China Cement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

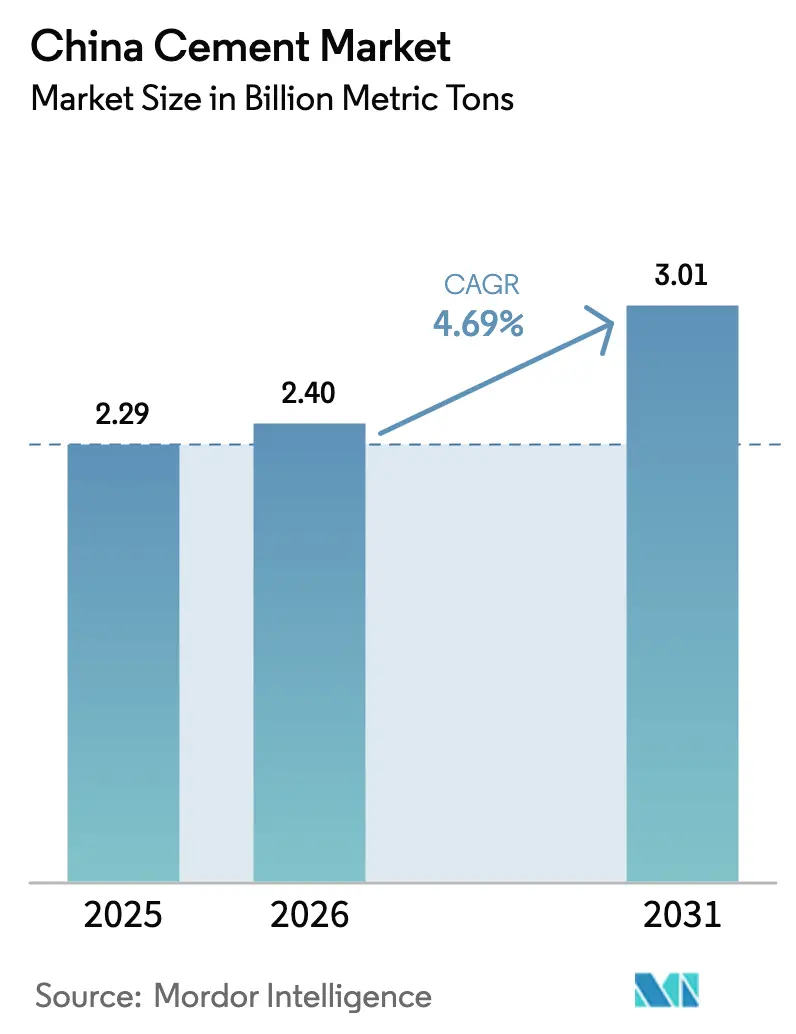

| Base Year Market Size (2025) | 2.29 Billion metric tons |

| Market Volume (2026) | 2.4 Billion metric tons |

| Market Volume (2031) | 3.01 Billion metric tons |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

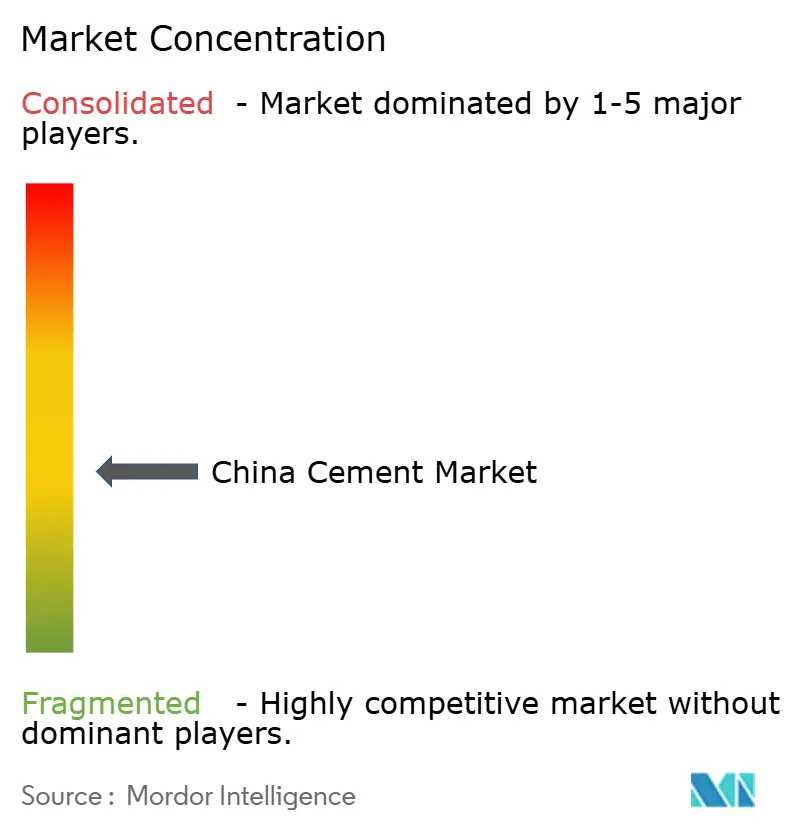

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Cement Market Analysis by Mordor Intelligence

China Cement Market size in 2026 is estimated at 2.4 billion metric tons, growing from 2025 value of 2.29 billion metric tons with 2031 projections showing 3.01 billion metric tons, growing at 4.69% CAGR over 2026-2031. This sustained growth signals a transition away from the boom-bust cycles that characterized earlier decades toward steadier expansion supported by targeted infrastructure spending, urbanization in emerging city tiers, and technology-enabled process upgrades. The Belt and Road Initiative keeps domestic plants running near optimal utilization by creating export outlets for clinker and finished cement, buffering demand against sporadic slowdowns in commercial real-estate activity. Western provinces absorb rising volumes because of transport corridors and energy projects, while eastern provinces maintain higher price realizations through stricter environmental enforcement and tighter market concentration. Rapid adoption of blended and low-clinker formulations further underpins the long-term resilience of the Chinese cement market.

Key Report Takeaways

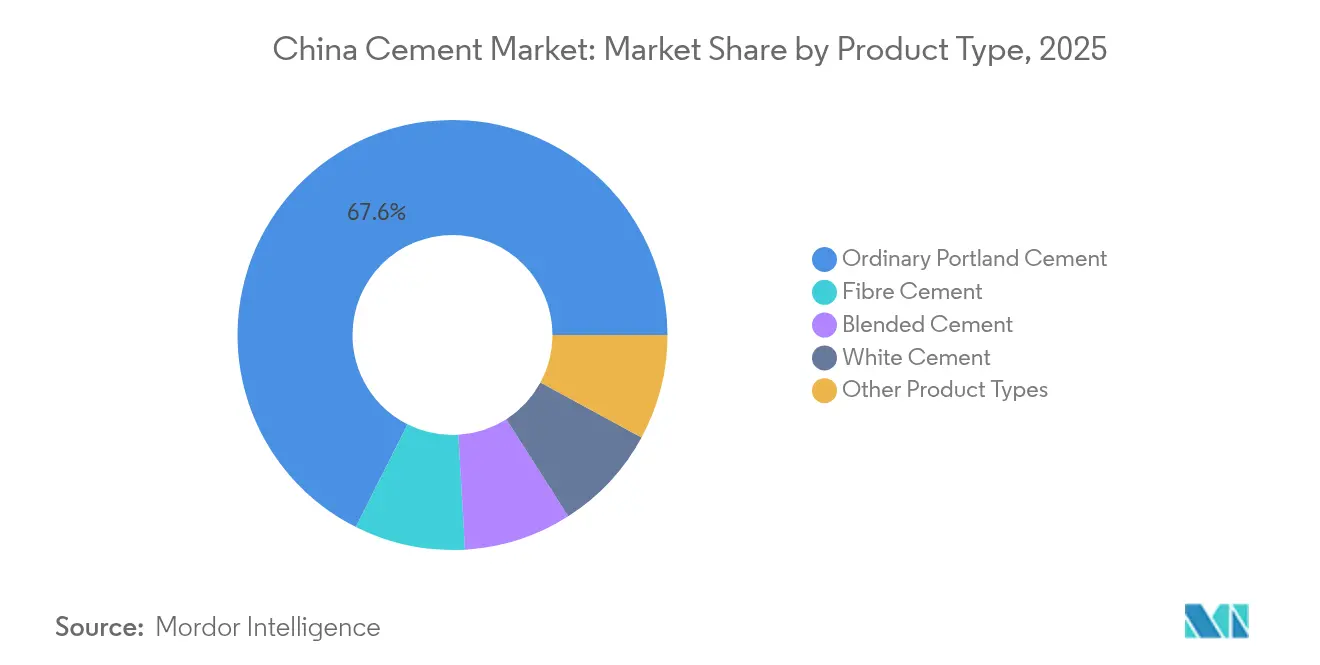

- By product type, Ordinary Portland Cement led with 67.58% of the China cement market share in 2025, while fiber Cement is projected to expand at 7.02% CAGR between 2026 and 2031.

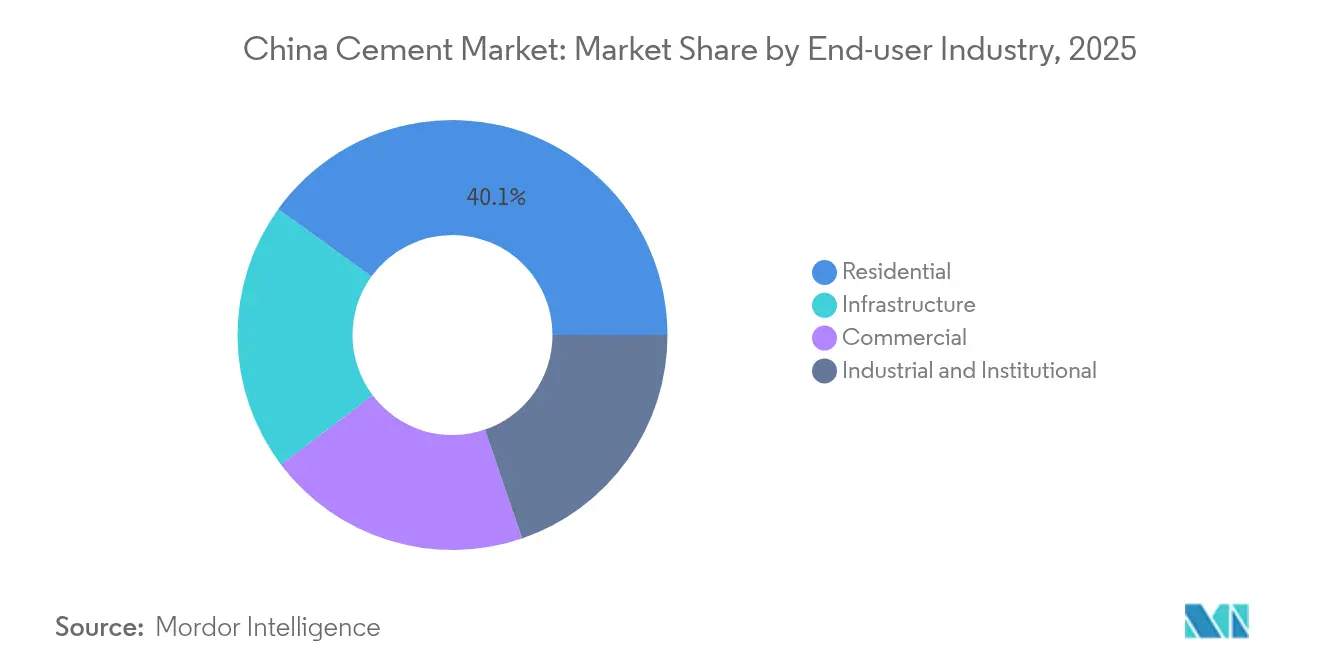

- By end-user industry, the Residential segment accounted for 40.05% share of the China cement market size in 2025, while Infrastructure demand is forecast to advance at a 6.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Cement Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanisation fuelling residential and commercial demand | +1.2% | National, with a concentration in Tier 2-3 cities | Medium term (2-4 years) |

| Infrastructure spending under 14th FYP and BRI pipeline | +1.8% | National, with emphasis on western regions | Long term (≥ 4 years) |

| Western-region development and urban cluster initiatives | +0.9% | Western provinces, spillover to central regions | Long term (≥ 4 years) |

| Adoption of low-clinker, blended cements for CO₂ compliance | +0.7% | National, with early adoption in eastern provinces | Medium term (2-4 years) |

| Provincial carbon-quota trading impact on project timing | +0.4% | National, with pilot regions leading implementation | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanisation Fuelling Residential and Commercial Demand

Urban residents exceeded 922 million in 2025, and the incremental population concentrates in mid-sized inland cities where land is affordable and government relocation incentives are generous. Consistent housing starts in these Tier 2 and Tier 3 locations stabilise bulk cement off-take even as top-tier markets pivot toward urban renewal. Local authorities package residential blocks with neighbourhood schools and clinics, which broadens commercial cement requirements in situ. Transport-oriented development around new metro lines further elevates ready-mix consumption. The residential segment’s 40.76% share of the China cement market confirms the centrality of urbanisation, although growth decelerates as demographic momentum slows.

Infrastructure Spending under the 14th FYP and Belt and Road Pipeline

Beijing approved 182 major projects valued at CNY 340 billion (USD 46.8 billion) in Q1 2025 alone, including high-speed rail extensions, pumped-storage hydropower, and data centres. Western routes such as the Sichuan–Tibet Railway require tunnelling through complex geology that consumes high-performance cement. Overseas Belt and Road contracts in Southeast Asia and Sub-Saharan Africa also absorb surplus clinker, lowering inventory risk for domestic kilns. The push toward a 50,000 km high-speed rail network by 2025 implies an average addition of 3,800 km each year, well above historic completion rates. Mega hydro schemes such as the Tibet cascade dam further amplify volume requirements.

Western-Region Development and Urban Cluster Initiatives

Since 2012, the government has channelled USD 550 billion into transport and utilities across the West, accelerating cement demand for highways, airports, and energy pipelines. The Dali–Ruili Railway’s 34.5 km Gaoligongshan tunnel sets a new benchmark for high-altitude concrete durability. Provinces such as Shaanxi and Gansu support urban clusters that link resource-rich plateaus with processing hubs. These corridors stimulate stable orders for ordinary cement and specialised sulphate-resistant grades used in arid environments. Government directives emphasise ecological protection, spurring demand for blended formulas with lower embodied carbon.

Adoption of Low-Clinker Blended Cements for CO₂ Compliance

China’s expansion of its national emissions trading system to cover the cement sector in 2025 raises the internalised cost of carbon. Producers respond by raising clinker substitution ratios using fly ash, slag and calcined clay. Limestone Calcined Clay Cement (LC3) lowers greenhouse-gas intensity by up to 40% without sacrificing strength. CBMI Construction commissioned the country’s first flash-calcination clay unit in January 2025. Early adopters in the east capture premium prices from green procurement policies.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter NOx/SO₂ emission caps and kiln retrofit costs | -0.8% | National, with stricter enforcement in eastern regions | Short term (≤ 2 years) |

| High volatility in thermal coal and petcoke prices | -0.6% | National, with a higher impact on energy-intensive regions | Short term (≤ 2 years) |

| Rising popularity of alternate building materials (CLT, steel-prefab) | -0.3% | Urban centers and high-end construction segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter NOx and SO₂ Emission Caps and Kiln Retrofit Costs

The Ministry of Ecology and Environment requires cement kilns in eastern provinces to achieve NOx levels under 50 mg/Nm³, forcing the rapid installation of selective catalytic reduction systems[1]Ministry of Ecology and Environment. "Guidelines for greenhouse gas emissions accounting and reporting for cement industry," www.mee.gov.cn. Retrofits are technically challenging because flue gases carry high dust loads that shorten catalyst life. Scientific case studies estimate capex of USD 30 million for a 5,000 tons per day line incorporating SCR, continuous monitors, and heat-recovery upgrades[2]Science Editors, “Potentials for DeNOx in Chinese Cement Industry with the Life Cycle Assessment Method,” Scientific.net, scientific.net. Smaller independent plants struggle to fund the overhaul, leading to phased shutdowns and industry consolidation. Near-term supply tightness occasionally supports prices, yet prolonged downtime can offset volume growth.

Rising Popularity of Alternative Building Materials

Cross-laminated timber and modular steel frames shorten build times, attracting some developers in coastal megacities. Premium office towers also employ composite structures that reduce concrete volumes. Although the substitution effect remains modest today, the visibility of low-carbon certification schemes adds momentum. Cement producers respond through value-added products such as ultra-high-performance concrete and carbon-captured blocks to protect their share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ordinary Dominance Meets Specialised Momentum

Ordinary Portland Cement (OPC) provided 67.58% of China's cement market share in 2025 because of its broad specification acceptance and mature supply chains. Infrastructure megaprojects continue to anchor bulk orders, keeping utilisation high at integrated works across Sichuan, Henan, and Anhui. OPC’s growth, however, moderates as regulatory pressure raises clinker costs and encourages blended alternatives.

Fiber Cement posts the fastest trajectory, accelerating at 7.02% CAGR through 2031. Builders favour fibre-reinforced sheets for façades, partition walls, and roof underlays because the material resists fire and moisture better than gypsum board. Provincial rebate programmes for non-combustible cladding after recent fire-safety audits further lift demand. Raw material suppliers such as New Element ramp up domestic capacity to meet the interior-decor and light-steel-villa segments.

By End-User Industry: Infrastructure Takes the Lead While Residential Holds Base

The Infrastructure segment commands the fastest expansion at 6.31% CAGR to 2031, aligned with Beijing’s funding of rail, water, and digital utility corridors. Each kilometre of high-speed rail requires 13,000 tons of cement for viaduct piers, ballastless track bedding, and station buildings. Mega hydropower projects in Yunnan and Tibet employ low-heat blended cement to mitigate crack risks in massive pours. Central planners prioritize airport revamps in Chengdu, Xi’an, and Urumqi, where passenger terminals adopt high-albedo white concrete to cut cooling loads.

Residential construction retains 40.05% of the Chinese cement market size in 2025 because urbanisation continues, albeit at a slower clip. Policy-linked lending supports affordable housing starts that use standard C30 OPC mixes. Rising refurbishment of ageing 1990s apartments sustains demand for bagged cement and dry-mix mortar. Developers in cost-sensitive inland cities adopt precast walls that still rely on cementitious grout and panel cores. Nonetheless, overall residential cement intensity edges down as apartment sizes shrink and steel-reinforced concrete cores replace thick load-bearing walls.

Geography Analysis

Eastern provinces such as Jiangsu, Zhejiang, and Guangdong contribute more than 35% of national shipments and receive the highest average ex-factory prices because of tight license quotas and strict emission enforcement. Producers here lead in the commercial deployment of LC3 and waste-heat-recovery power units, cutting operating costs and carbon liabilities. The region’s dense motorway network supports just-in-time deliveries to precast yards, further boosting premium cement uptake.

Central China, encompassing Henan, Hubei, and Hunan, acts as a logistics crossroad linking coastal markets to the west. Plants benefit from limestone abundance and access to both river and rail freight. Balanced demand from residential, commercial, and ongoing expressway widening projects smooths volume volatility. Central governments designate multiple high-speed rail maintenance depots in Wuhan and Zhengzhou, increasing steady consumption of specialty grouting cement.

Competitive Landscape

The Chinese cement industry is moderately fragmented and features national champions such as Anhui Conch, CNBM, and Huaxin alongside more than 100 provincial firms. Large groups integrate limestone quarries, clinker plants, grinding terminals, and ready-mix networks. Vertical control shields margins against ex-factory price swings and ensures kiln utilisation above 85%. Digitalisation differentiates leaders. Anhui Conch and Huawei jointly deploy machine-vision models that predict quality deviations two hours before lab confirmation. Environmental compliance reinforces consolidation. Smaller kilns unable to meet ultra-low-emission deadlines face shutdowns or forced sales, enabling larger groups to raise regional market share. In provinces where the top two producers exceed 65%, ex-factory prices stabilise more quickly after fuel shocks, demonstrating the profit benefit of scale.

China Cement Industry Leaders

-

Anhui Conch Cement Co., Ltd.

-

Beijing BBMG Group Co., Ltd.

-

China National Building Materials Group Co., Ltd. (CNBM)

-

China Resources Building Materials Technology Holdings Co., Ltd.

-

Huaxin Cement Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: West China Cement Limited acquired a 91% majority stake in Cimenterie de Lukala SA in the Democratic Republic of Congo, thus expanding its operations.

- December 2024: Holcim sold its 83% stake in Lafarge Africa to Huaxin Cement for USD 1 billion. The transaction includes four cement plants in Nigeria with combined capacity of 10.5 million tons per year.

China Cement Market Report Scope

Cement is a fine powdery substance composed primarily of limestone (calcium), sand or clay (silicon), bauxite (aluminum), and iron ore and may also include shells, chalk, marl, shale, clay, blast furnace slag, and slate. It is used for making concrete and mortar and has a variety of other applications in the construction sector. The cement market is segmented by product type, and end-use sector. By product type, the market is segmented into Ordinary Portland Cement, Blended Cement, White Cement, Fiber Cement, and Other Product Types. By end-use sector, the market is segmented into Residential, Commercial, Infrastructure, and Industrial & Institutional. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Ordinary Portland Cement |

| Blended Cement |

| White Cement |

| Fibre Cement |

| Other Product Types |

| Residential |

| Commercial |

| Infrastructure |

| Industrial and Institutional |

| By Product Type | Ordinary Portland Cement |

| Blended Cement | |

| White Cement | |

| Fibre Cement | |

| Other Product Types | |

| By End-user Industry | Residential |

| Commercial | |

| Infrastructure | |

| Industrial and Institutional |

Key Questions Answered in the Report

What is the current size of the China cement market?

The China cement market size stood at 2.4 billion metric tons in 2026.

Which segment is expanding the fastest?

Fiber Cement is growing at 7.02% CAGR through 2031, the quickest among product types.

How will the national ETS influence producers?

The ETS prices carbon, encouraging higher clinker substitution ratios and accelerating investment in low-clinker products.

Which region offers the highest growth potential?

Western China exhibits the strongest volumetric gains because of large-scale energy and transport infrastructure funded under long-term development programmes.

Page last updated on: