Surgical Robots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

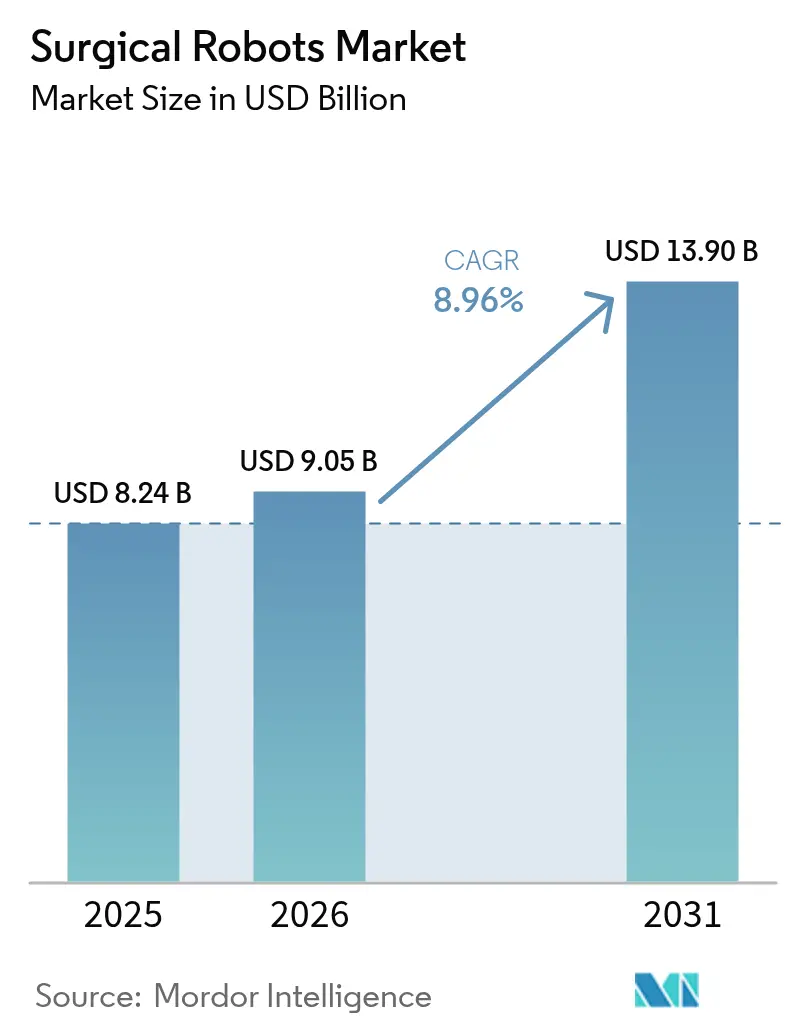

| Market Size (2026) | USD 9.05 Billion |

| Market Size (2031) | USD 13.90 Billion |

| Growth Rate (2026 - 2031) | 8.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Robots Market Analysis by Mordor Intelligence

The surgical robots market size was valued at USD 8.24 billion in 2025 and is estimated to grow from USD 9.05 billion in 2026 to reach USD 13.90 billion by 2031, at a CAGR of 8.96% during the forecast period (2026-2031). Robust capital spending by consolidated hospital systems, demographic pressure from aging populations in Europe and Japan, and rapid progress in artificial-intelligence-enabled vision and force feedback are widening the procedure mix to include complex cardiovascular and neurosurgical cases. Reimbursement improvements from the Centers for Medicare and Medicaid Services and China’s National Reimbursement Drug List are shortening payback periods on new installations, even as recent device recalls and a shortage of fellowship-trained surgeons in tier-2 cities temper near-term momentum. Portable and cart-based platforms that can shuttle between operating rooms or ambulatory surgical centers are attracting budget-sensitive buyers, while onshore component manufacturing in the United States is mitigating tariff risk and qualifying equipment for Buy America provisions. Competitive intensity remains elevated as incumbents refresh installed bases and challengers position modular systems to undercut acquisition costs and expand the surgical robots market into underserved specialties.

Key Report Takeaways

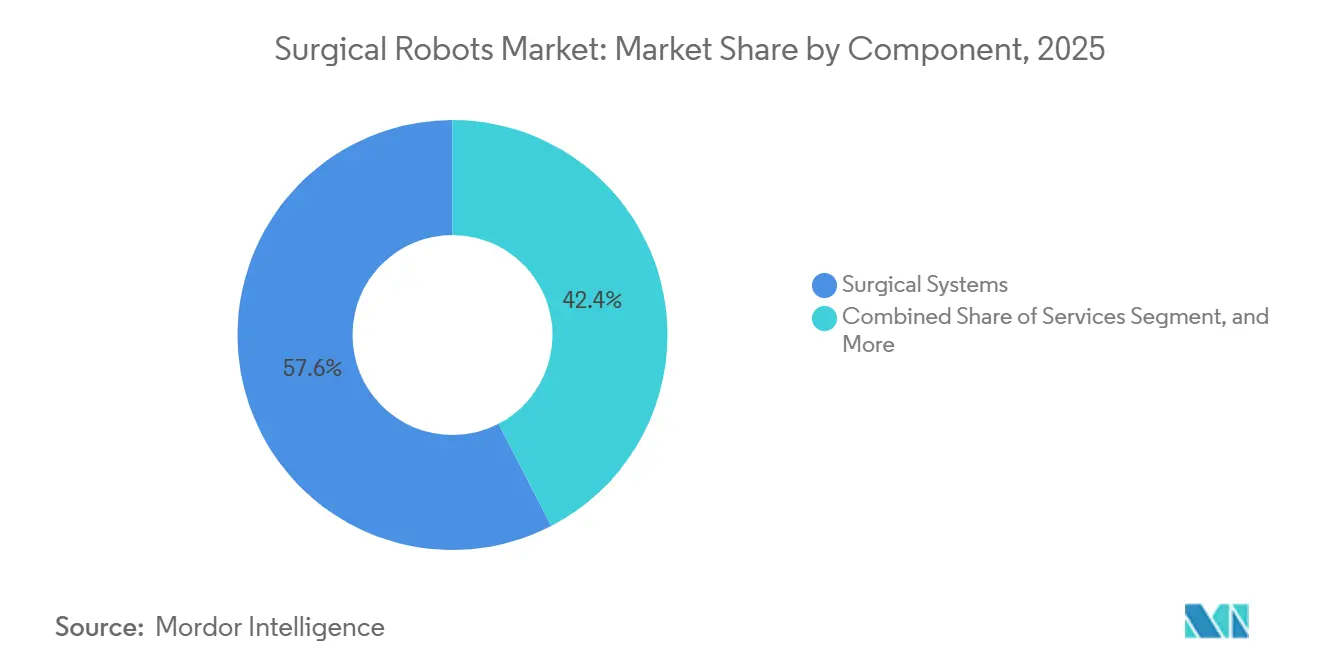

- By component, surgical systems captured 57.59% of 2025 revenue, while services are on track for the fastest 9.53% CAGR to 2031.

- By area of surgery, orthopedic procedures led with a 36.41% share in 2025; neurosurgery is poised for the highest 9.32% CAGR through 2031.

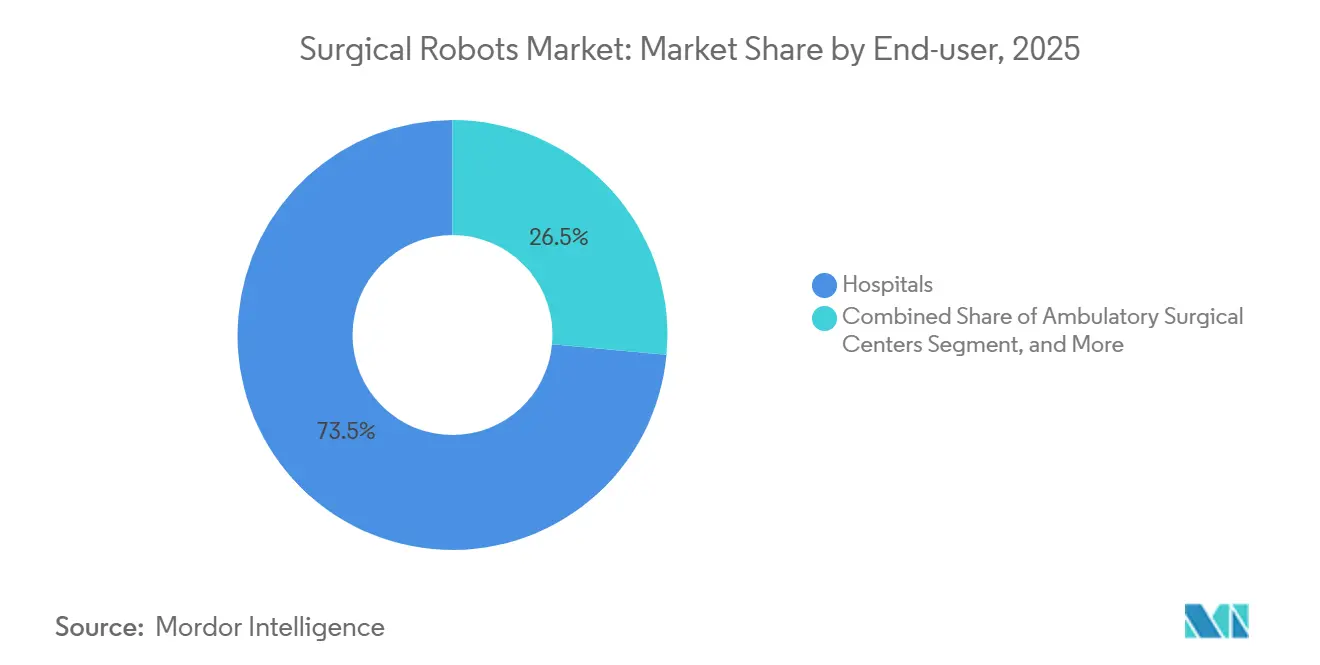

- By end-user, hospitals accounted for 73.53% of demand in 2025, whereas ambulatory surgical centers are forecast to advance at a 9.88% CAGR.

- By product, non-portable systems represented 42.49% of 2025 sales, yet portable and cart-based platforms are projected to grow at a 9.73% CAGR.

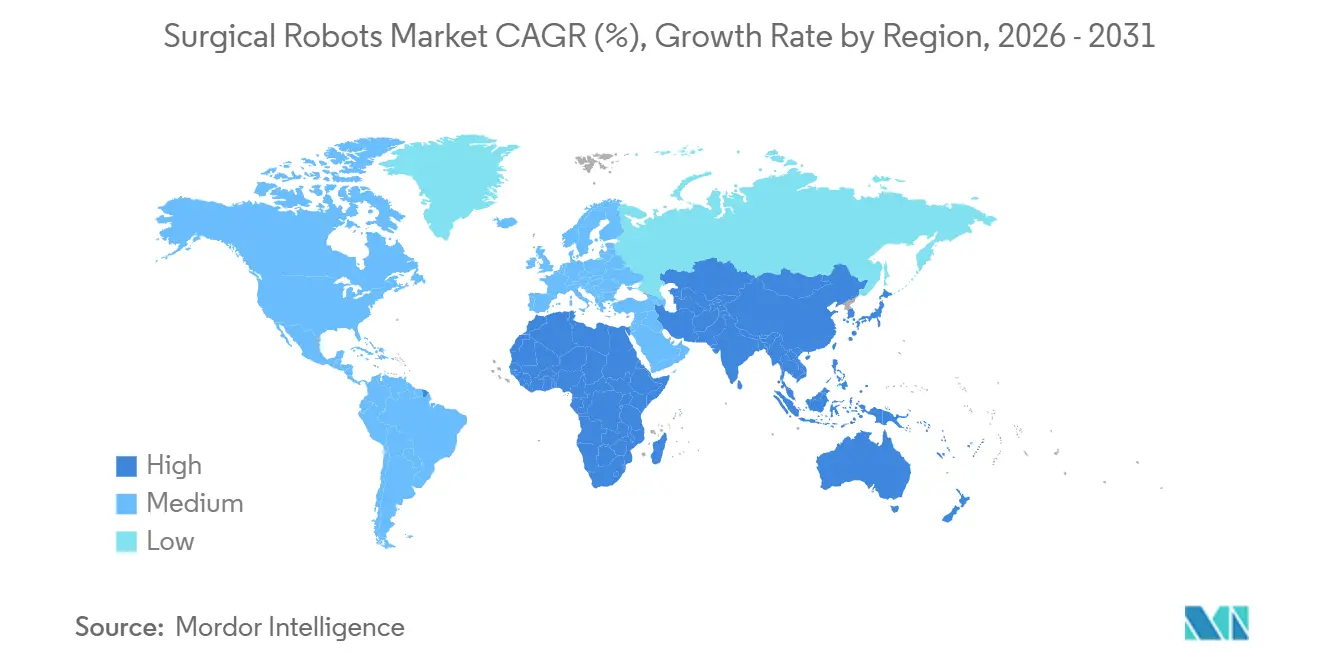

- By geography, North America remains the largest with 42.71% market share in 2025, Asia-Pacific is the fastest-growing region with 9.88% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in orthopedic-robot adoption driven by Europe and Japan's aging population | +2.10% | Europe, Japan, developed APAC | Medium term (2-4 years) |

| AI-enabled vision and haptics expanding complex soft-tissue indications | +1.80% | Global, with early adoption in North America and EU | Long term (≥ 4 years) |

| US-CMS and China-NRDL reimbursement approvals improving ROI | +1.50% | United States, China, spill-over to emerging markets | Short term (≤ 2 years) |

| Hospital-consolidation budgets favoring high-utilization robotic platforms | +1.30% | North America and EU primarily | Medium term (2-4 years) |

| ASC shift in the US spurring demand for compact robots | +1.00% | United States, early adoption in Canada | Short term (≤ 2 years) |

| Med-tech localization funds (India PLI, EU IPCEI) boosting manufacturing | +0.90% | India, EU Member States, select emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging-Driven Orthopaedic and Urologic Procedure Surge

Europe’s share of residents aged 65 and above is on track to hit 30% by 2050, while Japan already reports a 29% cohort, sustaining high volumes of knee and hip arthroplasty plus robotic prostatectomy. Orthopaedic robots such as Stryker’s Mako and Zimmer Biomet’s Rosa Knee are reducing revision rates, a metric that feeds bundled-payment incentives,[1]United Nations, “World Population Ageing 2024,” un.org Urologic demand also benefits as older male populations face rising benign prostatic hyperplasia and prostate cancer incidence, supporting uptake of da Vinci and Hugo systems.[2]Medtronic, “Hugo Robotic-Assisted Surgery System Receives FDA Clearance,” medtronic.com Japan’s 2024 reimbursement expansion for additional gastrointestinal and urologic indications accelerated hospital procurement. These demographic forces underpin long-run growth in the surgical robot’s market well past 2031.

AI-Enabled Vision and Haptic Feedback Expanding Soft-Tissue Indications

Artificial-intelligence vision now classifies tissue and tracks instruments in real time, lowering cognitive load during delicate dissections.[3]IEEE, “AI-Enhanced Vision Systems in Surgical Robotics,” ieee.org Intuitive Surgical’s da Vinci 5 integrates force feedback that cuts peak suture tension by 43%, improving anastomosis quality. Johnson and Johnson’s pending OTTAVA system predicts instrument collisions and optimizes port placement, addressing ergonomic barriers. Haptic guidance is especially valuable in cardiovascular robotics; Medtronic’s Hugo earned clearance for urologic use in 2025 and is pursuing cardiac applications. Collectively, these enhancements widen the addressable pool beyond high-volume general surgery, extending the surgical robot’s market into complex, premium-reimbursement cases.

CMS and NRDL Reimbursement Expansion Improving Hospital ROI

CMS revised Current Procedural Terminology codes in its 2025 Medicare rule, enriching reimbursement for several orthopaedic and urologic robotic procedures and cutting capital payback periods. China’s NRDL began covering robotic surgery in Guangdong, Zhejiang, and Shanghai, pushing domestic manufacturers MicroPort and TINAVI to scale output. Ambulatory surgical centers profit too, as CMS added robotic cases to its outpatient list, spurring demand for compact carts. Because platform prices range from USD 1 million to USD 2.5 million, predictable per-case margins are pivotal before boards release capital. Clearer reimbursement therefore accelerates adoption across the surgical robot’s market.

Hospital-System Capital Pooling Favouring Multi-Specialty Platforms

Consolidated health systems are centralizing budgets to acquire robots that span orthopaedic, urologic, gynaecologic, and general-surgery service lines, raising utilization and amortizing fixed costs. Intuitive Surgical’s da Vinci 5 supports more than 20 specialties, illustrating how broad portfolios secure preferred-vendor status. Medtronic’s modular Hugo and CMR Surgical’s Versius allow hospitals to add specialty kits as volume grows, Capital pooling thus entrenches incumbents yet also opens white space for challengers that deliver flexible architectures, reinforcing multi-specialty demand in the surgical robot’s market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long capital pay-back in low-volume Middle East and Africa hospitals | -0.80% | Middle East, Africa, select South America markets | Long term (≥ 4 years) |

| Device-recall incidents (2022-24) denting surgeon confidence | -0.60% | Global, with heightened scrutiny in North America and Europe | Short term (≤ 2 years) |

| Shortage of fellowship-trained robotic surgeons in Tier-2 cities | -0.50% | Asia-Pacific tier-2 cities, Middle East, Africa | Medium term (2-4 years) |

| Under-reported: Cyber-security liability premiums raising total cost of ownership | -0.40% | North America, Europe, with emerging impact in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Long Capital Pay-Back in Middle East and Africa Hospitals

Many Middle Eastern and African facilities log fewer than 200 robotic procedures a year, stretching payback beyond seven years and deterring boards seeking sub-five-year returns. Shared-service models rotate robots across hospital groups, but scheduling complexity suppresses utilization. Sparse reimbursement schedules further cloud margins, while outbound medical tourism siphons complex cases. Isolated bright spots such as tertiary centers in Johannesburg and Dubai prove viability yet represent a small slice of regional demand. Until procedure counts or equipment pricing shifts, low-volume headwinds will cap regional uptake within the global surgical robot’s market.

Device-Recall Incidents Denting Surgeon Confidence

Between 2022 and 2024 the U.S. Food and Drug Administration issued multiple Class I and II recalls linked to software glitches, instrument breakage, and sterility lapses. Intuitive Surgical’s 2023 recall of select da Vinci instruments prompted retraining and heightened scrutiny. Regulators responded with tighter pre-market reviews and expanded post-market surveillance, prolonging development timelines and compliance costs. Although no widespread patient harm emerged, the events reinforced perceptions of added failure modes in robotic platforms, especially in cardiovascular and neurosurgery. Confidence is recovering as design fixes roll out, yet the recall legacy will linger in capital-budget discussions through 2027, moderating near-term momentum in the surgical robot’s market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpacing Systems as Installed Base Matures

Services revenue is projected to rise at 9.53% through 2031, overtaking system growth as hospitals lock in multiyear maintenance, software, and training contracts that protect uptime. Recurring instruments and accessory sales exceeded USD 4 billion for Intuitive Surgical in 2025, highlighting a pivot toward annuity-like flows tied to utilization rather than capital cycles. High switching costs deter hospitals from platform changes, anchoring manufacturer margins and making services the steadiest pillar of the surgical robot’s market.

Surgical systems still generated 57.59% of 2025 component revenue, buoyed by upgrade cycles in North America and first-wave placements in Asia-Pacific. Intuitive shipped 532 systems in 4Q 2025 alone, with 303 da Vinci 5 units meeting pent-up demand for advanced vision and force feedback. Domestic vendors in China and India are broadening access at lower price points, yet the shift toward services signals a maturing installed base that will redefine how the surgical robots market size grows across the decade.

By Area of Surgery: Neurosurgery Fastest Growing as Spine and Cranial Robots Gain Traction

Neurosurgery is on pace for a 9.32% CAGR to 2031 as spine and cranial robots demonstrate sub-millimeter accuracy that reduces revision rates and nerve injury. Medtronic’s Stealth AXiS, cleared in February 2026, integrates imaging with navigation, while Zimmer Biomet’s 2025 acquisition of Monogram Orthopaedics underscores strategic intent to enter autonomous bone preparation. These entrants diversify the surgical robot’s market beyond orthopaedic anchors.

Orthopaedic procedures retained 36.41% of 2025 volume thanks to knee and hip arthroplasty throughput, yet saturation in high-income regions is slowing incremental growth. Cardiovascular and thoracic applications remain nascent, but recent da Vinci 5 cardiac approvals hint at future upside. This specialty diversification supports steady expansion of the surgical robot’s market share across multiple disciplines.

By End User: Ambulatory Surgical Centers Growing Fastest as CMS Expands Outpatient Eligibility

Ambulatory surgical centers are forecast to post a 9.88% CAGR after CMS added more robotic urologic and gynaecologic cases to its outpatient list. Compact carts such as Versius and da Vinci SP fit smaller suites, letting centers capture higher-margin cases without hospital overhead. This outpatient migration underpins fresh demand within the surgical robot’s market.

Hospitals still held 73.53% of 2025 demand, serving high-complexity cases and acting as training hubs. Yet with academic centers nearing saturation, incremental placements are shifting toward community sites and ambulatory surgical centers, broadening the surgical robots market size beyond legacy footprints and lowering entry thresholds for emerging vendors.

By Product: Portable and Cart-Based Systems Gaining Share as Flexibility Becomes Strategic Priority

Portable and cart-based robots are projected to rise at a 9.73% CAGR, reflecting hospital preference for systems that can roll between rooms without lengthy recalibration. Versius Plus, cleared in February 2026, detaches modular arms in under ten minutes, exemplifying the mobility trend. Intuitive’s da Vinci SP similarly targets single-port and natural-orifice cases where small footprints are critical.

Non-portable flagships such as da Vinci Xi and Hugo still dominate high-volume suites, representing 42.49% of product value in 2025, but growth is slower as institutions favour fleet flexibility. Mobility platforms enabling shared-service rotation to remain experimental due to infection-control logistics, yet rising real-estate costs in Europe and Asia-Pacific position portability as a strategic differentiator in the evolving surgical robot’s market.

Geography Analysis

North America leads global revenue thanks to early da Vinci adoption, established reimbursement, and 18% 2025 procedure growth. CMS outpatient eligibility is widening access, while tariff-driven on-shore manufacturing secures supply continuity. Canada’s provincial coverage expansion and Mexico’s private-sector investments further enlarge the regional surgical robot’s market.

Europe benefits from entrenched orthopaedic and urologic penetration in Germany, the United Kingdom, France, and Italy. The European Union Medical Device Regulation raises entry barriers, favouring incumbents with robust clinical data. Rising adoption in Spain and Portugal follows Intuitive Surgical’s 2025 distribution consolidation, while local Russian initiatives aim to offset import constraints.

Asia-Pacific is the fastest-growing geography, propelled by China’s NRDL coverage in major provinces and Japan’s reimbursement additions for prostatectomy and gastrectomy. Domestic vendors such as MicroPort undercut prices, scaling access and swelling regional surgical robots market size. India is emerging via private hospital chains expanding into tier-2 cities, and South Korea sustains double-digit growth through government innovation incentives.

The Middle East and Africa remain restrained by low procedure volume and uncertain reimbursement, though tertiary centers in Dubai, Riyadh, and Johannesburg show viable economics. South America sees gradual rollout in Brazil and Argentina via public-private financing, yet currency volatility tempers capital commitments. As Asia-Pacific accelerates, North America’s share moderates, but the broader surgical robots market continues to expand as price points fall and regulatory clarity improves across regions.

Competitive Landscape

The surgical robots market remains concentrated, with Intuitive Surgical controlling over 70% of global procedures through an installed base exceeding 11,000 units and USD 4 billion in 2025 recurring revenue. High switching costs lock hospitals into da Vinci consumables, but pressure is mounting from modular challengers.

CMR Surgical’s Versius Plus positions low-cost flexibility to capture ambulatory surgical centers, while Medtronic’s Hugo leverages entrenched purchasing relationships and modular design. Johnson and Johnson’s OTTAVA, now in De Novo review, layers machine-learning port guidance onto a vast surgical toolbox, promising cross-selling upside.

Chinese firms MicroPort and TINAVI deploy price-competitive systems aligned with provincial reimbursement, expanding in Asia-Pacific and threatening established margins. White-space remains in cardiovascular and neurosurgical robotics, where penetration rates sit below 5% and first-mover advantage is still attainable. Technology differentiation now pivots on AI-guided vision, force feedback, and autonomous instrument control, all raising R and D costs yet expanding the surgical robots market into complex procedures. Players balancing clinical performance, capital efficiency, and recurring-revenue streams will keep or gain share, while single-specialty or fixed-installation strategies risk obsolescence.

Surgical Robots Industry Leaders

Intuitive Surgical, Inc.

Stryker Corporation

Johnson & Johnson (Auris + DePuy)

Medtronic PLC

Zimmer Biomet Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Medtronic secured FDA clearance for the Stealth AXiS spine robot, integrating imaging and navigation to guide pedicle-screw placement within sub-millimeter tolerances.

- February 2026: CMR Surgical won FDA clearance for Versius Plus, adding advanced visualization and articulation to its modular platform.

- January 2026: Intuitive Surgical obtained FDA clearance for cardiac surgery applications on the da Vinci 5 platform, including mitral valve repair and coronary artery bypass grafting.

- January 2026: Johnson and Johnson submitted a De Novo application for the OTTAVA robotic system with machine-learning collision prediction.

Global Surgical Robots Market Report Scope

The Surgical Robots Market Report is Segmented by Component (Surgical Systems, Instruments and Accessories, Training, Services), Area of Surgery (Gynecological, Urological, Orthopedic, Neurosurgery, Cardiovascular, General and Laparoscopic, Thoracic, Other Specialties), End-user (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), Product (Non-portable Systems, Portable/Cart-based Systems, Mobility Platforms), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Surgical Systems |

| Instruments And Accessories |

| Training |

| Services (Maintenance) |

| Gynecological |

| Urological |

| Orthopedic |

| Neurosurgery |

| Cardiovascular |

| General and Laparoscopic |

| Thoracic |

| Other Specialties |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Non-portable Systems |

| Portable / Cart-based Systems |

| Mobility Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Component | Surgical Systems | |

| Instruments And Accessories | ||

| Training | ||

| Services (Maintenance) | ||

| By Area of Surgery | Gynecological | |

| Urological | ||

| Orthopedic | ||

| Neurosurgery | ||

| Cardiovascular | ||

| General and Laparoscopic | ||

| Thoracic | ||

| Other Specialties | ||

| By End-user | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Product | Non-portable Systems | |

| Portable / Cart-based Systems | ||

| Mobility Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the surgical robots market today and where is it heading by 2031?

It was valued at USD 9.05 billion in 2026 and is forecast to reach USD 13.90 billion by 2031, reflecting an 8.96% CAGR.

Which surgical specialty is growing fastest for robotic systems?

Neurosurgery leads with a projected 9.32% CAGR as spine and cranial robots secure regulatory clearances and show superior accuracy.

Why are ambulatory surgical centers adopting robots more quickly than hospitals?

CMS added more robotic cases to its outpatient list and compact cart systems fit smaller suites, enabling centers to earn higher margins on eligible procedures.

Which geographic region is expected to contribute the most incremental revenue?

Asia-Pacific, buoyed by China and Japan's reimbursement expansions and domestic manufacturers lower-priced platforms, will add the largest share of new installations.

Who currently dominates global procedure volume and how are challengers competing?

Intuitive Surgical controls over 70% of procedures through its da Vinci fleet; rivals such as CMR Surgical and Medtronic are positioning modular, cost-efficient systems to undercut acquisition costs.

What technological advances are expanding robotic eligibility into complex surgeries?

AI-driven vision, real-time force feedback, and machine-learning collision prediction are making robotics viable in cardiovascular and neurosurgical domains.

Page last updated on: