Supplementary Cementitious Materials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

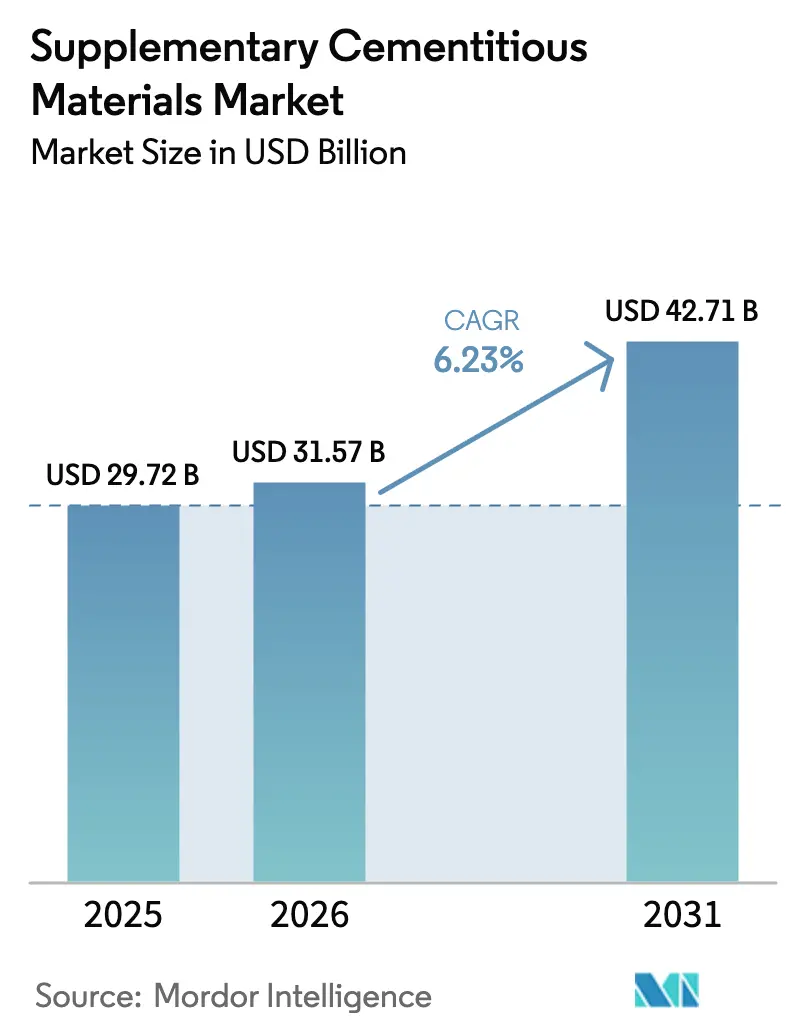

| Market Size (2026) | USD 31.57 Billion |

| Market Size (2031) | USD 42.71 Billion |

| Growth Rate (2026 - 2031) | 6.23% CAGR |

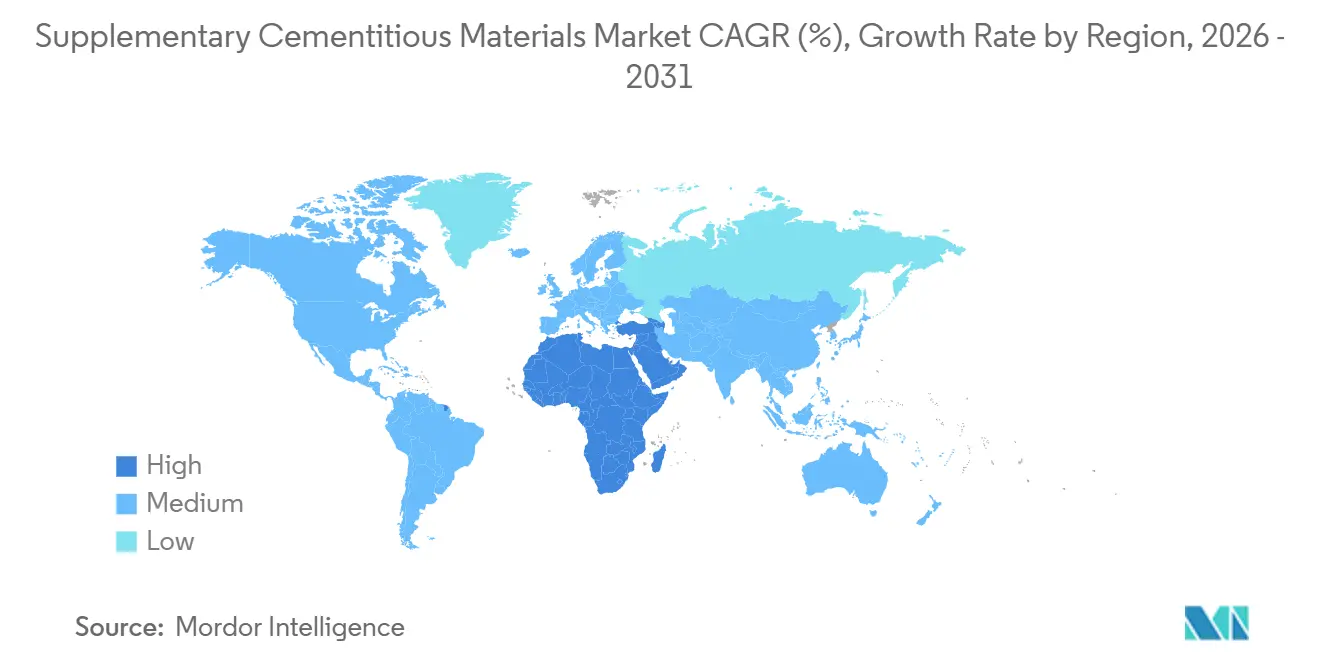

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Supplementary Cementitious Materials Market Analysis by Mordor Intelligence

The Supplementary Cementitious Materials Market size is projected to expand from USD 29.72 billion in 2025 and USD 31.57 billion in 2026 to USD 42.71 billion by 2031, registering a CAGR of 6.23% between 2026 to 2031. Carbon-pricing rules in the EU, California, and China continue to add USD 50-60 per tonne to clinker production, tilting procurement toward blends that replace at least 40% of the clinker fraction. Powder products still dominate but slurry formats are scaling fast in dense urban markets where silo space is at a premium. Fly ash remains the anchor raw material, yet diminishing coal capacity in North America and Europe is hastening a pivot to calcined-clay and limestone fillers. Public infrastructure programs in India, Saudi Arabia, and the United States are embedding low-carbon criteria into bid documents, while integrated cement majors pursue slag-grinding acquisitions to control feedstock and hedge against import volatility.

Key Report Takeaways

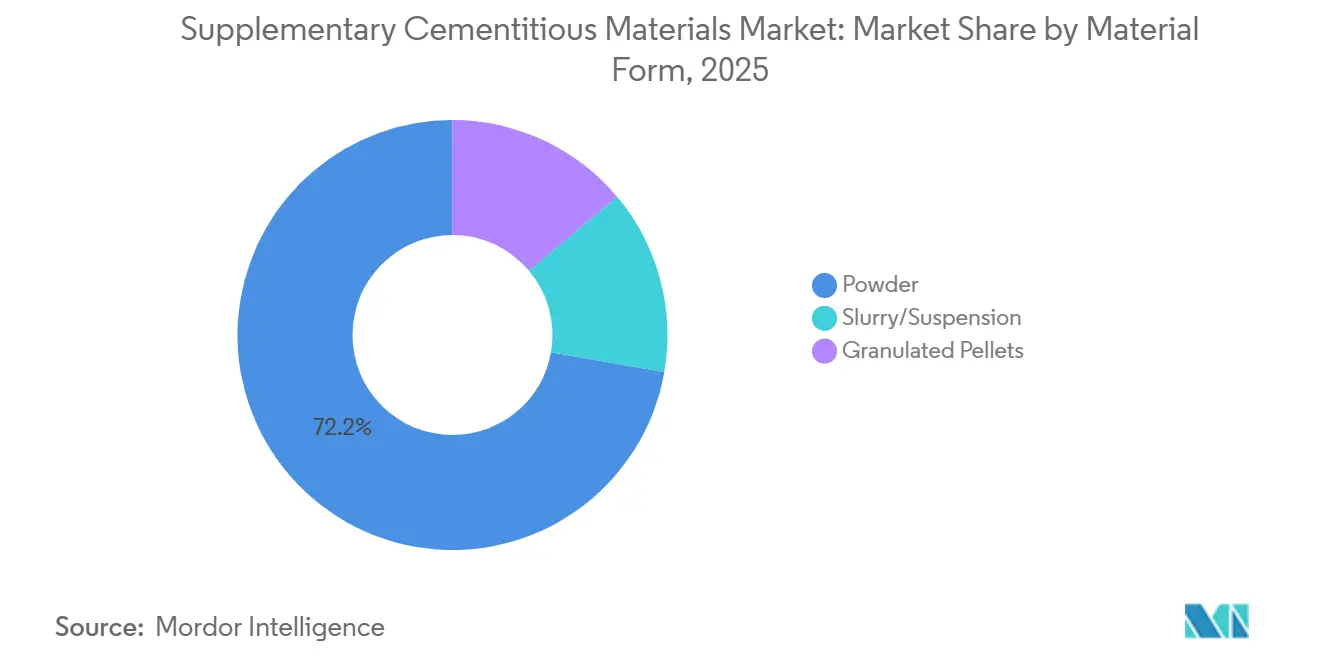

- By material form, powder commanded 72.25% of the supplementary cementitious materials market share in 2025, whereas slurry/suspension is projected to expand at a 6.56% CAGR through 2031.

- By SCM type, fly ash led with 42.21% of the supplementary cementitious materials market share in 2025, while calcined clay is forecast to register the fastest 6.92% CAGR to 2031.

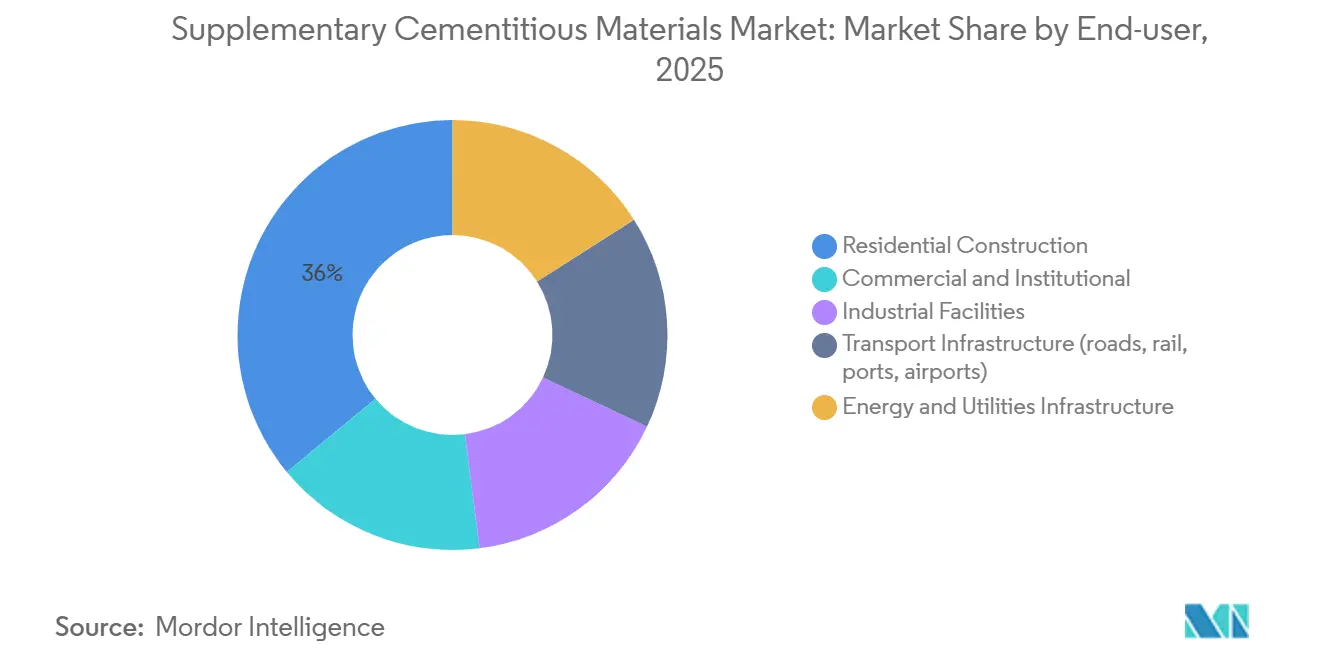

- By end user, residential construction accounted for 35.99% of 2025 volume, whereas transport infrastructure is advancing at a 6.83% CAGR through 2031.

- By geography, Asia-Pacific captured 48.89% of 2025 value, yet the Middle-East and Africa region is poised for the strongest 6.48% CAGR over through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Supplementary Cementitious Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter CO₂-emissions regulations and carbon-pricing schemes | +1.8% | Global, with EU, California, China leading; spillover to ASEAN, Middle-East | Medium term (2-4 years) |

| Rapid adoption of blended/green cements (e.g., PLC) | +1.5% | North America, Europe core; APAC and Latin America acceleration | Short term (≤ 2 years) |

| Government green-procurement incentives | +1.2% | North America (IRA, Buy Clean), Europe (EU Taxonomy), India (infrastructure mandates) | Medium term (2-4 years) |

| Commercial scale-up of calcined-clay and natural-pozzolan processing | +1.0% | Global, early gains in Europe, India, Brazil | Long term (≥ 4 years) |

| Performance-based specs accelerating alternative SCM acceptance | +0.7% | North America, Europe, APAC transport infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter CO₂-Emissions Regulations And Carbon-Pricing Schemes

The EU ETS cleared EUR 80 per allowance in 2026, inflating clinker costs by nearly EUR 60 per tonne and making 50% clinker-replacement blends price-competitive even without subsidies. California’s cap-and-trade and China’s national market impose similar penalties, prompting rapid commercialization of LC3 mixes that cut CO₂ intensity 40% relative to ordinary Portland formulations. The EU Carbon Border Adjustment Mechanism extends those costs to imports, compelling exporters in Turkey, Egypt, and Morocco to pivot to slag- and clay-rich blends. Parallel standards such as ISO 14067 and the draft ISO 19694 series institutionalize life-cycle carbon disclosures, forcing suppliers to audit SCM sourcing and transport footprints.

Rapid Adoption of Blended/Green Cements

Portland Limestone Cement (Type IL) has climbed above a 30% shipment share in North America since its 2018 approval, lowering clinker demand 10-15% with minimal strength trade-offs. India funded 12 LC3 demonstration plants totaling 5 million t of annual capacity by 2027, and global producers such as CEMEX now market Vertua concrete with up to 70% CO₂ reduction across 30 countries. Elevated SCM ratios slow early strength gain, so admixture suppliers have launched new accelerator chemistries that restore seven-day performance to OPC benchmarks, smoothing adoption in high-throughput infrastructure pours.

Government Green-Procurement Incentives

The U.S. Inflation Reduction Act allocates USD 4.5 billion for “Buy Clean,” awarding contracts only to mixes that beat sector average embodied-carbon baselines by 20%, effectively mandating 30-40% SCM replacement. Ireland capped embodied carbon in public buildings at 300 kg CO₂e / m³, while India’s highway ministry mandates 25% fly ash in concrete pavements built under Bharatmala. Colorado has shifted to durability-based specifications, encouraging innovative metakaolin blends that outperform conventional fly-ash mixes in freeze-thaw environments.

Commercial Scale-Up of Calcined-Clay and Natural-Pozzolan Processing

Flash-calcination plants in France and India are proving metakaolin economics at 250,000-500,000 t / yr capacity while operating 200 °C below clinker kilns, trimming energy needs by 20%. India’s UltraTech will open a 500,000-t facility in Rajasthan by Q3 2026, leveraging 18 billion t of kaolinitic clay reserves identified by CSIR. Regional cost competitiveness is strongest within 300 km of deposits, creating localized oligopolies and reinforcing the supplementary cementitious materials market’s emerging supply-chain geography.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High variability in SCM quality/specifications | -0.9% | Global, acute in ASEAN, Latin America, Africa | Short term (≤ 2 years) |

| Price volatility of imported slag and pozzolans | -0.7% | North America, Europe (slag importers); Middle-East (pozzolan importers) | Medium term (2-4 years) |

| Logistics and silo-capacity bottlenecks at ready-mix plants | -0.5% | Urban centers in North America, Europe, APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Variability In SCM Quality/Specifications

Calcium-oxide content in fly ash ranges from 1% to 35%, swinging setting times and heat of hydration far beyond what ASTM C618 covers, so ready-mix firms spend an extra USD 150-250 per truckload on batch-specific reactivity tests[1]ASTM International, “Standard Specification for Fly Ash and Raw or Calcined Natural Pozzolan for Use in Concrete (C618),” astm.org. Electric-arc-furnace slag, now 30% of global steel output, underperforms traditional blast-furnace slag yet sells under the same ASTM C989 grade, creating hidden variability. India’s 2024 IS 16714 introduced laser-diffraction and Blaine fineness rules, but enforcement outside Tier-1 cities is patchy, letting sub-spec material permeate rural projects. Color variability in metakaolin complicates architectural applications, throttling broader uptake despite strong mechanical benefits.

Price Volatility of Imported Slag and Pozzolans

Delivered slag costs in Europe jumped from EUR 100 to EUR 150 /t in Q1 2025 when Chinese mills cut exports, driving producers to costlier silica fume or lower-ratio blends. Pacific-to-U.S. freight doubled between 2023 and 2025, eroding North America’s slag cost advantage versus domestic fly ash. Turkish pozzolan flipped from 25% cheaper to more expensive within six months after Ankara added export taxes, illustrating foreign-exchange and policy risk[2]Turkish Statistical Institute, “Mineral Exports 2024-2025,” turkstat.gov.tr . Long-term offtake contracts hedge some volatility but require silo expansions that many metro plants cannot permit, complicating inventory planning in the supplementary cementitious materials market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Form: Slurry Gains in Space-Constrained Cities

Powder accounted for 72.25% of 2025 revenue within the supplementary cementitious materials market, reflecting decades-old silo infrastructure and operator familiarity. Yet slurry/suspension is scaling at a 6.56% CAGR because tanker-delivered mixes bypass silo bottlenecks in dense metros such as Mumbai and São Paulo. Continuous pours exceeding 500 m³ per batch for bridge decks or mat foundations now favor slurry supply chains that ensure uninterrupted flow and uniform reactivity. Pre-blended granulated materials are winning share in precast factories where dust abatement and dosing precision justify premiums. Adoption has triggered a standards gap; ASTM C1709 for slurry SCMs remains under committee review, leaving public owners hesitant to approve contracts without definitive viscosity and shelf-life limits. In tropical Southeast Asia, humidity drives caking and flow losses in powders, giving slurries an edge in workability and quality consistency, a trend likely to broaden as urbanization intensifies.

Powders will remain deeply entrenched in low-rise residential builds and rural projects where batching plants have enough silos for binary cement-fly-ash blends and truck volumes remain modest. Slurries are penetrating infrastructure programmes such as India’s Gati Shakti corridor and Saudi Arabia’s Vision 2030 rail expansions, where 1,000 m³ continuous placements are routine. Granulated pellets are carving out a foothold in architectural precast façades by slashing airborne particulates 90%, aligning with stricter occupational-health limits. Over the forecast horizon, slurry supply chains are projected to capture incremental share chiefly in high-throughput megacities, whereas powders will persist as the staple format across the broader supplementary cementitious materials industry.

By SCM Type: Calcined Clay Disrupts a Fly-Ash-Centric Mix

Fly ash controlled 42.21% of 2025 revenue in the supplementary cementitious materials market, but coal retirements in the United States and Europe are shrinking domestic output by 3 million t annually, elevating import prices 40-60% above local benchmarks. India still utilizes 80% of its 230 million t fly-ash yield thanks to coal baseload generation and mandatory-use rules, yet even their policy makers are championing LC3 to hedge future shortages. Calcined clay, expanding at a 6.92% CAGR, leverages abundant kaolinite reserves in India, Brazil, and West Africa and can cut CO₂ intensity 25-30% at equivalent 28-day strength. Slag cement claims roughly a quarter of marine and sulfate-exposure applications, prized for low permeability but increasingly supply-constrained as steelmaking transitions to electric arcs that generate 70% less slag per tonne. Silica fume stays niche—priced at USD 800 /t—and limestone filler under ASTM C595 Type IL is the fastest-growing commodity SCM, often blended at 10-15% with negligible performance trade-off.

Long term, calcined clay stands to erode fly-ash share most aggressively in North America and Europe where coal-fired output is sliding toward single-digit market shares. Slag will hold strong in specialty infrastructure yet face price spikes tied to metallics cycles. Emerging pozzolans like ground glass and rice-husk ash together represent less than 7% of value because consistency, logistics, and test-method gaps limit broader acceptance. Market leadership will likely gravitate to players with proprietary flash-calcination know-how and mine-to-mix vertical integration, giving them a durable cost edge and supply surety within the supplementary cementitious materials market.

By End-user: Infrastructure Specifications Pull the Mix Toward Ternary Blends

Residential construction absorbed 35.99% of 2025 volume thanks to cost-sensitive binary mixes that shave 8-12% off material bills without stretching curing schedules. Transport infrastructure is accelerating at a 6.83% CAGR as agencies like AASHTO now specify chloride permeability below 1,000 coulombs and freeze-thaw durability above 90%, thresholds hard to meet without ternary or quaternary blends rich in slag, silica fume, and metakaolin. India’s Bharatmala alone consumes 15 million t of fly ash per year, and Saudi megaprojects stipulate 50-60% SCM replacement to tame heat of hydration in massive viaduct pours. Commercial offices, data centers, and hospitals blend 30-50% SCM to hit LEED or BREEAM carbon limits, while industrial facilities hedge against sulfates with slag-heavy recipes.

Segmentation is blurring as modular prefabrication rises; precast yards increasingly adopt slurry SCM feeds and pelletized forms, enabling robotic batching lines that drive labor savings and consistent quality. Energy and utilities work—wind-turbine bases, hydro dams, transmission-tower footings—leans on silica fume additions that boost tensile capacity and resist cyclic weathering. Through 2031, infrastructure and utility applications are expected to be the prime demand flywheel, channeling public-finance mandates into deeper substitution and lifting the supplementary cementitious materials market size for high-reactivity inputs.

Geography Analysis

Asia-Pacific generated 48.89% of 2025 value for the supplementary cementitious materials market, anchored by China’s 2.4 billion t cement capacity and India’s USD 130 billion National Infrastructure Pipeline. Beijing’s 14th Five-Year Plan targets a 40% CO₂-intensity cut, but rising non-fossil power constrains fly-ash supply, nudging producers toward limestone fillers and imported Indonesian ash. India’s PM Gati Shakti master plan synchronizes rail, road, and port investments across 16 ministries, locking in steady demand for fly-ash-rich concrete; the highway ministry alone used 12 million t in 2024. ASEAN growth quality variance remains severe because Vietnam’s TCVN 10302 lacks strict enforcement, allowing sub-grade ash into rural jobsites.

In North America, the U.S. Federal Buy Clean program now ties contract awards to EPD metrics, effectively mandating 30-40% SCM content in federal concrete. Canada’s CSA A3000-2025 ushers in a “Low Carbon” cement class with 40-50% SCM, priming uptake in infrastructure funded by Ottawa’s Investing in Canada Plan. Mexico’s cement market is rising, yet limited fly-ash production forces 400,000 t-plus slag imports from East Asia for coastal builds.

The EU Taxonomy only labels cement green when CO₂ intensity dips below 0.498 t per tonne of binder, nudging mixes toward ≥50% SCM. Germany permits slag-limestone-silica ternary overlays provided 100-year durability models pass audit, and France channels green-bond proceeds into low-carbon public housing that favors LC3.

The Middle-East and Africa is the fastest-growing region at 6.48% CAGR. Saudi Arabia’s Vision 2030 pipeline and the UAE’s 350 kg CO₂e / m³ cap in structural mixes create structural pull. South Africa’s USD 100 billion plan strains local slag supply, forcing higher-cost imports from India. In Egypt, abundant limestone and the absence of carbon charges dampen SCM adoption, keeping penetration below 15%.

South America is led by Brazil, with slag and pozzolan blends already driving demand. Argentina and Chile lag because smaller steel sectors limit local slag, but natural-pozzolan deposits in the Andes are spurring pilot projects that could diversify feedstocks by decade’s end.

Competitive Landscape

The top 5 suppliers control an estimated 50% of global capacity, leaving moderate fragmentation in the supplementary cementitious materials market. Integrated majors such as Holcim, CEMEX, and HeidelbergMaterials are buying slag-grinding assets to secure feedstock; Holcim added 1.5 million t of capacity in Poland and Romania during 2024. ArcelorMittal’s construction-materials division monetized EUR 800 million in slag sales last year, demonstrating how steelmakers are exploiting circular-economy premiums. Pure-play firms like Ecocem scale by selling pre-blended ternary mixes to readymix firms that lack internal formulation expertise.

Technology alliances signal the next competitive turn. Holcim and Sublime Systems aim to pilot electrochemical cement that eliminates the kiln, pairing calcium hydroxide synthesized from brine with 60-70% SCM replacement for carbon-negative concrete. CEMEX installed a 100 t-per-day carbon-capture unit at Monterrey and now markets Vertua mixes with up to 70% emission cuts. Danish startup CemGreen is commercializing a 650 °C flash process that lowers calcination energy 25%, enabling economic metakaolin from low-grade clay.

Regulatory certification under EN 197-1 and ASTM C595 requires 12-18 months of durability and performance testing, a barrier that slows rapid newcomer entry but also assures quality. Incumbents with global terminal networks and long-term offtake contracts enjoy scale synergies that are hard to replicate quickly, yet niche innovators focusing on slurry logistics or localized clay calcination can still carve out high-margin beachheads.

Supplementary Cementitious Materials Industry Leaders

HOLCIM

Heidelberg Materials

CEMEX S.A.B. de C.V.

Charah Solutions, Inc.

ECO MATERIAL TECHNOLOGIES

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Boral Limited completed the development of a low-carbon concrete product incorporating locally sourced calcined clay. This achievement followed successful laboratory testing and large-scale field trials, positioning Boral Limited as the first Australian company to create a next-generation calcined clay concrete solution.

- May 2025: Heidelberg Materials, in partnership with CBI Ghana Ltd, a prominent cement manufacturer based in Tema, Ghana, completed the construction of the world's largest industrial-scale flash calciner for clay. The facility had an annual capacity exceeding 400,000 tons of calcined clay.

Global Supplementary Cementitious Materials Market Report Scope

Supplementary cementitious materials (SCM) are inorganic materials that contribute to the properties of a cementitious mixture through hydraulic or pozzolanic or both activities. Fly ash, slag cement, and silica fume are some of the extensively used SCMs.

The supplementary cementitious materials market is segmented by material form, SCM type, end-user, and geography. By material form, the market is segmented into powder, slurry/suspension, and granulated pellets. By SCM type, the market is segmented into fly ash, slag cement (ground-granulated blast-furnace slag), silica fume, calcined clay/metakaolin, limestone filler, and other SCM types. By end-user, the market is segmented into residential construction, commercial and institutional, industrial facilities, transport infrastructure (roads, rail, ports, airports), and energy and utilities infrastructure. The report also covers the market size and forecasts for supplementary cementitious materials in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Powder |

| Slurry/Suspension |

| Granulated Pellets |

| Fly Ash |

| Slag Cement (Ground-granulated Blast-Furnace Slag) |

| Silica Fume |

| Calcined Clay/Metakaolin |

| Limestone Filler |

| Other SCM Types |

| Residential Construction |

| Commercial and Institutional |

| Industrial Facilities |

| Transport Infrastructure (roads, rail, ports, airports) |

| Energy and Utilities Infrastructure |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Form | Powder | |

| Slurry/Suspension | ||

| Granulated Pellets | ||

| By SCM Type | Fly Ash | |

| Slag Cement (Ground-granulated Blast-Furnace Slag) | ||

| Silica Fume | ||

| Calcined Clay/Metakaolin | ||

| Limestone Filler | ||

| Other SCM Types | ||

| By End-user | Residential Construction | |

| Commercial and Institutional | ||

| Industrial Facilities | ||

| Transport Infrastructure (roads, rail, ports, airports) | ||

| Energy and Utilities Infrastructure | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What CAGR is projected for supplementary cementitious inputs between 2026 and 2031?

The supplementary cementitious materials market is forecast to grow at a 6.23% CAGR from USD 31.57 Billion in 2026 to USD 42.71 Billion in 2031.

Which raw material is gaining ground as fly-ash supply tightens?

Calcined clay is expanding at a 6.92% CAGR as LC3 technology scales and kaolinite deposits are commercialized.

Why are slurry formats becoming popular in megacities?

Slurry deliveries bypass silo limits at crowded batch plants, ensuring uninterrupted high-volume pours and improving quality control.

How do carbon-pricing schemes affect procurement decisions?

Allowance prices above EUR 80 per tonne make 50% clinker-replacement blends cost-competitive, accelerating blended-cement adoption in regulated markets.

Page last updated on: