Surveillance Radar Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

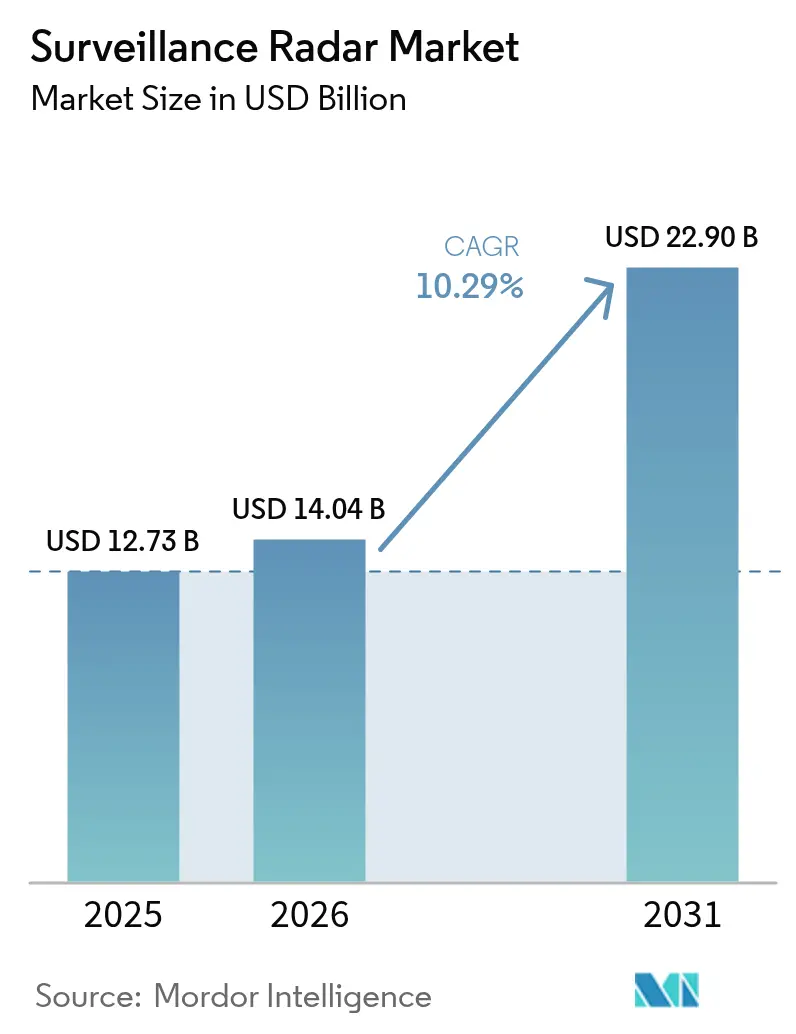

| Market Size (2026) | USD 14.04 Billion |

| Market Size (2031) | USD 22.9 Billion |

| Growth Rate (2026 - 2031) | 10.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surveillance Radar Market Analysis by Mordor Intelligence

Surveillance radar market size in 2026 is estimated at USD 14.04 billion, growing from 2025 value of USD 12.73 billion with 2031 projections showing USD 22.9 billion, growing at 10.29% CAGR over 2026-2031. Heightened defense-modernization programs, rising border-security imperatives, and rapid progress in active electronically scanned array (AESA) technology are the primary forces behind this expansion. Nations are retiring legacy mechanically steered radars in favor of software-defined architectures that adapt to new threat signatures within milliseconds. Adopting AI-enabled autonomous target-recognition systems reduces operator workload and supports multi-domain operations. At the same time, gallium-nitride semiconductors are improving power density, range, and reliability while lowering size, weight, and cooling penalties.

Key Report Takeaways

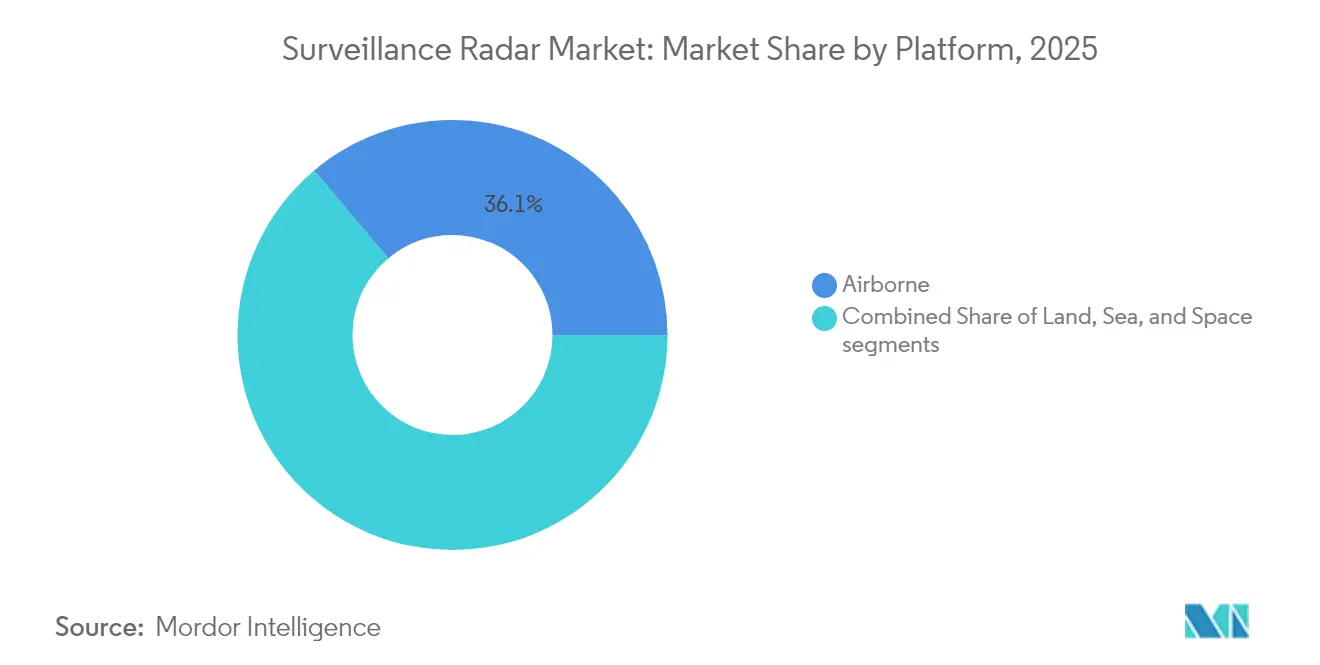

- By platform, airborne systems led with 36.12% revenue share in 2025; space-based platforms are forecasted to expand at a 9.47% CAGR to 2031.

- By component, antennas represented the largest 24.08% share in 2025, whereas digital-signal processors are projected to grow fastest at an 8.22% CAGR.

- By application, military uses controlled 68.95% of the surveillance radar market share in 2025, while commercial uses are set to grow at an 8.58% CAGR through 2031.

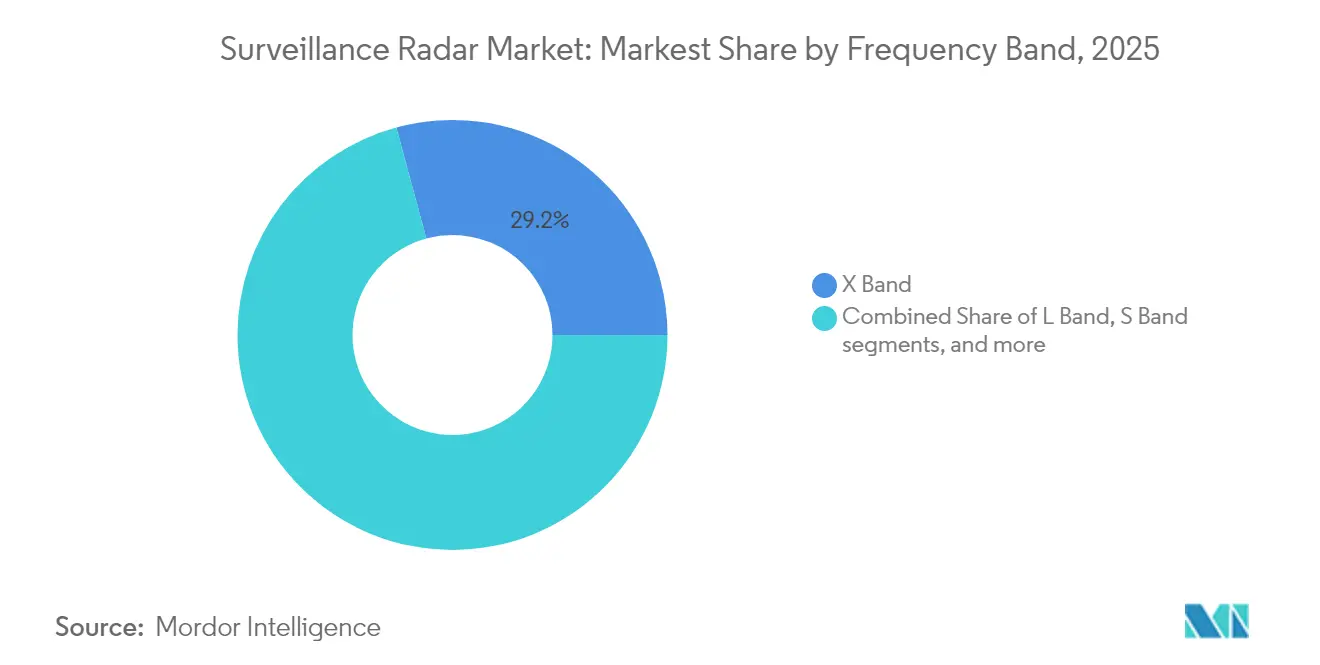

- By frequency band, X-band held 29.21% of the surveillance radar market size in 2025, whereas Ku/K-band systems are projected to rise at a 10.38% CAGR between 2026 and 2031.

- By range, long-range radars held a 41.88% share of the surveillance radar market in 2025; short-range units are poised for the fastest 8.63% CAGR.

- By radar dimension, 2-D systems dominated with a 46.10% share in 2025, while 4-D systems are set to expand at a 7.56% CAGR through 2031.

- By geography, North America commanded 35.12% revenue share in 2025, while Asia-Pacific is anticipated to register the highest 7.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surveillance Radar Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating defense budgets and fleet modernization | +2.8% | North America and Europe | Medium term (2-4 years) |

| Heightened border-security surveillance needs | +2.1% | APAC and Middle East | Short term (≤2 years) |

| Rapid adoption of AESA-based systems | +1.9% | North America and EU; expanding into APAC | Medium term (2-4 years) |

| AI-enabled autonomous target recognition | +1.4% | North America and EU; spill-over to APAC | Long term (≥4 years) |

| Proliferation of multi-static and passive radar networks | +1.2% | Europe and North America; selective APAC adoption | Long term (≥4 years) |

| UTM-grade lightweight radars for commercial drones | +1.0% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Defense Budgets and Fleet Modernization

NATO allies have pledged to lift defense outlays toward 5% of GDP by 2035, a sizeable jump from the 2% guideline in 2024.[1]Euronews Staff, “NATO Allies Aim for 5 Percent of GDP on Defence by 2035,” euronews.com This expenditure shift unlocks multi-billion-dollar radar recapitalization programs, such as the US Air Force’s USD 472 million procurement of 19 TPY-4 systems scheduled for operational acceptance in 2028. Collective procurement—exemplified by Europe’s order of 1,000 Patriot GEM-T missiles—pools national budgets while harmonizing radar-integration requirements across the alliance. Capability-based planning models keep radar line items insulated even when total force-structure budgets fluctuate. As multi-domain doctrine matures, commanders prioritize resilient sensing architecture, securing steady allocations for next-generation radar.

Heightened Border-Security Surveillance Needs

Territorial disputes, migration flows, and narco-trafficking spur radar deployments outside conventional military theaters. Canada’s USD 48.4 million Polar Over-the-Horizon Radar contract safeguards Arctic approaches and complements broader NORAD modernization.[2]ATCO Ltd., “Polar Over-the-Horizon Radar Contract Awarded,” atco.com The Netherlands’ drone-detection radar donation to Ukraine underscores the fast crossover of civil surveillance technologies into active conflict zones. China’s counter-stealth installations on South China Sea reefs demonstrate how radar assets cement de facto borders. Operators now demand low-altitude cover, unmanned integration, and rapid cueing for interdiction forces, keeping near-term demand buoyant.

Rapid Adoption of AESA-Based Systems

Gallium-nitride AESA arrays deliver 360-degree coverage, jam-resilience, and software-defined mission re-role. Raytheon’s LTAMDS proves the concept and enters serial production with Milestone C approval in April 2025. Turkey’s integration of ASELSAN’s MURAD onto Bayraktar Akıncı unmanned aircraft validates AESA scalability for compact platforms.[3]Army Recognition, “USAF Contracts 19 TPY-4 Radars,” armyrecognition.com Northrop Grumman’s G/ATOR replaces five legacy sensors with a single AESA air-ground-maritime solution, cutting life-cycle costs and logistics tails. Modular architectures allow incremental software drops that insert new waveforms without redesigning hardware, translating into sustained update revenue streams.

AI-Enabled Autonomous Target Recognition

The data rate of modern radars reaches terabytes per sortie, overwhelming human analysts. Raytheon’s Cognitive Algorithm Deployment System embeds machine-learning classifiers that rank threats aboard F-16 processing chains with sub-second latency. Russia’s AI-enabled Nebo-SV mobile radar reportedly tracks objects at 600 km range and re-vectors anti-air assets autonomously. Predictive maintenance algorithms also reduce unscheduled downtime, extending mean time between failures and trimming ownership costs. Edge computing shifts processing to the sensor, lessening bandwidth loads on contested tactical networks and elevating tempo in joint all-domain operations.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and lifecycle costs | -1.8% | Global, acute in emerging markets | Short term (≤2 years) |

| Spectrum congestion and regulatory limits | -1.2% | North America and Europe | Medium term (2-4 years) |

| Cyber-EW vulnerability of networked radars | -0.9% | NATO allies | Long term (≥4 years) |

| GaN semiconductor supply bottlenecks | -0.7% | Western manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Lifecycle Costs

Raytheon’s LTAMDS has a unit price approaching USD 130 million, a threshold that strains even top-tier defense budgets.[4]Defense-Express Analysts, “LTAMDS Cost Analysis,” defense-express.com Over a 25-year service life, support, training, and periodic tech refreshes can triple the original purchase outlay. Smaller states pursue cost-sharing frameworks—Europe’s pooled Patriot buy being a prime example—to secure premium capability without a standalone capital burden. Modular open-systems architectures that insert commercial off-the-shelf components are gaining approval but must still have clear, stringent military qualifications, tempering the near-term impact on affordability.

Spectrum Congestion and Regulatory Limits

Civil 5G rollouts occupy mid-band frequencies long used by air-defense radars, forcing operators upward into Ka-band and beyond, where signal attenuation worsens. Lengthy national certification cycles—nine months for the US Air Force in 2024—delay the fielding of new systems. Automotive radar and small-UAV sensors exacerbate mutual interference, compelling the adoption of adaptive waveforms and cognitive sensing that hike development complexity. International harmonization lags, raising long-term uncertainty for multinational exercises and coalition operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Space Systems Drive Innovation

Space-based radars form the quickest-rising branch, sustaining a 9.47% CAGR on the back of the Deep Space Advanced Radar Capability program’s USD 200 million trilateral buildout. In value terms, the segment will add more than USD 2 billion to the surveillance radar market by 2031. Airborne platforms retained dominance with a 36.12% share in 2025, supported by General Atomics’ EagleEye integration, doubling Gray Eagle endurance while enhancing synthetic-aperture resolution. Land-based mobile radars deliver expeditionary flexibility for Army maneuver forces, whereas sea-based arrays integrate with combat-management suites to extend weapons engagement zones.

Platform priorities shift toward persistent, globally accessible surveillance unobstructed by geography or over-flight rights. China’s geosynchronous SAR satellite covers almost one-third of Earth’s surface continuously, exemplifying the strategic premium on orbital assets. Commercial constellations from Iceye and Capella Space inject fresh capacity, furnishing near-real-time tasking feeds for public and private customers. Concurrently, manned and unmanned airborne assets merge roles as modular radar pods migrate across airframes. The result is a multi-layered sensing architecture where cross-cueing between orbital, airborne, and ground sensors becomes routine, amplifying overall mission resilience.

By Component: Digital Signal Processors Lead Innovation

Digital-signal processors (DSPs) constitute the fastest-growing component class with an 8.22% CAGR, mirroring the AI workload rising within modern sensors. Antennas, at 24.08% share in 2025, represent the single largest cost driver in the surveillance radar market. Advancements in gallium-nitride front-ends offer a 5- 10x power-density uplift over gallium-arsenide predecessors, trimming cooling mass while boosting detection range. Transmit-receive modules now integrate analog-to-digital conversion on-chip, shrinking the RF path and simplifying calibration.

The surveillance radar market benefits from component miniaturization that enables insertion into attritable unmanned systems. MIT Lincoln Laboratory’s wideband selective-propagation project shows millimeter-wave radars executing long-range communication and precision sensing on one board. Power-amplifier breakthroughs cut thermal load, easing platform-level integration. Multi-mission designs that combine radar, electronic support, and satcom functions within a common aperture emerge as primary choices for procurement, bolstering recurring revenue for DSP and RF-chain suppliers.

By Application: Commercial Segments Accelerate

Military programs generated 68.95% of 2025 revenue; however, civilian uptake is pacing at an 8.58% CAGR as air-traffic authorities, energy firms, and smart-city consortia exploit radar for safety and efficiency gains. Germany’s air navigation service and HENSOLDT aim to certify passive radar for civil aviation by 2026, highlighting regulatory momentum. Drone-detection grids proliferate around airports, oil refineries, and sports venues, creating a high-volume, low-unit-cost sub-segment.

Beyond transportation, hydrometeorology agencies deploy C-band Doppler arrays for severe weather forecasting, while power utilities integrate medium-range radars to protect high-voltage corridors against low-flying aircraft. The FAA’s waiver for beyond-visual-line-of-sight drones equipped with onboard radar establishes a template that other civil aviation regulators are replicating. Consequently, commercial innovators enter the surveillance radar market armed with agile-development cultures and venture financing, challenging defense primes to realign their go-to-market strategies.

By Frequency Band: Ku/K Band Technologies Surge

The Ku/K-band slice is projected to add more than USD 4 billion to the surveillance radar market size by 2031, expanding at a 10.38% CAGR. Its finer beamwidth yields sub-meter resolution, a coveted attribute for counter-stealth missions and anomaly-detection imaging. X-band, by contrast, preserves its lead with 29.21% share because of entrenched naval and air-defense inventories.

Frequency agility is a hallmark of current procurement, with new builds sporting multi-band feed networks capable of hopping from S-band to Ku-band in a single pulse pattern. The surveillance radar market increasingly rewards vendors that deliver single-aperture solutions spanning wide frequency spectra, thereby shrinking topside footprint on congested superstructures. At the extreme, W-band concepts under test promise micro-Doppler signatures that can discern rotor blade counts or human gait, enabling ultra-fine classification for special-operations forces.

By Range: Short Range Systems Expand Rapidly

Systems under 50 km register the fastest 8.63% CAGR, driven by dense-urban drone monitoring, border fences, and campus-security skins. Meanwhile, strategic sensors above 200 km retained 41.88% market share in 2025, sustained by early-warning missions and ballistic-missile-defense programs such as the Pentagon’s Long Range Discrimination Radar, which demonstrated detection past 2,000 km in recent trials.

Urban-air-mobility corridors require radar that can de-conflict passenger e-VTOL craft at altitudes below 500 ft. Quick-install mast kits, powered by solar arrays, appeal to municipalities seeking mobile perimeter coverage for high-profile events. Conversely, medium-range fire-control radars bridge the gap for ground-based air-defense batteries, offering both area coverage and precision-cue hand-off to missile launchers. The surveillance radar market thus spans a spectrum where range is not an end but a tunable parameter matched to mission and terrain.

By Radar Dimension: 4-D Systems Enable Precision

Three-dimensional sets remain the workhorse, but 4-D radars—adding Doppler velocity to azimuth, elevation, and range—are scaling at a 7.56% CAGR. Improved micro-motion tracking lowers false alarms against birds and drones, saving interceptor missiles for genuine threats. Research published in MDPI’s Remote Sensing proved millimeter-wavelength, 4-D Doppler arrays tracking low-observable supersonic objects with high fidelity.

Demand is strongest among integrated air-and-missile-defense networks pursuing shoot-look-shoot engagement loops. Fusion with EO/IR sensors yields composite tracks that populate common operational pictures for joint command centers. Vendors able to field upgrade kits that elevate legacy 2-D units to 3-D or 4-D capability will capture retrofit budgets abundant among mid-tier economies.

Geography Analysis

North America controlled 35.12% of 2025 turnover, and the region’s comprehensive NORAD modernization, plus the USD 175 billion Golden Dome missile-defense roadmap, preserves a sizable portion of future awards. Canada’s parallel USD 40 billion plan prioritizes over-the-horizon surveillance extending across the increasingly accessible Arctic routes. US congressional appropriations continue authorizing multi-year radar contracts, giving primes planning visibility through at least 2030.

Asia-Pacific is on track for a region-leading 7.41% CAGR as maritime flashpoints catalyze sovereign investments. China’s near-light-speed radar research hints at a paradigm shift in undersea monitoring, while Japan’s supply of coastal radars to the Philippines amplifies allied deterrence. India accelerates coastal surveillance buildouts and collaborates with Israel on joint AESA development to offset regional power asymmetry.

European momentum stems from NATO’s call for 5% GDP defense spending and funding vehicles such as the European Defence Fund. The EISNET consortium’s 23-partner effort to standardize air-missile-defense protocols is typical, driving bulk orders that spread R&D costs. Baltic procurement—Estonia’s GM400α and Latvia’s IRIS-T-based solution—reflects the bloc’s quick uptake of interoperable systems. Meanwhile, Middle East operators like the UAE localize production through joint ventures (EDGE-Indra) to secure supply chains and build indigenous capability. Africa shows selective demand where resource-rich states guard offshore installations, often financed via energy receipts or foreign military grants.

Competitive Landscape

The surveillance radar market is moderately consolidated. Heavyweights—RTX Corporation, Lockheed Martin Corporation, Northrop Grumman Corporation, Thales Group—hold entrenched positions through vertical control of transmitter-receiver modules, gallium-nitride wafer supply, and algorithm stacks. They invest in organic GaN fabrication lines and proprietary AI libraries to buffer against supply shocks and commoditization. Strategic teaming remains central: RTX and Kongsberg’s GhostEye collaboration extends a 30-year NASAMS partnership with 360-degree GaN coverage.

New entrants exploit software-defined architectures to bypass hardware fill rates. Anduril’s 2025 acquisition of Numerica’s Spyglass radar vaults the company from counter-UAS niche to mid-tier tactical-air-defense supplier, leveraging AI to compress kill-chain timelines. Rheinmetall’s 60% stake in ICEYE’s SAR satellite venture positions the German conglomerate as a cross-domain provider, bundling orbital imaging with land-based effectors. Such moves reshape competitive contours by marrying cloud-processed data services with traditional sensor hardware.

Primes respond through open mission-systems standards that invite external app development while locking customer data rights. Intellectual property protection around AI inference engines becomes the new battleground, with boutique analytics firms commanding high acquisition premiums. Talent scarcity in radar-signal processing amplifies this trend, prompting incumbents to set up university partnerships and in-house academies for next-generation engineer pipelines.

Surveillance Radar Industry Leaders

Lockheed Martin Corporation

HENSOLDT AG

RTX Corporation

Saab AB

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Anduril acquired Numerica Corporation’s radar and command-control businesses, adding Spyglass and Spark technologies to bolster automated sensing.

- March 2025: The US Army placed a USD 213 million order for 12 Sentinel A4 units under LRIP Lot 3, elevating air-and-missile-defense coverage.

- April 2025: Raytheon’s LTAMDS cleared Milestone C, commencing full-rate production; Poland became the first export buyer.

- April 2025: Canada awarded a USD 48.4 million Polar OTH Radar contract to ATCO for installation in the Northwest Territories.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the surveillance radar market as all newly manufactured, digitally controlled radar systems whose primary mission is continuous situational awareness, target detection, or early warning across land, sea, air, or space platforms. These units employ mechanically or electronically steered antennas that work from VHF through Ka-band, and the value captured includes hardware, embedded software, and original spare kits. Anchored by these boundaries, the study counts only purpose-built surveillance radars sold to defense, homeland security, and critical infrastructure operators.

Scope Exclusion: Weather forecast radars and multifunction fire control radars integrated in weapon guidance loops lie outside this market.

Segmentation Overview

- By Platform

- Airborne

- Land

- Sea

- Space

- By Component

- Antennas

- Transmitters

- Duplexers

- Digital Signal Processors

- Other Components

- By Application

- Commercial

- Military

- By Frequency Band

- VHF and UHF

- L Band

- S Band

- C Band

- X Band

- Ku/K Band

- Ka-Band and Above

- By Range

- Short-Range (Less than 50 km)

- Medium-Range (50–200 km)

- Long-Range (Greater than 200 km)

- By Radar Dimension

- 2-D

- 3-D

- 4-D

- By Geography

- North America

- United States

- Canada

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted in-depth interviews and structured surveys with procurement officers, radar program managers, electronics OEMs, and air traffic regulators across North America, Europe, Asia Pacific, and the Middle East. These conversations validated production run rates, upgrade cycles, and acceptance test timelines that secondary data alone could not reveal, and they refined cost escalation factors for GaN retrofit programs.

Desk Research

We first reviewed open defense budget documents from the US Congressional Service, NATO, and SIPRI, shipment duty data visible in Volza, and traffic statistics from the International Telecommunications Union to size platform backlogs and frequency allocations. Additional insight came from peer-reviewed IEEE radar conference papers, patent families mined through Questel, and annual reports of tier one radar integrators, which clarified adoption of AESA and GaN modules. D&B Hoovers and Dow Jones Factiva supplied audited revenue splits that helped approximate average selling prices across platform classes. These sources illustrate our evidence base and are not exhaustive, as many other public and paid references were tapped for confirmation.

Market Sizing and Forecasting

A top down reconstruction that ties defense expenditure, border length under electronic coverage, and radar density norms to unit demand builds the 2025 baseline, and results are cross checked by selective bottom up supplier roll ups to adjust platform splits. Key variables include approved procurement budgets, AESA versus MSA penetration, average selling price drift by frequency band, antenna power density improvements, and satellite launch manifests. A multivariate regression forecasts each driver, while scenario analysis captures deviations linked to geopolitical flashpoints. Where bottom up estimates lacked shipment proof, gap ratios derived from historical contract slippage were applied before final aggregation.

Data Validation and Update Cycle

Outputs pass three layers of analyst review, automated variance flags compare them with independent shipment trackers, and anomalies trigger source re contact before sign off. Reports refresh every twelve months, and significant contract awards or regulatory shifts yield interim updates so clients see the most current baseline.

Why Mordor's Surveillance Radar Baseline Earns Trust

Published estimates differ because firms pick dissimilar platform mixes, price assumptions, and refresh dates, and because some rely on budget announcements while others track physical deliveries.

Key gap drivers stem from whether space based constellations are counted, how commercial offshore radars are treated, and if unverified budget allotments are inflated into revenue without supplier confirmation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.73 bn (2025) | Mordor Intelligence | - |

| USD 8.9 bn (2025) | Global Consultancy A | Omits space platforms and values only signed contracts |

| USD 11.9 bn (2025) | Regional Consultancy B | Allocates fixed budget ratios and skips supplier roll ups |

Mordor delivers a balanced figure grounded in documented contracts, verified shipment data, and analyst cross checks, which together furnish a transparent, repeatable baseline that decision makers can rely on. In 2025 we size the market at USD 12.73 billion. External studies span USD 8.9 to 11.9 billion, reflecting the scope and validation gaps noted above.

Key Questions Answered in the Report

What is the current size of the surveillance radar market and how fast is it growing?

The surveillance radar market stands at USD 14.04 billion in 2026 and is projected to advance at a 10.29% CAGR to reach USD 22.9 billion by 2031.

Which platform segment holds the largest revenue share?

Airborne systems led in 2025 with a 36.12% share, reflecting sustained investment in multi-mission aircraft and unmanned platforms.

Which platform segment is expanding the fastest?

Space-based radars are projected to post the quickest 9.47% CAGR through 2031 as governments seek persistent global coverage.

What frequency band is expected to grow most rapidly?

Ku/K-band systems are forecast to register a 10.38% CAGR thanks to superior resolution for counter-stealth and space-surveillance missions.

Which geographic region is anticipated to record the highest growth rate?

Asia-Pacific is set to advance at a 7.41% CAGR, driven by maritime security programs and large-scale counter-stealth deployments.

What is the primary restraint weighing on near-term adoption?

High acquisition and life-cycle costs—up to USD 130 million per unit for top-tier systems—remain the biggest short-term drag on procurement.

Page last updated on: