Swab And Viral Transport Medium Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

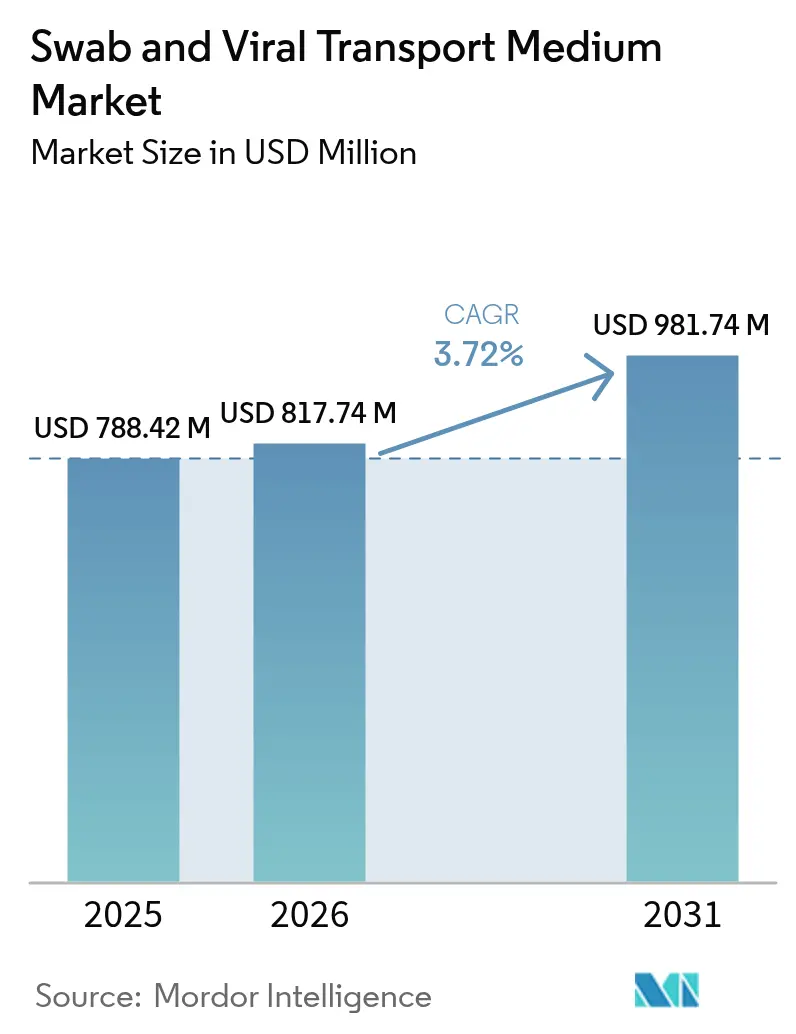

| Market Size (2026) | USD 817.74 Million |

| Market Size (2031) | USD 981.74 Million |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

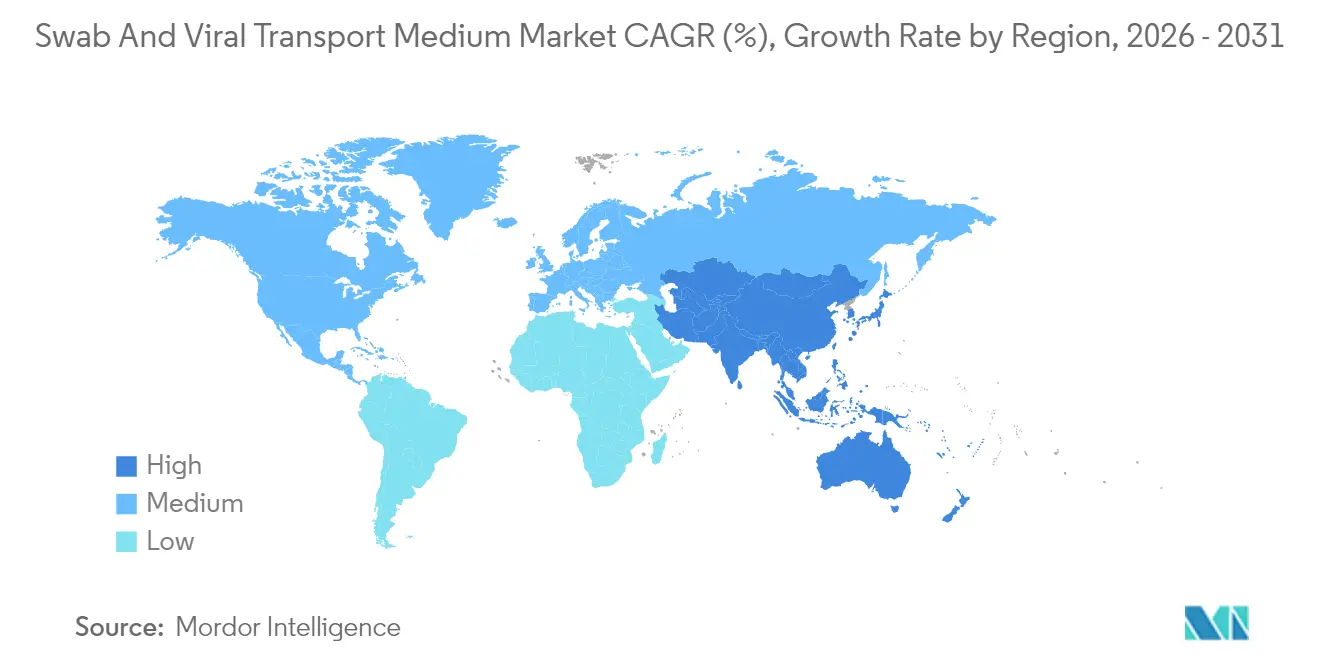

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Swab And Viral Transport Medium Market Analysis by Mordor Intelligence

The swab and viral transport medium market size is expected to grow from USD 788.42 million in 2025 to USD 817.74 million in 2026 and is forecast to reach USD 981.74 million by 2031 at 3.72% CAGR over 2026-2031. Sustained demand stems from institutionalized respiratory virus surveillance, broader preparedness funding, and the normalization of post-pandemic testing volumes. Growth is also influenced by the July 2024 FDA rule that brings laboratory-developed tests under medical device regulations, raising quality thresholds for collection systems. Supply-chain realignment toward domestic manufacturing, the rise of home sampling, and the rapid uptake of molecular diagnostics further support the swab and viral transport medium market trajectory. Competitive intensity remains moderate as scale advantages, regulatory expertise, and innovation in pathogen-inactivating media shape strategy.

Key Report Takeaways

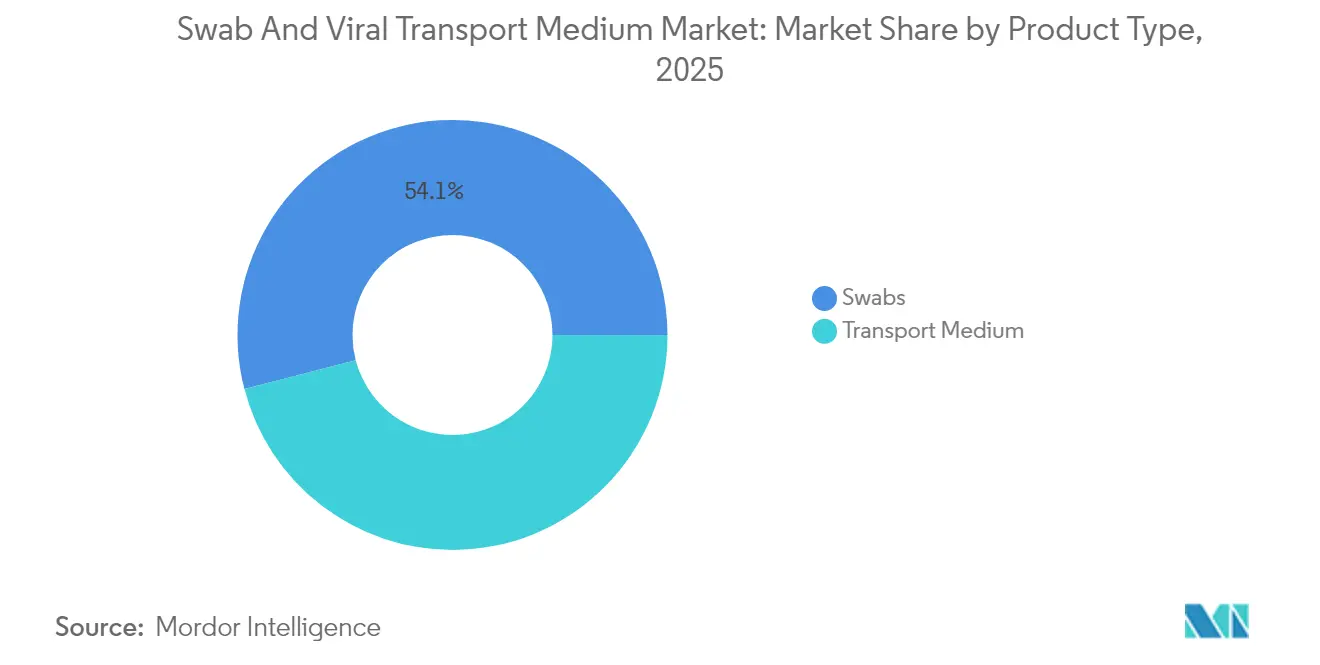

- By product type, swabs led with 54.05% revenue share in 2025, while transport medium is projected to post the fastest 5.52% CAGR through 2031.

- By swab material, flocked nylon held 45.98% of the swab and viral transport medium market share in 2025; polyester/rayon is expected to advance at a 5.63% CAGR to 2031.

- By application, COVID-19 dominated with 70.65% share of the swab and viral transport medium market size in 2025; respiratory syncytial virus testing is set to expand at a 6.62% CAGR through 2031.

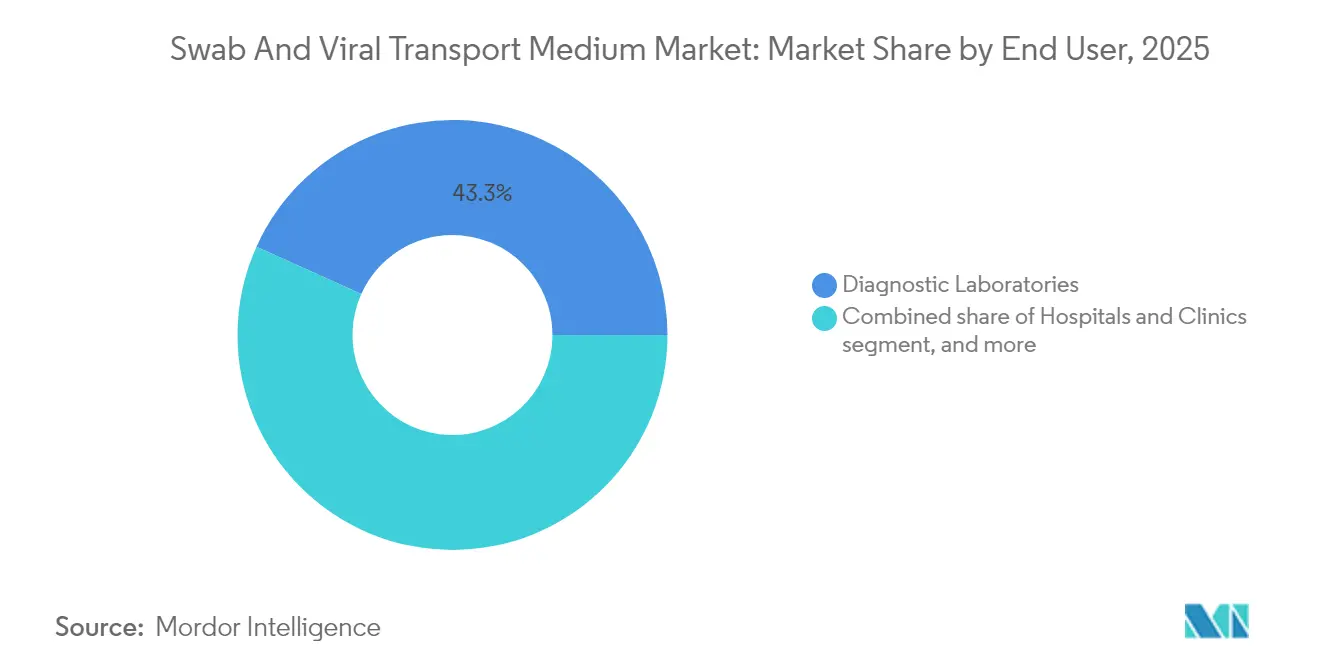

- By end user, diagnostic laboratories accounted for 43.26% share in 2025, whereas point-of-care testing centers register the highest projected 6.33% CAGR between 2026-2031.

- By distribution channel, direct tenders captured 60.98% share in 2025; online channels represent the fastest 6.12% CAGR amid procurement digitization.

- By geography, North America commanded 39.95% revenue share in 2025; Asia-Pacific is anticipated to grow at a 4.55% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Swab And Viral Transport Medium Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of respiratory viral infections | +1.2% | Global, highest in North America & Europe | Medium term (2-4 years) |

| Increasing adoption of molecular diagnostic testing | +0.9% | Global, led by developed markets | Long term (≥4 years) |

| Government investments in public health preparedness | +0.7% | North America, Europe, core APAC | Long term (≥4 years) |

| Expansion of home sampling and mail-back testing kits | +0.6% | North America & EU | Medium term (2-4 years) |

| Commercialization of room-temperature stable transport media | +0.5% | Global | Medium term (2-4 years) |

| Digitally tracked supply chains for sample integrity | +0.4% | Global, early uptake in developed markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Respiratory Viral Infections

Non-COVID respiratory pathogens are resurfacing, and adult RSV detection in Western Australia climbed from 16.3 per 100,000 in 2017 to 50.7 per 100,000 in 2023[1]National Center for Biotechnology Information, Foley et al., “Rising RSV Detection Rates,” ncbi.nlm.nih.gov. Hospitals now run year-round surveillance, maintaining higher inventories of collection kits to meet baseline demand. Multiplex PCR panels detect viral pathogens in more than half of pediatric outpatient specimens, increasing the need for validated swab-VTM pairings. Unpredictable viral seasonality following pandemic interventions forces laboratories to secure steady supplies. The resulting demand stability underpins long-term growth for the swab and viral transport medium market.

Increasing Adoption of Molecular Diagnostic Testing

Nucleic-acid amplification tests have supplanted culture methods and require media that inactivate pathogens yet preserve RNA integrity. FDA draft guidance obliges manufacturers to validate each swab-medium combination with spiking studies. Room-temperature stable products such as PrimeStore MTM reduce cold-chain expenses; over 60 million vials have been distributed globally. Point-of-care molecular devices need media that ensure biosafety without compromising sensitivity, pushing demand for premium formulations. Technology shifts therefore elevate both pricing and adoption rates for advanced transport media.

Government Investments in Public Health Preparedness

The US Critical Medical Device List classifies diagnostic collection systems as essential infrastructure, prompting federal stockpiling and domestic production grants[2]U.S. Department of Health & Human Services, “Critical Medical Device List,” hhs.gov. Thermo Fisher earmarked USD 2 billion for US manufacturing, offsetting tariff pressures and enhancing supply security. Emergency Use Authorization pathways remain in place for emerging pathogens, preserving rapid market-entry routes. Public funding increasingly links purchasing decisions to local manufacturing commitments, supporting baseline swab and viral transport medium market demand.

Expansion Of Home Sampling and Mail-Back Testing Kits

Consumer acceptance doubled the at-home testing market to USD 500 million in 2024. Dry swab protocols proved diagnostically equivalent to VTM in SARS-CoV-2 assays, simplifying mail-back workflows. SwabExpress achieved 100% sensitivity and 99.4% specificity in extraction-free testing, cutting processing costs while increasing throughput. Growth in self-collection drives product design toward leak-proof packaging and ambient-stable media, widening the addressable swab and viral transport medium market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain disruptions of medical-grade plastics | -0.8% | Global, acute in APAC hubs | Short term (≤2 years) |

| High incidence of false-negative results due to improper sampling | -0.6% | Global | Short term (≤2 years) |

| Stringent regulations on single-use plastic waste | -0.5% | Europe first, then global | Medium term (2-4 years) |

| Shift toward saliva and non-swab collection methods | -0.5% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions of Medical-Grade Plastics

Medical device makers now spend up to 20% of revenue on supply chain costs amid raw material inflation. Canada’s Federal Plastics Registry introduces detailed reporting for cotton swabs, adding compliance overhead[3]Government of Canada, “Federal Plastics Registry,” canada.ca. Companies respond by consolidating distribution centers and dual-sourcing polymers, but higher inventory requirements raise working-capital needs. Short-term turbulence could temper the swab and viral transport medium market growth until alternative supply routes stabilize.

Shift Toward Saliva and Non-Swab Collection Methods

Saliva-based assays reduce reliance on specialized swabs and VTM while maintaining accuracy for several respiratory viruses. Injection-molded polyester swabs such as ClearTip™ offer supply flexibility and improved comfort. Immediate processing in point-of-care devices eliminates transport media in some settings, shrinking demand in high-volume screening programs. Although these methods will not fully displace swab-based protocols, they present a medium-term headwind for traditional swab and viral transport medium industry incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Transport Medium Drives Innovation

Swabs captured 54.05% of the swab and viral transport medium market in 2025, but transport medium is forecast to post the fastest 5.52% CAGR through 2031. The transport-medium sub-segment benefits from room-temperature stable and pathogen-inactivating formulations that extend testing beyond conventional laboratories. COPAN’s eNAT, which preserves viral RNA for 14 days without cold chain, showcases this evolution.

Universal and molecular transport media gain traction as laboratories consolidate workflows, while DNA/RNA Shield variants support multi-pathogen tests. Regulatory requirements linking specific swab-medium pairings favor established suppliers that can execute full validation. As a result, the swab and viral transport medium market size for transport media is projected to widen its contribution, despite swabs’ headline revenue leadership.

By Swab Material: Polyester Innovation Challenges Nylon Dominance

Flocked nylon retained 45.98% share in 2025, yet polyester/rayon swabs are expected to expand at a 5.63% CAGR. Nylon’s superior specimen elution underpins clinical preference, but polyester offers scalable injection-molding and broader supplier availability. Manufacturers prioritize supply resilience after pandemic shortages; hence, polyester/rayon adoption rises even where sensitivity gains are marginal. The swab and viral transport medium market size for polyester-based devices is set to accelerate alongside cost-optimization mandates in procurement.

Continued R&D pursues hybrid materials that blend comfort and recovery efficiency. Patent filings around micro-injection molded tips and hydrophilic coatings illustrate differentiation attempts. Over time, diversified materials mitigate single-source risks and support the swab and viral transport medium market’s transition to balanced supply chains.

By Application: RSV Surveillance Drives Beyond-COVID Growth

COVID-19 testing still dominated with 70.65% share in 2025, yet RSV testing is predicted to advance at 6.62% CAGR to 2031. The introduction of nirsevimab prophylaxis heightens RSV monitoring needs, strengthening demand for accurate collection kits. Multiplex PCR panels that screen 15-20 pathogens concurrently require media able to preserve multiple targets, broadening transport-medium use-cases.

Influenza programs stabilize as seasonal patterns normalize, while emerging pathogen assays attract new investment following mpox and avian influenza alerts. The swab and viral transport medium market benefits as laboratories move from episodic to continuous respiratory surveillance, maintaining baseline purchase orders throughout the year.

By End User: Point-of-Care Testing Centers Accelerate Decentralization

Diagnostic laboratories generated 43.26% revenue in 2025 thanks to high-throughput infrastructure and regulatory credentials. However, point-of-care testing centers are forecast to experience the sharpest 6.33% CAGR, reflecting healthcare’s shift to decentralized decision-making. Clinics and urgent-care sites value collection media that inactivate pathogens for safe handling, including PrimeStore MTM.

Occupational health units, retail clinics, and home-health providers add incremental demand as payer models reward rapid diagnosis. Consequently, the swab and viral transport medium market share for decentralized settings increases, even if central labs remain the volume core for complex panels.

By Distribution Channel: Online Sales Transform Procurement

Direct tenders delivered 60.98% revenue share in 2025, underscoring institutional buying dynamics. Digital marketplaces nevertheless post the fastest 6.12% CAGR as hospitals adopt e-procurement for real-time inventory visibility. Online platforms shorten replenishment cycles and diversify vendor bases, reducing sole-source risk amid supply disruptions.

Distributors that integrate predictive analytics and automated restocking gain competitive advantage. These shifts redistribute margins but ultimately enlarge the swab and viral transport medium market by removing friction from purchasing.

Geography Analysis

North America held 39.95% of the swab and viral transport medium market in 2025, buoyed by robust regulatory oversight, extensive public-health funding, and domestic capacity expansions such as BD’s USD 30 million North Carolina plant. The FDA’s four-year LDT compliance timeline amplifies demand for validated collection systems, while US federal stockpiling secures baseline volumes. Strategic investments totaling USD 2 billion by Thermo Fisher further anchor manufacturing in the region.

Asia-Pacific represents the fastest-growing region at a 4.55% CAGR, propelled by diagnostic capacity build-outs and rising respiratory surveillance programs. China’s healthcare reform and demographic shifts expand testing volumes, whereas Japan and South Korea lead adoption of point-of-care molecular assays. ASEAN regulatory harmonization supports cross-border product standardization but still requires navigation of diverse approval timelines.

Europe maintains significant market influence through stringent MDR requirements and sustainability-focused regulations such as the Packaging and Packaging Waste directive effective August 2026. Roche’s EUR 600 million German diagnostics hub underscores regional commitment to supply security and automation. Middle East & Africa and South America continue to open opportunities tied to infrastructure upgrades, though economic volatility moderates near-term adoption rates.

Competitive Landscape

The swab and viral transport medium market is moderately fragmented. Thermo Fisher Scientific and Becton Dickinson leverage global production footprints and regulatory depth to defend share, while COPAN Diagnostics differentiates via eNAT’s pathogen-inactivation and stability profile. Technology adoption—including room-temperature media, digital supply-chain tracking, and automated swab molding—drives competitive advantage.

Patent filings for injection-molded tips and chemical stabilization cocktails create short-lived moats, yet basic device simplicity limits long-term exclusivity. Supply-chain resilience is now pivotal; firms investing in on-shore capacity and dual sourcing mitigate disruption risk and appeal to procurement teams prioritizing continuity. White-space opportunities exist in sustainable packaging and integrated sample-to-digital-report solutions, areas where smaller innovators may secure niche positions before incumbents scale offerings.

Investor activism, as seen in BD’s contemplated life-sciences divestiture, may catalyze portfolio reshaping and fresh alliances. Regulatory tightening favors larger players with established quality systems, potentially driving consolidation and a gradual rise in the swab and viral transport medium market concentration.

Swab And Viral Transport Medium Industry Leaders

COPAN Diagnostics

Puritan Medical Products

Thermo Fisher Scientific

Becton, Dickinson and Company

Longhorn Vaccines & Diagnostics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Becton Dickinson begins exclusive talks with Thermo Fisher Scientific and Danaher to divest its life-sciences unit for ~USD 21.5 billion, a move that could reconfigure competitive dynamics.

- April 2025: Thermo Fisher pledges USD 2 billion in US manufacturing and R&D over four years to counter USD 400 million tariff-driven revenue impact.

- March 2025: The FDA issues draft guidance detailing spiking-study validation for swab-VTM combinations during public-health emergencies.

- January 2025: Trinity Biotech acquires Waveform Technologies’ biosensor assets to diversify beyond legacy diagnostics.

- July 2024: The FDA grants EUA for a Non-variola Orthopoxvirus PCR kit to address mpox surveillance.

- May 2024: FDA’s final LDT rule takes effect, initiating a four-year phaseout of enforcement discretion.

Global Swab And Viral Transport Medium Market Report Scope

As per the scope of this report, Swab and Viral Transport Medium is a transport and collection system used for collecting clinical specimens for the diagnosis purpose. The Swab and Viral Transport Medium market is segmented by Type (Swab type (Nasopharyngeal swabs, Throat swabs), Transport medium), Application (COVID-19, Influenza, Herpes simplex Virus, ), End-user (Hospitals and clinics, Diagnostic Laboratories and Others) and Geography ( North America, Europe, Asia-Pacific, Middle East and Africa and South America). The Market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values in (in USD million) for the above segments.

| Swabs | Nasopharyngeal Swabs |

| Oropharyngeal (Throat) Swabs | |

| Anterior-nasal Swabs | |

| Mid-turbinate Swabs | |

| Transport Medium | Viral Transport Medium (VTM) |

| Universal Transport Medium (UTM) | |

| Molecular Transport Medium (MTM) | |

| DNA/RNA Shield & Others |

| Flocked Nylon |

| Foam |

| Polyester / Rayon |

| Other Swab Materials |

| COVID-19 |

| Influenza |

| Respiratory Syncytial Virus (RSV) |

| Herpes Simplex Virus |

| Other Applications |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Point-of-Care Testing Centers |

| Other End Users |

| Direct Tenders |

| Distributors / Wholesalers |

| Online Sales |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Swabs | Nasopharyngeal Swabs |

| Oropharyngeal (Throat) Swabs | ||

| Anterior-nasal Swabs | ||

| Mid-turbinate Swabs | ||

| Transport Medium | Viral Transport Medium (VTM) | |

| Universal Transport Medium (UTM) | ||

| Molecular Transport Medium (MTM) | ||

| DNA/RNA Shield & Others | ||

| By Swab Material | Flocked Nylon | |

| Foam | ||

| Polyester / Rayon | ||

| Other Swab Materials | ||

| By Application | COVID-19 | |

| Influenza | ||

| Respiratory Syncytial Virus (RSV) | ||

| Herpes Simplex Virus | ||

| Other Applications | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Point-of-Care Testing Centers | ||

| Other End Users | ||

| By Distribution Channel | Direct Tenders | |

| Distributors / Wholesalers | ||

| Online Sales | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the swab and viral transport medium market in 2026?

The market stands at USD 817.74 million in 2026 and is projected to reach USD 981.74 million by 2031.

What CAGR is forecast for global demand through 2031?

Demand is expected to rise at a 3.72% CAGR during 2026-2031.

Which product type is expanding the fastest?

Transport medium is forecast to grow at 5.52% CAGR, benefiting from room-temperature and pathogen-inactivating innovations.

Which region shows the highest growth potential?

Asia-Pacific is anticipated to grow at a 4.55% CAGR as diagnostic capacity and public-health investment expand.

How are supply-chain concerns shaping procurement?

Hospitals increasingly use online platforms for real-time purchasing, while manufacturers invest in domestic capacity to mitigate disruption risks.

What impact do new FDA regulations have on suppliers?

The July 2024 LDT rule imposes medical-device-level compliance, favoring manufacturers with robust quality systems and validated swab-medium combinations.

Page last updated on: