Air-to-Surface Missiles Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

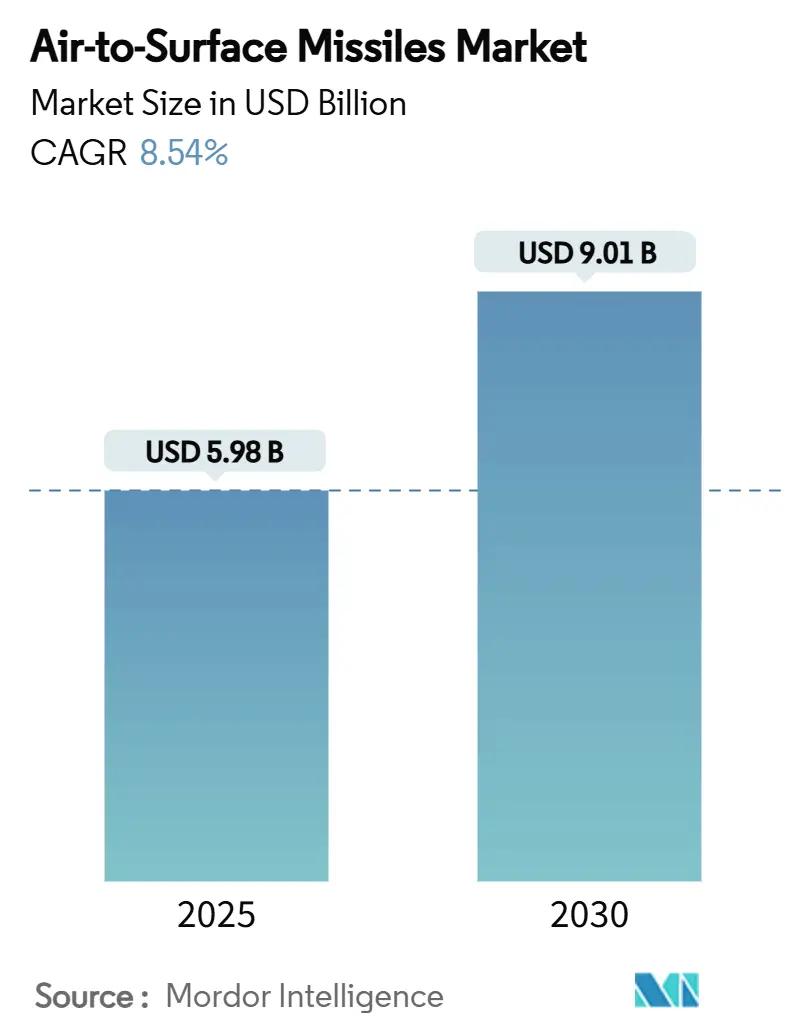

| Market Size (2025) | USD 5.98 Billion |

| Market Size (2030) | USD 9.01 Billion |

| Growth Rate (2025 - 2030) | 8.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air-to-Surface Missiles Market Analysis by Mordor Intelligence

The air-to-surface missiles market size is valued at USD 5.98 billion in 2025 and is forecasted to reach USD 9.01 billion by 2030, expanding at an 8.54% CAGR. Rapid modernization programs, rising regional tensions, and a clear preference for standoff precision strike weapons underpin this expansion, pushing governments to place multi-year orders that de-risk industrial capacity investments. The Pentagon’s USD 29.8 billion munitions request for FY2025, its largest on record, illustrates how buyers front-load demand signals to replenish stockpiles and fund next-generation systems. Hypersonic propulsion breakthroughs, such as Northrop Grumman’s scramjet exceeding Mach 5, compress decision cycles and spur platform upgrades that can carry heavier, faster weapons. At the same time, AI-enabled multi-mode seekers improve survivability against electronic warfare, encouraging adoption across fighter, bomber, and UAV fleets. Finally, production-rate increases—MBDA alone plans to double output by 2025—signal that prime contractors are scaling to meet a higher-volume, longer-duration demand environment.

Key Report Takeaways

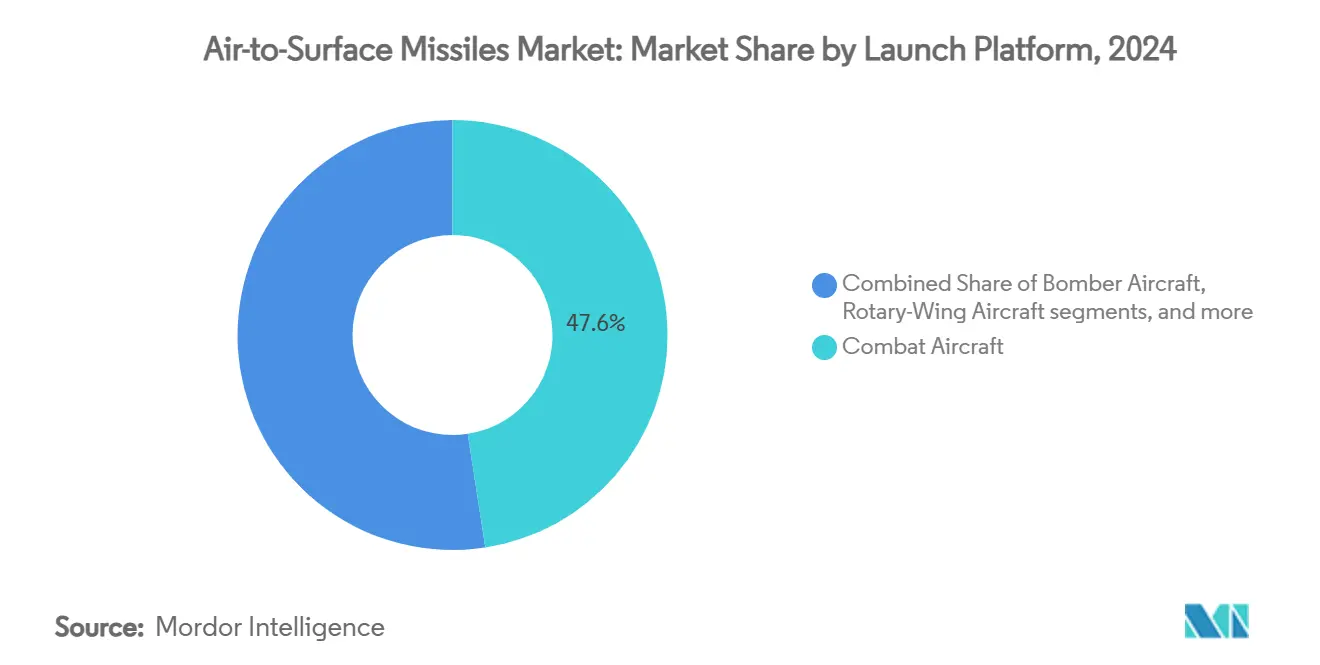

- By launch platform, combat aircraft led with 47.56% of the air-to-surface missiles market share in 2024; UAVs are projected to advance at an 11.25% CAGR through 2030.

- By range, medium-range missiles commanded a 49.21% share of the air-to-surface missiles market in 2024, while long-range variants are expanding at a 10.42% CAGR to 2030.

- By propulsion, solid rocket accounted for 34.75% of the air-to-surface missile market in 2024; ramjet and scramjet solutions are rising at a 9.55% CAGR through 2030.

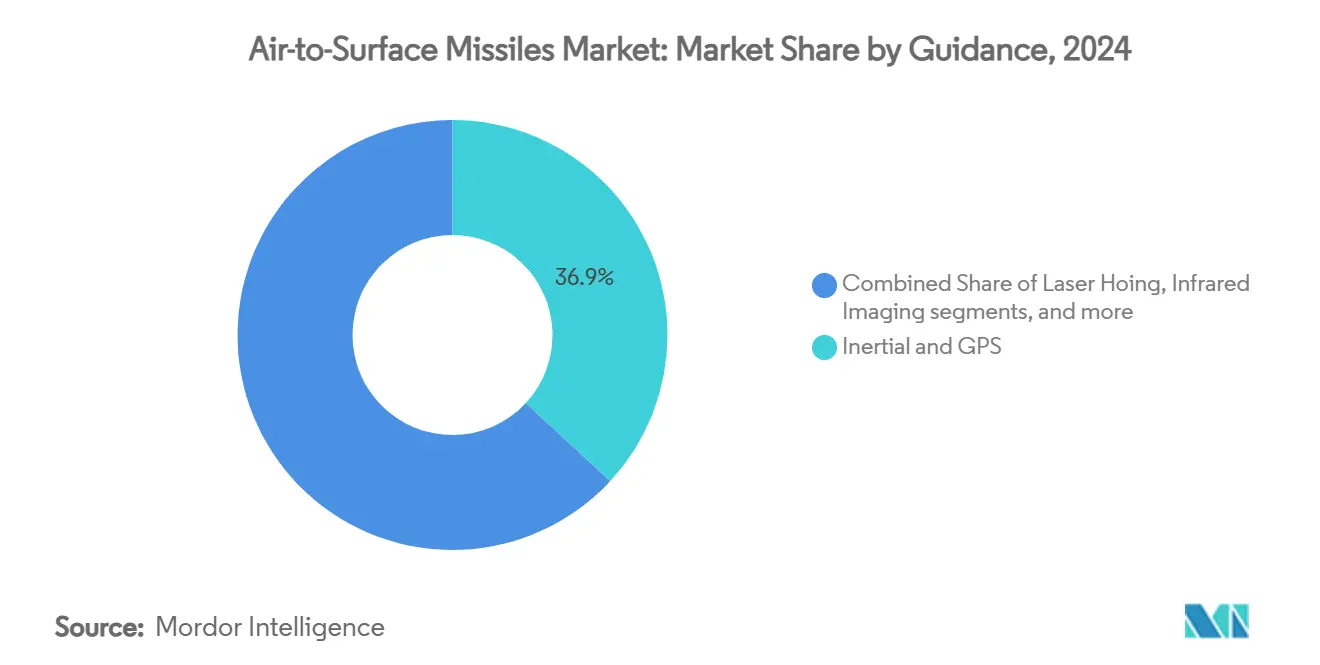

- By guidance, inertial and GPS combinations held 36.89% of the air-to-surface missiles market share in 2024; multi-mode seekers are growing at a 9.91% CAGR over the same period.

- By speed class, subsonic designs retained 58.34% share of the air-to-surface missiles market size in 2024, whereas hypersonic weapons are set to grow at an 11.80% CAGR to 2030.

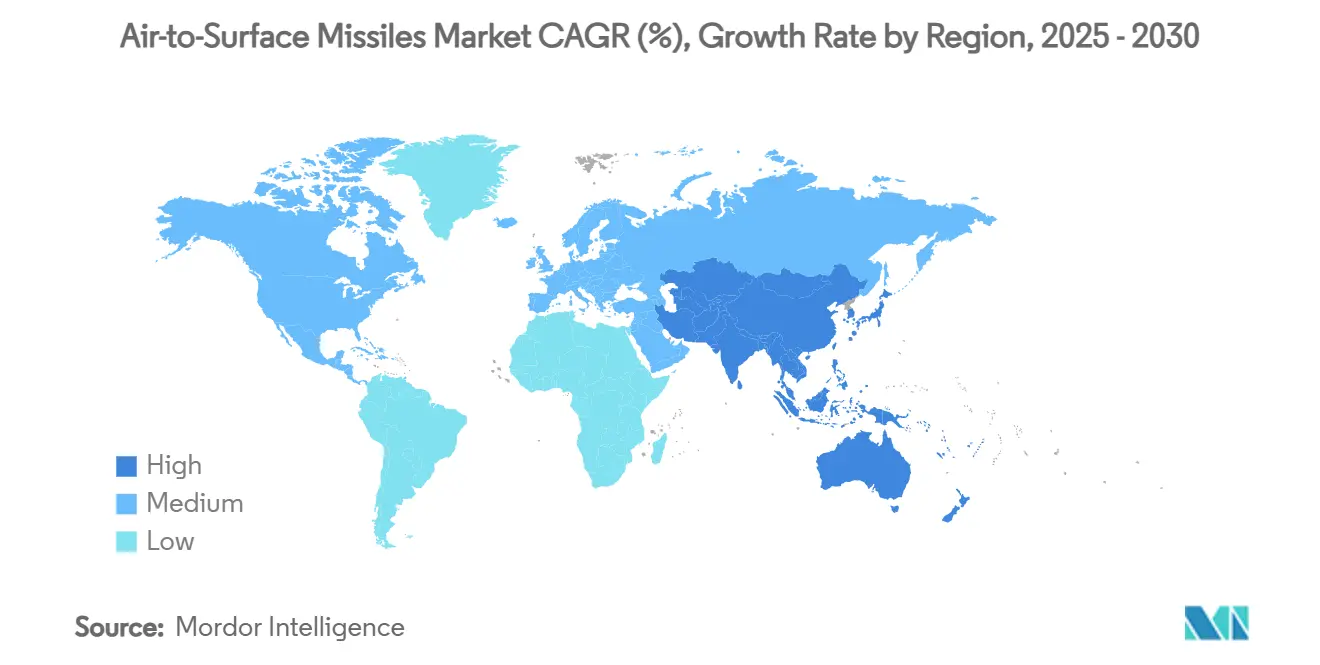

- By geography, North America held 36.18% revenue share in 2024, while Asia-Pacific is set to deliver the highest 10.75% CAGR over 2025-2030.

Global Air-to-Surface Missiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing defense spending allocated to precision-guided strike capabilities | +1.5% | Global | Medium term (2-4 years) |

| Ongoing aircraft modernization programs integrating advanced standoff munitions | +1.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Rising demand for low-collateral-damage munitions in counter-insurgency operations | +1.2% | Middle East, Africa | Short term (≤ 2 years) |

| Emergence of advanced air defense systems driving need for longer-range, high-speed ASMs | +1.4% | Asia-Pacific, Europe, Middle East | Medium term (2-4 years) |

| Adoption of AI-enabled multi-mode seekers improving target accuracy in contested environments | +0.9% | North America, Europe | Long term (≥ 4 years) |

| Development of modular, aircraft-agnostic pylons enabling rapid ASM integration across platforms | +0.6% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Defense Spending Allocated to Precision-Guided Strike Capabilities

Defense ministries channel larger portions of their weapons budgets toward precision munitions because standoff capabilities enable smaller formations to achieve disproportionate effects. The US Navy requested USD 7.9 billion for weapons procurement in FY2026, prioritizing replenishment of high-end stocks depleted by recent operations. East-Asian governments follow suit, evidenced by multiyear procurement frameworks that shield suppliers from volatility in demand. Budget planners view precision weapons as cost-effective force multipliers that deter aggression without needing sustained forward presence. The trend also reflects lessons from recent conflicts where accurate targeting proved decisive while curbing collateral damage. Persistent funding streams create a stable base for suppliers to invest in automation, additive manufacturing, and vertical integration that lower unit costs over time.

Ongoing Aircraft Modernization Programs Integrating Advanced Standoff Munitions

Weapon-agnostic pylons, upgraded power supplies, and software-defined stores management systems are becoming the cornerstone of fighter and bomber life-extension packages. The US Air Force’s Load Adaptable Modular (LAM) pylon for the B-1B increases carriage capacity for heavy hypersonic cruise missiles without redesigning the wing. Similar retrofit concepts for fourth-generation fighters use open-system software to accept new missiles via over-the-air updates rather than depot-level rewiring. As air-to-surface missiles market customers embed such modularity, aircraft procurement decisions increasingly hinge on a platform’s future-proofing, not just its baseline performance. System integrators collaborate early with missile primes to validate form-factor compatibility and digital twin models, compressing certification timelines while ensuring that next-wave weapons will fit legacy fleets.

Rising Demand for Low-Collateral-Damage Munitions in Counter-Insurgency Operations

Continued urban warfare in the Middle East and Africa pushes commanders to favor weapons that deliver pinpoint effects with smaller warheads. Extended-range attack munitions under development for partner nations incorporate navigation that survives GPS degradation and deliver sub-meter accuracy, allowing strikes within dense civilian zones while meeting strict rules of engagement. US doctrine now mandates civilian-harm mitigation assessments before strike approval, which drives seeker innovations such as millimeter-wave + infrared fusion for positive target identification. Original-equipment manufacturers are responding with configurable fuzes, reduced-yield blast-fragmentation designs, and algorithmic target-discrimination software. Such features sustain operational effectiveness while reducing political risk, ensuring continued funding for precision weapons despite tightening defense budgets.

Emergence of Advanced Air Defense Systems Driving Need for Longer-Range, High-Speed ASMs

Layered, sensor-fused air defenses fielded by peer adversaries have pushed offensive weapons well beyond the 400 km range band. Hypersonic air-to-surface missiles travelling above Mach 5 deprive defenders of reaction time, compelling nations to invest in matching or exceeding adversary speed thresholds. US Glide Phase Interceptor funding grew from USD 291.8 million to USD 832.8 million within two fiscal cycles, underscoring how hypersonic threats dictate offensive and defensive procurement. Because high-power radars can now track stealth aircraft, survivability is increasingly vested in missile kinematics and agile flight paths rather than airframe shaping alone. Consequently, the air-to-surface missiles market now rewards propulsion advances that extend range while maintaining terminal maneuverability, pressuring primes to innovate in materials and thermal-protection systems.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent export control regulations limiting cross-border technology transfer | –0.8% | Global | Long term (≥ 4 years) |

| Rising unit costs associated with hypersonic and low-observable missile programs | –1.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Ongoing supply chain vulnerabilities for advanced seeker and navigation components | –0.6% | Global | Short term (≤ 2 years) |

| Environmental and ethical opposition to the deployment of cluster munition variants | –0.4% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Export Control Regulations Limiting Cross-Border Technology Transfer

Successive revisions to the US International Traffic in Arms Regulations expand license requirements for software, design data, and defense services, complicating multinational missile development. Higher registration fees and broader military-end-user definitions dissuade smaller suppliers from entering export markets, narrowing the global supply base. For partner nations, protracted approvals delay co-production, encouraging indigenous alternatives or procurement from non-aligned suppliers. Prime contractors mitigate risk by segmenting design teams and “black-boxing” sensitive sub-systems, but that fragmentation raises integration costs. Over time, export barriers may slow technology diffusion, creating uneven capability gaps that shape regional deterrence balances.

Rising Unit Costs Associated with Hypersonic and Low-Observable Missile Programs

The Government Accountability Office notes that limited industrial experience with thermal-protection materials and precision tooling inflates hypersonic unit costs well above conventional strike weapons.[1]U.S. Government Accountability Office, “Hypersonic Weapons: DOD Could Reduce Cost and Schedule Risks,” gao.gov Dual-mode ramjets, advanced carbon-carbon aeroshells, and high-temperature avionics drive per-round expenses that only a handful of nations can absorb. Although additive manufacturing improves yields, the learning curve remains steep, forcing buyers to trade inventory depth for cutting-edge performance. Budget managers thus confront a capability-quantity dilemma: procure a few exquisite assets or field larger volumes of “good-enough” subsonic alternatives. Until production volumes rise and supply-chain chokepoints ease, affordability will cap hypersonic adoption rates within the air-to-surface missiles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Launch Platform: UAV Integration Accelerates Precision Strike Evolution

Combat aircraft retained 47.56% of the air-to-surface missiles market share in 2024 as multi-role fighters remain the backbone of inventory recapitalization programs. Modern digital store management systems allow these aircraft to employ legacy weapons and next-generation AI-enabled seekers, safeguarding platform relevance beyond 2030. Bomber fleets, led by the B-1B, benefit from modular pylons that double external hard-point capacity, allowing carriage of hypersonic cruise missiles without sacrificing conventional payloads. Rotary-wing assets exploit precision rockets for close-air-support roles where agility and low-altitude survivability matter.

Unmanned aerial vehicles (UAVs) are forecasted to post an 11.25% CAGR, the fastest launch platform, as force planners seek to mitigate pilot risk in dense threat environments. Demonstrations of armed multi-rotor systems validate that even Group 3 UAVs can deliver laser-guided rockets with minimal collateral damage. Swarm tactics and man-unmanned teaming concepts further expand demand for small-form-factor missiles optimized for autonomous flight control. As a result, the air-to-surface missiles market size attributed to UAVs is projected to nearly triple by 2030, cementing drones as indispensable nodes in distributed strike architectures.

By Range: Long-Range Systems Counter Modern Air Defenses

Medium-range weapons, covering 100 km to 400 km, held 49.21% of the air-to-surface missile market size in 2024 due to their versatility across anti-ship, land-attack, and suppression missions. They remain the workhorse category for joint forces that value balanced cost and reach. Short-range missiles—often laser-guided or dual-mode GPS/INS—still dominate close-air support and urban operations where precision outweighs standoff.

Long-range missiles exceeding 400 km are projected to expand at a 10.42% CAGR through 2030. The driver is clear: peer air defenses compel launch platforms to remain outside surface-to-air engagement envelopes. Emerging concepts such as palletized munitions and containerized cruise missiles further blur the line between traditional air launch and multi-domain deployment. Consequently, the air-to-surface missiles market sees procurement agencies underwriting extended-range demonstrations that combine autonomous navigation with hardened data links capable of retasking in flight.

By Propulsion Type: Ramjet Technology Ushers in Hypersonic Era

Solid rocket motors delivered 34.75% of the air-to-surface missiles market share in 2024, retaining supremacy due to mature supply chains and proven reliability across tactical and strategic inventories. Turbojet and liquid-fuel engines service cruise missile niches where endurance and loiter time matter, particularly in anti-ship roles.

Ramjet/scramjet propulsion is growing at a 9.55% CAGR as primes leverage dual-mode cycles that transition from subsonic combustion to supersonic airflow once past Mach 3. GE Aerospace’s recent hypersonic ramjet tests achieved triple the airflow of earlier prototypes, promising higher thrust-to-weight ratios.[2]GE Aerospace, “Dual-Mode Ramjet Test,” geaerospace.com China’s boron-fuel ramjet research, designed for air-to-underwater operation, hints at multi-medium applications that could transform littoral strike doctrines. These breakthroughs will shift the air-to-surface missiles market from platform-constrained to propulsion-constrained engineering, where thermal-protection and additive-manufactured components dictate feasibility.

By Guidance: Multi-Mode Seekers Boost Contested-Environment Survivability

Inertial/GPS combinations delivered 36.89% of the air-to-surface missiles market share in 2024, supplying baseline navigation even when external signals are jammed. Active-radar homing complements anti-ship profiles, while semi-active laser final-guidance modes support low-collateral damage strikes.

Multi-mode seekers—fusing radar, imaging infrared, and semi-active laser—are projected to grow at 9.91% CAGR as electronic-warfare environments become more congested. Raytheon’s StormBreaker demonstrates how machine-learning algorithms classify targets through weather and smoke, enabling “fire-and-forget” profiles that free aircrews for defensive maneuver.[3]Raytheon, “StormBreaker Tri-Mode Seeker,” rtx.com On-board AI also reduces datalink reliance, ensuring that guidance remains uncompromised even if communications are degraded. As cost curves fall, multi-mode architectures will migrate from premium cruise missiles into compact rockets, expanding their penetration across the air-to-surface missiles market.

By Speed Class: Hypersonic Weapons Compress Decision Timelines

Subsonic cruise missiles—valued for fuel efficiency and terrain-following stealth—captured 58.34% of the air-to-surface missile market in 2024. Supersonic designs add kinetic advantage against high-value mobile targets, shortening time-to-impact without incurring the cost premium of hypersonic materials.

Hypersonic missiles above Mach 5 are forecasted to register an 11.80% CAGR through 2030 as major powers race to pre-empt next-generation air defenses. Northrop Grumman’s scramjet flight tests and multi-year HACM demonstrations highlight how government R&D spending accelerates maturity levels. Although production rates remain low due to exotic material requirements, additive manufacturing and modular avionics promise cost reductions. As hypersonic glide vehicles and air-breathing systems converge, speed will transition from niche capability to mainstream requirement, reshaping performance baselines across the air-to-surface missiles market.

Geography Analysis

North America held 36.18% of the air-to-surface missiles market share in 2024, underpinned by the United States’ record munitions budget and an industrial base spanning propulsion, guidance, and warhead integration. Lockheed Martin Corporation secured USD 10 billion in missile awards during Q1 2025, illustrating the region’s unparalleled contract velocity. Demand is further buoyed by NORAD modernization and Arctic defense initiatives that require extended-range, all-weather standoff systems.

Asia-Pacific is the fastest-growing region at a 10.75% CAGR through 2030. China’s publicly disclosed USD 314 billion defense budget in 2024 has triggered acquisition races across Japan, India, South Korea, and Australia, each emphasizing indigenous long-range strike projects. Japan’s 21% budget surge funds missile-training facilities on Pacific islands, while India’s scramjet ground tests showcase self-reliance in hypersonic propulsion.[4]Airforce Technology, “India Conducts First Scramjet Ground Test,” airforce-technology.com Regional partnerships—such as the US-Japan Glide Phase Interceptor—further accelerate technology transfer and joint production, enlarging the collective air-to-surface missiles market size for local suppliers.

Europe experiences steady, procurement-driven growth as NATO members replenish stockpiles and invest in deep-strike capabilities. MBDA’s EUR 2.4 billion (USD 2.82 billion) capacity expansion and France’s EUR 600 million (USD 705.38 million) air-defense missile contracts confirm political willingness to finance indigenous solutions. Collaborative frameworks like the EU’s joint Mistral-3 procurement illustrate a shift toward pooled buying power, stabilizing order books while harmonizing requirements across the continent. These dynamics collectively sustain a resilient European contribution to the global air-to-surface missiles market.

Competitive Landscape

Industry concentration remains high as the prime contractors dominate end-to-end missile design, propulsion, guidance, and integration. Vertical integration allows them to safeguard intellectual property and mitigate supplier disruptions, yet it raises entry barriers for innovative startups. Regulatory bodies are increasingly alert to consolidation risks; the FTC’s intervention against Lockheed Martin’s attempted Aerojet Rocketdyne purchase preserved propulsion competition and signaled stricter scrutiny for future deals.

Technology leadership has become the chief differentiator. MBDA’s Orchestrike AI for SPEAR cruise missiles exemplifies how embedded autonomy can extend weapon lethality without compromising human agency. Northrop Grumman and GE Aerospace focus on dual-mode ramjets to unlock mass-producible hypersonic missiles, while Lockheed Martin leverages model-based engineering to halve integration timelines across multiple airframes.

Cost-effective precision has emerged as an exploitable white space: firms such as L3Harris and Mach Industries market modular mini-cruise missiles priced below USD 0.3 million, targeting customers who cannot afford high-end hypersonic rounds. At the same time, additive-manufacturing pioneers are courting primes with rapid prototyping capabilities that compress design-to-flight schedules. These trends ensure that, despite oligopolistic structures, innovation cycles within the air-to-surface missiles market remain vigorous.

Air-to-Surface Missiles Industry Leaders

Lockheed Martin Corporation

RTX Corporation

MBDA

Rafael Advanced Defense Systems Ltd.

The Boeing Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Lockheed Martin secured a USD 3.2-billion contract to manufacture JASSM and LRASM missiles for US allies. The Lot 22 procurement includes deliveries to NATO members Finland, Poland, the Netherlands, and Japan, strengthening their defense capabilities against evolving global security challenges.

- July 2024: Israel Aerospace Industries unveiled its new Wind Demon air-surface cruise missile. The company developed this cost-efficient system capable of accurately striking targets beyond 200 kilometers.

Global Air-to-Surface Missiles Market Report Scope

| Combat Aircraft |

| Bomber Aircraft |

| Rotary-Wing Aircraft |

| Unmanned Aerial Vehicles (UAVs) |

| Short-Range |

| Medium-Range |

| Long-Range |

| Solid Rocket |

| Liquid Fuel |

| Ramjet/Scramjet |

| Turbojet |

| Hybrid |

| Inertial and GPS |

| Laser Homing |

| Infrared Imaging |

| Active Radar |

| Multi-Mode |

| Subsonic |

| Supersonic |

| Hypersonic |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Launch Platform | Combat Aircraft | ||

| Bomber Aircraft | |||

| Rotary-Wing Aircraft | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Range | Short-Range | ||

| Medium-Range | |||

| Long-Range | |||

| By Propulsion Type | Solid Rocket | ||

| Liquid Fuel | |||

| Ramjet/Scramjet | |||

| Turbojet | |||

| Hybrid | |||

| By Guidance | Inertial and GPS | ||

| Laser Homing | |||

| Infrared Imaging | |||

| Active Radar | |||

| Multi-Mode | |||

| By Speed Class | Subsonic | ||

| Supersonic | |||

| Hypersonic | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current global value of the air-to-surface missiles market?

The air-to-air missiles market stands at USD 5.98 billion in 2025 and is projected to hit USD 9.01 billion by 2030 at an 8.54% CAGR.

Which launch platform segment is expanding the quickest?

Missiles launched from UAVs are forecasted to grow at an 11.25% CAGR through 2030.

Why are long-range missiles gaining traction?

Advanced air defenses are pushing strike requirements beyond 400 km, driving a 10.42% CAGR in the long-range segment.

What propulsion technology underpins hypersonic weapons?

Dual-mode ramjet and scramjet engines enable sustained flight above Mach 5 while remaining producible at scale.

Which guidance technologies best resist electronic-warfare jamming?

Multi-mode seekers that fuse radar, imaging infrared, and laser inputs maintain accuracy even when GPS or datalinks are disrupted.

Which region shows the highest growth potential?

Asia-Pacific is projected to lead with a 10.75% CAGR as regional defense budgets prioritize indigenous long-range strike capabilities.

Page last updated on: