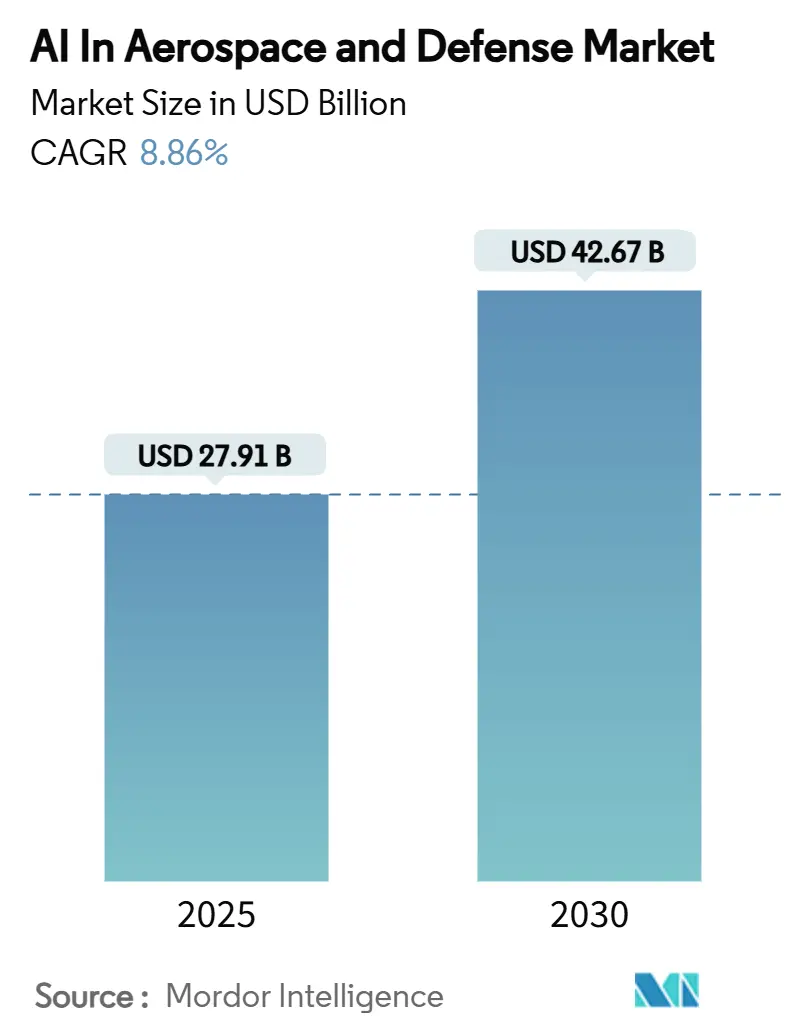

| Market Size (2025) | USD 27.91 Billion |

| Market Size (2030) | USD 42.67 Billion |

| Growth Rate (2025 - 2030) | 8.86% CAGR |

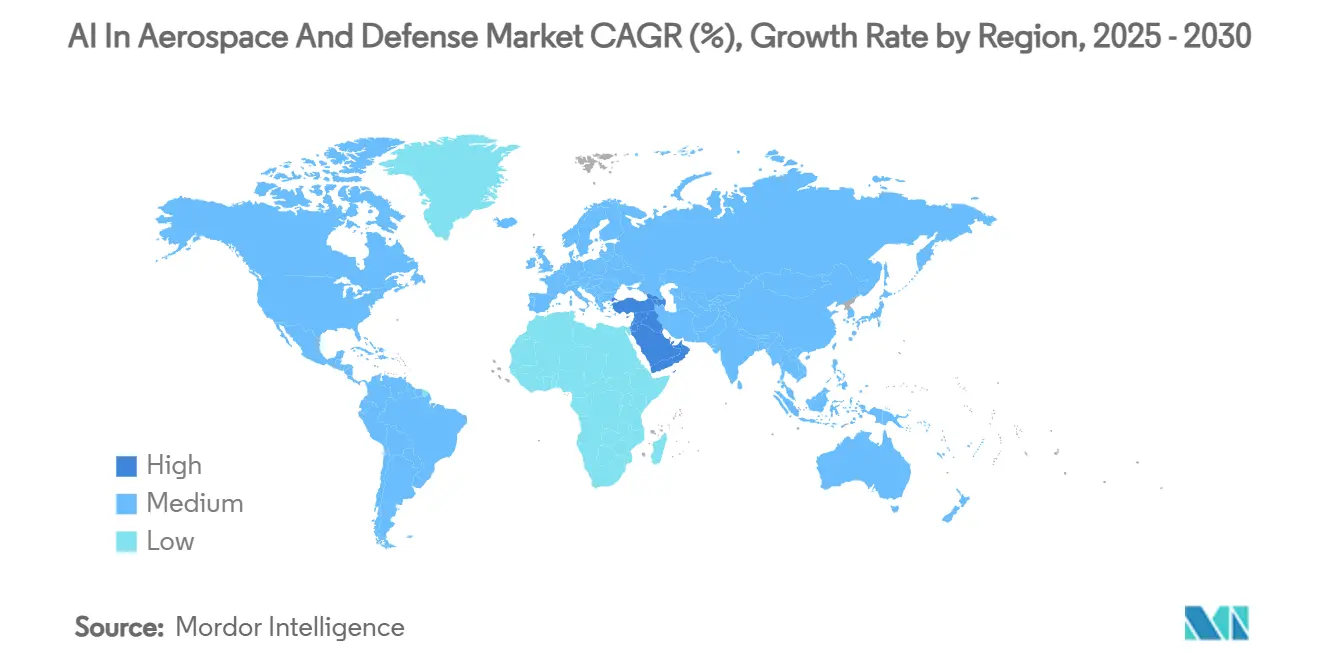

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

AI In Aerospace And Defense Market Analysis by Mordor Intelligence

The AI in the aerospace and defense market generated USD 27.91 billion in 2025 and is on track to reach USD 42.67 billion by 2030, implying an 8.86% CAGR over the forecast period. Military programs account for the largest spending block, while accelerating digital-transformation initiatives in commercial aviation and space exploration sustain a broad demand base. Rapid growth in defense AI budgets, ongoing fleet renewals, and a clear shift toward autonomy at the edge continue to widen the total addressable opportunity. Adoption is especially strong wherever predictive-maintenance analytics cut unscheduled downtime, and wherever certified edge-AI processors make real-time inference possible aboard aircraft, spacecraft, or unmanned vehicles. Competitive dynamics remain fluid as software-centric entrants challenge long-established primes, focusing on fast iteration, cloud-native deployment, and outcome-based contracting.

Key Report Takeaways

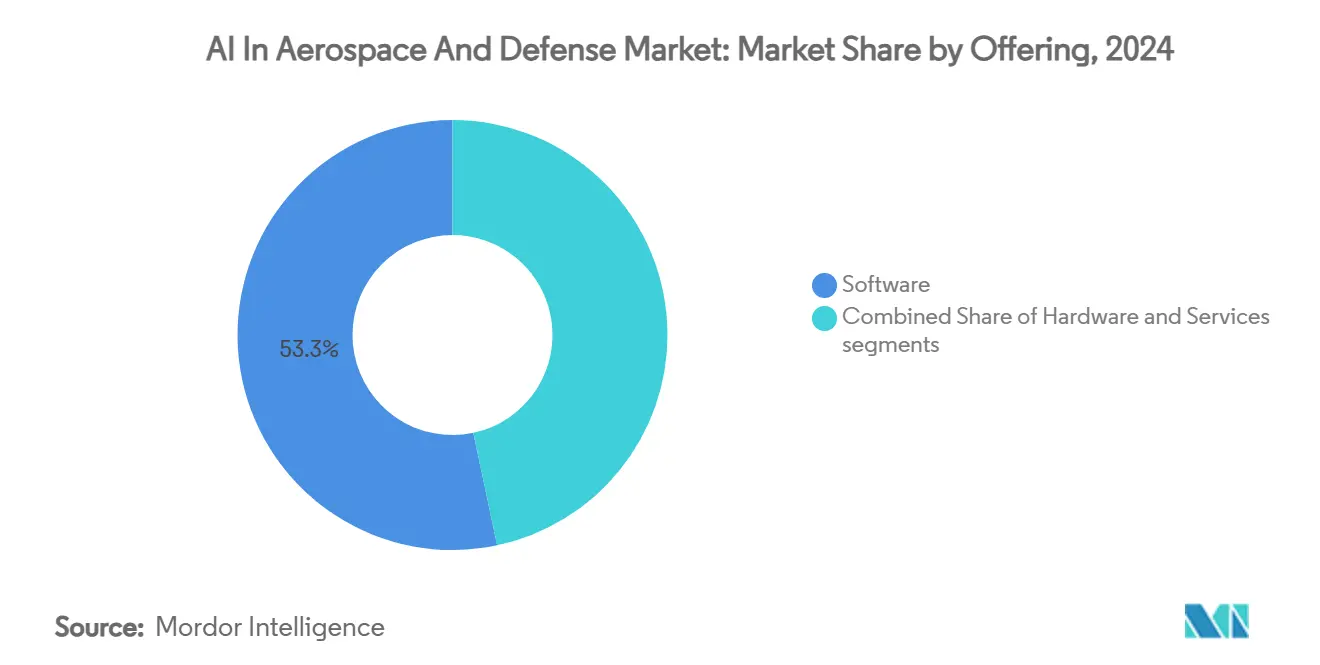

- By offering, software held 53.33% of the AI in aerospace and defense market share in 2024, while services are projected to expand at a 9.87% CAGR through 2030.

- By application, military systems led with 45.16% revenue share in 2024; the space segment is forecast to grow at 10.7% CAGR to 2030.

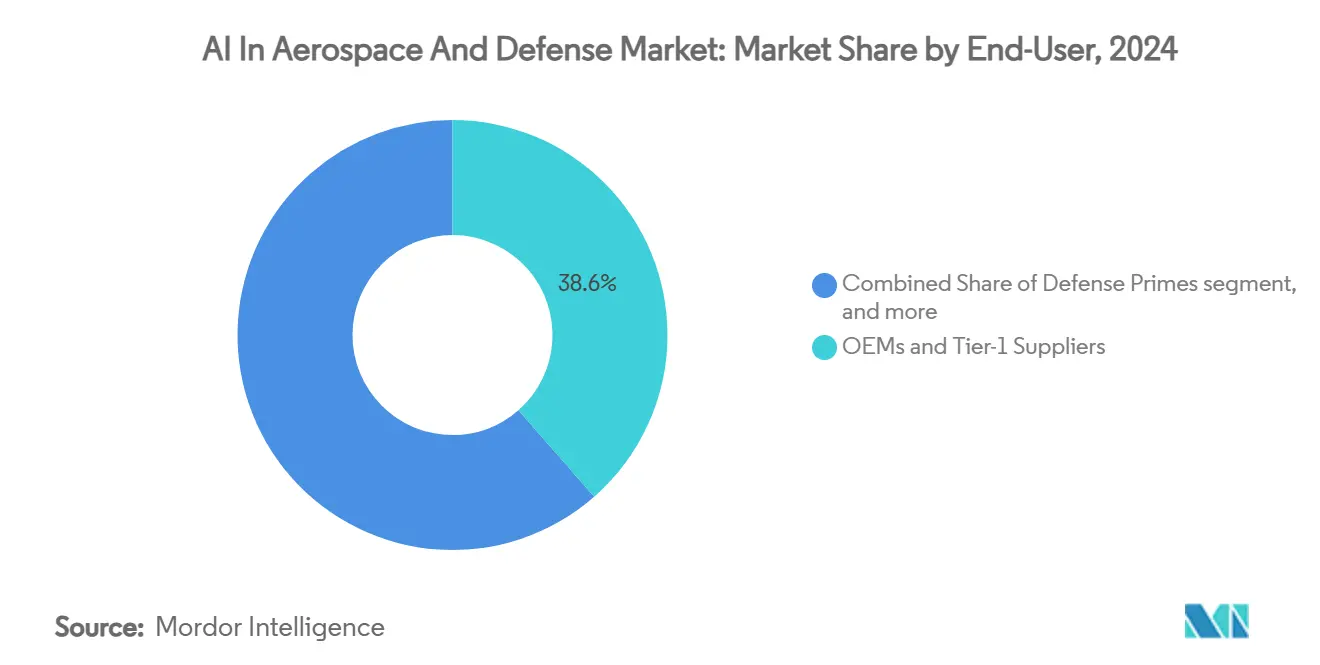

- By end-user, OEMs and Tier-1 suppliers controlled 38.55% share of the AI in aerospace and defense market size in 2024; space agencies and new-space operators are set to post the fastest 8.91% CAGR.

- By region, North America commanded a 33.45% share of the AI in aerospace and defense market in 2024, while the Middle East is expected to record a 9.31% CAGR through 2030.

Global AI In Aerospace And Defense Market Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring defense AI budgets | +2.1% | North America; spillover to allies | Short term (≤ 2 years) |

| Surge in predictive-maintenance adoption across MRO | +1.8% | Global; strongest in North America and Europe | Medium term (2-4 years) |

| Rapid growth of autonomy-ready UAV fleets | +1.5% | Global; early deployment in US, China, Israel | Medium term (2-4 years) |

| Edge-AI chips certified for flight and space | +1.2% | APAC core; spillover to North America and Europe | Long term (≥ 4 years) |

| Neuromorphic co-processors for SWaP-constrained platforms | +0.9% | North America and Europe; emerging in APAC | Long term (≥ 4 years) |

| Blockchain-secured multi-robot swarms | +0.4% | National programs in US, UK, France | Long term (≥ 4 years) |

Source: Mordor Intelligence

Soaring defense-AI budgets drive adoption

The FY-25 US Department of Defense allocation of USD 1.8 billion for AI—40% higher than FY-24—fast-tracks prototyping across autonomy, C4ISR, and decision-support systems.[1] Tara Copp, “Pentagon Doubles Down on AI in FY-25 Budget,” Defense One, defenseone.com DARPA directed USD 300 million to field projects such as the Advanced Capability Enabler, while the newly elevated Chief Digital and Artificial Intelligence Office consolidates enterprise authority. Contracts awarded to Lockheed Martin, Northrop Grumman, and Anduril cover automated mission-planning, synthetic-aperture radar exploitation, and manned–unmanned teaming capabilities. The spending surge sparks similar moves among NATO partners that co-invest in data-fusion platforms and secure edge-compute nodes.

Predictive-maintenance economics reshape MRO

Airlines employing AI-driven prognostics cut unscheduled events by 20-30%, saving several million USD per wide-body annually.[2]Editorial Team, “Boeing Advances Predictive Maintenance Across 777 Fleet,” Boeing, boeing.com Pratt & Whitney’s EngineWise processes 50 billion datapoints annually, while Lufthansa Technik’s AVIATAR reduces aircraft-on-ground time by 15%. Military operators mirror the trend: the US Air Force reports 25% higher mission-capable rates after rolling out its Predictive Analytics and Decision Assistant. Consequently, service providers pivot from reactive repairs toward outcome-based, analytics-backed contracts.

Autonomous UAV fleets reach maturity

Swarming demonstrations now coordinate dozens of air vehicles with minimal operator input, validating AI-enabled target recognition and route-deconfliction on the fly. Israel’s Harop loitering munition engages threats autonomously inside user-defined rules of engagement, while Zipline’s commercial drones rely on vision-based navigation to complete 400,000+ medical deliveries. Edge inference chips allow real-time avoidance and cooperative behavior without ground links, which is crucial for contested or disaster areas.

Edge-AI chips clear certification hurdles

AMD’s Versal ACAP earned space-grade radiation tolerance qualification, unlocking satellite onboard analysis. Testing on the ISS, Intel’s Loihi neuromorphic processor delivered 1,000× lower energy per inference for pattern-recognition tasks. AFRL’s Neuromorphic Computing in Space program validated BrainChip’s Akida for real-time imagery while staying within small-sat power budgets.[3]John Keller, “AFRL Demonstrates Neuromorphic Processing in Orbit,” AFRL, afrl.af.mil Certification—often a three-year process—creates high entry barriers yet guarantees reliability for mission-critical roles.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-control and autonomous-weapon regulations | −1.3% | Global; strong in US ITAR/EAR regimes | Medium term (2-4 years) |

| Cyber-supply-chain vulnerabilities | −0.8% | Global; heightened during near-peer tensions | Short term (≤ 2 years) |

| Acute aerospace and defense AI-talent shortage | −1.1% | North America and Europe | Medium term (2-4 years) |

| Thermal and power limits of edge compute in-flight | −0.6% | Global; severe for high-altitude and space assets | Long term (≥ 4 years) |

Source: Mordor Intelligence

Export controls impose technology choke points

Revisions to the US Commerce Control List now require licenses for facial-recognition or automated-targeting software shipped to designated states. European partners in the Future Combat Air System consequently develop parallel AI stacks to avoid ITAR constraints. Companies devote up to 20% of AI project budgets to compliance, and multi-national projects often slip 12–18 months while clearances are negotiated.

Cyber supply-chain threats undermine trust

SolarWinds-style attacks increasingly target model repositories and ML pipelines, embedding malicious code in popular open-source libraries.[4]CISA Analysts, “Software Supply-Chain Security Guidance for Developers,” CISA, cisa.gov DoD guidelines now mandate zero-trust architectures and formal verification of critical ML models. Several primes have transitioned to air-gapped training environments, raising costs and slowing iteration. Long-term remedies emphasize secure enclaves, continuous behavior monitoring, and digital-signature validation of every model update.

Segment Analysis

By Offering: Software Dominates While Services Accelerate

Software maintained 53.33% of 2024 revenue, reflecting the centrality of algorithms, data-fusion engines, and autonomy frameworks to every major platform. For instance, Palantir’s tactical intelligence platform underpinned multi-billion-USD defense awards in 2024. In value terms, the AI in aerospace and defense market size for software eclipsed USD 14 billion and is projected to climb at a 7.90% CAGR. Hardware trails as component commoditization offsets unit-volume gains.

The services line, however, will outpace all other categories at 9.87% CAGR through 2030 as customers lean on integration specialists to harden AI models for certification, connect legacy avionics, and operate AI-at-scale across hybrid clouds. Training-and-simulation services, underpinned by adaptive AI flight instructors, record double-digit billings, mirroring the military’s emphasis on ready-now pilots.

Note: Segment shares of all individual segments available upon report purchase

By Application: Space Surges Past a Strong Military Base

Military programs delivered 45.16% of 2024 revenue and are slated to grow 8.1% annually as manned–unmanned teaming, electronic warfare automation, and battle-management AI mature. Deep-space exploration and autonomous satellite constellations elevate the space segment, driving the fastest 10.7% CAGR. The AI in the aerospace and defense market thus pivots from predominantly terrestrial defense toward a broader orbit-centric profile.

Spacecraft now use embedded AI for terrain-relative navigation on the lunar surface, spacecraft health management, and onboard collision avoidance. NASA’s Perseverance rover relies on computer vision to steer across Martian obstacles. Parallel advances in launch cadence and small-sat economics magnify the opportunity, as each craft requires certified processors and AI toolchains.

By End-User: Agencies and New-Space Ventures Gain Ground

OEMs and Tier-1 suppliers controlled 38.55% of the total 2024 spending. Their dominance stems from embedding AI in design loops—from generative airframe optimization to robotic fastener inspection. Nonetheless, space agencies and venture-backed operators will record the fastest 8.91% CAGR, with mega-constellation owners procuring autonomous station-keeping, payload tasking, and inter-satellite routing as managed services.

Defense primes, meanwhile, expand platform life-cycle support, bundling AI upgrades with sustainment contracts. Airlines exploit revenue-management AI to realign fleets post-pandemic, while MRO houses turn to vision-based part inspection to shrink turnaround time.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America retained a 33.45% share of the AI market in aerospace and defense in 2024, buoyed by the United States' USD 1.8 billion FY-25 defense-AI budget, a robust venture ecosystem, and extensive university partnerships. Boeing’s collaboration with Microsoft Azure Government provides classified cloud training pipelines, while CAE Canada delivers AI-enabled flight-training devices globally. The region’s 7.8% historical CAGR is expected to rise 8.2% through 2030 as production programs come online and export demand for autonomous systems grows.

The Middle East is emerging as the fastest-growing theater, with a 9.31% forecasted CAGR on the back of sovereign AI roadmaps and defense-modernization funds. The UAE’s Mohammed bin Rashid Space Centre operates fully AI-driven Earth-observation scheduling, and Saudi Arabia has earmarked USD 20 billion for NEOM’s autonomous-aviation spine. Israel’s defense tech base continues to deliver world-class electronic-warfare AI, feeding export channels across the region.

Europe and Asia-Pacific maintain complementary strengths. Europe channels EUR 1.2 billion (USD 1.4 billion) from its European Defence Fund into collaborative AI for the Future Combat Air System. At the same time, Airbus and Dassault push common data fabrics for multi-domain operations. Iapan’s Global Combat Air Programme, India’s Indigenous AI radar, and China’s self-navigating UAV swarms illustrate escalating investment. In Asia-Pacific, both regions target balanced growth above 8% as civil aviation recovery meets national security imperatives.

Competitive Landscape

Legacy primes, such as The Boeing Company, Airbus SE, Lockheed Martin Corporation, and International Business Machines Corporation, maintain scale advantages in certification, system integration, and global sustainment networks. Yet software-native Anduril, Shield AI, and Helsing capture share by emphasizing modular autonomy stacks and rapid fielding cycles. Anduril’s 2024 purchase of Numerica’s radar business folds high-fidelity tracking into its Lattice OS, underscoring the strategic premium on sensor-fusion IP.

Partnerships dominate as incumbents seek algorithm talent: Airbus allied with Helsing to co-develop manned–unmanned teaming logic. At the same time, RTX invested in JetZero’s blended-wing demonstrator to couple advanced aerodynamics with AI-based flight controls. Private-equity capital flows into edge-hardware specialists and certifiable ML-ops toolkits, increasing competitive churn. Certification speed, data-sovereignty assurances, and open-architecture compliance are primary differentiators rather than production volume alone.

White-space opportunities include neuromorphic processing for deep-space missions, low-SWaP autonomy kits for attritable drones, and cockpit voice agents powered by large-language models. Consolidation is likely: Honeywell’s USD 1.9 billion acquisition of CAES, Safran’s EUR 220 million (USD 259.6 million) purchase of Preligens, and AeroVironment’s USD 4.1 billion deal for BlueHalo signal continuing roll-ups aimed at vertically integrating AI capabilities across sensing, effectors, and C2.

AI In Aerospace And Defense Industry Leaders

-

Lockheed Martin Corporation

-

Airbus SE

-

Northrop Grumman Corporation

-

The Boeing Company

-

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Saab flew a Gripen E under Helsing’s Centaur AI, achieving autonomous BVR engagement during combat trials.

- March 2025: Lockheed Martin expanded its Google Cloud pact to enable real-time AI geospatial analytics.

- February 2025: L3Harris partnered with Shield AI to co-develop autonomy kits for military aircraft.

- September 2024: Honeywell closed a USD 1.9 billion buyout of CAES, expanding AI avionics and space portfolios.

Global AI In Aerospace And Defense Market Report Scope

Artificial intelligence is the simulation of human intelligence processes by machines, especially computer systems. The A&D industry is adopting robotic technologies powered by sophisticated AI-driven technologies to improve overall equipment efficiency (OEE) and first-pass yield in production.

The scope of the study includes the use of artificial intelligence and robotics for various applications in aerospace and defense. Some of the important aspects covered in the study are the use of AI and robotics in the manufacturing of aircraft, operations and fleet management, and other applications by airlines, such as airport operations (like passenger handling, aircraft monitoring, inventory management, and others) and military applications (defense communications systems, unmanned systems and intelligence, surveillance, and reconnaissance applications, among others). The market is segmented by offering into hardware, software, and service and by application into military, commercial aviation, and space. The report also covers the market sizes and forecasts for artificial intelligence and robotics in the aerospace and defense markets across major regions. For each segment, the market sizing and forecasts have been done based on value (USD billion).

| By Offering | Hardware | AI Processors and Accelerators | ||

| Sensors and Avionics | ||||

| Robotic Platforms | ||||

| Edge Devices and Embedded Systems | ||||

| Software | AI/ML Platforms | |||

| Autonomy and Flight Control Algorithms | ||||

| Predictive Maintenance Analytics | ||||

| ISR and Mission Software Suites | ||||

| Services | Integration and Consulting | |||

| MRO and Predictive Maintenance Services | ||||

| Training and Simulation Services | ||||

| Managed Cloud and Edge Services | ||||

| By Application | Defense | C4ISR | ||

| Autonomous Weapons and Combat Systems | ||||

| Logistics and Maintenance | ||||

| Commercial Aviation | Flight Operations and ATC | |||

| Aircraft Manufacturing and Assembly | ||||

| MRO | ||||

| Space | Satellite Operations and Autonomy | |||

| Planetary Exploration Robotics | ||||

| Space Situational Awareness | ||||

| By End-User | Defense Primes | |||

| Airlines and MRO Providers | ||||

| Space Agencies and Commercial Operators | ||||

| OEMs and Tier-1 Suppliers | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | United Kingdom | |||

| Germany | ||||

| France | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Australia | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Rest of South America | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| UAE | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Rest of Africa | ||||

| Hardware | AI Processors and Accelerators |

| Sensors and Avionics | |

| Robotic Platforms | |

| Edge Devices and Embedded Systems | |

| Software | AI/ML Platforms |

| Autonomy and Flight Control Algorithms | |

| Predictive Maintenance Analytics | |

| ISR and Mission Software Suites | |

| Services | Integration and Consulting |

| MRO and Predictive Maintenance Services | |

| Training and Simulation Services | |

| Managed Cloud and Edge Services |

| Defense | C4ISR |

| Autonomous Weapons and Combat Systems | |

| Logistics and Maintenance | |

| Commercial Aviation | Flight Operations and ATC |

| Aircraft Manufacturing and Assembly | |

| MRO | |

| Space | Satellite Operations and Autonomy |

| Planetary Exploration Robotics | |

| Space Situational Awareness |

| Defense Primes |

| Airlines and MRO Providers |

| Space Agencies and Commercial Operators |

| OEMs and Tier-1 Suppliers |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the AI in aerospace and defense market today?

The market generated USD 27.91 billion in 2025 and is projected to reach USD 42.67 billion by 2030 at an 8.86% CAGR.

Which segment of the AI in aerospace and defense industry is growing the fastest?

Services, particularly integration and managed-AI offerings, are forecasted to expand at 9.87% CAGR as operators seek certified deployment expertise.

What region offers the highest growth potential?

The Middle East leads with a 9.31% forecasted CAGR, propelled by sovereign AI roadmaps and major defense-modernization budgets.

How significant is predictive maintenance in the AI in aerospace and defense market?

Airline deployments show 20-30% fewer unscheduled events and up to 15% lower aircraft-on-ground time, underscoring predictive maintenance as a primary ROI driver.

Which companies are disrupting incumbents?

Software-native entrants like Anduril, Shield AI, and Helsing leverage modular autonomy stacks and rapid iterations to win programs that previously defaulted to large primes.

What certification hurdles exist for AI hardware in space?

Radiation tolerance, fault-management protocols, and multi-year qualification campaigns are mandatory; AMD’s Versal and BrainChip’s Akida recently cleared such milestones, unlocking in-orbit inference.

Page last updated on: July 2, 2025