Chiropractic Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

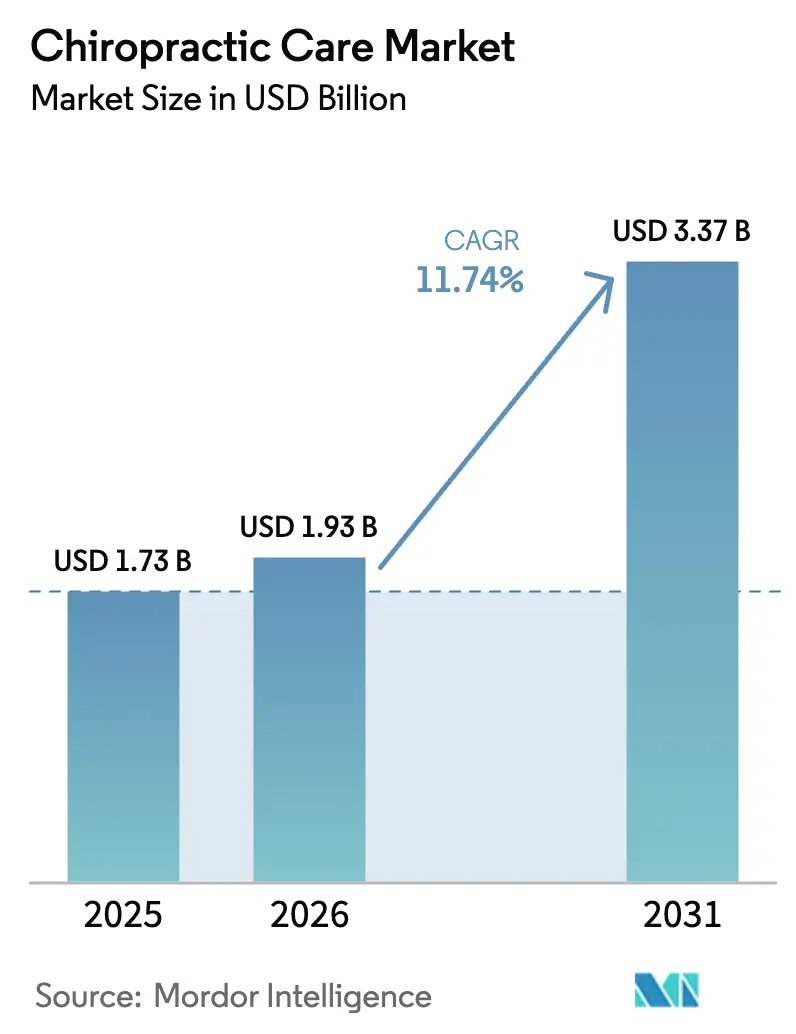

| Market Size (2026) | USD 1.93 Billion |

| Market Size (2031) | USD 3.37 Billion |

| Growth Rate (2026 - 2031) | 11.74% CAGR |

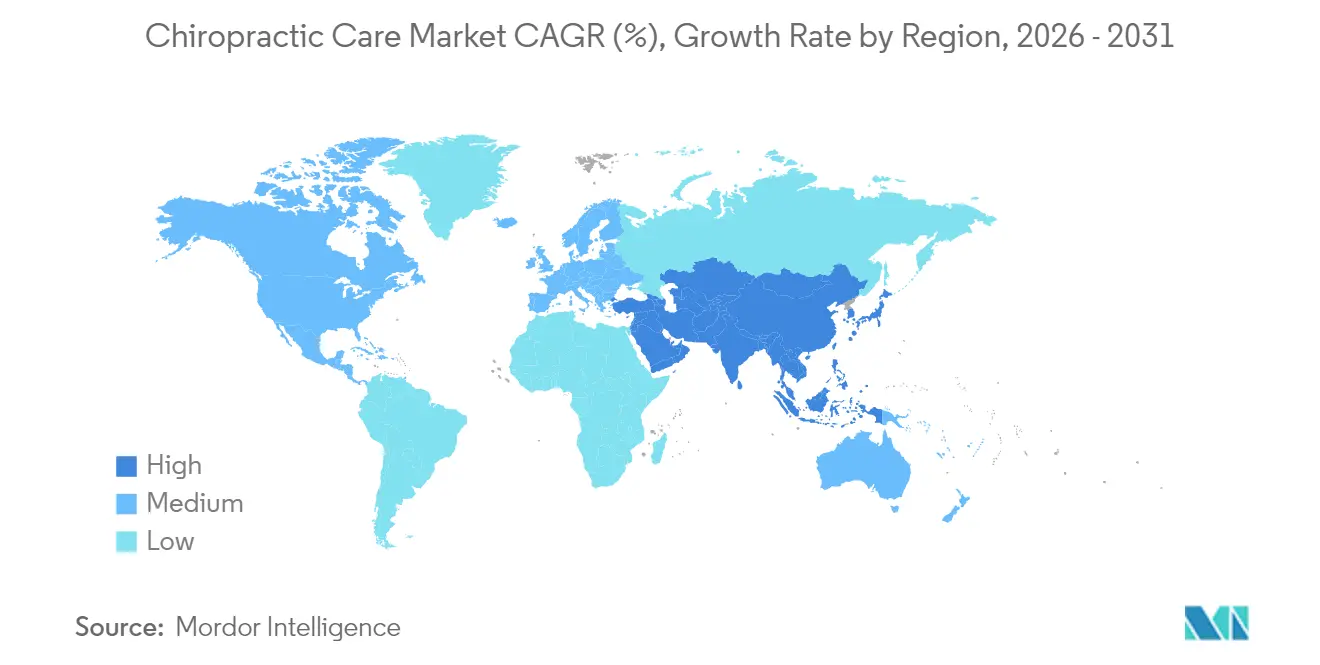

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chiropractic Care Market Analysis by Mordor Intelligence

Chiropractic care market size in 2026 is estimated at USD 1.93 billion, growing from 2025 value of USD 1.73 billion with 2031 projections showing USD 3.37 billion, growing at 11.74% CAGR over 2026-2031. Momentum stems from a worldwide preference for non-invasive, drug-free pain management, rising digital adoption inside clinics, and stronger evidence linking spinal manipulation to lower downstream surgical costs. Roughly 1 billion people now live with musculoskeletal disorders, yet only about 103,000 chiropractors serve them, underscoring a significant supply–demand gap. Consolidation through franchising is creating scalable brands, while AI-enabled posture-assessment platforms compress diagnosis times and personalize treatment pathways. Payer policy in high-income countries, especially the United States, continues to reimburse spinal manipulation when clinical progress is documented, which reinforces utilisation. Employers expanding on-site wellness clinics further widen patient funnels as they target absenteeism tied to back and neck pain.

Key Report Takeaways

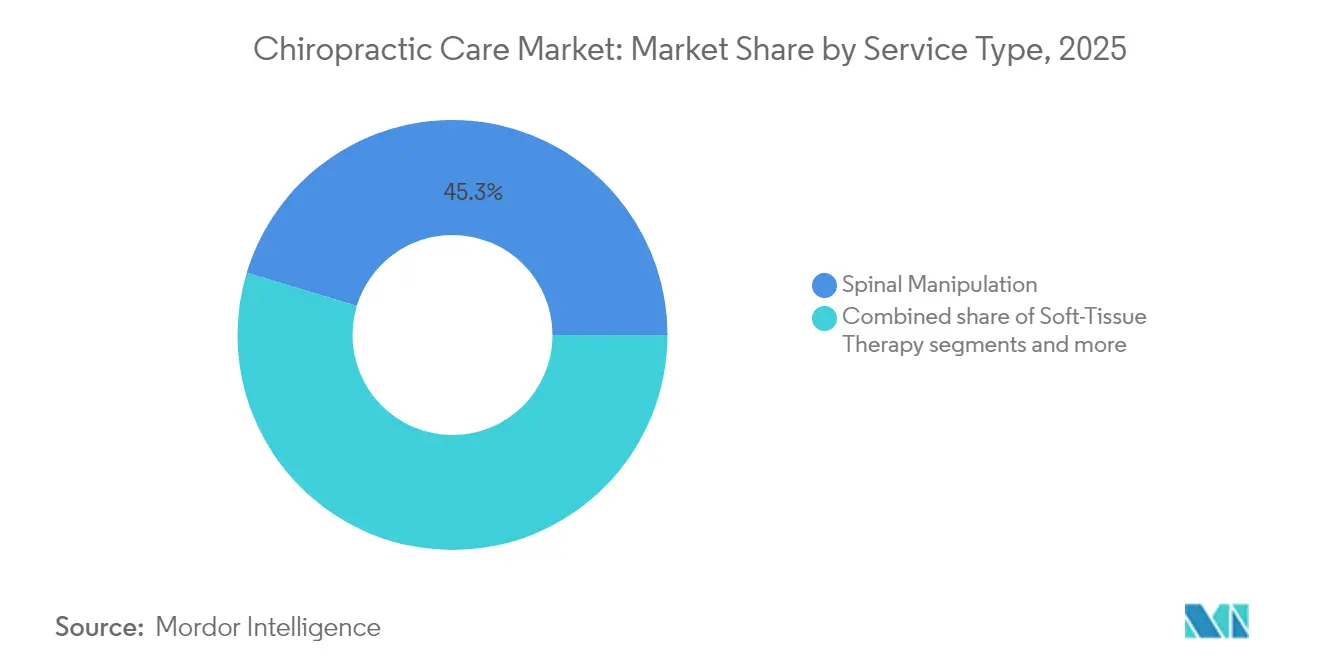

- By service type, spinal manipulation captured 45.32% of chiropractic care market share in 2025; digital posture-assessment and tele-chiropractic recorded the highest projected CAGR at 12.58% through 2031.

- By age group, adults commanded 61.87% share of the chiropractic care market size in 2025; the pediatric segment is projected to expand at 12.95% CAGR to 2031.

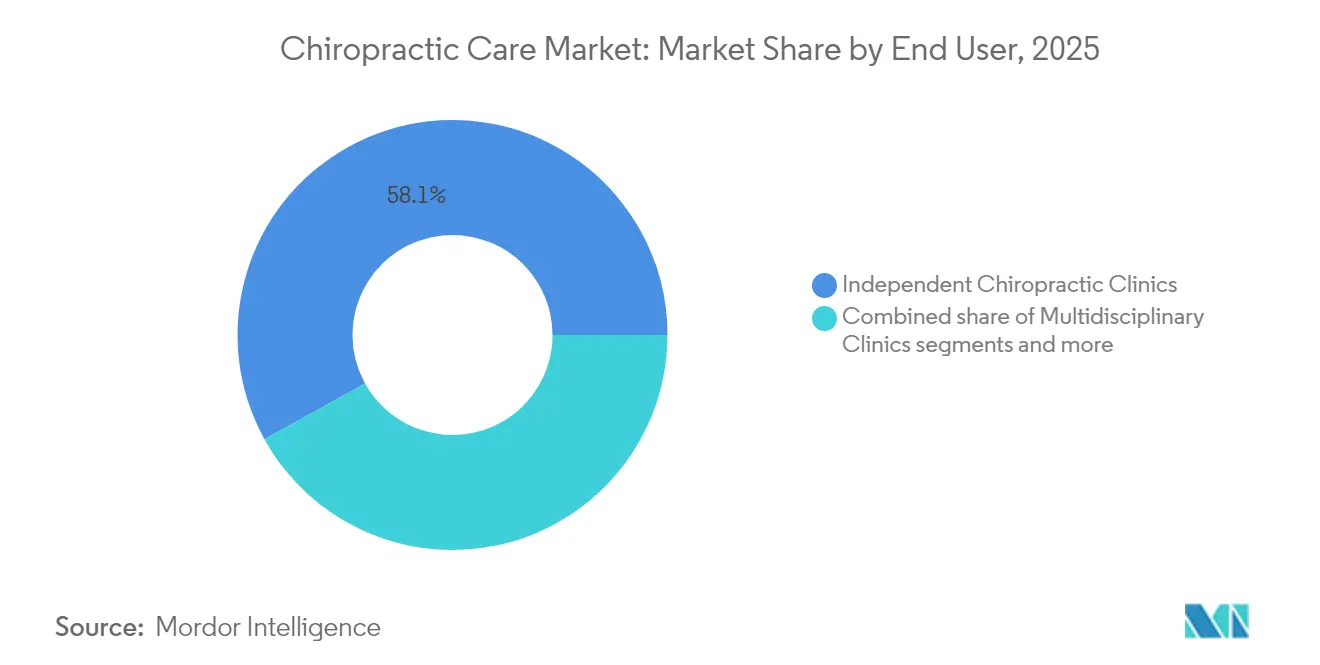

- By end user, independent chiropractic clinics accounted for 58.05% share of the chiropractic care market size in 2025; corporate and on-site wellness programs are advancing at 13.21% CAGR through 2031.

- By geography, North America led with 41.76% of chiropractic care market share in 2025; Asia-Pacific is forecast to grow at 13.55% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chiropractic Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of musculoskeletal disorders | +2.1% | Global, with highest impact in developed markets | Long term (≥ 4 years) |

| Growing geriatric population | +1.8% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Favourable reimbursement in developed markets | +1.2% | North America & Europe core, limited Asia-Pacific | Medium term (2-4 years) |

| Integration into corporate wellness programmes | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Digital posture-assessment & tele-chiro platforms | +0.8% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Franchise roll-outs in emerging economies | +0.6% | Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prevalence of Musculoskeletal Disorders

Low back pain alone affected 223 million people and is projected to reach 253 million cases by 2029, driving consistent demand for conservative care. Chronicity pushes repeat utilization, giving established clinics recurring revenue streams. Health-system executives view spinal manipulation as a cost-effective gatekeeper that can avert repeat surgeries, echoed by Veterans Health Administration utilisation forecasts. Emerging real-world evidence shows patients under chiropractic management experience fewer repeat lumbar operations, strengthening the modality’s value proposition. Global disease burden models highlight higher incidence in sedentary office populations, reinforcing employer-sponsored on-site clinics. Taken together, musculoskeletal prevalence elevates baseline visit volumes across every region.

Growing Geriatric Population

By 2030, people aged 65 and older will represent more than 20% of North America’s population, magnifying age-related spine and joint degeneration. Chiropractors increasingly collaborate with primary physicians to handle multimorbidity, guided by 70 new quality indicators that raise documentation standards. Successful practices customise care plans around osteoporosis risk and cardiovascular contraindications, therefore positioning themselves as integral nodes in integrated geriatric pathways. Europe’s public insurers fund pilot projects embedding chiropractors inside outpatient geriatric clinics, demonstrating system-level acceptance. Asia-Pacific will feel this demographic wave next, accelerating clinic openings in Japan, South Korea and urban China.

Favourable Reimbursement in Developed Markets

Blue Cross Blue Shield, Aetna and Cigna publish fee schedules that reimburse spinal manipulation when objective improvement appears within two weeks. New 2025 updates preserved coverage but capped maintenance therapy, nudging providers to document measurable functional gains. Clinics with electronic health records that auto-populate outcome metrics outperform in audit environments. Europe replicates similar rules under statutory health insurance, while Australia’s private insurers keep chiropractic on extras policies. Robust reimbursement shields patient out-of-pocket cost, sustaining high visit frequency.

Integration into Corporate Wellness Programmes

Employers face rising musculoskeletal-related compensation claims that average USD 13,000 per incident in the United States. Large firms now embed chiropractors on-site or contract mobile clinics to deliver preventive assessments during work hours. Sword Health’s AI platform, adopted by more than 10,000 employers, illustrates how digital triage and virtual therapy complement in-person manipulation, shaping hybrid care pathways. Occupational medicine departments report falls in lost-time injuries when chiropractic screening is scheduled quarterly. These measurable ROI outcomes underpin double-digit growth in the employer channel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited high-quality clinical evidence | -1.4% | Global, with higher impact in evidence-based markets | Long term (≥ 4 years) |

| Patchy insurance coverage in developing nations | -0.8% | Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| App-based physio alternatives cannibalising demand | -0.7% | Global, led by developed markets | Short term (≤ 2 years) |

| Scope-of-practice caps and regulatory variance | -0.5% | Global, with state-level variations in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited High-Quality Clinical Evidence

Only one active outcomes registry, Spine IQ, currently tracks chiropractic results at scale, limiting big-data analytics that payers increasingly require. Scholarly output remains below physical therapy and orthopaedics, which hampers guideline inclusion in some health systems. Educational institutions are widening research curricula, but longitudinal RCTs remain underfunded. Evidence gaps inhibit expansion into value-based contracts where reimbursement links to published outcomes. Without stronger datasets, adoption may plateau in academically driven markets.

App-Based Physio Alternatives Cannibalising Demand

Digital musculoskeletal platforms deliver AI-guided exercise regimes via smartphones, achieving pain-reduction outcomes comparable to in-person sessions at lower cost. Sword Health’s Phoenix AI enables each therapist to manage about 700 patients, a scale traditional clinics cannot match. The UK National Health Service has already launched an AI-run physiotherapy clinic to shorten waiting lists, signalling institutional acceptance. Younger consumers comfortable with telehealth may bypass brick-and-mortar chiropractic offices altogether, especially for mild conditions. To stay relevant, chiropractors are integrating remote monitoring and virtual consult layers into their value proposition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Platforms Disrupt Traditional Care

Spinal manipulation generated 45.32% of revenue in 2025, reaffirming its status as the therapeutic backbone of the chiropractic care market. Soft-tissue therapy and adjunctive physiotherapy together widened the clinical toolkit, but their combined pace trails virtual service formats. Digital posture-assessment and tele-chiropractic platforms are advancing at a 12.58% CAGR, propelled by smartphone sensor accuracy and payer acceptance of remote follow-up codes. AI overlays now flag spinal deviation degrees within seconds, letting clinicians focus session time on manipulation rather than screening. As a result, clinics using integrated digital intake workflows report visit throughput gains of up to 20%, elevating profitability. Point-of-care ultrasound and low-dose X-ray enable chiropractors to own more of the diagnostic value chain, though capital costs keep adoption uneven across regions. Continuous innovation suggests digital services will chip away at manipulation’s share, moving the chiropractic care industry toward hybrid care bundles.

Chiropractors deploying smart-platform kiosks in reception areas see stronger patient engagement scores, which insurers monitor under quality-linked fee schedules. Meanwhile, adjunct nutrition counselling remains a modest revenue buffer, bounded by regulation on supplement sales. Franchise networks like The Joint Corp beta-tested app-based loyalty programmes that auto-schedule maintenance sessions, pushing repeat visits above 22 per year. Overall, the chiropractic care market continues to pivot toward multimodal offerings where manual therapy, digital monitoring and lifestyle coaching converge.

By Age Group: Pediatric Segment Accelerates Growth

Adults aged 18-64 years contributed 61.87% to 2025 revenue, retaining primacy within the chiropractic care market share because workplace injuries and sports strains dominate case-mix. However, the pediatric cohort is expanding at 12.95% CAGR on the back of guideline-driven confidence among parents and paediatricians. Safety reviews published in 2024 found adverse events were mild and rare, encouraging insurers in Australia and Canada to pilot reimbursement for adolescent scoliosis management. Clinics that add child-friendly treatment rooms and collaborate with paediatric orthopaedists report uplift in family referrals.

In the geriatric bracket, age-related comorbidity often necessitates co-management with cardiology and endocrinology, slowing visit frequency but increasing billing complexity. Geriatric demand is nevertheless buoyed by demographic ageing; practices certified in fall-risk screening enjoy preference in Medicare Advantage networks. The chiropractic care industry thus faces a balancing act: scale paediatric capacity while tailoring protocols for osteoporotic spines, without diluting brand identity centred on manual expertise.

By End User: Corporate Wellness Drives Expansion

Independent clinics produced 58.05% of 2025 revenue, underlining the historic decentralised fabric of the chiropractic care market. Yet employer-sponsored and on-site wellness programmes are running ahead at 13.21% CAGR as benefits managers quantify musculoskeletal-related absenteeism costs. Direct-to-employer contracts offer chiropractors predictable monthly fees in exchange for preventive screenings, posture workshops and triage of acute injuries. Multidisciplinary clinics that house physical therapy, acupuncture and sports medicine under one roof are also scaling, satisfying patient demand for one-stop musculoskeletal solutions.

Hospital-based chiropractic departments remain niche but gain visibility when integrated into spine-surgery programmes to handle pre- and post-operative rehab, shortening length of stay. Corporate programmes often bundle virtual ergonomics coaching, bridging in-person manipulation with app-guided exercise, a model that sword-health-style platforms readily complement rather than replace. The competitive frontier therefore lies in crafting flexible service menus that embed seamlessly into diverse employer health strategies while preserving the profession’s manual-care identity.

Geography Analysis

North America retained 41.76% revenue dominance in 2025, grounded in mature insurance coverage, broad practitioner density and franchise scalability. The Joint Corp alone operates more than 950 locations and generates in excess of 13 million annual patient visits, illustrating brand power inside a fragmented provider universe. State-level regulatory divergence still complicates expansion; Missouri authorises 92 chiropractic procedures, whereas Texas restricts the list to 33, forcing multi-state operators to customise care menus. Proposed 2025 Medicare modernization may further widen scope of practice, albeit opposed by sections of organised medicine. Tele-health parity laws in 20 states now reimburse virtual follow-ups at in-office rates, encouraging clinics to integrate digital check-ins between manipulation sessions.

Asia-Pacific registers the fastest trajectory at 13.55% CAGR to 2031, reflecting swelling middle-class willingness to pay for wellness-oriented services. Australia and Japan dominate practitioner density, yet China and India embody the principal untapped volumes. Governments courting integrative medicine models have opened pilot pathways combining traditional bone-setting with modern neuromuscular stimulation, a convergence that gives chiropractors cultural resonance. Franchise systems replicate Western branding to build trust, though local licence exams and foreign ownership caps slow rollout. Multinational insurers entering the region extend supplemental policies that include chiropractic riders, thereby boosting utilisation among urban professionals.

Europe contributes stable single-digit growth, anchored by strong geriatric demographics and regional moves toward conservative care in guidelines for low back pain. Nordic countries reimburse manipulation within public primary care, while Germany’s private-statutory hybrid model encourages out-of-pocket spending. Latin America presents dual dynamics: swelling demand for minimally invasive spine interventions—projected at USD 10.5 billion by the mid-2030s—creates an economic rationale for chiropractic triage to delay surgery. Middle East and Africa remain nascent, but Dubai’s health authority now licenses chiropractors under allied health, signalling regulatory openness. Across all regions, the chiropractor-to-population ratio remains well below thresholds that epidemiologists consider adequate, implying sustained clinic pipeline opportunity for decades.

Competitive Landscape

Fragmentation defines the current chiropractic care market, though consolidation is rising via franchise economics and software-driven roll-ups. The Joint Corp’s June 2025 sale of 31 company-owned clinics and acquisition of Northwest regional developer rights illustrates a pivot toward an asset-light royalty model. These platforms elevate operational sophistication among clinics that traditionally relied on paper notes, thereby improving payer compliance and margins.

Technology constitutes the chief battleground. AI-embedded platforms now quantify spinal range-of-motion using smartphone cameras, producing objective outcome reports that satisfy insurer audit criteria. Clinics failing to invest risk referral leakage toward digital-first musculoskeletal providers. Meanwhile, venture-backed disruptors such as Sword Health scale employer contracts globally, amassing data sets that bolster algorithmic efficacy, an advantage hard for single-site chiropractors to replicate. Nevertheless, manual spinal manipulation retains differentiation where patients value tactile expertise, and numerous surveys cite higher satisfaction scores versus purely virtual care.

Regulatory politics remain a wildcard. Scope-expansion bills could let chiropractors order imaging or refer directly to specialists under Medicare, widening clinical influence but inviting physician pushback. In parallel, safety critics seek mandatory reporting systems for adverse manipulation events, which could impose additional compliance costs. Overall, strategic agility—combining franchising, digital enablement and payer-friendly documentation—will separate future leaders from lagging independents.

Chiropractic Care Industry Leaders

Atlanta Chiropractic and Wellness

Chiro One Wellness Centers LLC

Emergency Chiropractic PC

Excelsia Injury Care (Multi-Specialty Healthcare)

FV Hospital (ACC Chiropractic Clinic)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Horizon Blue Cross Blue Shield of New Jersey updated reimbursement guidance for Evaluation & Management services delivered alongside chiropractic manipulation, clarifying coding combinations

- June 2024: Sword Health raised USD 130 million, bringing valuation to USD 3 billion and reporting more than 3 million AI-guided therapy sessions delivered globally

Global Chiropractic Care Market Report Scope

As per the scope of the report, chiropractic is a licensed healthcare profession that emphasizes the body's ability to heal itself. Treatment typically involves manual therapy, often including spinal manipulation. The chiropractic care market is segmented by type, treatment method, age group, end users, and geography. The type segment is further segmented into pain management care, functional corrective care, and maintenance and preventative care. The treatment method is further divided into chiropractic adjustments, soft-tissue therapy, chiropractic exercises and stretches, and other treatment methods. The age group is further bifurcated into below 21 years, 21 to 44 years, 45 to 64 years, and above 64 years. The end user segment is further divided into hospitals, rehabilitation centers, home care settings, and other end users. The geography segment is further segmented into North America, Europe, Asia-Pacific, and Rest of the World. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (USD) for the above segments.

| Spinal Manipulation / Adjustment |

| Soft-Tissue Therapy |

| Adjunctive Physiotherapy |

| Diagnostics & Imaging |

| Others (Lifestyle, Supplements, etc.) |

| Pediatrics (0-17 yrs) |

| Adults (18-64 yrs) |

| Geriatric (65+ yrs) |

| Independent Chiropractic Clinics |

| Multidisciplinary Clinics |

| Hospitals & Specialty Centres |

| Corporate / On-site Wellness |

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Service Type | Spinal Manipulation / Adjustment | |

| Soft-Tissue Therapy | ||

| Adjunctive Physiotherapy | ||

| Diagnostics & Imaging | ||

| Others (Lifestyle, Supplements, etc.) | ||

| By Age Group | Pediatrics (0-17 yrs) | |

| Adults (18-64 yrs) | ||

| Geriatric (65+ yrs) | ||

| By End User | Independent Chiropractic Clinics | |

| Multidisciplinary Clinics | ||

| Hospitals & Specialty Centres | ||

| Corporate / On-site Wellness | ||

| By Geography | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the global chiropractic care market in 2026?

The chiropractic care market size reached USD 1.93 billion in 2026 and is set to climb to USD 3.37 billion by 2031.

Which region grows the fastest for chiropractic services?

Asia-Pacific leads with a 13.55% CAGR through 2031, propelled by rising middle-class spending and regulatory openings.

What service category dominates provider revenue?

Spinal manipulation accounts for 45.32% of 2025 revenue, though digital posture-assessment is expanding quickly at 12.58% CAGR.

Why are employers adding chiropractic benefits?

On-site and contracted programs help cut musculoskeletal-related absenteeism and workers compensation costs, justifying 13.21% CAGR in this channel.

What key restraint may slow market expansion?

Limited high-quality clinical evidence relative to other musculoskeletal disciplines still impedes broader guideline inclusion and value-based contracts.

Page last updated on: