Surrogacy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

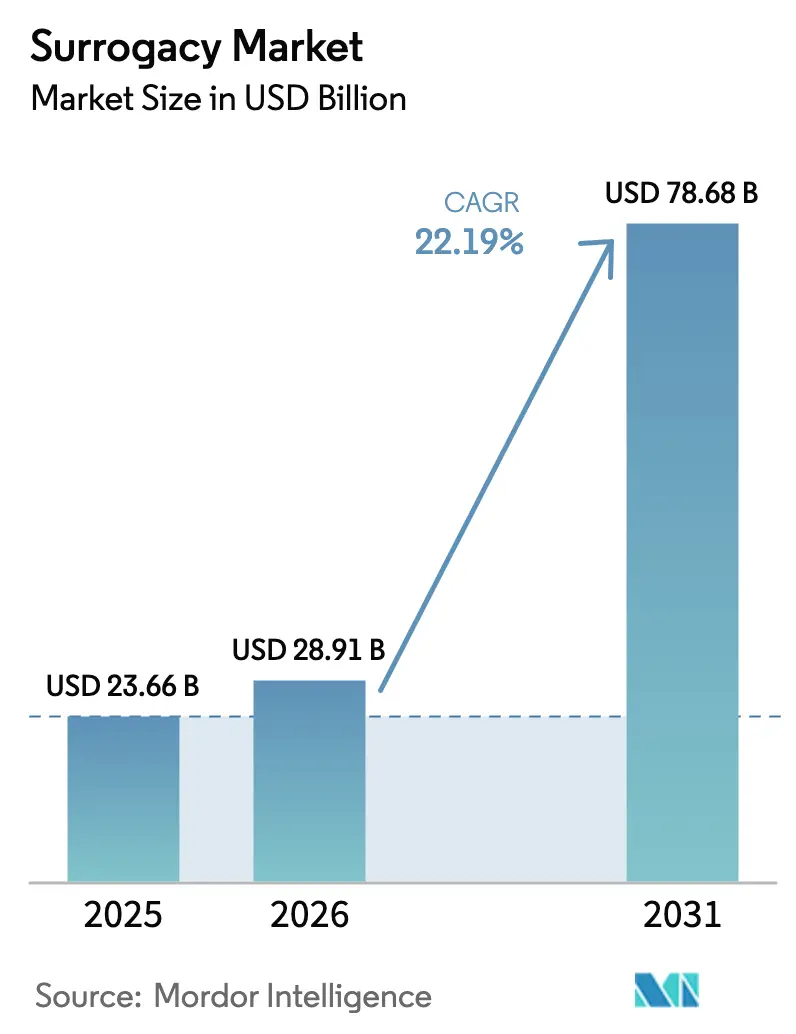

| Market Size (2026) | USD 28.91 Billion |

| Market Size (2031) | USD 78.68 Billion |

| Growth Rate (2026 - 2031) | 22.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

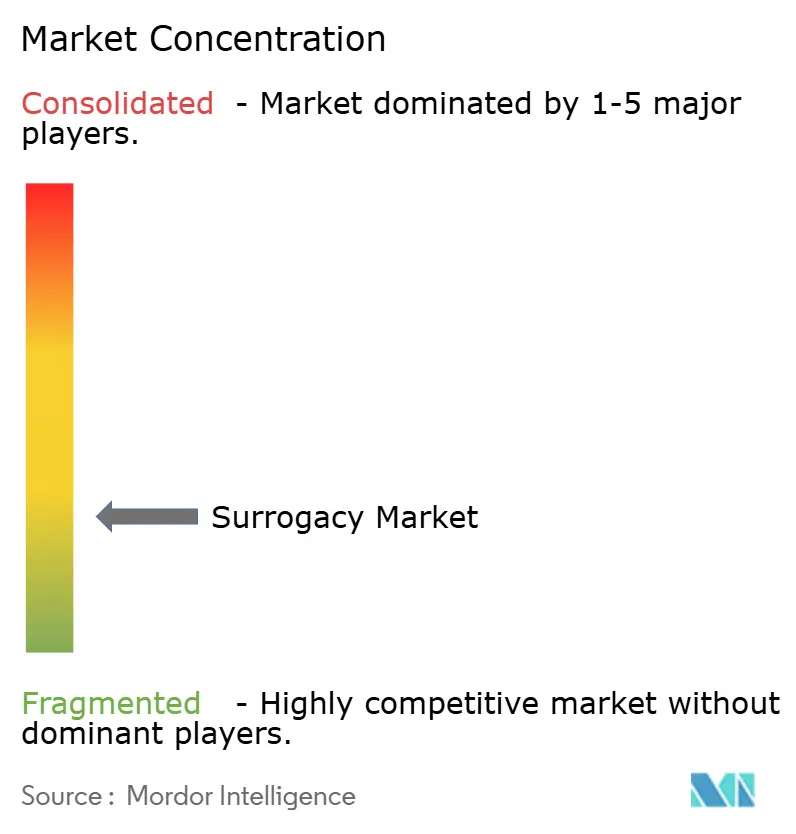

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surrogacy Market Analysis by Mordor Intelligence

Surrogacy market size in 2026 is estimated at USD 28.91 billion, growing from 2025 value of USD 23.66 billion with 2031 projections showing USD 78.68 billion, growing at 22.19% CAGR over 2026-2031. Growth stems from delayed parenthood among millennials, higher infertility prevalence, and wider acceptance of diverse family structures. Legal reforms in the United States, Thailand, and several European countries are redrawing international patient flows, while rapid gains in in-vitro fertilization (IVF) success rates shorten treatment timelines. Fertility centers continue to integrate artificial-intelligence embryo selection, cutting costs and increasing reliability. Cross-border demand is expanding toward lower-cost, regulation-light destinations in Eastern Europe, Latin America, and Southeast Asia as intended parents search for clear parentage rules and favorable pricing.

Key Report Takeaways

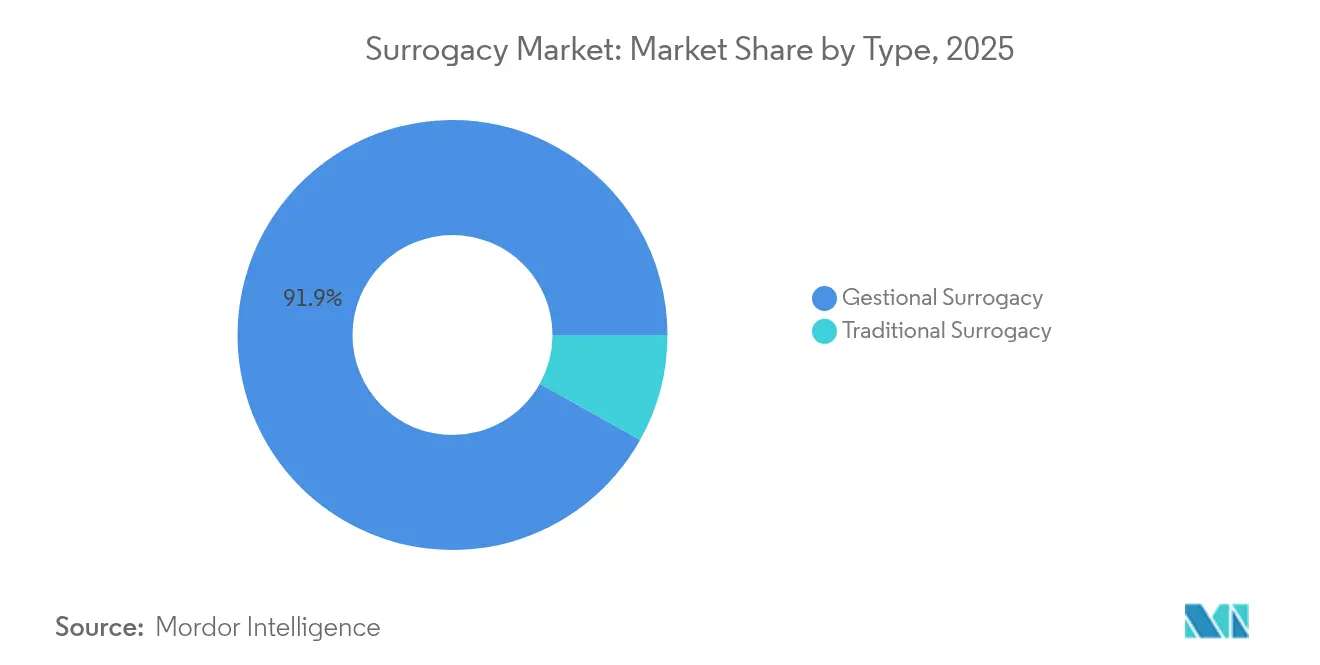

- By type, gestational surrogacy led with 91.88% revenue share in 2025; traditional surrogacy is forecast to expand at a 23.55% CAGR to 2031.

- By compensation model, commercial arrangements held 83.95% surrogacy market share in 2025 and are projected to grow at a 22.95% CAGR through 2031.

- By technology, IVF accounted for 66.12% of the surrogacy market size in 2025 and is expected to advance at a 24.42% CAGR through 2031.

- By intended parent type, heterosexual couples represented 76.05% of demand in 2025; same-sex couples record the fastest growth at 22.68% CAGR to 2031.

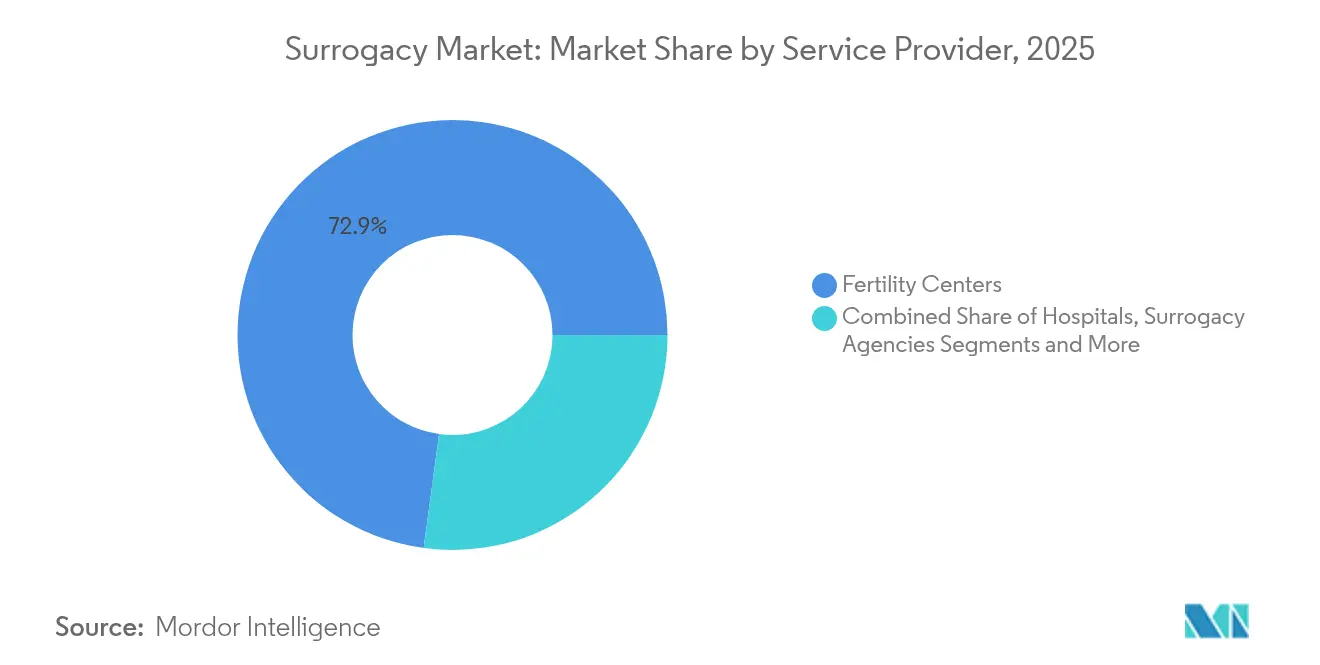

- By service provider, fertility centers controlled 72.86% of 2025 revenue, while surrogacy agencies are expanding at 22.61% CAGR as specialized intermediaries.

- By arrangement geography, domestic surrogacy held 60.74% share in 2025, while cross-border arrangements are forecast to rise at a 23.71% CAGR through 2031.

- By geography, North America commanded 40.78% of the market in 2025, whereas Asia-Pacific is set to post a 22.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surrogacy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Infertility Prevalence & Delayed Parenthood | + 4.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Rising LGBTQ+ And Single-Parent Family Formation Demand | + 3.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Fertility-Tourism To Lower-Cost / Regulation-Light Destinations | + 3.5% | Global, primarily from developed to emerging markets | Short term (≤ 2 years) |

| Improved IVF Success Rates Via Artificial Intelligence & PGT-A | + 3.1% | Global, led by North America & Europe | Medium term (2-4 years) |

| Employer-Funded Fertility Benefits Expansion | + 2.9% | North America & EU, early adoption in APAC | Medium term (2-4 years) |

| Acceptance Of Crypto / BNPL Financing For ART Procedures | + 2.3% | Global, concentrated in tech-savvy demographics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Infertility Prevalence & Delayed Parenthood

Declining fertility linked to advanced maternal age is entrenching long-run demand for assisted reproductive services. Corporate benefit plans echo this reality; 35% of large employers signaled richer surrogacy coverage in 2024. The surrogacy market therefore enjoys a stable growth foundation as career-oriented women and dual-income couples shift childbearing to later years.

Rising LGBTQ+ and Single-Parent Family Formation Demand

Same-sex couples show strong intent, with 63% planning to use assisted reproduction.[1]Courtney Reagan, “Gay Male Couples Face More Challenges, Higher Costs to Start a Family,” CNBC, cnbc.comMichigan’s 2025 law explicitly safeguarding LGBTQ+ intended parents removes a key access barrier and signals broader legislative momentum. Suppliers respond by tailoring inclusive counseling and legal services, broadening the surrogacy market without undermining existing demand from heterosexual couples.

Fertility Tourism to Lower-Cost, Regulation-Light Destinations

Ukraine and Georgia offer program fees starting at USD 30,000-60,000 versus USD 150,000-250,000 in the United States, prompting many intended parents to travel. Planned legalization in Thailand could redirect sizable volumes to Southeast Asia. Although geopolitical risks persist, transparent legal regimes and bundled medical-tourism packages sustain a brisk flow of clients into emerging hubs.

Improved IVF Success Rates via AI & PGT-A

AI-enabled embryo selection systems achieve up to 93% predictive accuracy, far surpassing manual scoring.[2]Felix Beacher, “AI Raises In Vitro Fertilization Success Rate to Nearly 100%,” AI Business, aibusiness.comAutomated labs such as Conceivable Life Sciences’ AURA in Mexico City process 2,000 cycles annually with lean staffing. Higher success rates shorten treatment courses, reducing emotional strain and overall expense for intended parents.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Bans On Commercial Surrogacy In Key Countries | -2.8% | Europe, selective APAC markets | Short term (≤ 2 years) |

| High Out-Of-Pocket Cost & Limited Insurance Coverage | -2.4% | Global, most acute in developing markets | Long term (≥ 4 years) |

| Ethical Scrutiny & Reputational Risk For Providers | -1.9% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Cross-Border Legal Parentage Uncertainty | -1.6% | Global, affecting international arrangements | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Bans on Commercial Surrogacy in Key Countries

Spain ended consular birth registrations for surrogacy babies in May 2025, while Italy criminalized overseas arrangements in 2023.[3]Angelique Williams, “Effective May 1, 2025 – Spain Bans Embassies and Consulates from Registering Babies Born Through Surrogacy,” Greenspoon Marder LLP, gmlaw.com Although these moves force families to reroute, they complicate legal parentage and raise compliance costs for providers.

High Out-of-Pocket Cost & Limited Insurance Coverage

Typical United States packages range USD 150,000-250,000, limiting access to high-income households. Employer fertility benefits and new financing plans mitigate the burden, yet most global health systems still classify surrogacy as elective, leaving patients with large personal bills.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Gestational Preference Sustains Dominance

Gestational surrogacy commanded 91.88% market share in 2025, reflecting clear parentage rules and reduced emotional complexity. The surrogacy market size for gestational arrangements is projected to expand solidly through 2031 on the back of IVF synergy and regulatory acceptance. Traditional surrogacy remains niche but grows quickly as new laws in Michigan and similar jurisdictions clarify legal status, enabling cost-conscious couples to consider genetically related surrogates. Over time, incremental acceptance widens surrogate availability, but clinical providers still emphasize gestational protocols to minimize legal risk and facilitate genetic links for intended parents.

Traditional pathways attract emerging markets where IVF infrastructure is less mature and cultural norms allow biological ties between surrogate and child. Growth in these regions hinges on standardized contracts and transparent compensation terms. Clinics balance emotional counseling with streamlined legal frameworks to protect all parties involved. Despite headwinds, the traditional option’s 23.55% CAGR illustrates underlying demand among intended parents seeking simpler laboratory requirements and lower clinical fees.

By Compensation Model: Commercial Arrangements Maintain Leadership

Commercial surrogacy held 83.95% of revenues in 2025, buoyed by explicit contracts and financial incentives for surrogates. The surrogacy market benefits because commercial frameworks ensure reliable surrogate recruitment and clear dispute resolution mechanisms. Jurisdictions such as certain U.S. states and parts of Mexico permit enforceable agreements, supporting industry scalability. Altruistic models, while encouraged in Australia and the United Kingdom, suffer from surrogate shortages and stricter advertising rules, limiting throughput for clinics.

Commercial models also align with employer-funded benefit expansions that offset large upfront payments, increasing affordability for middle-income families. Nonetheless, ethical debates around commodification remain active. Some countries experiment with hybrid reimbursement-plus-stipend structures that preserve surrogate motivation while capping profit elements, demonstrating how regulatory compromise can sustain market momentum without inviting bans.

By Technology: IVF Anchors Clinical Success

IVF captured 66.12% market share in 2025 and underpins most gestational arrangements. Rising success rates from AI-guided embryo grading and pre-implantation genetic testing advance surrogacy market growth by increasing live-birth probability per cycle. Intracytoplasmic sperm injection further widens eligibility for male-factor infertility cases, while automation technologies cut lab overhead. The surrogacy market size for IVF-enabled cycles is projected to widen rapidly as leading platforms license AI algorithms across clinics.

Intrauterine insemination persists for traditional surrogacy or cases with mild infertility, offering lower costs but reduced success probabilities. Emerging research on in-vitro gametogenesis hints at future disruption, potentially enabling egg or sperm creation from somatic cells. Although commercially distant, such breakthroughs could reshape technology choice and diversify clinical offerings by the end of the forecast period.

By Intended Parent Type: Heterosexual Couples Remain Core Base

Heterosexual couples represented 76.05% of intended parents in 2025 and remain the financial backbone of the surrogacy market. Regulatory familiarity and cultural norms favor married couples, ensuring steady case volumes. However, the surrogacy market will increasingly diversify as same-sex couples register the fastest CAGR, supported by expanding legal recognition and targeted financing products. Single parents also gain traction, particularly in jurisdictions that relax parental status requirements.

Legal progress, notably Michigan’s 2025 Act, reinforces inclusive access, while advocacy groups lobby for broader insurance mandates. Clinics respond with tailored counseling and donor-matching platforms to address diverse family structures. As barriers erode, market messaging pivots toward inclusivity, emphasizing psychological support and transparent cost disclosures.

By Service Provider: Fertility Centers Command Market Power

Fertility centers held 72.86% of revenues in 2025, benefiting from integrated medical teams and robust brand trust. Their dominance allows cross-selling of prenatal diagnostics and genetic counseling, reinforcing revenue per patient. The surrogacy market share of specialized agencies is growing rapidly as they refine surrogate-matching algorithms and offer turnkey legal services, appealing to time-pressed intended parents.

Hospitals remain relevant for high-risk or multiple pregnancies but often partner with independent fertility specialists to access cutting-edge labs. Independent consultants cater to bespoke demands but struggle to scale. Industry consolidation accelerates, evident in IVI RMA’s acquisition of Boston IVF assets, enabling larger networks to pool embryo data for AI training and achieve superior outcomes.

By Arrangement Geography: Domestic Preference Versus Cross-Border Economics

Domestic arrangements captured 60.74% of cases in 2025 as intended parents prioritize legal certainty, easier prenatal visits, and familiar healthcare systems. The surrogacy market nevertheless records higher growth in cross-border arrangements where cost savings outweigh travel complexity. Ukraine, Georgia, and Mexico actively market bundled services with transparent parentage orders, while Thailand positions to enter the segment once its legislation passes.

Providers build international referral networks and multilingual case managers to manage documentation across borders. Rising notarization and escrow services lower fraud risk, yet regulatory volatility remains a concern. Recent European restrictions illustrate how sudden legal shifts can disrupt planned births, prompting some parents to maintain dual contingencies within their fertility journeys.

Geography Analysis

North America led with 40.78% share in 2025 and enjoys robust infrastructure and favorable insurance innovations. Corporate benefit programs from NVIDIA and Estee Lauder provide up to full reimbursement, while Michigan’s legalization removed the last statewide ban. Canadian altruistic statutes offer clarity, attracting outbound demand from Europe. Mexico supplements regional capacity but exhibits state-level regulatory variation that requires careful legal navigation.

Asia-Pacific is the fastest-growing region, advancing at 22.92% CAGR to 2031. Government IVF subsidies in Singapore and the impending Thai legalization attract inflows from China and Australia, where domestic rules are restrictive. India’s tighter regulations have cooled international volumes but catalyzed domestic shift toward accredited clinics. Australia’s altruistic-only model sends many citizens overseas, underscoring the link between regulation and patient migration.

Europe experiences uneven progress. Spain’s consular ban and Italy’s criminalization reduce outbound parents’ confidence. The United Kingdom permits only altruistic arrangements, while Ukraine and Georgia continue commercial services despite geopolitical tension. The Hague Conference’s parentage project aims to harmonize rules but remains several years from ratification, leaving providers to manage a patchwork of requirements.

Competitive Landscape

The surrogacy market is moderately fragmented, with no single provider exceeding a dominant threshold. Fertility centers benefit from vertical integration and high-volume IVF labs, while agencies expand through technology-enabled surrogate matching. Private equity investments accelerate consolidation; IVI RMA’s Boston IVF acquisition signals rising appetite for scale efficiencies. AI platforms such as Fairtility’s CHLOE support over 100 clinics, leveling the technology playing field.

Automation innovators like Overture Life and Conceivable Life Sciences strive to cut per-cycle costs, potentially lowering entry prices and amplifying demand. Reputation management remains crucial, highlighted by lawsuits over mishandled embryos that quickly undermine patient trust. Companies differentiate through transparent pricing, rigorous surrogate screening, and embedded legal counsel. Expansion into emerging markets offers growth but requires astute regulatory risk assessment and culturally sensitive marketing.

Surrogacy Industry Leaders

IVI RMA Global

Virtus Health

Bourn Hall Clinic

Circle Surrogacy

New Hope Fertility Center

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Spain barred embassies from registering surrogacy-born children, sparking route changes for European intended parents.

- April 2025: Overture Life raised USD 20.6 million to scale IVF automation platforms.

- April 2025: Michigan enacted the Family Protection Act, legalizing compensated surrogacy statewide.

- February 2025: Future Family introduced national IVF insurance offering refunds for unsuccessful cycles.

Global Surrogacy Market Report Scope

As per the scope of the report, surrogacy is an arrangement, often supported by a legal agreement, whereby a woman (the surrogate mother) agrees to bear a child for another person or persons who will become the child's parent(s) after birth.

The surrogacy market is segmented by type, technology, service providers, and geography. By type, the market is segmented as gestational surrogacy and traditional surrogacy. By technology, the market is segmented as intrauterine insemination (IUI), in-vitro fertilization, and other technologies. By service providers, the market is segmented into hospitals, fertility clinics, and other service providers. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The Report Offers the Value in USD for the Above Segments.

| Gestational Surrogacy |

| Traditional Surrogacy |

| Commercial Surrogacy |

| Altruistic Surrogacy |

| Intrauterine Insemination (IUI) | |

| In-Vitro Fertilization | Classic / Standard IVF |

| Intracytoplasmic Sperm Injection (ICSI) | |

| Other Technologies |

| Heterosexual Couples |

| Same-Sex Couples |

| Single Intended Parents |

| Others |

| Fertility Centers |

| Hospitals |

| Surrogacy Agencies |

| Independent Consultants |

| Domestic Surrogacy |

| Cross-Border Surrogacy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Gestational Surrogacy | |

| Traditional Surrogacy | ||

| By Compensation Model | Commercial Surrogacy | |

| Altruistic Surrogacy | ||

| By Technology | Intrauterine Insemination (IUI) | |

| In-Vitro Fertilization | Classic / Standard IVF | |

| Intracytoplasmic Sperm Injection (ICSI) | ||

| Other Technologies | ||

| By Intended Parent Type | Heterosexual Couples | |

| Same-Sex Couples | ||

| Single Intended Parents | ||

| Others | ||

| By Service Provider | Fertility Centers | |

| Hospitals | ||

| Surrogacy Agencies | ||

| Independent Consultants | ||

| By Arrangement Geography | Domestic Surrogacy | |

| Cross-Border Surrogacy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the surrogacy market?

The surrogacy market is valued at USD 28.91 billion in 2026 and is projected to reach USD 78.68 billion by 2031 at a 22.19% CAGR.

Which region leads the surrogacy market?

North America leads with 40.78% share in 2025, supported by favorable legislation and advanced medical infrastructure.

Why is gestational surrogacy more popular than traditional surrogacy?

Gestational arrangements avoid genetic links between surrogate and child, offering clearer legal parentage and fewer emotional complexities, which drives 91.88% market share.

How are AI technologies affecting surrogacy success rates?

AI-driven embryo selection now reaches predictive accuracy up to 93%, shortening time to pregnancy and lowering overall treatment costs.

What major regulatory changes occurred in 2025?

Michigan legalized compensated surrogacy statewide, while Spain restricted embassy birth registrations, reshaping international patient flows.

How expensive is a surrogacy journey in the United States?

Comprehensive programs typically range USD 150,000-250,000, although employer benefits and new financing products are helping to reduce the upfront burden.

Page last updated on: