Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

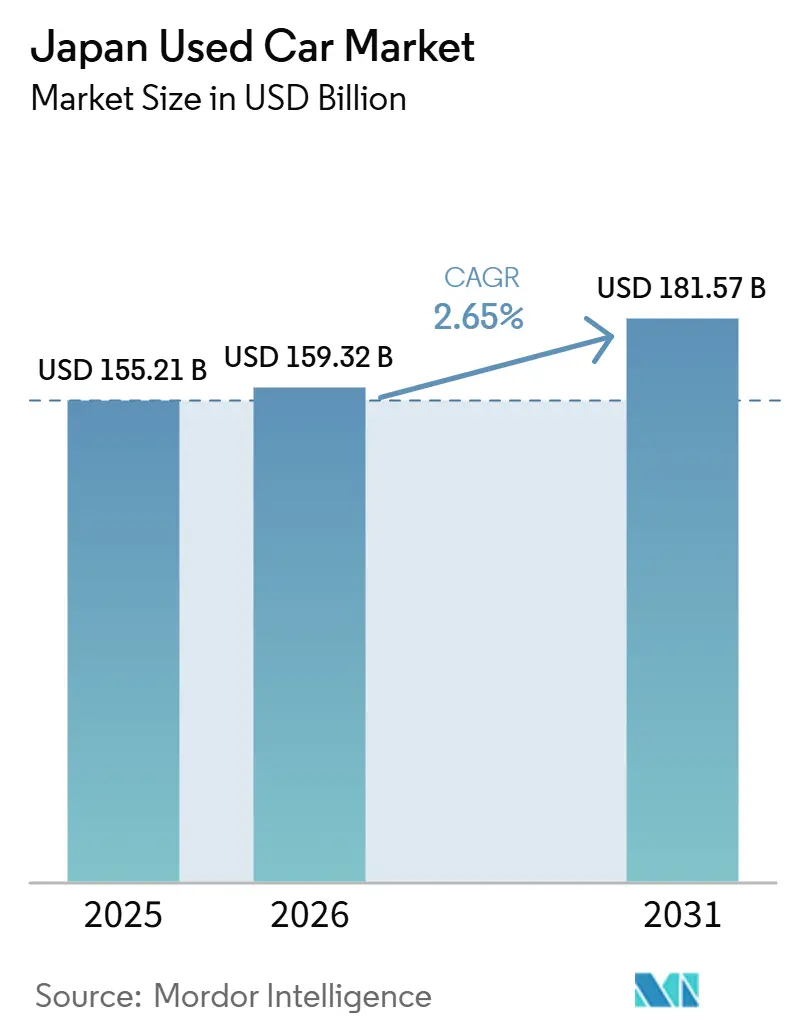

| Base Year Market Size (2025) | USD 155.21 Billion |

| Market Size (2026) | USD 159.32 Billion |

| Market Size (2031) | USD 181.57 Billion |

| Growth Rate (2026 - 2031) | 2.65% CAGR |

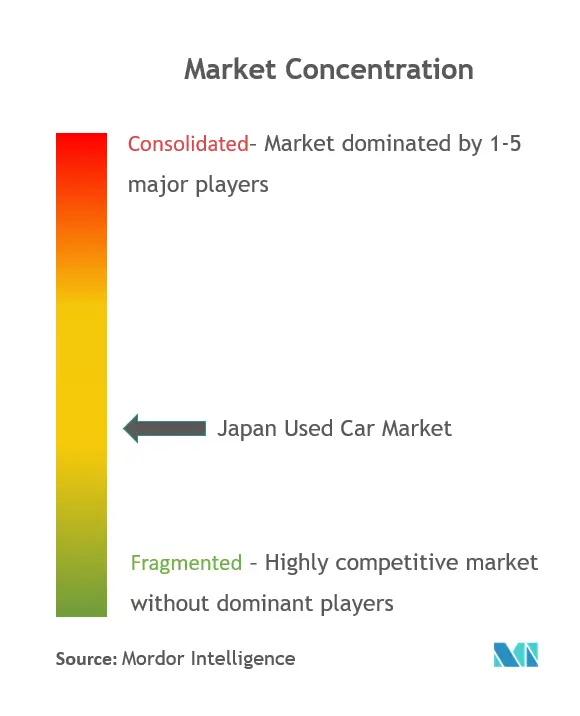

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Used Car Market Analysis by Mordor Intelligence

The Japan used car market size is expected to grow from USD 155.21 billion in 2025 to USD 159.32 billion in 2026, and is forecast to reach USD 181.57 billion by 2031, at a 2.65% CAGR over 2026-2031. Elevated new-car prices have widened the affordability gap, guiding budget-sensitive buyers toward pre-owned vehicles. A steady flow of three-year-old lease returns is adding late-model inventory with advanced safety and connectivity features. Digital marketplaces now connect dealers and consumers nationwide, erasing many local stock constraints. Meanwhile, government electrification targets and battery subsidies are beginning to shape future secondary-market supply as early electric vehicles enter resale channels.

Key Report Takeaways

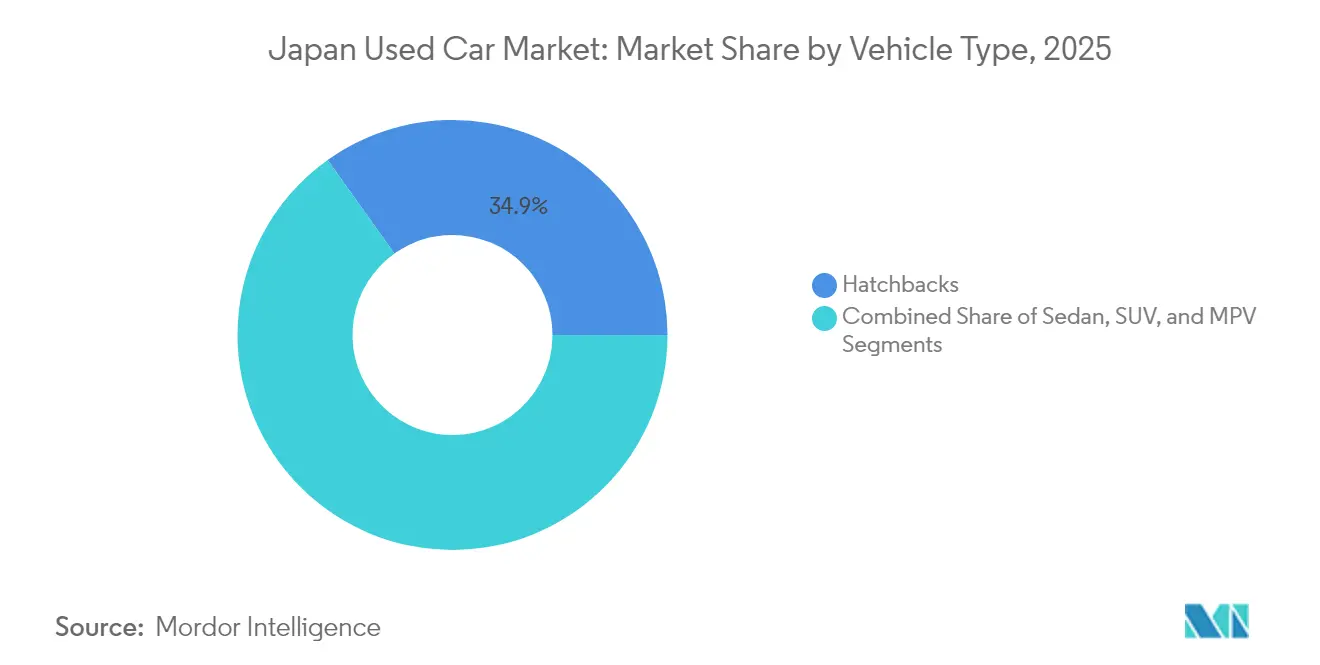

- By vehicle type, hatchbacks led with a 34.86% revenue share in 2025, while SUVs are on track for the highest segment growth at a 6.02% CAGR through 2031.

- By fuel type, gasoline cars accounted for 53.92% of 2025 revenue; electric vehicles are projected to grow at a 14.15% CAGR through 2031.

- By vehicle age, the 3-5-year bracket accounted for 44.35% of 2025 transactions; 0-3-year units are the fastest-growing age group at a 6.88% CAGR.

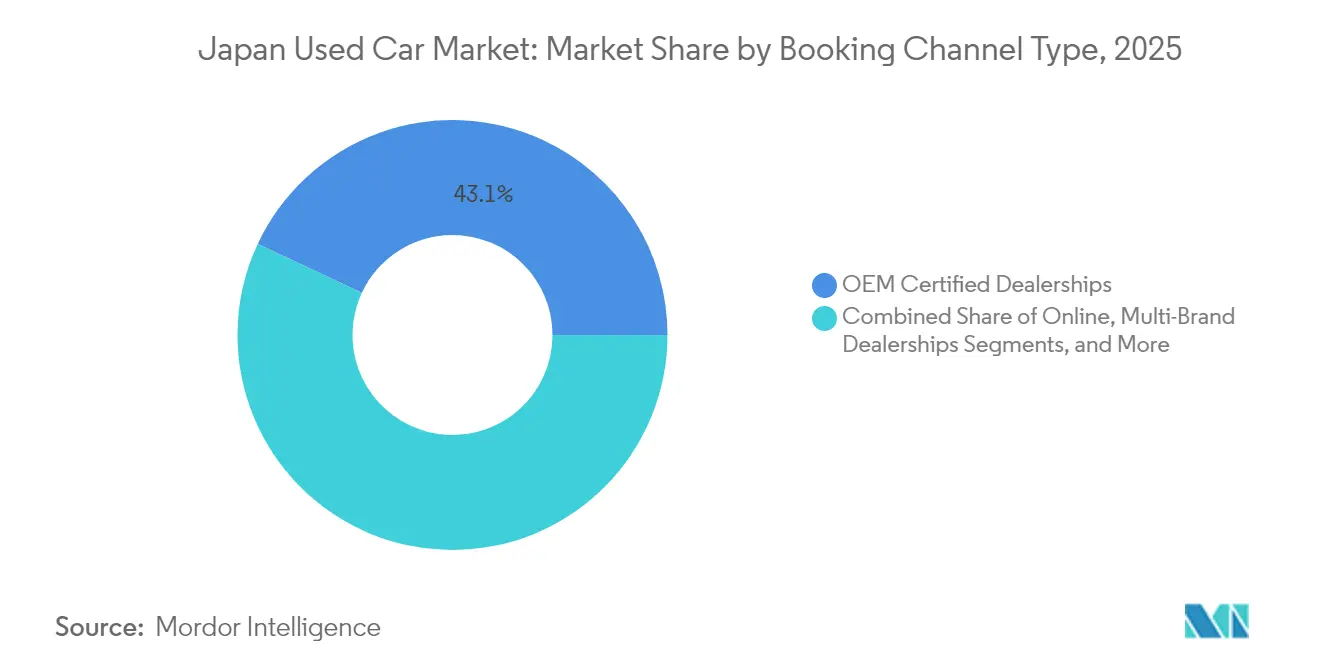

- By booking channel, OEM-certified dealerships controlled 43.05% of 2025 sales; online platforms will rise at an 10.74% CAGR through 2031.

- By transaction type, full-payment purchases maintained a 63.72% share in 2025, while financed deals are forecast to advance at a 8.95% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring New-car Prices Widen Affordability Gap | +0.5% | National, Concentrated in Urban Centers | Short term (≤ 2 years) |

| Accelerated 3-year Depreciation Cycles Release High-quality Stock | +0.4% | National, with Spillover to Export Markets | Medium term (2-4 years) |

| Online-first Dealer Platforms Scale Nationwide Inventory | +0.3% | National, Early Gains in Metropolitan Areas | Medium term (2-4 years) |

| Kei-car Tax Advantage Sustains Demand for Used Micro-cars | +0.3% | National, Stronger in Rural Regions | Long term (≥ 4 years) |

| End-of-lease OEM Subscription Fleets Flood Secondary Market | +0.2% | National, Concentrated Near Urban Lease Centers | Short term (≤ 2 years) |

| Circular-economy Incentives Favor Vehicle Reuse Over Scrappage | +0.2% | National, Aligned with Government Sustainability Goals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring New Car Prices Widen Affordability Gap

Persistently high factory-gate prices have shifted buyers toward used vehicles, a trend reinforced by a 2.5–3% CPI outlook, which keeps new-car ownership out of reach for many households.[1]“Outlook for Economic Activity and Prices,”, Bank of Japan, boj.or.jp Toyota’s FY2025 domestic volume fell by 10.8%, underscoring price resistance and shifting demand toward pre-owned channels. Late-model cars in the 3-5-year bracket now combine modern driver-assistance features with lower capital costs, strengthening their appeal. As wages inch upward but still trail vehicle inflation, the Japanese used car market continues to absorb buyers who might otherwise delay purchasing.

Accelerated 3 Year Depreciation Cycles Release High Quality Stock

Corporate fleet programs and subscription models have shortened replacement intervals, sending newer, low-mileage vehicles into resale lanes every 36 months. Honda and Mitsubishi’s ALTNA joint venture exemplifies this pattern by leasing batteries and repurposing returned EVs.[2]“ALTNA Joint Venture Announcement,”, Mitsubishi Corporation, mitsubishicorp.com Tokyo Century’s automobility division posted record earnings in 2024, reflecting brisk secondary-market turnover of these high-spec units. The resulting breadth of inventory bolsters consumer confidence and limits price spikes, even when new-car supply remains tight.

Online First Dealer Platforms Scale Nationwide Inventory

E-commerce acceptance—evident in a JPY 24.8 trillion (~USD 0.15 trillion) B2C market—has migrated to automotive retail, enabling shoppers in Hokkaido and Kyushu to browse Kanto-based stock via mobile apps.[3]“Clean Energy Vehicle Subsidy Guidelines,”, Ministry of Economy, Trade and Industry, meti.go.jp Virtual inspections, integrated financing, and home delivery reduce transaction time, enhancing the platform's competitiveness against brick-and-mortar dealerships. As digital network effects deepen, the Japanese used-car market is becoming less geographically fragmented, enabling price discovery on a national scale.

Kei Car Tax Advantage Sustains Demand for Used Micro Cars

Preferential taxes keep kei-cars attractive for rural households and small businesses. April 2025 registration data show Honda N-BOX and Suzuki Spacia topping charts, evidence that supply continues to funnel into secondary channels.[4]“Monthly Kei-Car Registration Data,”, National Light Vehicle Association, zenkeijikyo.or.jp Fuel-efficient 660 cc powertrains align with carbon goals while keeping the total cost of ownership well below that of compact imports. As these micro-cars age, their residual values remain firm, ensuring steady turnover within the Japanese used car market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight Domestic Supply After Pandemic-era Production Cuts | -0.6% | National, with Regional Inventory Imbalances | Short term (≤ 2 years) |

| Odometer Fraud Scandals Erode Consumer Trust | -0.4% | National, Concentrated in Dealer Network Segments | Medium term (2-4 years) |

| Shrinking Licensed-driver Pool Amid Rapid Ageing | -0.3% | National, More Pronounced in Rural Areas | Long term (≥ 4 years) |

| Stricter 2027 Emission Norms May De-value Older ICE Stock | -0.3% | National, Urban Areas with Stricter Enforcement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tight Domestic Supply After Pandemic Era Production Cuts

Japanese output touched a 45-year low of 7.85 million units in 2021, and those missing vehicles are now absent from the 3-5 year-old pool. With fewer trade-ins and lease returns entering the auction market, wholesale prices have firmed, forcing retailers to seek right-hand-drive imports abroad. Although overseas production rebounded, domestic scarcity still limits stock diversity, slowing growth in the Japanese used car market.

Odometer Fraud Scandals Erode Consumer Trust

High-profile mileage-tampering cases have prompted the transport ministry to tighten inspection rules and revoke licenses of non-compliant workshops. Itochu’s acquisition and rebranding of a major offender required USD 256 million in remediation and compliance upgrades. Added verification costs and stricter disclosure protocols slow transaction velocity and pressure smaller dealers, challenging short-term expansion in the Japanese used car market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUV Growth Challenges, Hatchback Dominance

Hatchbacks retained a 34.86% share of the Japanese used car market in 2025, anchored by tight urban parking and narrow streets. Compact SUVs, however, are set to post a 6.02% CAGR to 2031, propelled by lifestyle shifts toward higher seating and versatile cargo layouts. Used-car auctions now list more late-model SUVs as three-year depreciation cycles deliver stock with autonomous-driving aids and infotainment upgrades.

Rural migration to urban centers supports hatchback turnover, yet rising disposable income among young families favors two-row crossovers that combine maneuverability with extra ride height. Dealers stocking both categories hedge risk while capturing the broadening taste spectrum in the Japanese used car market.

By Fuel Type: Electric Surge Disrupts Gasoline Hegemony

Gasoline vehicles held 53.92% of 2025 sales, but battery electric and plug-in hybrids will clip that lead by 14.15% annually to 2031. Government rebates of up to JPY 850,000 per EV lower entry barriers. The Japanese used car market for electric models will expand rapidly once the current fleet leases mature.

Battery-leasing schemes address resale-value anxiety, providing structured pathways for second owners. Meanwhile, diesel demand wanes as emission rules tighten in major cities, and hybrids bridge the transition by offering familiar refueling habits with incremental efficiency gains.

By Vehicle Age: Premium Shifts Toward Newer Inventory

Cars aged 3-5 years captured 44.35% of transactions in 2025, a sweet spot balancing depreciation and feature currency. Near-new 0-2-year units will grow 6.88% yearly as subscription fleets rotate stock quickly. In monetary terms, the Japanese used car market size for these near-new vehicles is forecast to climb sharply, while older 6-8-year-old units serve the value segment.

Japan’s 92-94% vehicle-recycling rate removes obsolete stock, pushing shoppers to choose younger, safer cars. Corporate ESG goals further shorten holding periods, funneling premium inventory into retail lots.

By Booking Channel: Digital Disruption Accelerates

OEM-certified outlets accounted for 43.05% of bookings in 2025, yet pure-online platforms are projected to compound at 10.74% annually. Nationwide logistics and remote inspection tools now allow Hokkaido buyers to secure vehicles in Kyushu without travel. This scale reduces search friction, supporting broader liquidity across the Japanese used car market.

Multi-brand dealers respond by integrating click-and-collect services, while C2C apps monetize peer-to-peer trade. High web penetration and secure digital payment rails remove barriers that once favored local showrooms.

By Transaction Type: Financing Growth Challenges, Cash Dominance

Cash still ruled 63.72% of deals in 2025, reflecting Japan’s high household savings. Yet an 8.95% annual increase in financed purchases shows younger drivers prioritizing liquidity and opting for higher-priced EVs on loan. Banks now tailor products with longer tenors and residual-value guarantees, broadening the buyer pool in the Japanese used car market.

Subscription models bundle insurance and maintenance, echoing smartphone plans. As these offerings mature, outright cash may dip, although cultural aversion to debt suggests a gradual shift rather than a wholesale change.

Geography Analysis

Japan’s auction grid and bullet-train logistics have effectively nationalized supply. Metropolitan clusters such as Tokyo, Osaka, and Nagoya show the highest turnover, fed by frequent leasing cycles and stringent smog rules that retire older units sooner. Rural prefectures rely on kei cars for low tax and insurance costs. Yet, they increasingly source vehicles online from urban lots, that convergence blurs historical regional price spreads in the Japanese used car market.

Aging demographics shift vehicle demand toward city centers as seniors forfeit licenses; rural depopulation trims sales volumes outside metro corridors. Digital dealers offset regional imbalances by shipping stock overnight through established auto-transport carriers. Uniform national inspection standards further ease cross-preference transfers, maintaining consistent vehicle quality.

Regulatory focus on CO2 reduction is strongest in the Kanto and Kansai regions, nudging urban buyers toward hybrids and EVs. Conversely, Hokkaido’s harsh winters keep demand for AWD gasoline SUVs resilient. These micro-preferences illustrate how the Japanese used car market balances national trends with local realities.

Competitive Landscape

Three competitive tiers define the arena. First, wholesale auctions—USS Co., PROTO, and Aucnet—process the majority of used stock and enjoy economies of scale that are difficult for newcomers to replicate. Second, nationwide dealer networks rely on these auctions but add value through certified refurbishment, warranties, and financing. Third, digital-native platforms leverage data science to match vehicles and buyers in real time, monetizing nationwide reach without heavy real estate footprints.

Technology adoption is the decisive battleground. AI-driven pricing engines and 360-degree virtual tours reduce asymmetry between buyer and seller. Corporate scandals have spurred consolidation: Itochu’s USD 256 million rescue of a distressed chain underscores how governance compliance can translate into market share gains.

Environmental policy also shapes strategy. Auction houses now segment lanes for zero-emission vehicles, while startups build dedicated EV marketplaces that reassure consumers on battery health. As electrified stock rises, incumbents unable to certify battery condition risk losing relevance in the Japan used car market.

Japan Used Car Industry Leaders

USS Co., Ltd.

PROTO Corporation

IDOM Inc. (Gulliver)

ORIX Auto Corporation

SBT Japan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Audi VW Retail Japan (AVRJ) unveiled "Outlet Cars", its new online platform for selling used cars. The service focuses on vehicles traded at AVRJ's dealerships.

- October 2024: Toyota Tsusho Corporation ("Toyota Tsusho") has unveiled plans to launch TOYOTA TSUSHO AUCTION ("TTA"). This new service will offer insights into used car auctions, aiming to bolster exports to emerging markets, notably in Africa.

- May 2024: A significant event occurred in the Japanese used car market. ITOCHU Corporation and ITOCHU ENEX CO., LTD. jointly established WECARS Co., Ltd. (formerly JKH Co., Ltd.) in partnership with J-Will Partners Co., Ltd. This new entity was formed through a company split, with all businesses of BIGMOTOR Co., Ltd. and its subsidiaries transferred to WECARS.

Japan Used Car Market Report Scope

Any vehicle that has previously been owned and is being resold through private sellers, classified ads, or local dealers without undergoing a significant vehicle inspection by an expert is considered to be a used car.

The Japanese Used Car Market is segmented by Vehicle Type (Hatchback, Sedan, Sport Utility Vehicle (SUV), and Multi-purpose Vehicle (MPV)), by Booking Channel (Online, OEM Certified/Authorized Dealerships, and Multi-Brand Dealerships), and by Transaction Type (Full Payment and Finance). For each segment, the market sizing and forecasts have been provided on the basis of value (in USD million) and volume (in metric tons).

By Vehicle Type

| Hatchbacks |

| Sedan |

| Sport-Utility Vehicle (SUV) |

| Multi-Purpose Vehicle (MPV) |

By Fuel Type

| Gasoline |

| Diesel |

| Hybrid |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

By Vehicle Age

| 0-2 Years |

| 3-5 Years |

| 6-8 Years |

| Above 8 Years |

By Booking Channel

| Online |

| OEM Certified / Authorised Dealerships |

| Multi-Brand Dealerships |

| C2C Digital Marketplaces |

By Transaction Type

| Full Payment |

| Finance (Loan / Lease) |

| By Vehicle Type | Hatchbacks |

| Sedan | |

| Sport-Utility Vehicle (SUV) | |

| Multi-Purpose Vehicle (MPV) | |

| By Fuel Type | Gasoline |

| Diesel | |

| Hybrid | |

| Battery Electric Vehicle (BEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| By Vehicle Age | 0-2 Years |

| 3-5 Years | |

| 6-8 Years | |

| Above 8 Years | |

| By Booking Channel | Online |

| OEM Certified / Authorised Dealerships | |

| Multi-Brand Dealerships | |

| C2C Digital Marketplaces | |

| By Transaction Type | Full Payment |

| Finance (Loan / Lease) |

Key Questions Answered in the Report

What is the Japan used car market size in 2026?

The market stands at USD 159.32 billion in 2026 and is forecast to reach USD 181.57 billion by 2031.

What compound annual growth rate (CAGR) is expected for 2026-2031?

The market is projected to expand at a 2.65% CAGR over the five-year period.

How rapidly are electric vehicles gaining ground in the used market?

Electric and plug-in hybrid models are forecast to grow at a 14.15% CAGR, outpacing all other fuel categories.

What effect will stricter 2027 emission standards have on older vehicles?

Tighter rules are expected to depress residual values for high-mileage ICE cars while boosting demand for newer, compliant models.

In what way are online platforms reshaping distribution?

Digital marketplaces now post an 10.74% CAGR, giving nationwide inventory visibility and shortening purchase cycles.

Page last updated on: