Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

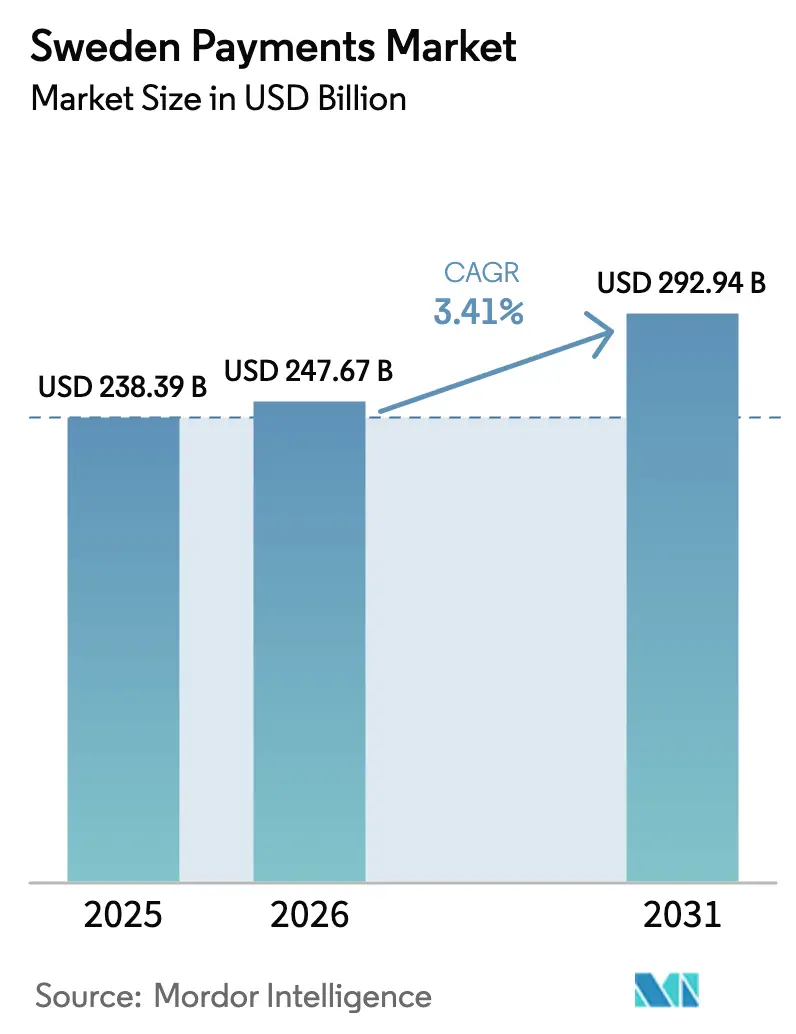

| Base Year Market Size (2025) | USD 238.39 Billion |

| Market Size (2026) | USD 247.67 Billion |

| Market Size (2031) | USD 292.94 Billion |

| Growth Rate (2026 - 2031) | 3.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Payments Market Analysis by Mordor Intelligence

The Sweden payments market size was valued at USD 238.39 billion in 2025 and is estimated to grow from USD 247.67 billion in 2026 to reach USD 292.94 billion by 2031, at a CAGR of 3.41% during the forecast period 2026-2031. Momentum remains steady because the nation already records cash usage below 10% of point-of-sale turnover and has near-universal smartphone penetration. Growth now rests on elevating cross-border acceptance, closing rural connectivity gaps, and curbing push-payment fraud rather than on persuading new demographics to abandon notes and coins. Competitive dynamics are shaped by Swish’s ubiquity in domestic transfers, card-network efforts to defend interchange with tokenization, and fintech moves to embed high-margin services such as subscription management and stablecoin settlement. Regulatory initiatives, including the e-krona pilot and the European Banking Authority’s payee-name verification mandate, will either accelerate or restrain digital migration depending on their success in balancing security with compliance cost.

Key Report Takeaways

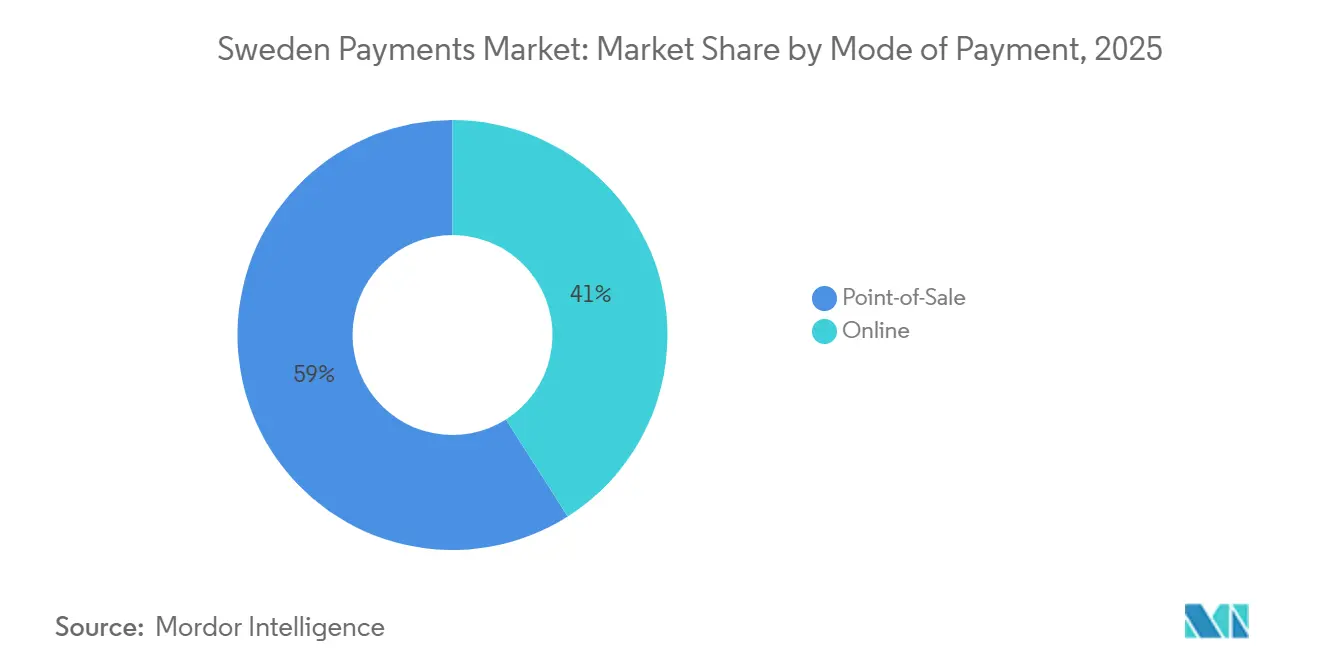

- By mode of payment, point-of-sale channels held 60.17% of Sweden payments market share in 2025 while online sale is expected to post the quickest expansion at a 4.03% CAGR through 2031.

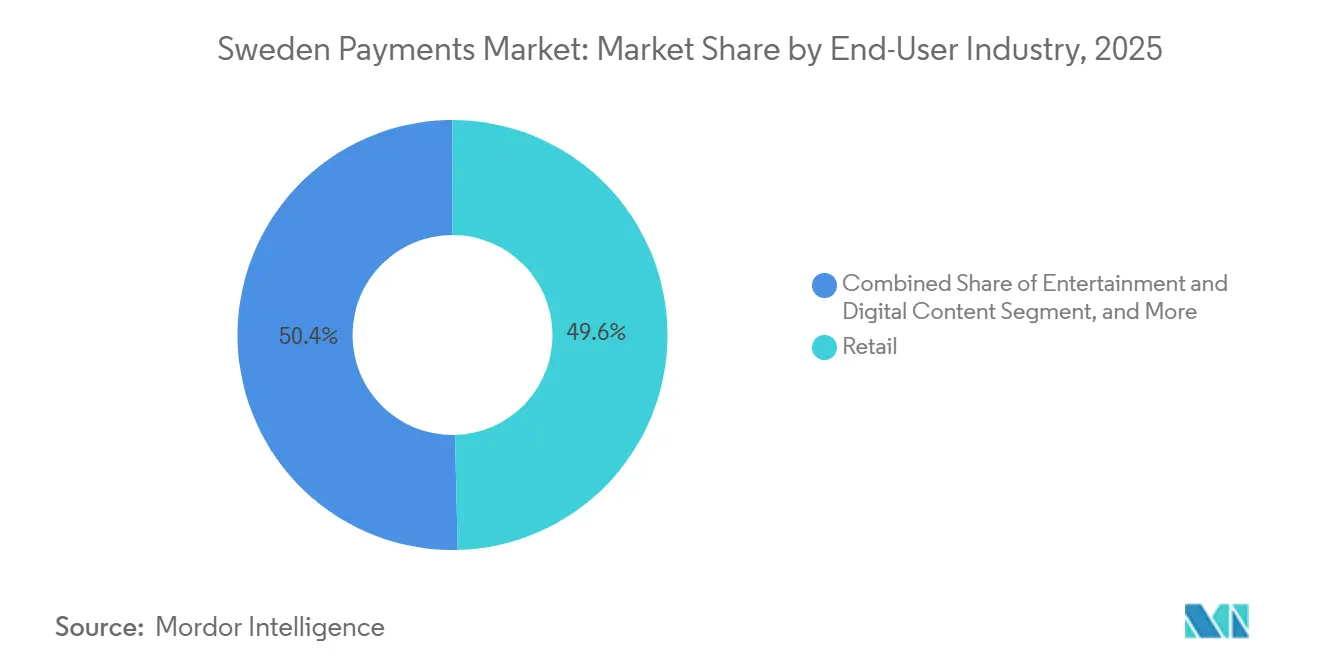

- By end-user industry, retail accounted for 49.61% of the Sweden payments market size in 2025 whereas healthcare is projected to register the highest growth at 4.57% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Sweden Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Proliferation and Cross-Border Shopping Driving Higher Digital Spend | +0.8% | National and Nordic hubs | Medium term (2-4 years) |

| National Instant-Payment Rail Swish Hitting 9 of 10 Adults, Catalyzing Account-to-Account Retail Payments | +0.7% | Urban and suburban Sweden | Short term (≤ 2 years) |

| Riksbank e-krona Pilot Strengthening Confidence in a Cash-Lite Future | +0.4% | Major cities | Long term (≥ 4 years) |

| Merchant Adoption of SoftPOS and Tap-to-Phone in SME Segment | +0.5% | Nationwide with SME focus | Medium term (2-4 years) |

| Nordic Interchange Caps Lowering Acceptance Cost for Micro-Ticket Segments | +0.3% | Nationwide | Medium term (2-4 years) |

| Growth of Embedded-Finance Checkout in Swedish SaaS Platforms | +0.4% | National with Nordic export | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Proliferation and Cross-Border Shopping Driving Higher Digital Spend

Swedish online transaction value climbed to SEK 140 billion (USD 13.33 billion) in 2024, helped by a one-click checkout experience that blends Swish for domestic buyers with foreign alternatives such as Bancontact and iDEAL.[1]PostNord Research Team, “E-barometern 2024,” PostNord, postnord.se Klarna now processes more than 2 million daily embedded-checkout transactions across 45 countries, trimming merchant onboarding from weeks to hours and cutting acceptance cost by up to 50 basis points. The convenience widens the Sweden payments market because micro-ticket retailers can funnel savings into promotion budgets that attract incremental shoppers. Yet Swedish banks charge an average 3.5% fee on cross-border credit transfers, a premium that invites stablecoin rails to displace legacy corridors and siphon volume.[2]Riksbank Analysts, “Payments in Sweden 2024,” Riksbank, riksbank.se

National Instant-Payment Rail Swish Hitting 9 of 10 Adults

Swish reached 8.5 million active users in December 2024 and moved 1 billion transactions in 2023, confirming its role as the default person-to-person and merchant instrument.[3]Getswish AB, “Swish Annual Report 2024,” Getswish, getswish.se February 2024 migration to RIX-INST lowered settlement latency to less than 3 seconds, enabling usage in quick-service restaurants and metro ticketing where queues must clear rapidly. A flat SEK 3 merchant fee makes Swish cheaper than debit cards for tickets under SEK 150 (USD 16.8), prompting small outlets to promote QR acceptance. Card schemes reply with tokenization and biometrics, aiming to secure premium interchange on higher-value baskets.

Merchant Adoption of SoftPOS and Tap-to-Phone in the SME Segment

SoftPOS converts Android devices into contactless readers at zero hardware cost, a proposition that reached 12,000 active Swedish merchants by late 2024. Elavon and Softpay reduced onboarding to ten minutes, enticing sole traders such as electricians and hairdressers who previously stayed cash-only.[4]Elavon Nordic Unit, “Softpay Partnership Announcement,” Elavon, elavon.com Swedbank Pay extended similar functionality in June 2024 bundled with working-capital loans, illustrating a path for banks to monetize embedded paymentsE. Liability for lost or stolen phones still deters some merchants, so uptake will hinge on insurance products and improved mobile-OS security.

Riksbank e-krona Pilot Strengthening Confidence in a Cash-Lite Future

The e-krona pilot entered phase 3 in 2024 with offline capability, programmable payments, and voice navigation intended for visually impaired and elderly users. Although issuance remains undecided, the test clarifies that public access to central-bank money will persist even if physical cash circulation falls further. A successful launch could neutralize demographic resistance by allowing zero-fee peer-to-peer transfers and instant government disbursements, therefore expanding the Sweden payments market. Interaction with the prospective digital euro may accelerate timelines, ensuring Nordic-EU interoperability and avoiding fragmentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rural Cash Dependency Among Age 70+ and Differently-Abled Consumers | -0.3% | Norrland, Dalarna, rural Småland | Long term (≥ 4 years) |

| Rising Fraud in Push-Payment and BNPL Transactions Eroding Trust | -0.5% | Major metropolitan areas | Short term (≤ 2 years) |

| High Network Fees on Corporate Purchasing Cards Limiting B2B Migration | -0.2% | Nationwide corporates | Medium term (2-4 years) |

| Limited Interoperability Between National QR Schemes and EU-wide Solutions | -0.2% | Tourism and e-commerce flows | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rural Cash Dependency Among Older and Differently-Abled Consumers

One-fifth of residents aged 70 and above withdrew cash weekly in 2024 while ATM density in several northern counties dropped below 5 machines per 100,000 inhabitants. Bank branch closures make seniors travel an average 22 kilometers for basic services, entrenching reliance on notes. Screen-reader shortcomings and absent audio cues on many terminals further disadvantage visually impaired shoppers. The Post and Telecom Authority now requires all payment apps to meet WCAG 2.1 AA by January 2026, yet until adoption is universal, demographic exclusion will dampen Sweden payments market expansion.

Rising Fraud in Push-Payment and BNPL Transactions

Authorized push-payment scams and buy-now-pay-later delinquencies cost households and merchants SEK 7.5 billion (USD 714.29 million) in 2024, up 22% from the prior biennium. The European Banking Authority’s payee-name verification rule for transfers over EUR 100 (USD 110) takes effect in October 2025, compelling banks to invest SEK 450 million (USD 50.4 million) in real-time IBAN checks. While strong customer authentication shrank card-not-present fraud by 18% over 2021-2024, scams exploiting human error remain unchecked. Consumer wariness therefore restrains instant-payment uptake, slowing the Sweden payments market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Instant Rails Anchor Physical Commerce

Point-of-sale transactions represented 60.17% of Sweden payments market share in 2025 as contactless terminals and Swish QR codes permeated brick-and-mortar stores. Debit cards dominate within this channel because salaries flow directly into checking accounts, allowing low-cost direct-debit usage. Credit cards support business travel and big-ticket retail but remain a niche relative to other European markets. Digital wallets such as Apple Pay held roughly 15% of point-of-sale value on the back of near-universal NFC acceptance and biometric log-in convenience.

Online sale contributes the fastest incremental value. The segment is forecast to expand at a 4.03% CAGR through 2031, propelled by cross-border shopping, embedded checkout, and Swish integrations that shorten settlement from days to seconds. Card payments still lead but their weight is sliding as BNPL and tokenized wallets eliminate form-fill friction. Stripe’s 2024 decision to add Swish trimmed cross-border fees by 120 basis points, making instant bank transfer affordable even for foreign merchants. Invoice payment remains a Swedish quirk favored by electronics and furniture buyers who value the option to inspect goods before remitting.

By End-User Industry: Retail Maturity, Healthcare Momentum

Retail controlled 49.61% of the Sweden payments market size in 2025 after grocery chains and fashion outlets deployed QR checkout and contactless card readers well ahead of continental peers. Loyalty programs within these chains also encouraged wallet adoption, sealing habitual behavior changes. Despite saturation, incremental growth persists as foreign apparel platforms localize Swish and Klarna buttons.

Healthcare shows a 4.57% CAGR outlook, the fastest across industries, because telehealth portals now clear copays in real time and pharmacies shifted one-quarter of prescription sales online. Regional pilots that integrated billing with patient records trimmed administrative overhead by 18% and slashed payment cycles from 21 days to under 5 days, freeing hospital working capital. The eHealth Agency’s 2025 mandate for interoperable portals will extend similar efficiencies to dental and elder-care segments, sustaining Sweden payments market expansion.

Geography Analysis

Urban centers drive transaction density. Stockholm, Gothenburg, and Malmö together hold roughly 55% of digital-payment value while accounting for 40% of the population. Smartphone ownership in Stockholm hit 94% in 2024, and NFC acceptance surpassed 98% of physical outlets, producing a feedback loop that normalizes cashless behavior. Swish merchant density in cities stands at 12 locations per 1,000 residents compared with 4 in rural districts. The European Payments Council memorandum signed in February 2026 seeks to extend this interoperability across borders, promising to cut cross-border costs by up to 200 basis points once standards converge.

Rural municipalities lag because branch closures and patchy mobile coverage hinder real-time authentication. Nine percent of rural respondents reported failed digital payments in 2024 due to connectivity gaps. Offline e-krona prototypes aim to bridge that divide by storing credentials locally, yet commercial rollout is years away. Until then, older residents continue weekly cash withdrawals that dilute Sweden payments market efficiency.

Cross-border friction further shapes geography. Banks charge 3.5% for European Economic Area transfers, surpassing the EU average of 1.4% and hurting exporters that remit to Germany, Poland, and the Netherlands. Tourists also face elevated card-scheme fees near 4% on corporate cards, depressing B2B acceptance. Stripe’s Swish integration lowered those costs, but a full solution awaits harmonized instant rails under the European Payment Area project.

Competitive Landscape

The top five participants, Klarna, Getswish, Visa, Mastercard, and Adyen, collectively capture around 60% of 2025 transaction value, indicating moderate concentration. Card networks and global acquirers protect cross-border and high-value flows while Swish dominates domestic peer-to-peer volume. Mastercard’s 2024 purchase of Minna Technologies embeds subscription-management into its stack, showcasing a shift to value-added ecosystems rather than pure payment plumbing. Klarna responded by introducing peer-to-peer transfers and launching a USD-pegged stablecoin to capture deposit float and foreign-exchange spread, signaling convergence between BNPL and full-service banking.

SoftPOS innovators such as Elavon and Swedbank Pay attack micro-merchant acceptance costs. Their tap-to-phone solutions eliminate hardware fees, unlocking new merchants and broadening the Sweden payments market. Visa’s tokenization cut card-not-present fraud by 18% in three years, underscoring security as a differentiator. Regulatory costs may thin the field; mandatory IBAN-name checks require SEK 450 million (USD 50.4 million) in bank investment, an outlay that smaller acquirers may struggle to absorb.

White-space persists in B2B payments. Sixty percent of domestic invoices travel on open-credit terms and one-third arrive overdue, revealing demand for dynamic discounting and supply-chain finance. Providers that bundle compliance, financing, and payment in one API stand positioned to win incremental Sweden payments market share.

Sweden Payments Industry Leaders

Qred AB

Getswish AB

Stripe, Inc.

2Checkout (Verifone, Inc.)

PayPal Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The European Payments Council signed a memorandum to create the European Payment Area, aligning Swish, Vipps MobilePay, and other Nordic schemes for QR standardization and cross-border instant transfers by 2028.

- January 2026: Klarna introduced peer-to-peer transfers inside its Swedish app, permitting phone number or email-based money movement without bank-account disclosure.

- November 2025: Klarna launched KlarnaUSD, a USD-pegged stablecoin on Ethereum to expedite merchant settlement and mitigate foreign-exchange volatility.

- October 2025: The European Payments Council rolled out payee-name verification across 15 EU states including Sweden, obliging banks to deliver real-time IBAN-name matching on transfers over EUR 100 (USD 110).

Sweden Payments Market Report Scope

The Swedish payment market can be divided into two payment types: POS and e-commerce. E-commerce payments include online purchases of goods and services, such as purchases on e-commerce websites and online booking of travel and accommodation. As far as POS is concerned, all transactions made at the time of physical sale are within the scope of the market, such as credit and debit card payments and more. This includes all face-to-face transactions, regardless of where they occur, not just traditional in-store transactions. Cash is also considered for both cases (cash-on-delivery for e-commerce sales).

The Sweden Payments Market Report is Segmented by Mode of Payment (Point-of-Sale including Card Payments and Digital Wallets, Online Sale including Card Payments and Digital Wallets), End-user Industry (Retail, Entertainment and Digital Content, Healthcare, Hospitality and Travel, Government and Utilities), and Geography (Sweden). The Market Forecasts are Provided in Terms of Value (USD).

Segmentation by Mode of Payment

| Point-of-Sale | Card Payments | Debit Cards |

| Credit Cards | ||

| Bank Financing Prepaid Cards | ||

| Digital Wallets (includes Mobile Wallet) | ||

| Other Point-of-Sale | ||

| Online Sale | Card Payments | Debit Cards |

| Credit Cards | ||

| Bank Financing Prepaid Cards | ||

| Digital Wallets | ||

| Other Online Sales (includes Cash on Delivery, Bank Transfer, and Buy Now Pay Later) |

By End-user Industry

| Retail |

| Entertainment and Digital Content |

| Healthcare |

| Hospitality and Travel |

| Government and Utilities |

| Other End-user Industries |

| Segmentation by Mode of Payment | Point-of-Sale | Card Payments | Debit Cards |

| Credit Cards | |||

| Bank Financing Prepaid Cards | |||

| Digital Wallets (includes Mobile Wallet) | |||

| Other Point-of-Sale | |||

| Online Sale | Card Payments | Debit Cards | |

| Credit Cards | |||

| Bank Financing Prepaid Cards | |||

| Digital Wallets | |||

| Other Online Sales (includes Cash on Delivery, Bank Transfer, and Buy Now Pay Later) | |||

| By End-user Industry | Retail | ||

| Entertainment and Digital Content | |||

| Healthcare | |||

| Hospitality and Travel | |||

| Government and Utilities | |||

| Other End-user Industries | |||

Key Questions Answered in the Report

How large is the Sweden payments market in 2026?

The Sweden payments market size is valued at USD 247.67 billion in 2026, on track to reach USD 292.94 billion by 2031.

What growth rate is expected for Sweden's digital payments through 2031?

The market is projected to grow at a 3.41% CAGR for the 2026-2031 period.

Which payment channel holds the largest share in Sweden?

Point-of-sale transactions lead with 60.17% of Sweden payments market share as of 2025.

Which end-user sector is growing fastest for payments?

Healthcare payments exhibit the quickest rise with a 4.57% CAGR projected through 2031.

Why is fraud considered a key restraint in Sweden's payment landscape?

Push-payment scams and BNPL delinquencies cost SEK 7.5 billion (USD 714.29 million) in 2024, eroding consumer trust and slowing instant-payment adoption.

How will the European Payment Area initiative influence Sweden?

Harmonized QR standards and cross-border instant transfers planned by 2028 could shave 150-200 basis points from international transaction costs, expanding e-commerce volume.

Page last updated on: