Surface To Air Missiles Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

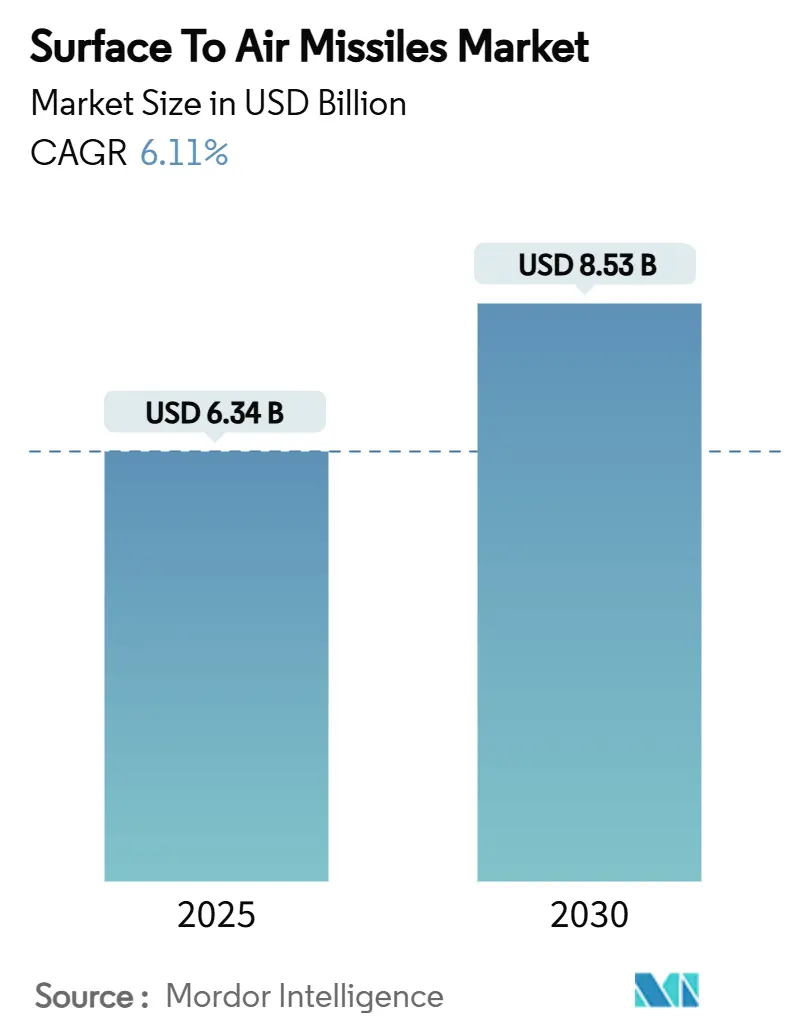

| Market Size (2025) | USD 6.34 Billion |

| Market Size (2030) | USD 8.53 Billion |

| Growth Rate (2025 - 2030) | 6.11% CAGR |

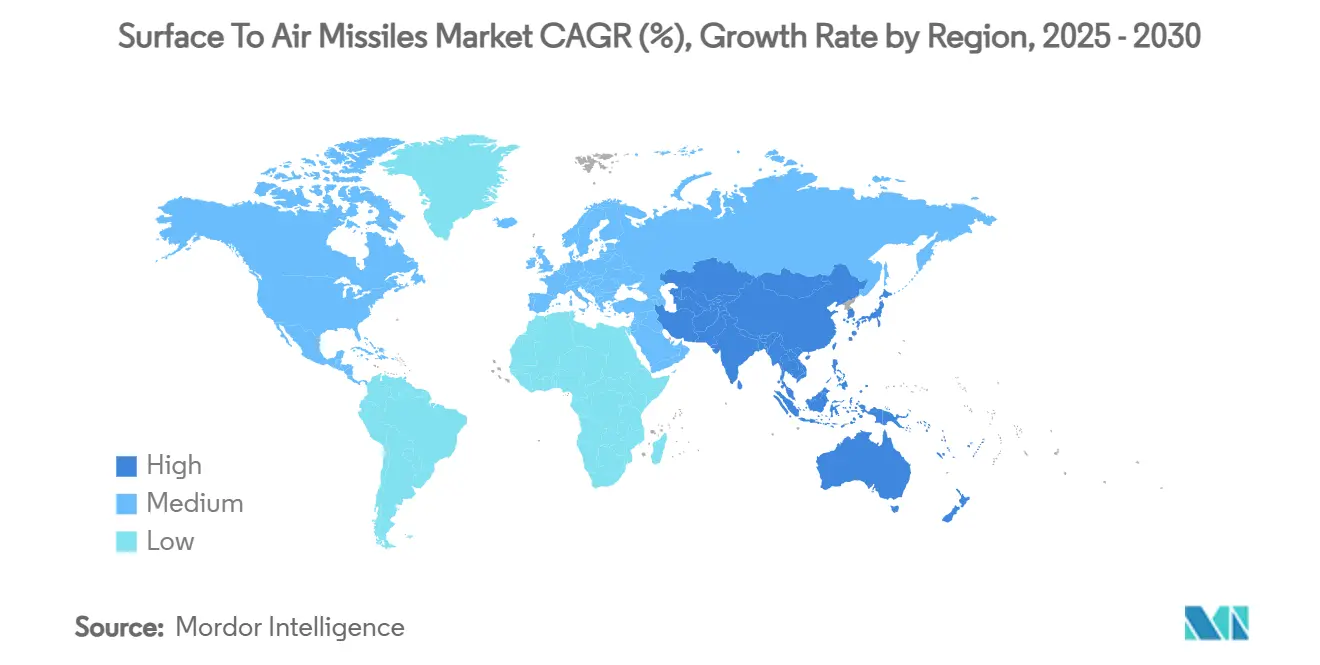

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

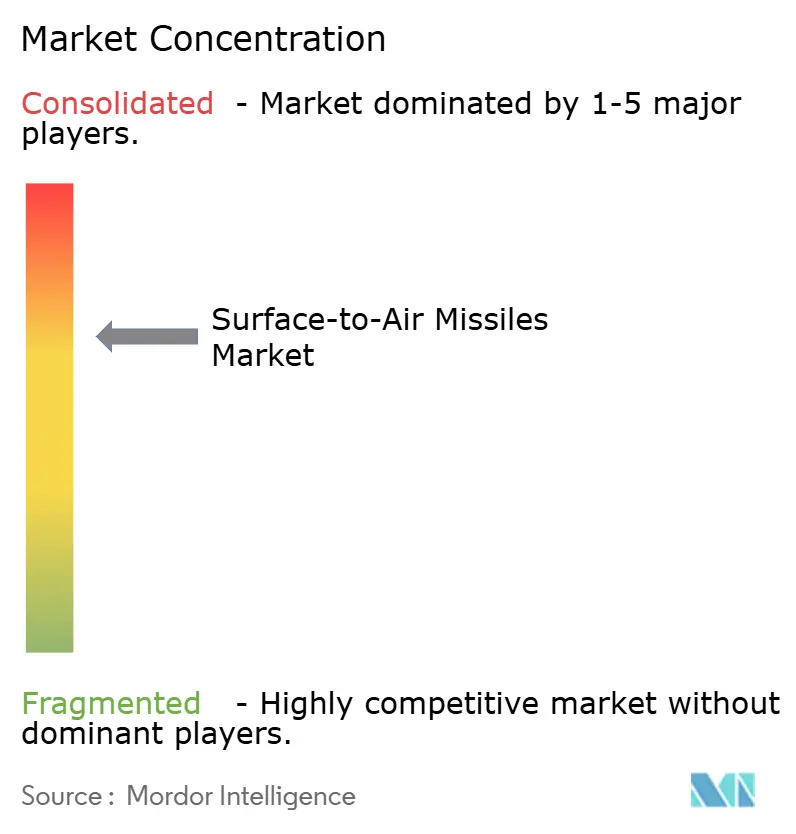

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surface To Air Missiles Market Analysis by Mordor Intelligence

The surface-to-air missiles market size is estimated at USD 6.34 billion in 2025 and is anticipated to expand at a CAGR of 6.11%, raising its value to USD 8.53 billion by 2030. Rising geopolitical tension, the re-emergence of great-power rivalry, and the rapid modernization of air defense networks are the primary forces driving spending on new intercept solutions. Sustained budget increases in the United States, NATO, East Asia, and the Middle East are widening procurement pipelines for high-end and cost-effective missile systems, while technological advances in sensors, seekers, and propulsion are reshaping performance benchmarks. Concerns about unmanned aerial vehicles, cruise missiles, and the latest generation of hypersonic weapons are also prompting a shift toward layered, network-enabled architectures capable of short-notice engagement. Ongoing supply chain constraints—particularly solid rocket motors—shape competitive strategies as prime contractors form new partnerships to safeguard production scalability.

Key Report Takeaways

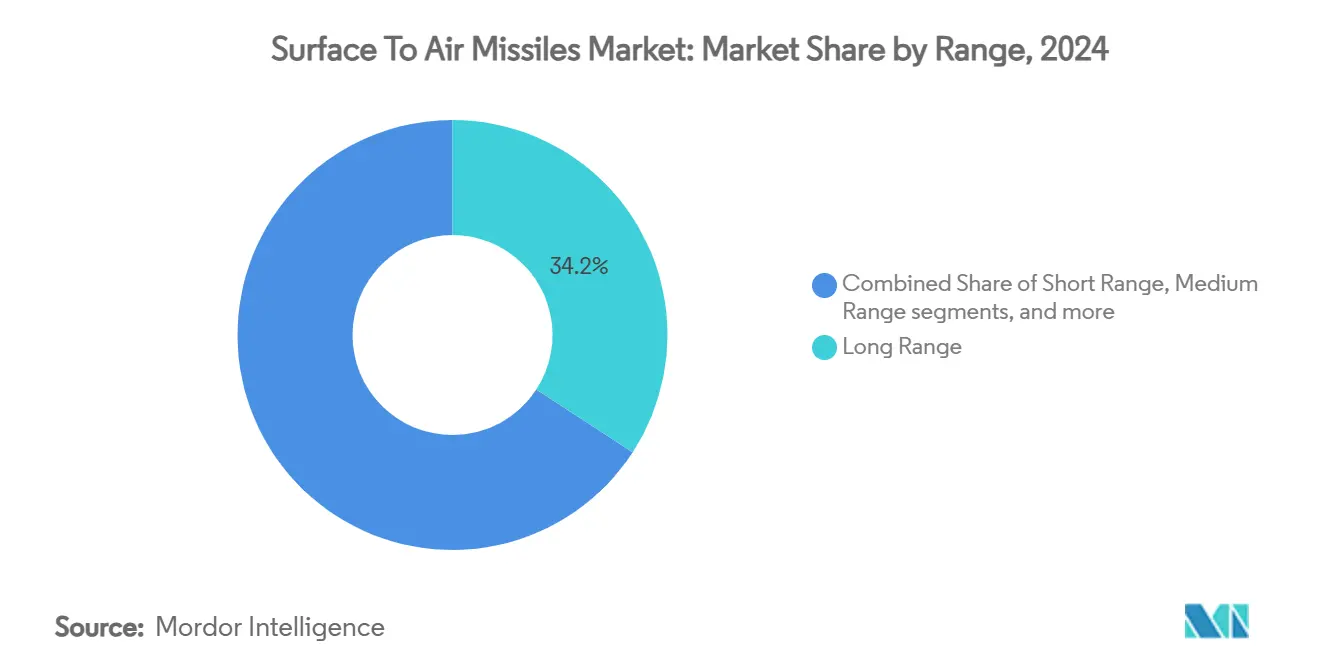

- By range, long-range systems captured 34.18% of the surface-to-air missiles market share in 2024, while extended range variants are projected to post the highest 8.76% CAGR to 2030.

- By launch platform, mobile/land vehicle-mounted platforms held the largest 38.65% revenue share of the surface-to-air missiles market in 2024. In contrast, naval-based platforms are forecasted to register the quickest 7.21% CAGR through 2030.

- By propulsion type, solid propulsion accounted for 71.20% of the surface-to-air missiles market size in 2024; ramjet/scramjet technologies are accelerating at an 8.18% CAGR over the same period.

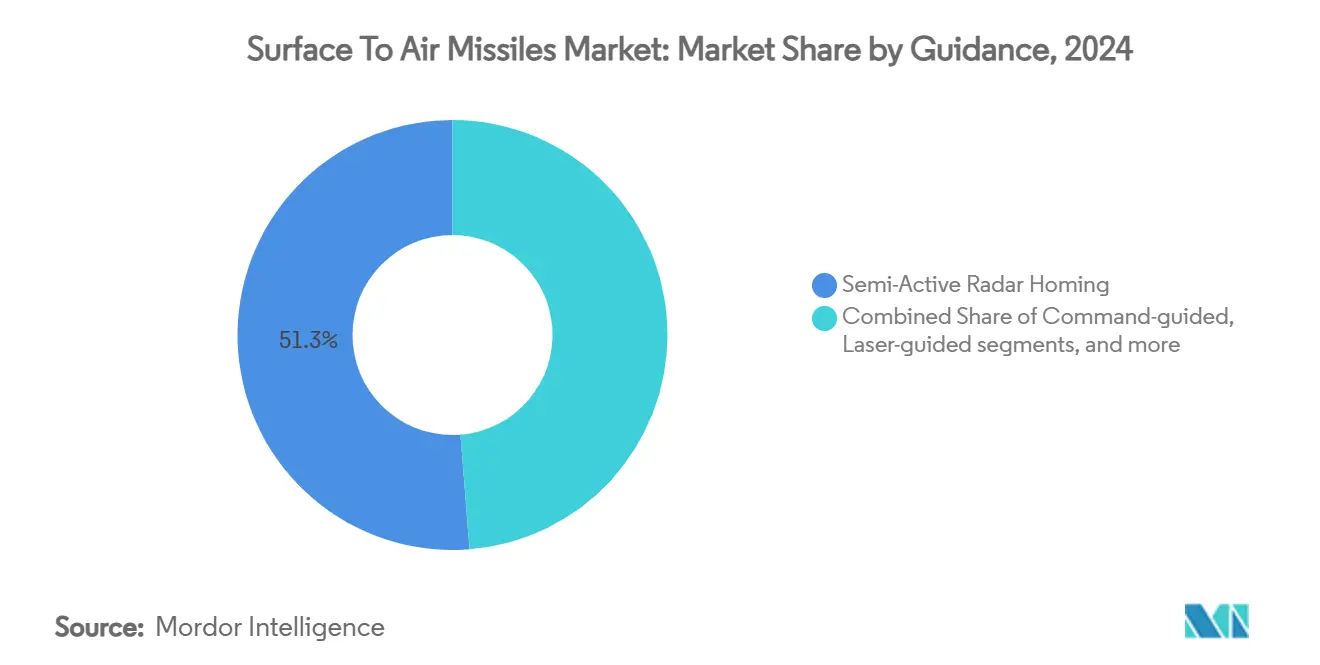

- By guidance, semi-active radar homing captured 41.01% share in 2024, while laser-guided systems are rising fastest at a 7.65% CAGR through 2030.

- By speed class, supersonic missiles held 56.71% of sales in 2024, and hypersonic interceptors are increasing at an 8.33% CAGR to 2030.

- By geography, North America dominated the surface-to-air missiles market with a 32.78% share in 2024, whereas Asia-Pacific is projected to grow at an 8.75% CAGR through 2030.

Global Surface To Air Missiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense expenditures driven by intensifying great-power rivalry | +1.8% | Global with concentration in NATO, Asia-Pacific, Middle East | Medium term (2-4 years) |

| Accelerated replacement and modernization of aging surface-to-air missile systems | +1.5% | North America, Europe, select Asia-Pacific nations | Long term (≥ 4 years) |

| Increasing threat from UAVs, cruise missiles, and hypersonic weapons requiring advanced intercept capabilities | +2.1% | Global, particularly Eastern Europe, Middle East, Indo-Pacific | Short term (≤ 2 years) |

| Growing adoption of network-enabled, cooperative engagement architectures for integrated air defense | +1.2% | NATO countries and advanced Asia-Pacific militaries | Medium term (2-4 years) |

| Rapid deployment of canisterized, road-mobile launch platforms in developing defense markets | +0.9% | Asia-Pacific, Middle East, emerging markets | Medium term (2-4 years) |

| Government-led co-development programs fostering domestic industrial participation and capability building | +0.7% | India, South Korea, European Union, select Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Defense Expenditures Driven by Intensifying Great-Power Rivalry

Considerable powers are allocating unprecedented sums to reconstitute layered air defenses. NATO’s resolve to devote 5% of its collective GDP to defense by 2035 equates to a potential USD 1.4 trillion outlay, with a meaningful portion earmarked for ground-based intercept solutions that were neglected after the Cold War. The United States is accelerating procurement cycles under multi-year contracts, guaranteeing industrial throughput stability. Middle Eastern military budgets expanded 21.8% to USD 195.4 billion in 2024 as regional actors strengthened protection for energy infrastructure and urban centers. East Asian governments followed suit, lifting spending by 6.2% to USD 411 billion due to China’s force posture and long-range precision strike arsenal.[1]“East Asia military spending up 6.2% as China tensions mount,” Nikkei Asia, nikkei.com The resulting demand spans premium systems such as Patriot and lower-tier interceptors that permit sustained operations without unsustainable cost-exchange ratios. Modernization mandates and forward-deployed contingents reinforce the surface-to-air missiles market across all range classes.

Accelerated Replacement and Modernization of Aging Surface-to-Air Missile Systems

Cold-War-era interceptors are approaching obsolescence, driving urgent recapitalization. Germany ordered an additional Patriot battery valued at USD 1.2 billion in 2024 to close capability gaps revealed by the Ukraine conflict. The Netherlands closed a USD 529 million Patriot deal to backfill assets transferred to Kyiv and uphold the readiness of NATO. Within Asia-Pacific, South Korea budgeted USD 1.19 billion for its indigenous L-SAM program, underscoring the momentum toward tiered defense constructs capable of intercepting ballistic missiles at 40-60 km altitudes. These programs are not isolated purchases but components of systematic force overhauls intended to ensure technological advantage well into the 2030s.

Increasing Threat from UAVs, Cruise Missiles, and Hypersonic Weapons Requiring Advanced Intercept Capabilities

The ubiquity of inexpensive drones and the rapid maturation of hypersonic cruise missiles are challenging legacy engagement envelopes. Washington allocated USD 6.9 billion to hypersonic defense research in its 2025 budget, recognizing the limited reaction time presented by Mach 5-plus threats. Chinese demonstrations of near-space hypersonic drones, such as the MD-22, highlight an expanding target spectrum that traditional radar and missile systems struggle to track. As a result, procurement pipelines increasingly include multi-mode seekers, agile data links, and high-velocity interceptors designed to defeat maneuvering vehicles at high altitudes. The US Counter-Unmanned Aerial Systems market alone is valued at USD 10.1 billion over 2024-2029, evidencing the growing emphasis on converged kinetic and non-kinetic solutions.

Growing Adoption of Network-Enabled, Cooperative Engagement Architectures for Integrated Air Defense

Network-centric doctrine is redefining how air defense resources are coordinated. The US Navy’s Cooperative Engagement Capability provides fire-control-quality tracks to dispersed units, enabling simultaneous, cooperative missile launches against fast-moving threats. The Army’s Integrated Battle Command System fuses multiple sensors and effectors to establish a single, resilient kill chain for ballistic, cruise, and drone targets. Poland’s selection of this architecture illustrates export traction for systems that deliver shared situational awareness and improved battalion-level flexibility. Such frameworks expand engagement bubbles, extend detection ranges, and optimize munition expenditure rates, making them central to new acquisition requirements.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and life-cycle costs compared to alternative air defense systems | -1.1% | Global, focused on cost-sensitive markets | Medium term (2-4 years) |

| Strict export regulations under ITAR and MTCR frameworks limiting global sales opportunities | -0.8% | Global, affecting US and allied exporters | Long term (≥ 4 years) |

| Long development and testing timelines delaying system fielding and operational readiness | -0.6% | Advanced defense markets | Long term (≥ 4 years) |

| Supply chain constraints in solid rocket motor production impacting program scalability | -1.3% | Global, concentrated in US and allied bases | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Life-Cycle Costs Compared to Alternative Air Defense Systems

Premium interceptors carry high procurement and sustainment price tags that strain budgets, especially where drone and rocket attacks outpace more expensive missile salvos. Bahrain has faced unfavorable cost-exchange ratios when launching USD 3 million Patriot interceptors at USD 30,000 drones, a dilemma common across the Gulf.[2]“Middle East Nations Need Less Expensive Air, Missile Defense Tech,” National Defense Magazine, nationaldefensemagazine.org Competitively priced alternatives such as China’s HQ-9, marketed between USD 200-400 million per battery, are challenging US and European dominance in price-sensitive regions. Directed energy weapons (DEWs) and cheaper kinetic rounds are advancing, but they remain several years from wide-scale fielding, leaving a near-term affordability gap.

Strict Export Regulations Under ITAR and MTCR Frameworks Limiting Global Sales Opportunities

Category IV of the United States Munitions List places surface-to-air missiles under stringent congressional notification thresholds, constraining lead-time responsiveness and complicating licensing for third-party components. Non-MTCR suppliers, notably Russia and China, exploit these restrictions to secure contracts in regions where Western exporters encounter approval delays. The 2025 Defense Export Handbook underscores how early incorporation of Defense Exportability Features can mitigate some risks by embedding technology-protection mechanisms at the design stage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Range: Extended Reach Drives Next-Generation Capabilities

Long-range systems retained a 34.18% surface-to-air missiles market share in 2024 due to theater-level air defense requirements across NATO and Indo-Pacific alliances. Extended-range missiles, however, are pacing the segment with an 8.76% CAGR through 2030 as operators seek engagements well beyond 150 km to counter standoff bombers and missile carriers. This growth trajectory is closely tied to ramjet propulsion breakthroughs and network-enabled guidance that permit off-board cueing from airborne early-warning assets.

The surface-to-air missiles market size for extended-range variants is set to climb alongside hypersonic defense investments, while their integration into modular launchers lowers infrastructure costs. Long-range interceptors remain indispensable for defending capital assets, yet emerging operational doctrine pairs them with medium and very-short-range layers to optimize cost per shot. Protracted conflicts have demonstrated the need for diversified inventories where low-cost interceptors handle mass drone attacks and high-performance missiles tackle ballistic or hypersonic weapons.

By Launch Platform: Naval Modernization Accelerates Growth

Mobile/Land vehicle-mounted solutions dominated 38.65% of revenue in 2024, reflecting the preference for highly mobile batteries that survive counter-fire and redeploy rapidly. Naval platforms are on track for a 7.21% CAGR as surface fleets modernize and add vertical launch capacity for area defense roles.

A fleet of new frigates and destroyers in Europe and Asia is fitted with canisterized CAMM, Aster, and Standard Missile interceptors, thus raising the surface-to-air missiles market size allocated to sea-based applications. Fixed-site launchers retain relevance for critical infrastructure but are increasingly secondary to mobile or shipboard systems that can reposition as the battlespace evolves. Man-portable air defense systems (MANPADS) remain niche, providing last-ditch protection to maneuver formations.

By Propulsion Type: Advanced Technologies Challenge Solid Fuel Dominance

Solid fuel motors comprised 71.20% of the 2024 shipment value, underscoring their proven robustness and low-maintenance storage profile. Ramjet- and scramjet-equipped interceptors are climbing at an 8.18% CAGR as defense planners address hypersonic trajectories that require sustained thrust throughout endgame maneuvers.

The surface-to-air missiles market share for solid propulsion could narrow slightly as advanced energetic materials boost specific impulse in combined-cycle engines. Hybrid systems, while technically promising, face safety and handling constraints. Liquids find limited use outside strategic or test environments due to logistical burdens, while cryogenic propulsion remains confined to national missile defense interceptors.

By Guidance: Laser and Advanced Seekers Drive Innovation

Semi-active radar homing held 41.01% of 2024 revenue as it balances cost, maturity, and resilience against moderate jamming. Laser beam-riding missiles are forecasted to post a 7.65% CAGR to 2030 as their immunity to radiofrequency jamming and low conspicuity proves advantageous in denied environments.

The surface-to-air missile market size tied to multi-mode seekers is also increasing as operators demand flexibility against stealthy or cluttered targets. Integrating artificial intelligence (AI) for automatic target recognition is improving discrimination and hit probability while reducing reliance on operator intervention. Command-guided and infrared systems continue servicing specialized roles, although their growth lags radar and laser segments.

By Speed Class: Hypersonic Capabilities Reshape Engagement Paradigms

Supersonic designs generated 56.71% of 2024 turnover, supporting defense against conventional aircraft and missiles. Hypersonic interceptors, while a fraction of current deliveries, show an 8.33% CAGR given the urgent need to match offensive weapons traveling beyond Mach 5.

Hypersonic interceptor development elevates demands on high-temperature materials, real-time guidance algorithms, and wide-band sensor coverage. The surface-to-air missiles market share for subsonic interceptors remains stable for low-slow threats. Yet, procurement focus is moving toward mixed inventories capable of tailored responses based on threat vector and cost.

Geography Analysis

North America maintained a 32.78% revenue lead in 2024, driven mainly by US multiyear contracts for Patriot PAC-3 MSE and IFPC increments. The region benefits from a deep industrial base, export financing tools, and a steady pipeline of foreign military sales to allied nations.[3]“Pentagon Goes All-In: US Quadruples PAC-3 MSE Missile Orders,” United24 Media, united24media.com Canada’s synchronized modernization under the Defence Development Sharing Program, which aligns sensor and interceptor standards for binational operations, reinforces North American demand.

Asia-Pacific is the fastest expanding geography at an 8.75% CAGR through 2030, reflecting heightened tensions in the Taiwan Strait, South China Sea, and the Korean Peninsula. Regional programs such as L-SAM, Akash-NG, and Japan’s Aegis Ashore derivative illustrate a three-layered defensive posture that pairs nationally brewed interceptors with US systems to ensure depth and redundancy. India’s pursuit of the S-500 Prometheus indicates an ambition to out-range emerging Chinese air-breathing threats while complementing existing S-400 coverage.

Europe is deciding between continued reliance on US Patriot and investment in indigenous solutions such as SAMP/T NG. Belgium’s selection of SAMP/T and France’s order for eight systems underscore the drive for sovereign industrial capability, which, in turn, buffers against transatlantic supply constraints. Eastern European members prioritize rapid deliveries and interoperability to close gaps exposed by the Ukraine conflict.

The Middle East and Africa combine robust purchasing power with acute threat environments. Saudi Arabia’s USD 78 billion 2025 defense budget and its USD 15 billion layered system integration—including THAAD, Pantsir-S1M, and Silent Hunter lasers—illustrate the fusion of US, Russian, Chinese, and European technologies to counter rockets, drones, and ballistic missiles simultaneously. African modernization is more gradual, constrained by budget but stimulated by critical infrastructure protection around energy corridors.

South America remains a niche opportunity characterized by focused event security and border protection purchases. However, Brazil’s ongoing strategic partnership with European missile houses could seed a regional center for assembly and maintenance, supporting incremental demand as neighboring states upgrade aging inventories.

Competitive Landscape

The surface-to-air missiles market exhibits moderate concentration. Five prime contractors—Lockheed Martin Corporation, RTX Corporation, MBDA, Almaz–Antey Air and Space Defence Corporation, and Israel Aerospace Industries Ltd.—collectively controlled over 50% of global revenue in 2024. Lockheed Martin Corporation secured USD 10 billion in missile awards during Q1 2025, highlighting scale advantages in R&D, supply chain leverage, and lobbying resources.[4]“Lockheed Martin reports USD 10 billion in advanced air and missile systems contracts,” Army Recognition, armyrecognition.com Raytheon, striving to alleviate solid-motor bottlenecks, established a multi-source strategy that brings in Nammo and Avio, thereby reducing dependence on an overstretched domestic base.

European manufacturers differentiate through all-azimuth radars, reduced crew footprints, and rapid emplacement. SAMP/T NG’s 360-degree radar and modular booster options challenge Patriot dominance at the battalion level. South Korean producers, leveraging lower labor costs and agile decision cycles, are carving export share by offering PAC-3-comparable performance at reduced prices, which resonates in markets balancing capability and affordability.

The focus of innovation is shifting toward artificial intelligence, autonomous seeker updates, and reduced recurring cost per intercept. Companies exploring directed energy are poised to disrupt the engagement mix, though production-ready platforms will likely coexist with missiles rather than replace them inside the 2025-2030 horizon. White-space innovation extends to vertical take-off drone interceptors and containerized launch cells designed for commercial ships, offering additional revenue streams for agile firms.

Surface To Air Missiles Industry Leaders

Lockheed Martin Corporation

RTX Corporation

MBDA

Almaz–Antey Air and Space Defence Corporation

Israel Aerospace Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Ministry of Defence (MoD) signed a contract worth INR 2,960 crore (USD 342.5 million) with Bharat Dynamics Limited (BDL) to supply the Indian Navy with Medium-Range Surface-to-Air Missiles (MRSAM).

- November 2024: The US Army awarded Lockheed Martin a contract modification to increase the annual production capacity of Patriot Advanced Capability-3 (PAC-3) Missile Segment Enhancement missiles from 550 to 650 units, addressing global demand and strengthening air defense capabilities for warfighters and allies.

- October 2024: The Saudi Ministry of Defense announced the integration of six air defense systems into its Armed Forces. The deployment of these multi-national systems strengthens the country's defense capabilities against ballistic missiles, drones, and precision-guided weapons.

Global Surface To Air Missiles Market Report Scope

| Very Short Range |

| Short Range |

| Medium Range |

| Long Range |

| Extended Range |

| Man-Portable |

| Mobile/Land Vehicle-Mounted |

| Fixed-Site Ground Installations |

| Naval-based |

| Solid |

| Liquid |

| Hybrid |

| Cryogenic |

| Ramjet/Scramjet |

| Command-guided |

| Semi-Active Radar Homing |

| Infrared (IR) Homing |

| Laser-guided |

| Subsonic |

| Supersonic |

| Hypersonic |

| North America | United States | |

| Canada | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Range | Very Short Range | ||

| Short Range | |||

| Medium Range | |||

| Long Range | |||

| Extended Range | |||

| By Launch Platform | Man-Portable | ||

| Mobile/Land Vehicle-Mounted | |||

| Fixed-Site Ground Installations | |||

| Naval-based | |||

| By Propulsion Type | Solid | ||

| Liquid | |||

| Hybrid | |||

| Cryogenic | |||

| Ramjet/Scramjet | |||

| By Guidance | Command-guided | ||

| Semi-Active Radar Homing | |||

| Infrared (IR) Homing | |||

| Laser-guided | |||

| By Speed Class | Subsonic | ||

| Supersonic | |||

| Hypersonic | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What value does the surface to air missiles market reach by 2030?

It is projected to reach USD 8.53 billion in 2030 based on a 6.11% CAGR forecast.

Which launch platform category grows the fastest toward 2030?

Naval-based platforms post the quickest 7.21% CAGR due to fleet modernization across multiple maritime powers.

Which geographic region records the highest growth through the forecast period?

Asia-Pacific advances at an 8.75% CAGR, propelled by territorial security imperatives and large-scale modernization drives.

How dominant are solid fuel motors in current interceptor deliveries?

Solid propulsion held 71.20% of 2024 shipment value, although its share is slowly eroding as ramjet and scramjet solutions emerge.

What is driving demand for network-enabled air defense architectures?

The need for cooperative engagement against mass drone swarms and hypersonic missiles is encouraging adoption of integrated command systems that fuse multiple sensors and effectors.

Page last updated on: