Market Overview

| Study Period | 2019 - 2031 |

|---|---|

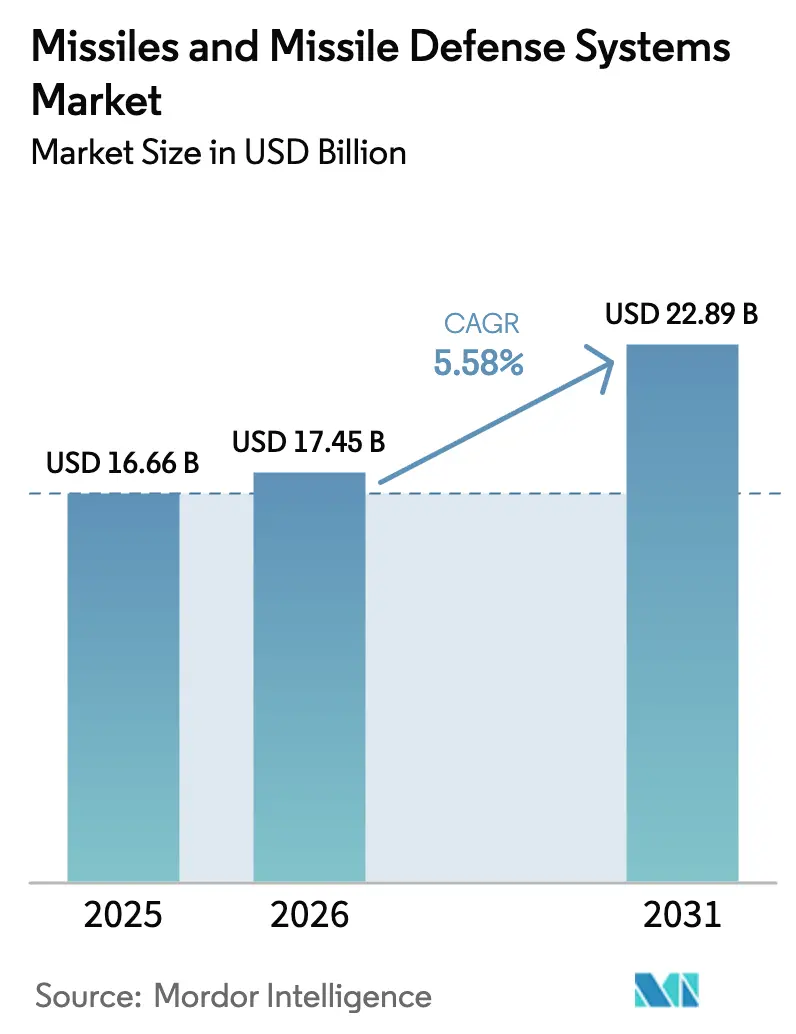

| Market Size (2026) | USD 17.45 Billion |

| Market Size (2031) | USD 22.89 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Missiles And Missile Defense Systems Market Analysis by Mordor Intelligence

The missiles and missile defense systems market size is expected to grow from USD 16.66 billion in 2025 to USD 17.45 billion in 2026 and is forecasted to reach USD 22.89 billion by 2031 at a 5.58% CAGR over 2026-2031. This growth is supported by the rising procurement of short-range interceptors for active conflict zones, expanding orders for intermediate-range platforms that deter stand-off strikes, and the rapid adoption of space-based sensor layers that enhance tracking fidelity. [1]Source: U.S. Department of Defense, “Fiscal Year 2025 Defense Budget Request,” DEFENSE.GOV Nations are transitioning from episodic purchases to multi-year framework agreements that ensure propellant and semiconductor supply, a shift that lowers unit costs but concentrates risk among a few tier-1 vendors. Hypersonic threat proliferation is steering research funding toward kinetic-kill vehicles capable of engaging Mach 15 targets, while artificial-intelligence guidance upgrades are making export-controlled systems more attractive to treaty allies. Competitive pressure is intensifying as vertically integrated Asian contractors bundle missiles with radar and command software, forcing Western primes to safeguard gallium-nitride supply through upstream investments.

Key Report Takeaways

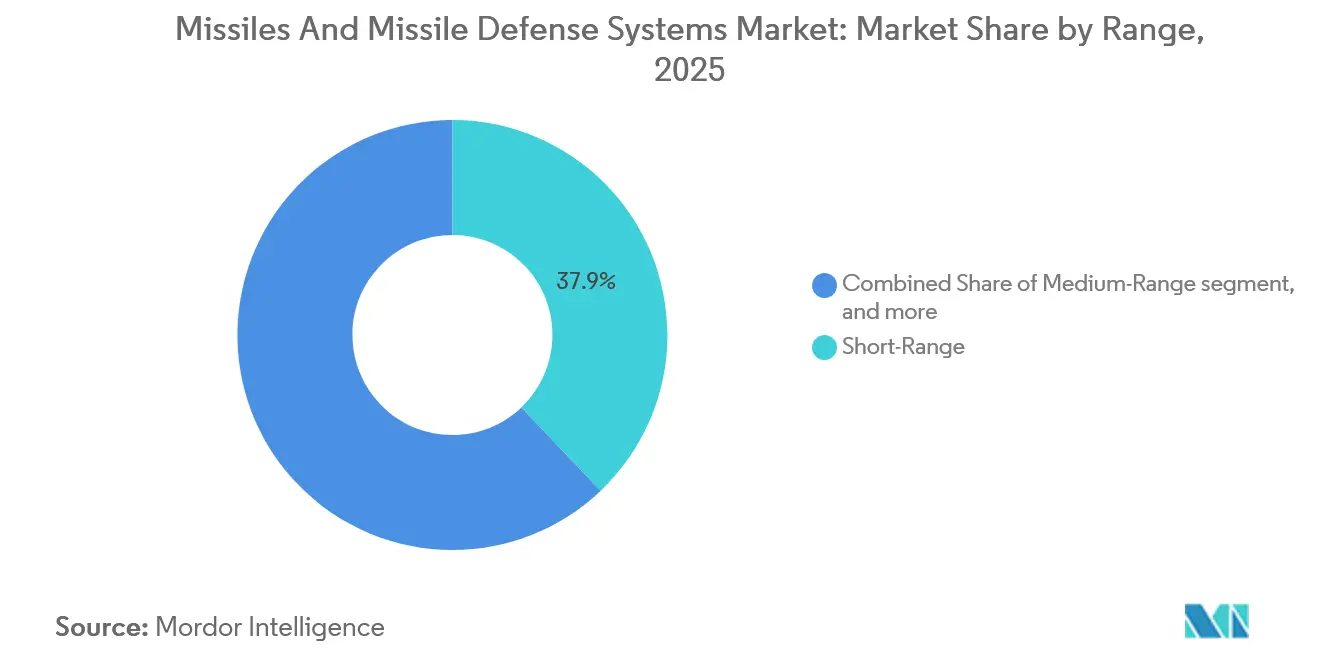

- By range, short-range systems held 37.89% of the missiles and missile defense systems market share in 2025, while intermediate-range platforms are forecast to expand at a 6.25% CAGR to 2031.

- By system type, missile-defense interceptors accounted for 51.45% of the missiles and missile defense systems market size in 2025, and anti-aircraft missiles are expected to track the fastest growth at a 5.89% CAGR through 2031.

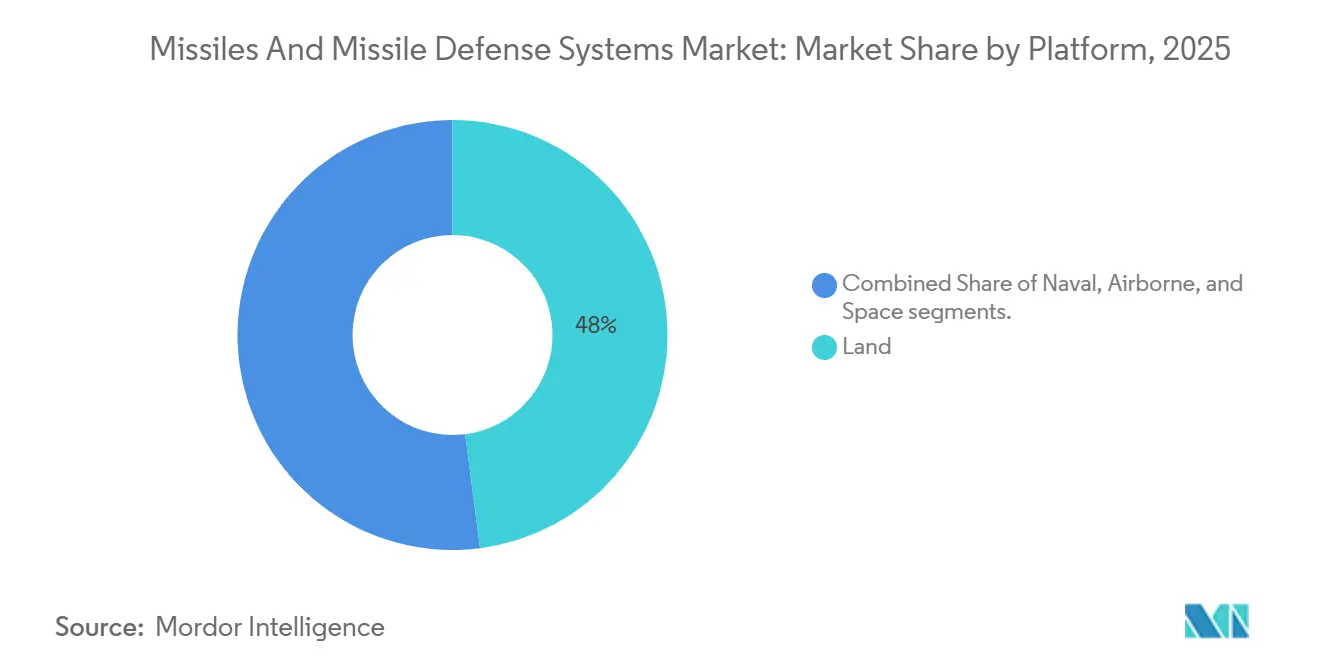

- By platform, land-based launchers captured 47.95% of the revenue in 2025; space-based assets are growing at an 8.35% CAGR.

- By end user, the army led with 41.20% of spending in 2025, while the navy logged a 6.45% CAGR through 2031.

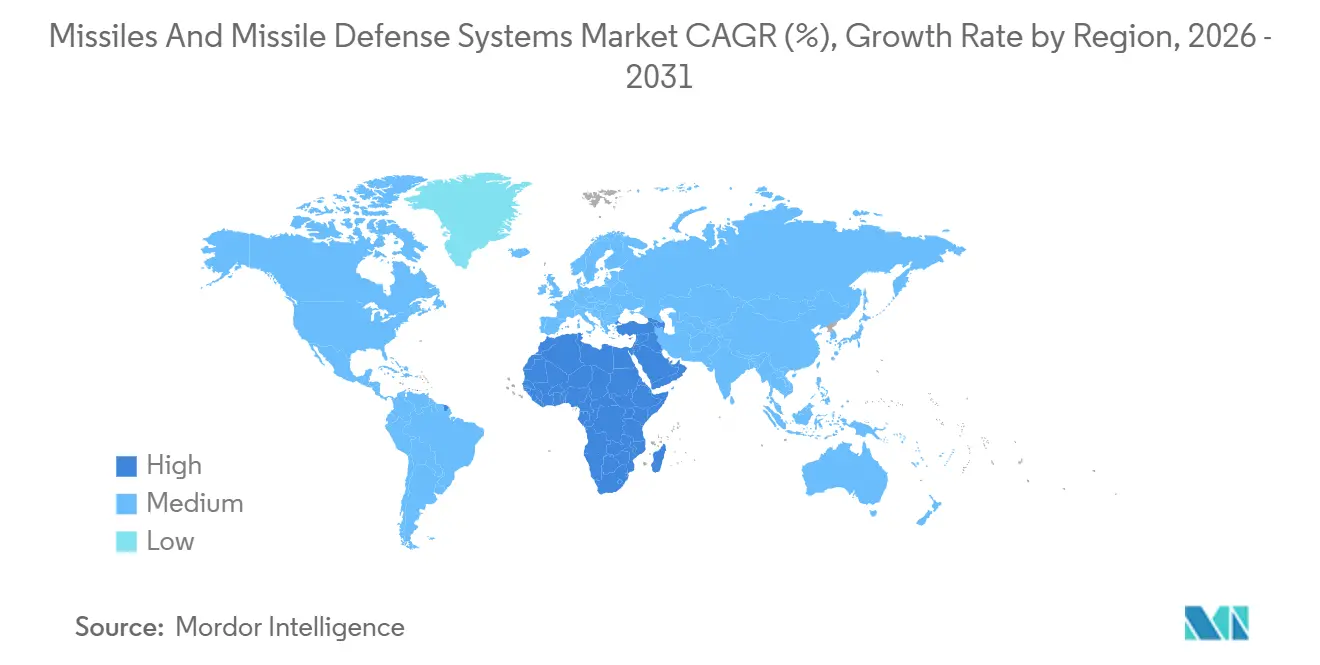

- By geography, North America accounted for 35.65% of the revenue in 2025, while the Middle East and Africa are expected to grow at the fastest rate, with a 6.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Missiles And Missile Defense Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating great-power tensions and sustained defense-budget growth | +1.2% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Global shift toward layered Integrated Air and Missile Defense procurements | +0.9% | North America, Europe, Middle East, Asia-Pacific | Medium term (2–4 years) |

| Rapid emergence of hypersonic threats accelerating interceptor and sensor demand | +1.1% | North America, Russia, China, allied nations | Medium term (2–4 years) |

| AI-enabled guidance, C2 and sensor-fusion boosting accuracy and exportability | +0.8% | North America, Europe, Israel | Short term (≤ 2 years) |

| National strategic-stockpile programs securing long-term energetics offtake | +0.6% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Proliferated space-based tracking constellations lowering entry barriers | +0.7% | United States, Europe, emerging space powers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating Great-Power Tensions and Sustained Defense-Budget Growth

Defense budgets continue to rise, led by a US request of USD 849.8 billion for fiscal 2025 that earmarks USD 33.7 billion for missile defense programs. China’s official allocation rose to USD 236 billion in 2025, while independent estimates suggest real spending is significantly higher. [2]Source: Stockholm International Peace Research Institute, “Military Expenditure Database 2025,” SIPRI.ORG Middle-power states respond by accelerating purchases, as seen in Poland’s USD 3.5 billion Javelin order, which locked in semiconductor supply and reduced unit costs. Multi-year agreements now dominate procurement, smoothing production lines for energetics and launch vehicles. This steady funding cycle supports the missiles and missile defense systems market by guaranteeing volume for prime contractors and their upstream suppliers.

Global Shift Toward Layered Integrated Air and Missile Defense Procurements

Nations are integrating radars, satellites, and airborne sensors into a single command network that cues any interceptor from any sensor. NATO’s 2024 Brussels communiqué mandates the implementation of Link 16 and Cooperative Engagement Capability by 2028. [3]Source: NATO, “Brussels Summit Communiqué 2024,” NATO.INTGermany’s IRIS-T SLM and Spain’s Patriot PAC-3 MSE buys include software radios that enable real-time track handoff. The resulting demand boost extends beyond missiles to open-architecture launchers and battle-management software vendors, broadening revenue opportunities inside the missiles and missile defense systems market.

Rapid Emergence of Hypersonic Threats Accelerating Interceptor and Sensor Demand

Russia’s Avangard and China’s DF-ZF glide vehicles highlight the need for interceptors that maneuver at high-G loads. The US Missile Defense Agency budgeted USD 4.7 billion for the Glide Phase Interceptor, aiming for fielding by 2029. Japan’s USD 1.2 billion contract with Mitsubishi Heavy Industries to create a hypersonic Chu-SAM variant shows allied urgency. Heat-resistant composites and divert-control systems become bottlenecks, concentrating market power in firms with wind tunnels and ceramics expertise. These challenges elevate R&D spending, yet they also raise switching costs that favor incumbents in the missiles and missile defense systems market.

AI-Enabled Guidance, C2 and Sensor-Fusion Boosting Accuracy and Exportability

Lockheed Martin’s Long Range Anti-Ship Missile integrates a neural network that classifies maritime targets when GPS is jammed. Israel’s Iron Dome reduced intercept cost by 18% after adding machine-learning allocation logic. The US State Department has green-lit Patriot AI upgrades for Poland, noting that adaptive algorithms are complex to reverse-engineer, which eases export approvals. As autonomy advances, nations seek systems that maximize hit probability at a lower cost per shot, thereby reinforcing demand in the missiles and missile defense systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extremely high R&D and unit-procurement costs | -0.7% | Global, smaller defense budgets | Long term (≥ 4 years) |

| Tightening export-control and compliance regimes | -0.5% | Global, acute for non-aligned nations | Medium term (2–4 years) |

| Heat-resistant material and GaN TR-module supply-chain bottlenecks | -0.6% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Rising cyber-security and system-integration risk profile | -0.4% | NATO and allied nations | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Extremely High R&D and Unit-Procurement Costs

Next-generation interceptors carry price tags many buyers cannot absorb. The Glide Phase Interceptor program totals USD 18.9 billion, with a projected unit cost of near USD 45 million, which dwarfs the USD 3 million price of the PAC-3 MSE. European Sky Shield pools 15 nations to gain IRIS-T volume discounts, but collective buying slows schedules. As costs rise, some governments trim orders, eroding economies of scale and restraining growth in the missiles and missile defense systems market.

Tightening Export-Control and Compliance Regimes

ITAR, MTCR, and the EU Dual-Use Regulation now cover machine-learning guidance software, which adds paperwork and increases the risk of rejection. A 2024 ITAR denial blocked Javelin sales to a Southeast Asian state, steering the buyer toward Turkish alternatives. The result is a bifurcated supply chain, where Western manufacturers serve treaty allies. At the same time, Russia, China, and Turkey fill gaps elsewhere, limiting the total accessible revenue for some vendors in the missiles and missile defense systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Range: Tactical Dominance Meets Strategic Hedging

Short-range platforms generated 37.89% of 2025 revenue, illustrating the tactical urgency that keeps production lines active for low-cost interceptors. The missiles and missile defense systems market size for short-range solutions is expanding as armies counter drones and loitering munitions that evade heavy radars. Mobile batteries, such as the IRIS-T SLM, achieved a 95% intercept success rate in 2024 operations, strengthening buyer confidence. Volume demand supports economies of scale that hold unit prices steady despite gallium-nitride shortages. Suppliers leverage standard launch canisters across ranges to streamline logistics.

Intermediate-range systems are forecast to rise at a 6.25% CAGR through 2031, reflecting strategic hedging against regional stand-off weapons. Japan’s 2025 Tomahawk purchase demonstrates how democracies can expand their reach without violating nuclear treaties. Although lower in volume, these missiles generate premium margins, thereby lifting the overall market for missiles and missile defense systems. Manufacturers manage the diverse portfolio by sharing seeker electronics and propulsion sub-assemblies between ranges, smoothing production planning across cycles.

By Missile and Defense System Type: Interceptors Lead, Anti-Aircraft Gains

Interceptor programs brought 51.45% of 2025 revenue, making them the cornerstone of the missiles and missile defense systems market share. THAAD, Arrow 3, and Ground-based Midcourse Defense fill the exo-atmospheric niche that demands high-priced kinetic kill vehicles. Open-architecture launchers now accept multiple interceptor types, enabling forces to tailor loadouts to specific scenarios and extend platform life.

Anti-aircraft missiles are projected to expand at a rate of 5.89% through 2031, as low-altitude cruise missiles challenge traditional radar defenses. NASAMS sales to Ukraine proved the value of mobile command-and-control kits that network with legacy radars. Suppliers retrofit seekers with software upgrades instead of hardware swaps, cutting integration time. This agility widens adoption across smaller militaries and underscores the diversity within the missiles and missile defense systems market.

By Platform: Land Anchors, Space Accelerates

Land-based launchers accounted for 47.95% of 2025 revenue, driven by vehicles that can quickly reposition when sensors detect threat vectors. Crew training pipelines already exist, lowering entry barriers for new batteries. Standardized rail launchers accept guided rockets, cruise missiles, and interceptors, maximizing tactical flexibility.

Space-based assets show the fastest momentum with an 8.35% CAGR. The Tracking Layer’s 126 satellites incur an incremental cost of USD 15 million each, a fraction of the cost of past geostationary platforms. Commercial data-as-a-service models enable middle-income states to purchase cueing feeds without sovereign launch programs, thereby broadening the customer reach for the missiles and missile defense systems industry. Ground contractors that translate raw infrared data into fire-control tracks are capturing value once reserved for satellite builders.

By End-User: Army Leads, Navy Climbs

Army formations accounted for 41.20% of 2025 spending, emphasizing forward-deployed units that require immediate protection against rockets and drones. The IAMD Battle Command System integrates Patriot, THAAD, and future hypersonic interceptors into a single, unified console, thereby enhancing situational awareness for operators.

Naval budgets grow at a 6.45% CAGR because fleets integrate vertical-launch cells that fire both anti-ship and ballistic interceptors. Japan’s Maya-class destroyers demonstrate how a single hull can accommodate multiple mission sets, justifying investment despite limited ship numbers. Multimission capacity ensures steady demand for radar upgrades and software licenses, boosting recurring revenue within the missiles and missile defense systems market size calculation for naval platforms.

Geography Analysis

North America accounted for 35.65% of 2025 revenue, driven by the United States’ layered IAMD architecture and Canada’s NORAD modernization. The 2025 US Missile Defense Agency budget allocates USD 13.5 billion for next-generation interceptors, thereby preserving domestic production lines. Canada’s CAD 4.9 billion (USD 5.16 billion) North Warning System upgrade funds over-the-horizon radars that detect glide vehicles. Regional dominance stems from dense contractor ecosystems and test ranges, though future congressional caps could temper spending growth.

The Middle East and Africa region is the fastest-growing, with a 6.78% CAGR. Saudi Arabia fielded THAAD under a USD 15 billion program, adding exo-atmospheric coverage to Patriot batteries. The United Arab Emirates expanded PAC-3 deployments to protect infrastructure after drone raids. Israel sustains a layered defense by procuring Iron Dome, David’s Sling, and Arrow interceptors, creating a robust local supply chain that feeds regional exports. Emerging buyers in Sub-Saharan Africa signal new demand for locally assembled missiles.

Asia-Pacific pursues domestic development to ease ITAR constraints. Japan spends USD 5.1 billion on a hypersonic Chu-SAM interceptor. South Korea’s L-SAM intercepted a ballistic target at 50 km altitude and is moving to production in 2027. India flight-tested the Agni-Prime with a canister launch, enhancing its survivability. China’s DF-17 expansion prompts neighbors to accelerate the development of sensor networks, thereby enlarging the market for missiles and missile defense systems in the region.

Competitive Landscape

The missiles and missile defense systems market shows moderate concentration. Western primes race to debut glide-phase interceptors, while Asian contractors bundle missiles with radars to undercut prices. Lockheed Martin and Northrop Grumman push Mach 15 interceptors despite fixed-price contract risks that penalize overruns.

Vertical integration is a clear theme. RTX acquired a stake in Wolfspeed to secure gallium-nitride wafer capacity, thereby shortening radar lead times. European players joined forces when MBDA and Thales formed a EUR 450 million (USD 525.11 million) venture to craft a continental hypersonic interceptor, diversifying away from US supply chains.

Disruptors emerge from Turkey and South Korea. Roketsan’s SOM cruise missile secured a USD 450 million export sale due to flexible end-use terms that bypassed strict ITAR clauses. Hanwha Aerospace co-produces Chunmoo launchers in Poland, expanding its industrial reach into Europe. Smaller specialists in modular launchers, such as Kongsberg, capture value with open-architecture designs that reduce integration costs for multinational fleets.

Missiles And Missile Defense Systems Industry Leaders

Lockheed Martin Corporation

RTX Corporation

Northrop Grumman Corporation

The Boeing Company

MBDA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Israel Aerospace Industries (IAI) secured a USD 3.1 billion contract with Israel's Ministry of Defense to expand Germany's procurement of the Arrow 3 missile defense system, part of a broader USD 6.5 billion agreement. This deal underscores Israel's growing role in global defense exports and highlights Germany's strategic investment in advanced missile defense capabilities, reflecting broader trends in European defense modernization amid evolving geopolitical security challenges.

- December 2025: TAURUS Systems GmbH (TSG), a joint venture between MBDA and SAAB, secured a contract with the Federal Office of Bundeswehr Equipment, Information Technology and In-Service Support (BAAINBw) to establish a serial production line for the TAURUS NEO stand-off guided missile system. This development underscores Germany's strategic focus on enhancing its deep strike capabilities, with implications for defense readiness and potential ripple effects across the European defense manufacturing landscape.

Global Missiles And Missile Defense Systems Market Report Scope

The missiles are designed to deliver a large warhead over long distances with high precision. Modern cruise missiles can travel at high subsonic, supersonic, or hypersonic speeds. They are self-navigating and can fly on a non-ballistic, extremely low-altitude trajectory. A missile defense interceptor is a surface-to-air missile designed to intercept and destroy incoming hostile ballistic missiles. It achieves this by either a direct "hit-to-kill" impact (kinetic energy) or through an explosive warhead, which can be conventional, nuclear, chemical, or biological, to neutralize threats during their flight.

The missile and missile defense systems market is segmented by range, missile and defense system type, platform, end-user, and geography. By Range, the market is segmented into the short-range, medium-range, intermediate-range, and intercontinental. By missile and defense system type, the market is segmented into missile-defense interceptors, anti-aircraft missiles, anti-ship missiles, and anti-tank missiles. By platform, the market is segmented into land, naval, airborne, and space. By end-user, the market is segmented into the army, navy, and air force. The report also covers the market sizes and forecasts for the missiles and missile defense systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

By Range

| Short-Range (Less than 1 000 km) |

| Medium-Range (1 000–3 000 km) |

| Intermediate-Range (3 001–5 500 km) |

| Intercontinental (More than 5 500 km) |

By Missile and Defense System Type

| Missile-Defense Interceptors |

| Anti-Aircraft Missiles |

| Anti-Ship Missiles |

| Anti-Tank Missiles |

By Platform

| Land |

| Naval |

| Airborne |

| Space |

By End-User

| Army |

| Navy |

| Air Force |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Range | Short-Range (Less than 1 000 km) | ||

| Medium-Range (1 000–3 000 km) | |||

| Intermediate-Range (3 001–5 500 km) | |||

| Intercontinental (More than 5 500 km) | |||

| By Missile and Defense System Type | Missile-Defense Interceptors | ||

| Anti-Aircraft Missiles | |||

| Anti-Ship Missiles | |||

| Anti-Tank Missiles | |||

| By Platform | Land | ||

| Naval | |||

| Airborne | |||

| Space | |||

| By End-User | Army | ||

| Navy | |||

| Air Force | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the missiles and missile defense systems market in 2026?

The market stands at USD 17.45 billion in 2026 and is forecast to reach USD 22.89 billion by 2031.

Which range category leads current purchases?

Short-range systems hold 37.89% of 2025 revenue because armies need rapid-reaction interceptors for drones and cruise missiles.

What drives investment in space-based missile tracking?

Low-cost constellations such as the Tracking Layer cut per-satellite cost to about USD 15 million, giving middle-income states affordable access to global cueing data.

Why are interceptor programs so expensive?

Programs like the Glide Phase Interceptor involve new materials and guidance packages, pushing unit prices near USD 45 million and total R&D above USD 18 billion.

Which region is growing the fastest?

The Middle East and Africa record the highest CAGR at 6.78% as Gulf states add THAAD and Patriot batteries to counter regional ballistic threats.

How are export-control rules shaping competition?

Tightening ITAR and EU dual-use regulations divert some buyers toward suppliers in Turkey, South Korea, and China that impose fewer end-use restrictions.

Page last updated on: