Surface-to-Surface Missiles Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 10.97 Billion |

| Market Size (2030) | USD 15.31 Billion |

| Growth Rate (2025 - 2030) | 6.89% CAGR |

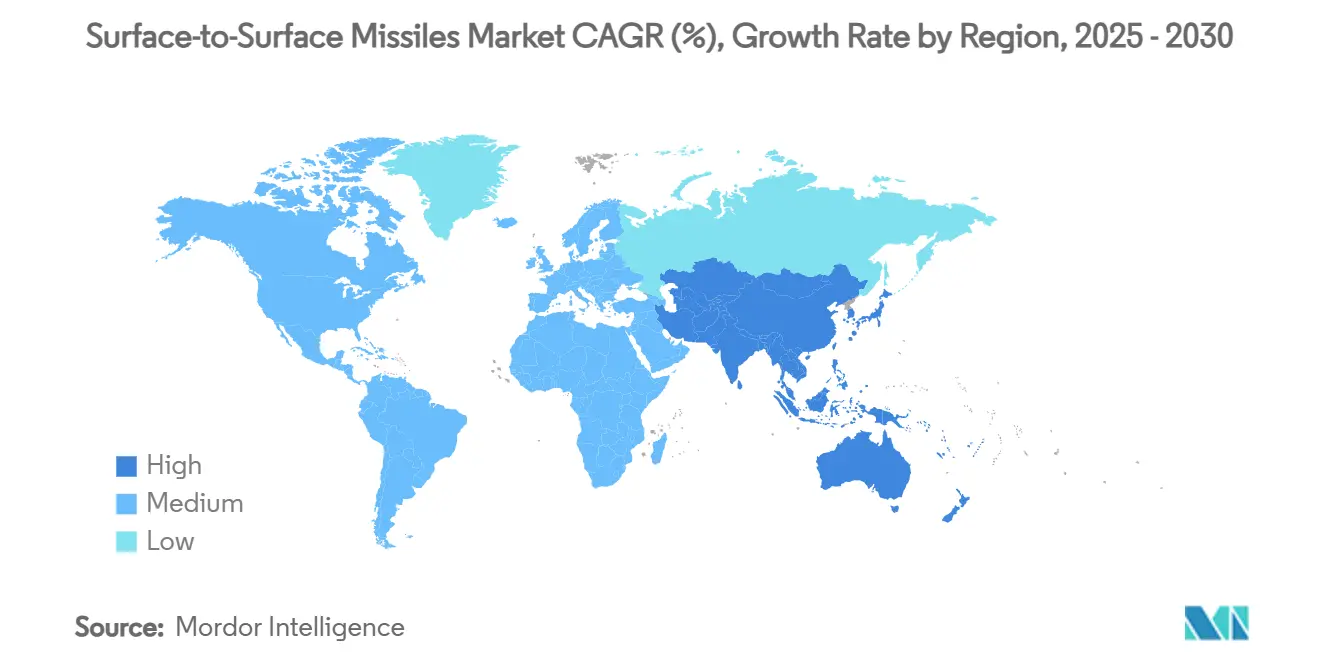

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

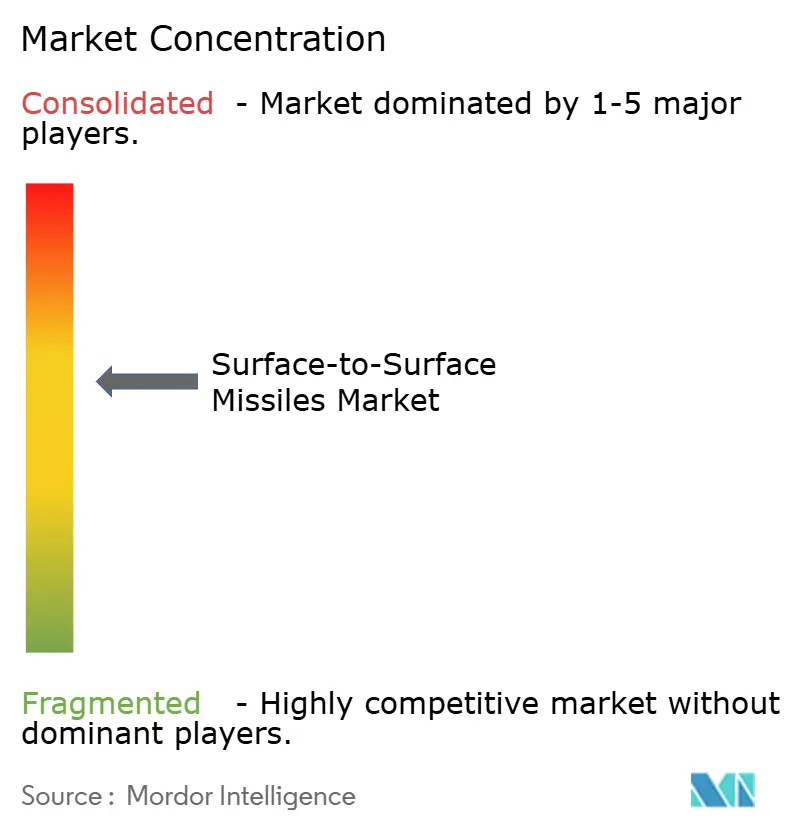

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surface-to-Surface Missiles Market Analysis by Mordor Intelligence

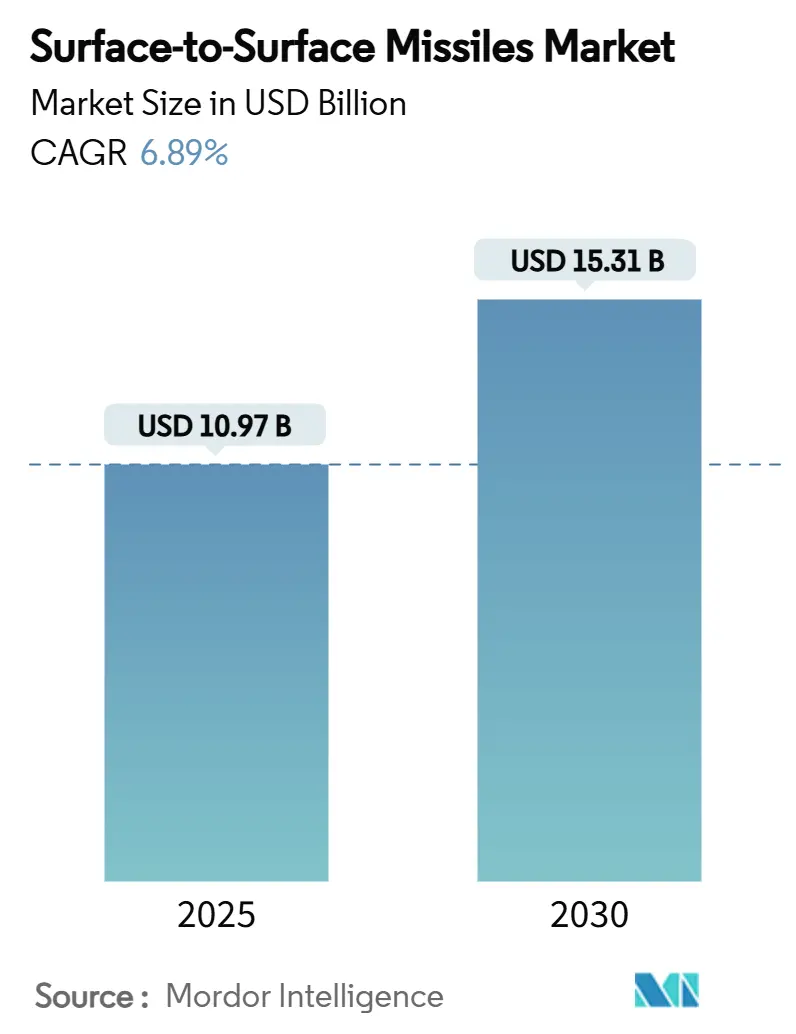

The surface-to-surface missiles market size stood at USD 10.97 billion in 2025 and is forecasted to reach USD 15.31 billion by 2030, translating into a 6.89% CAGR across the assessment period. Heightened great-power rivalry, steady defense outlays, and the strategic need to replace ageing Cold War-era inventories keep demand upward. Solid-propellant systems presently dominate volumes because they store well and launch quickly, while hypersonic programs built around ramjet and scramjet propulsion represent the fastest-growing technological niche. Asia-Pacific registers the sharpest regional expansion on the back of Chinese, Indian, and Japanese force-modernization initiatives. Yet, North America retains the largest revenue pool due to the United States’ sustained procurement pipeline. Program spending visibility, protected national industrial bases, and a clear preference for mobile, survivable launchers underpin a stable, mid-single-digit growth outlook for the surface-to-surface missiles market.

Key Report Takeaways

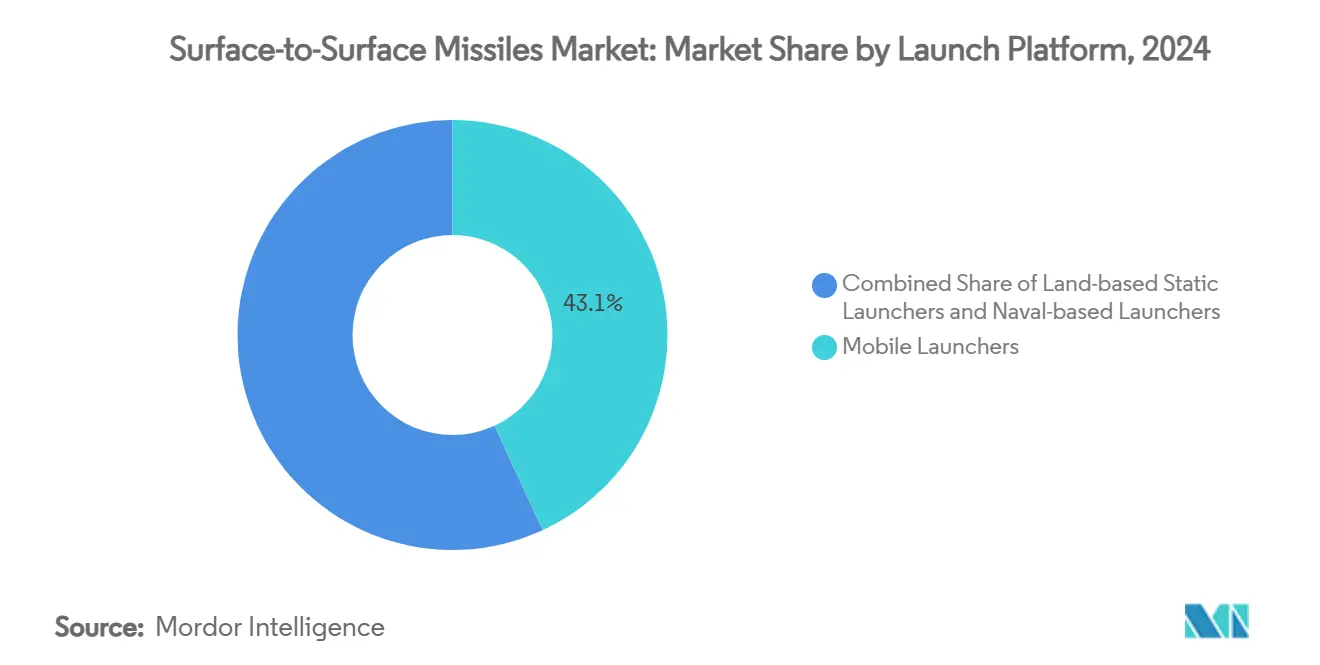

- By launch platform, mobile launchers held 43.11% of the surface-to-surface missiles market share in 2024, whereas naval launchers are projected to advance at a 7.86% CAGR to 2030.

- By range class, short-range missiles held a 38.65% share of the surface-to-surface missiles market in 2024, while intermediate-range systems are forecast to expand at an 8.12% CAGR through 2030.

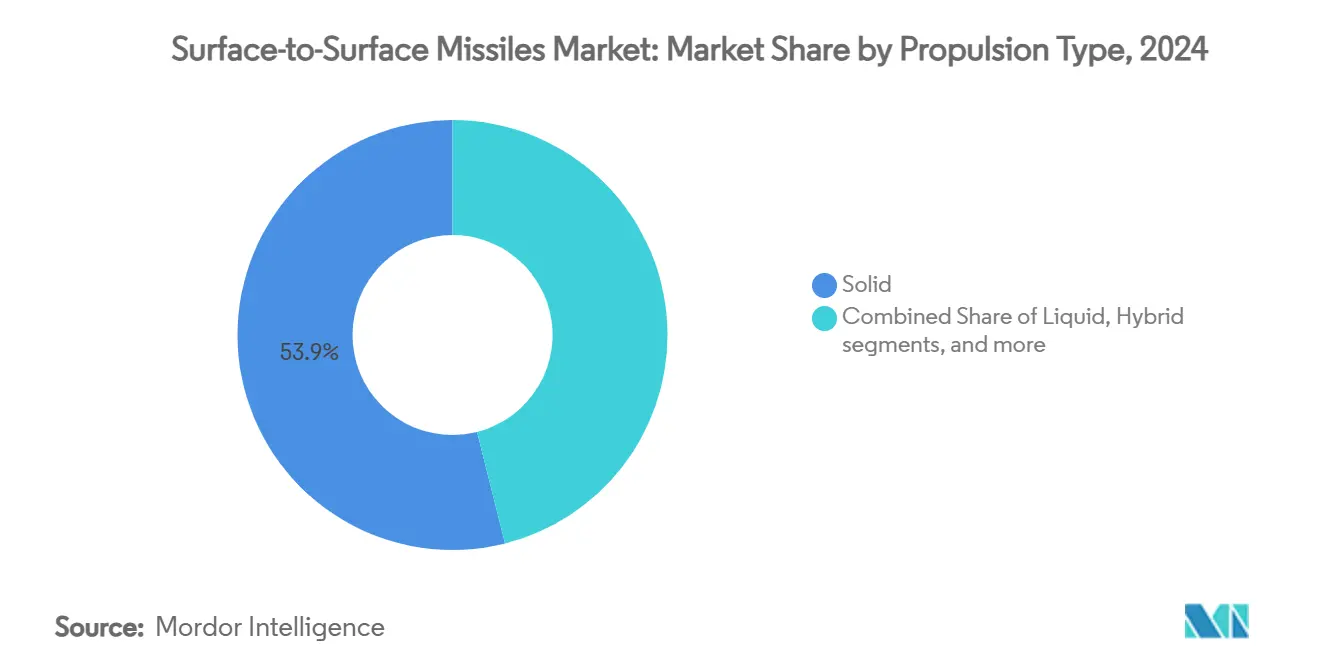

- By propulsion, solid-fuel designs commanded 53.92% of the surface-to-surface missiles market share in 2024, and ramjet/scramjet platforms are growing at a 9.01% CAGR.

- By guidance, inertial navigation led with 40.15% revenue share in 2024, while satellite/GPS-aided missiles register the highest projected CAGR at 8.23% through 2030.

- By speed class, supersonic platforms generated 43.72% of 2024 revenue, and hypersonic systems are pacing at a 9.25% CAGR to 2030.

- By geography, North America absorbed 33.10% of 2024 turnover, whereas Asia-Pacific is set to record an 8.31% CAGR between 2025 and 2030.

Global Surface-to-Surface Missiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense budgets amid intensifying great-power competition | +1.8% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Accelerated modernization and replacement of legacy ballistic inventories | +1.2% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Growing demand for precision-guided long-range strike capabilities in multi-domain operations | +1.4% | Indo-Pacific and European theaters | Medium term (2-4 years) |

| Growing global emphasis on indigenous missile development programs | +0.9% | Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Proliferation of road-mobile transporter erector launchers (TELs) enabling dispersed launch tactics | +0.7% | Global, with emphasis on contested regions | Short term (≤ 2 years) |

| Advancements in miniaturized navigation and guidance technologies | +0.6% | Global, technology-driven adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Defense Budgets Amid Intensifying Great-Power Competition

Global defense allocations moved decisively toward peer-warfare postures. The United States’ FY 2025 top-line defense bill reached USD 886 billion, with USD 33.4 billion earmarked for missile procurement and development. China’s military outlays exceeded USD 300 billion, channeling resources into mass-production lines that now turn out more than 700 Iskander-class missiles annually. European spending rose 18% in 2024, with Germany reserving EUR 85 billion (USD 99.80 billion) through 2030 for modernization programs. Accelerated procurement of long-range strike assets reflects an urgent push to deter near-peer threats. Robust multi-year funding commitments offer suppliers predictable production horizons, reinforcing a stable demand backbone for the surface-to-surface missiles market.

Accelerated Modernization and Replacement of Legacy Missile Inventories

Cold War-era arsenals show obsolescence in reliability, survivability, and precision metrics. The US Army retired the MGM-140 ATACMS and shifted to the Precision Strike Missile, doubling operational reach while fitting current launch vehicles. Russia tripled Iskander production to refresh ageing equipment, and India fielded the indigenous solid-fuel Pralay to succeed the older Prithvi class. These modernization cycles typically extend 15–20 years, guaranteeing recurring procurement windows well beyond immediate crises. For manufacturers, the shift replaces low-margin sustainment work with higher-value new-build contracts, sustaining expansion for the surface-to-surface missiles market.

Growing Demand for Precision-Guided Long-Range Strike Capabilities in Multi-Domain Operations

Contemporary doctrine calls for synchronized effects across land, sea, air, space, and cyber. Long-range missiles fitted with multi-mode seekers now strike with sub-meter accuracy, minimizing collateral damage in congested theaters. The US Navy demonstrated a solid-fuel ramjet launched from an unmanned target drone, pointing to the eventual pairing of hypersonic propulsion with autonomous platforms.[1]“U.S. Navy Successfully Tests Advanced Solid Fuel Ramjet from Unmanned Vehicle,” Defence-Industry Europe, defence-industry.eu Japan is procuring Tomahawk missiles and developing indigenous counter-strike assets, signaling a regional shift toward stand-off deterrence. Artificial-intelligence-enabled guidance packages permit real-time retargeting, supporting dynamic targeting in fluid battlespaces. This premium capability mix lifts average selling prices and reinforces the value accretion visible in the surface-to-surface missiles market.

Growing Global Emphasis on Indigenous Missile Development Programs

Export-control regimes push emerging powers to cultivate homegrown design and production skills. India’s BrahMos-NG entered production in 2025 with Mach 4.5 performance, while BrahMos-II hypersonic work progressed under the India–Russia partnership. South Korea advanced the Hyunmoo family and Turkey field-tested the TAYFUN series, evidencing a broader pivot toward self-reliance. Preferential domestic procurement policies protect these programs, limiting addressable export volumes for foreign primes but simultaneously expanding global installed bases, elevating aftermarket opportunities for the surface-to-surface missiles market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent export controls under international missile technology regimes | -0.8% | Global, affecting non-allied nations | Long term (≥ 4 years) |

| High development and lifecycle costs of hypersonic and dual-use systems | -0.6% | Advanced technology markets | Medium term (2-4 years) |

| Global supply chain shortages of key propellant feedstocks and materials | -0.4% | Global, with acute impacts in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Operational challenges posed by advanced missile defense system deployments | -0.3% | Regional, primarily affecting offensive missile effectiveness | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Export Controls Under International Missile Technology Regimes

The 35-member Missile Technology Control Regime imposes presumptive-denial rules on Category I systems exceeding 300 km range and 500 kg payload. United States regulations under Section 742.5 of Title 15 of the Code of Federal Regulations (CFR) require licensing associated hardware, software, and data, fragmenting the addressable customer set.[2]“15 CFR § 742.5 – Missile Technology,” Cornell Law School, law.cornell.edu Compliance obligations drive administrative overhead and slow deal cycles, particularly for small contractors without specialized export-control teams. Supplier–customer pairings consequently center on treaty allies, limiting global diffusion and restraining upside momentum in the surface-to-surface missiles market.

High Development and Lifecycle Costs of Hypersonic and Dual-Use Systems

Hypersonic projects demand exotic materials, sophisticated computational fluid-dynamics tools, and purpose-built test infrastructure. The US Air Force’s Air-Launched Rapid Response Weapon program experienced cost growth exceeding 50% before its temporary cancellation, spotlighting budgetary hazards. Dual-use missiles able to carry nuclear or conventional payloads confront additional security and certification layers, extended schedules, and inflated total ownership costs. High entry tickets confine competition to cash-rich prime contractors and state-funded entities, dampening innovation diversity and capping growth potential for the surface-to-surface missiles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Launch Platform: Mobile Dominance Drives Survivability

Mobile launchers generated 43.11% of 2024 revenue, underpinning the preference for on-road concealment and frequent repositioning that complicate enemy targeting. North Korea’s 12-axle vehicles and China’s DF-17 road-mobile units illustrate how mobility extends even to theater-range weapons. Naval platforms show the quickest incremental gains, helped by blue-water fleet expansion and the certainty that sea-based assets can skirt terrestrial missile defenses.

Shipborne vertical-launch cells offer multirole flexibility, welcoming cruise and ballistic payloads inside a single architecture. The option to task torpedo-tube-launched ballistic missiles in submarines also broadens survivability. Consequently, naval deployment revenues are expected to reach USD 3.2 billion in 2030, reinforcing supplier appetite for marinized systems. Static silos remain relevant for strategic deterrence in nuclear-armed states. Yet, their share of the surface-to-surface missiles market is set to erode as mobility becomes synonymous with survivability.

By Range: Short-Range Systems Lead Despite Expanding Intermediate-Range Demand

Short-range missiles captured 38.65% revenue in 2024 and continue to anchor tactical deep-fire missions inside 300 km envelopes. The surface-to-surface missiles market size for this range band reached USD 4.24 billion in 2025 and is forecast at USD 5.69 billion by 2030, underpinned by quantities required for high-tempo battlefield employment. Interoperability with legacy MLRS launchers keeps acquisition costs manageable, encouraging large-volume buys.

Intermediate-range weapons with 1,000 to 5,500 km range show the fastest growth at 8.12% CAGR, driven by Indo-Pacific theater requirements, where archipelagic geography places adversary infrastructure at extended distances. Japan’s decision to field Tomahawk Block V and Australia’s push for conventionally armed strike options validate an emerging market sweet spot. These systems bridge strategic and tactical mission sets, enabling one platform to serve a broader target. As a result, intermediate-range volume is expected to surpass 900 annual units by 2030, lifting the surface-to-surface missiles market.

By Propulsion Type: Solid-Fuel Supremacy Meets Ramjet Upside

Solid motors delivered 53.92% of 2024 shipments because they store for years and launch on short notice without fuelling logistics. Despite emerging alternatives, the surface-to-surface missiles market share for solid propulsion is forecast to remain above 50% through 2030. Liquid engines retain niches in heavy-lift strategic roles where impulse density overrides maintenance burden. Hybrid solutions combine liquid oxidizers and solid fuel grains, yet face scale-up barriers.

The technology spotlight is on ramjet and scramjet propulsion, which is pacing at a 9.01% CAGR. The US Navy’s 2025 flight test of a solid-fuel ramjet validated a compact, storable design that reaches sustained Mach 4 plus while maintaining the operational convenience of a single-package motor. India’s BrahMos-NG and BrahMos-II pipelines confirm that emerging economies also use air-breathing propulsion as a credible missile-defense countermeasure. This dual dynamic ensures healthy competition and continued research investment in the surface-to-surface missiles market.

By Guidance: Inertial Systems Retain Primacy as Satellite Aids Surge

Inertial navigation delivered 40.15% of 2024 sales owing to full autonomy from external signals, a critical attribute under electronic-warfare conditions. High-grade ring-laser and fiber-optic gyros now fit compact missile frames, aligning accuracy with stringent rules of engagement. Satellite-aided options advance fastest at 8.23% CAGR as multi-constellation services, including GPS, Galileo, and BeiDou, reduce dependency on any single provider. However, jamming vulnerability forces designers to adopt blended solutions.

Terminal seekers—whether radar, imaging infrared, or millimeter-wave—add last-second correction against moving, hardened, or deeply buried targets. Development focus shifts to artificial intelligence-driven scene-matching algorithms that accelerate discrimination in cluttered environments. As military customers demand redundancy, tri-mode guidance stacks are becoming common, uplifting bill-of-material values and raising the average selling price within the surface-to-surface missiles market.

By Speed Class: Supersonic Baseline Faces Hypersonic Momentum

Supersonic missiles formed 43.72% of 2024 revenue due to decades-long field experience and balanced cost-performance metrics. Subsonic cruise designs keep relevance for endurance missions, yet their share diminishes as defenders raise interception proficiency. Hypersonic platforms, moving above Mach 5, yield the steepest CAGR at 9.25%. The revived US Air-Launched Rapid Response Weapon and Russia’s Kinzhal deployment incentivize other actors to accelerate comparable programs, fostering a technology-race narrative that lifts research budgets.

Thermodynamic loads at these speeds necessitate advanced ceramic composites, cooling innovations, and novel test protocols. Suppliers who field manufacturable thermal-protection systems win early contracts, reflecting how materials science leadership is now strategic. Consequently, hypersonic maturation is the pre-eminent technology escalator propelling value expansion within the surface-to-surface missiles market.

Geography Analysis

North America remained the revenue leader with 33.10% share in 2024, anchored by the United States’ USD 33.40 billion missile procurement line and production facilities spanning boosters, seekers, and launchers. Canada’s NORAD modernization injects incremental demand for integrated command-and-control and joint test activity. The surface-to-surface missiles market size for the region will likely cross USD 5.2 billion by 2030 as mid-decade block buys for hypersonic glide vehicles reach production maturity.

Asia-Pacific is the quickest climber, posting an 8.31% CAGR through 2030. China’s capacity expansion now outputs more than 700 theater-range missiles annually, while India’s BrahMos-NG serial production secures a sustained domestic base and potential export inventory. Japan, South Korea, and Australia all fund long-range precision fires in response to regional security shifts, translating into an incremental USD 1.9 billion in annual addressable spending by 2030. This intense procurement tempo is expected to tighten component supply chains and could catalyze new JV manufacturing sites across Southeast Asia.

Europe holds a solid revenue footprint driven by multinational programs and MBDA’s record EUR 13.8 billion (USD 16.20 billion) order intake in 2024. Franco-German Future Combat Air System missiles and the UK-led Storm Shadow capacity ramp exemplify collaborative models pooling R&D risks. The Middle East attracts US and European vendors as Gulf states integrate THAAD and Patriot PAC-3 defenses, stimulating demand for offensive countermeasures. Africa’s low but rising spend indicates nascent opportunities, especially for export-compliant short-range systems in peace-keeping roles.

Competitive Landscape

The surface-to-surface missiles market exhibits moderate consolidation. Five prime contractors—Lockheed Martin Corporation, RTX Corporation, Northrop Grumman Corporation, MBDA, and Rafael Advanced Defense Systems Ltd.—control the majority of system-level revenue. Lockheed Martin secured a USD 4.94 billion production contract for Precision Strike Missile lots 3 and 4 in 2024, following a USD 3.2 billion JASSM/LRASM ceiling award, reinforcing scale advantages. MBDA’s multinational structure lets it hedge currency fluctuations and win diverse European orders, demonstrated by its 33% output surge in 2024.[3]“Record Orders Push MBDA Output Higher,” Defense One, defenseone.com

Competitive intensity rises in hypersonic and seeker subsystems, where agile mid-tier suppliers offer niche technologies such as additive-manufactured cooling jackets or AI-enabled digital-scene correlation. Yet major primes lock in full-rate production through long-term agreements and in-house component verticalization, creating high switching costs for government buyers. Indigenous players in India, South Korea, and Turkey increasingly compete for home-market volumes, narrowing Western export prospects but expanding partnership avenues around propulsion or guidance co-development. Strategic alliances—such as Japan’s Tomahawk procurement with embedded technology-transfer—illustrate the hybrid competitive-collaborative interplay now customary in the surface-to-surface missiles market.

Surface-to-Surface Missiles Industry Leaders

Lockheed Martin Corporation

RTX Corporation

MBDA

Rafael Advanced Defense Systems Ltd.

Northrop Grumman Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The Japanese Ministry of Defense contracted Mitsubishi Heavy Industries to develop long-range surface-to-surface missiles designed to target both land and maritime objectives.

- November 2024: The US Army awarded Lockheed Martin a USD 752.3 million contract modification to increase the production capacity of Patriot Advanced Capability-3 Missile Segment Enhancement (PAC-3 MSE) missiles. The contract aims to improve the annual production rate from 550 to 650 missiles to meet the global demand for PAC-3 MSE.

Global Surface-to-Surface Missiles Market Report Scope

| Land-based Static Launchers |

| Mobile Launchers |

| Naval-based Launchers |

| Short-Range |

| Medium-Range |

| Intermediate-Range |

| Intercontinental |

| Solid |

| Liquid |

| Hybrid |

| Ramjet/Scramjet |

| Inertial Navigation |

| Satellite/GPS |

| Terminal Guidance |

| Others |

| Subsonic |

| Supersonic |

| Hypersonic |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Launch Platform | Land-based Static Launchers | ||

| Mobile Launchers | |||

| Naval-based Launchers | |||

| By Range | Short-Range | ||

| Medium-Range | |||

| Intermediate-Range | |||

| Intercontinental | |||

| By Propulsion Type | Solid | ||

| Liquid | |||

| Hybrid | |||

| Ramjet/Scramjet | |||

| By Guidance | Inertial Navigation | ||

| Satellite/GPS | |||

| Terminal Guidance | |||

| Others | |||

| By Speed Class | Subsonic | ||

| Supersonic | |||

| Hypersonic | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2025 value of the ballistic surface-to-surface missiles market?

It is valued at USD 10.97 billion with a forecast CAGR of 6.89% toward 2030.

Which launch platform currently dominates demand?

Mobile transporter-erector-launchers hold 43.11% revenue share because militaries prize survivable, road-movable assets.

Why is Asia-Pacific the fastest-growing region?

Chinese mass-production, Indian and Japanese modernization and broader Indo-Pacific security concerns drive an 8.31% CAGR through 2030.

What propulsion technology is expanding quickest?

Ramjet and scramjet engines supporting hypersonic speeds are projected to grow at a 9.01% CAGR.

How do export controls affect sales?

The Missile Technology Control Regime restricts transfers of long-range missiles, limiting suppliers mainly to treaty allies and trimming global market reach.

Page last updated on: