Europe Cement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

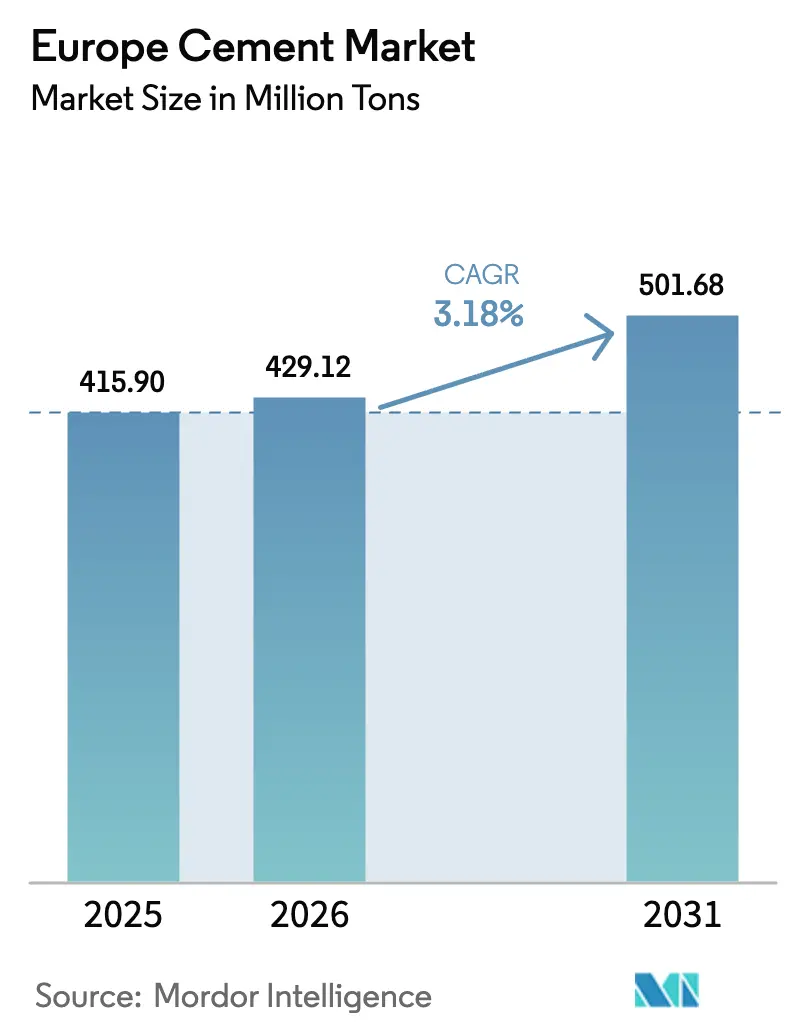

| Base Year Market Size (2025) | 415.90 Million tons |

| Market Volume (2026) | 429.12 Million tons |

| Market Volume (2031) | 501.68 Million tons |

| Growth Rate (2026 - 2031) | 3.18% CAGR |

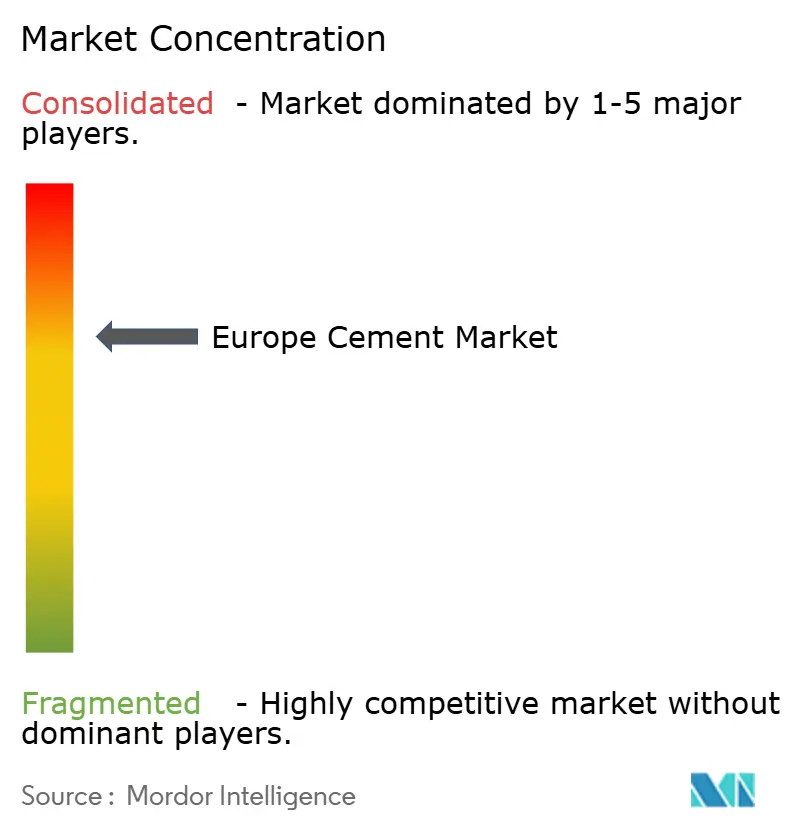

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Cement Market Analysis by Mordor Intelligence

The Europe Cement Market size is expected to grow from 415.90 million tons in 2025 to 429.12 million tons in 2026 and is forecast to reach 501.68 million tons by 2031 at 3.18% CAGR over 2026-2031. This steady growth trajectory reflects the sector’s ability to balance stringent decarbonization rules, volatile energy inputs, and a cyclical construction environment. Persistently high energy costs—still 21% above pre-crisis levels—continue to pressure margins, yet efficiency gains and fuel switching have already cut industry CO₂ output by 7% in 2023. Public-sector stimulus remains a defining demand catalyst: the EU Recovery & Resilience Facility (RRF) alone is expected to mobilize EUR 891.70 billion of investment through 2030, funneling resources toward transport corridors, renewable-energy plants, and building-renovation programs that are inherently cement-intensive.

Key Report Takeaways

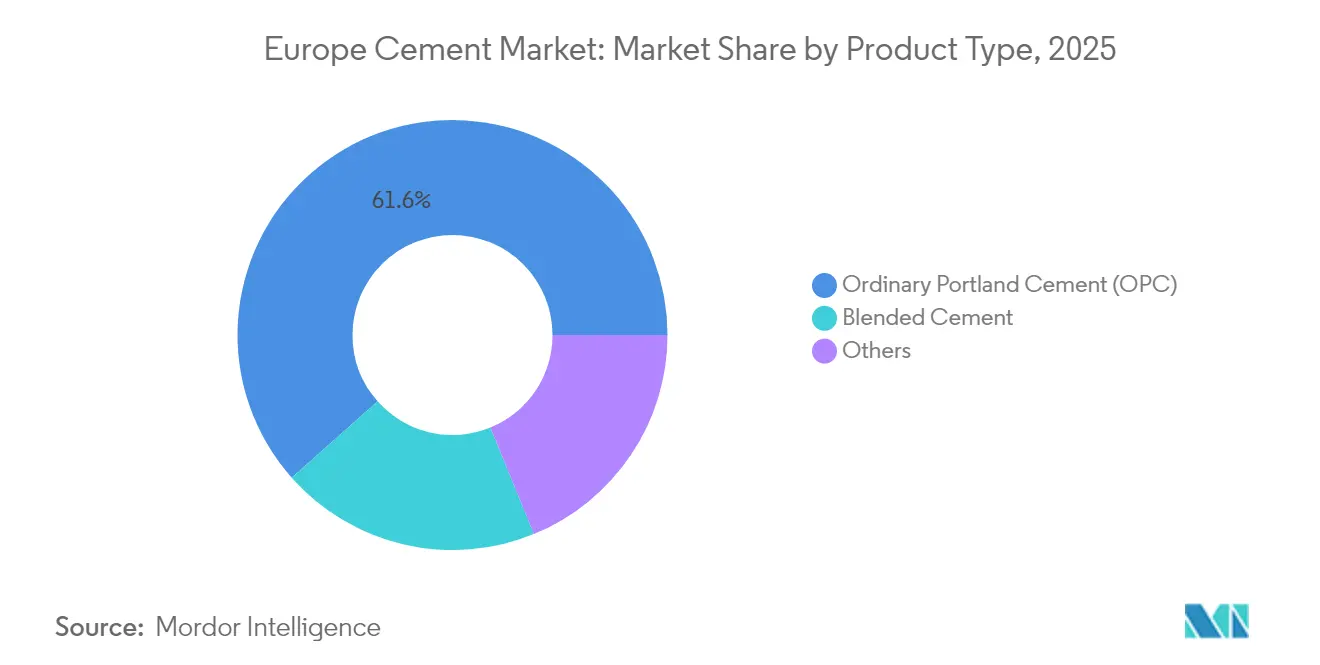

- By product type, Ordinary Portland Cement led with 61.55% of Europe cement market share in 2025; Blended Cement is projected to expand at a 4.62% CAGR through 2031.

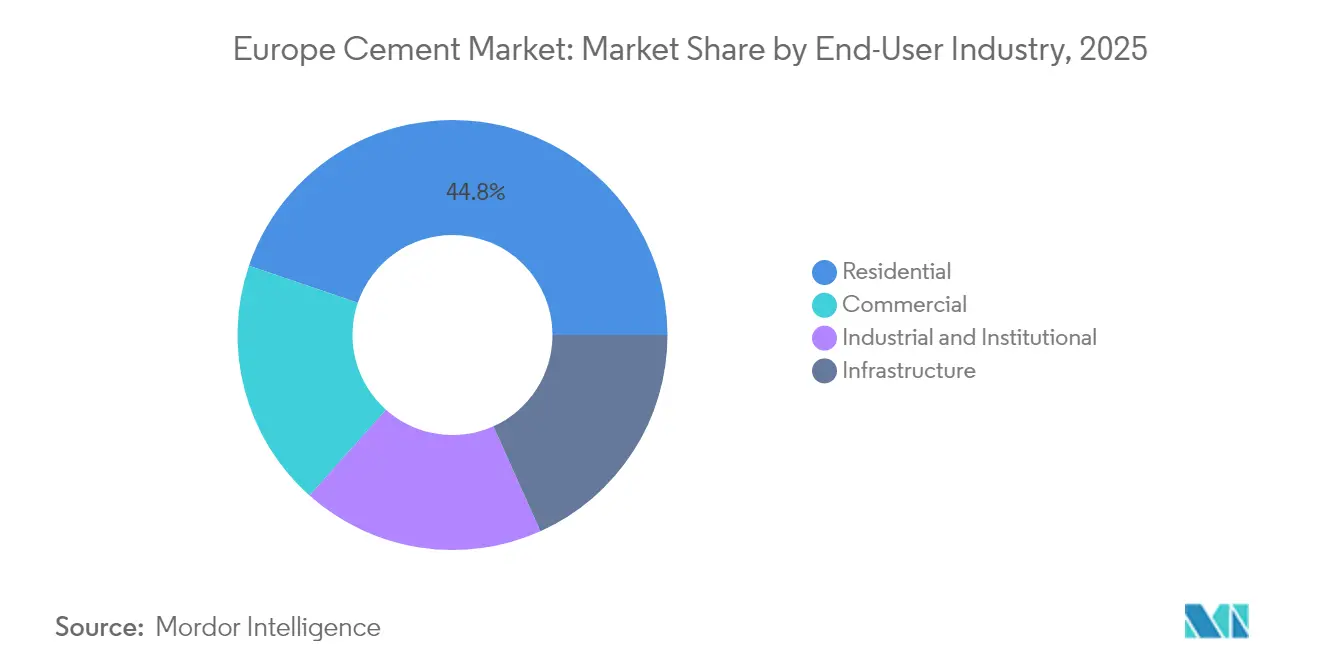

- By end-user industry, the residential segment accounted for 44.78% of the Europe cement market size in 2025, while commercial construction is set to rise at a 4.08% CAGR to 2031.

- By geography, Germany held 26.40% of the Europe cement market size in 2025; Spain is forecast to be the fastest-growing market at a 4.23% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Cement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in residential & renovation construction | +0.80% | Germany, France, Nordic Countries | Medium term (2-4 years) |

| EU Recovery & Resilience Facility infrastructure spending | +1.20% | Global, with a concentration in Spain, Italy | Medium term (2-4 years) |

| Expansion of green / low-carbon construction mandates | +0.60% | EU-wide, strongest in Germany, Netherlands | Long term (≥ 4 years) |

| Carbon Border Adjustment Mechanism (CBAM) demand pull for low-carbon cement | +0.40% | EU borders, affecting imports from Turkey, Russia | Short term (≤ 2 years) |

| Prefabricated modular housing boosting specialty cement demand | +0.30% | Nordic Countries, Germany, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Residential & Renovation Construction

New housing starts fell 6.20% in 2023 and a further 8.60% in 2024, but renovation already constitutes 30.30% of total construction spend, anchoring steady demand for the Europe cement market. Sweden posted the steepest downturn with a 37.2% decline in new builds, yet refurbishment remained stable as EU climate directives mandate energy-efficient retrofits on 35 million buildings by 2030. Renovation projects typically employ specialty mortars compatible with heritage facades and insulation overlays, creating premium niches for low-alkali and rapid-setting formulations. Because retrofit cycles extend beyond the housing boom-and-bust dynamic, producers enjoy smoother, less volatile order books. The segment’s structural resilience therefore offsets short-term weakness in greenfield construction and supports continued pricing discipline across the Europe cement market.

EU Recovery & Resilience Facility Infrastructure Spending

The RRF earmarks EUR 68 billion specifically for clean-tech and decarbonization projects that translate into concrete-intensive structures, from offshore-wind foundations to CO₂ transport pipelines. Spain’s EUR 240 billion pipeline exemplifies how member-state plans cascade into localized cement demand surges. Although disbursements reached only EUR 225 billion by 2024, the facility’s milestone-based payment design reduces the political risk of project cancellations and encourages timely execution. Cross-border freight and energy corridors boost clinker and finished-cement volumes in adjacent states such as Germany and Slovakia, magnifying the program’s regional impact. Consequently, the Europe cement market benefits from a multi-year backlog that cushions cyclicality and provides visibility for capacity-planning decisions.

Expansion of Green / Low-Carbon Construction Mandates

Brussels’ 90% economy-wide emissions-reduction target for 2040 effectively forces project owners to specify cements with lower embodied carbon. Certifications like BREEAM and DGNB now award extra credits for clinker-factor reductions, enabling producers such as Cementir to command premiums for FUTURECEM, which cuts CO₂ by 30% via limestone-calcined-clay substitution. This dual regulatory and market pull accelerates capital allocation toward calcined-clay kilns, SCM grinding capacity, and carbon-capture pilots. Over time, traditional OPC could face a margin squeeze as ETS allowance costs rise while low-carbon variants monetize eco-label advantages, reshaping competitive stakes inside the Europe cement market.

Prefabricated Modular Housing Boosting Specialty Cement Demand

Prefabrication can reduce cement tonnage in a given building by up to 60%, yet it simultaneously raises quality thresholds that favor high-value mixes with rapid strength gain and precise rheology[1]World Cement Association, “Opportunities and Challenges in Offsite & Modular Manufacturing,” worldcementassociation.org . Germany’s “Adaptive Modularized Constructions” program targets compressive strengths achieved five times faster than conventional slabs, requiring bespoke admixture packages. Labor shortages and tighter building envelopes are driving the increased adoption of modular construction in Mediterranean markets. For producers, the shift condenses shipments into large, centrally located precast plants, improving truck utilization and reducing on-site waiting penalties. The specialty niche, therefore, offsets the headline volume loss and adds margin depth to the Europe cement market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU ETS phase-IV emission caps | -1.10% | EU-wide, particularly Germany, Italy, Poland | Short term (≤ 2 years) |

| Volatile energy prices (natural gas & electricity) | -0.70% | Germany, Netherlands, energy-intensive regions | Medium term (2-4 years) |

| Shrinking fly-ash supply as coal plants close | -0.50% | Germany, Poland, Czech Republic, coal-dependent regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent EU ETS Phase-IV Emission Caps

Phase IV removes free allowances at an accelerated pace, compelling cement plants to purchase nearly 100% of their emissions rights by 2034. For a facility emitting 600 kg CO₂ per ton of clinker, the difference between grandfathered allocations and paid allowances can exceed EUR 15 per ton at current carbon prices. Operators with advanced carbon-capture pilots, such as Heidelberg’s GeZero site, gain a head start in cost avoidance, while laggards risk negative EBITDA. Already, German mills report capacity curtailments and potential closures, signaling a rationalization wave that could reshape the supply landscape over the next five years.

Volatile Energy Prices (Natural Gas & Electricity)

Industrial gas demand declined further in 2023, yet kiln-fuel costs remain significantly high, constituting a notable portion of cement's cash costs. Electricity prices follow a similarly volatile path, with the European Central Bank estimating that a permanent 10% increase could shave 1-2% from heavy-industry employment[2]European Central Bank, “How Enduring High Energy Prices Could Affect Jobs,” ecb.europa.eu . Faced with this environment, producers debate whether to lock into multi-year contracts that provide predictability but cap upside on future renewables penetration. Although solar surpassed coal in the EU’s generation mix for the first time in 2024, grid intermittency investments could paradoxically elevate power tariffs in the near term[3]Ember Climate, “European Electricity Review 2025,” ember-energy.org . Such uncertainties feed into cautious capital budgeting and may moderate clinker-capacity additions inside the Europe cement market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Blended Cement Gains Ground Despite OPC Dominance

OPC commanded 61.55% of Europe cement market share in 2025, reflecting its entrenched role in structural concrete and roadwork applications. Even so, Blended Cement is projected to compound at 4.62% annually to 2031, outpacing overall Europe cement market growth as climate criteria tighten and supplementary materials become more widely available. Producers are scaling calcined-clay facilities—just 14 plants operated in 2023, yet 79 are scheduled by 2035—to capitalize on clinker-factor reductions that deliver 30-40% CO₂ savings without sacrificing compressive strength. This shift also aligns with national low-carbon roadmaps that prioritize limestone-calcined-clay systems (LC3) and fly-ash hybrids for public procurement.

Investor interest mirrors the transition. Stockholm-based Cemvision raised EUR 10 million in 2024 to commercialize a net-zero formulation that achieves five-fold faster early strength, illustrating how venture capital is migrating from pure-tech to industrial-materials plays. As a result, the value pool is tilting toward premium-priced, performance-oriented cements that address both regulatory compliance and contractor efficiency. While OPC will retain a foundation share of the Europe cement market size for high-load and mass-concrete jobs, blended variants are poised to capture incremental volumes in urban development, precast, and refurbishment niches.

By End-User Industry: Commercial Outpaces Residential Growth

Residential applications generated 44.78% of the Europe cement market size in 2025, underpinned by a building-renovation wave that offers stable, year-round workloads. Commercial construction, however, is forecast to expand at a 4.08% CAGR as corporate tenants demand energy-positive offices and logistics developers race to satisfy e-commerce throughput. Investment into clean-tech manufacturing—battery gigafactories, electrolyzer plants, and advanced biofuels refineries—also feeds into the industrial sub-slice, creating a virtuous cycle of demand for high-strength floors, acid-resistant binders, and low-carbon slabs. Prefabrication further re-shapes order patterns: large, repeatable modules permit longer-term supply agreements, boosting volume visibility for producers and allowing optimization of kiln maintenance windows.

The Europe cement market benefits from diversification across these end-user verticals. Renovation absorbs peaks in energy-efficient screeds; commercial projects reward suppliers that can document cradle-to-gate carbon intensities; and industrial builds open avenues for alkali-activated materials tailored to chemical environments. The aggregate effect is a demand profile less exposed to single-segment downturns, supporting the region’s projected mid-single-digit tonnage expansion.

Geography Analysis

The Europe cement market exhibits pronounced geographic bifurcation. Mature Northern economies such as Germany, France, and the Netherlands rely heavily on renovation and infrastructure maintenance, yielding predictable but slower volumes. Southern and Eastern states—including Spain, Poland, and Slovakia—enjoy stronger percentage growth on the back of greenfield transport and energy investments, albeit from lower baselines. Germany’s market contraction in 2024 has been partially offset by export runs into Benelux and Scandinavia, demonstrating the integrated nature of intra-EU clinker flows. Spain’s high-speed rail extensions and port expansion schemes are expected to lift domestic demand.

Western Europe’s strict environmental codes accelerate adoption of blended binders, evidenced by the Netherlands mandating maximum 50% clinker factor in public projects from 2027. In Central Europe, Poland’s industrial boom triggers clinker imports from Czechia and Slovakia, yet CBAM cost pass-throughs could render such inflows uneconomic once full pricing starts in 2026. Meanwhile the Nordic Countries leverage abundant renewable power to pioneer net-zero cement plants that may ultimately serve export markets.

Cross-border supply chains thus depend on ETS allocation disparities, freight-rail availability, and coastal kiln proximity. Producers positioned on deep-water terminals—such as Heidelberg Materials in northern Germany—retain a logistics advantage for shipping surplus clinker to the United Kingdom or Ireland, cushioning plant utilization rates. These inter-regional dynamics mitigate localized recessions and reinforce the strategic necessity of geographic diversification within the Europe cement market.

Competitive Landscape

The Europe cement industry features a moderately consolidated structure. Heidelberg Materials generated EUR 21.2 billion in revenue during 2024 and leads the decarbonization race with the GeZero carbon-capture project slated to abate 1 million tons of CO₂ annually upon commissioning. Holcim recorded CHF 26.4 billion in net sales and is rolling out the OLYMPUS near-zero cement line in Greece, a 2 million-ton facility backed by the EU Innovation Fund. Fresh from relocating its primary listing to the United States, CRH delivered USD 35.6 billion in revenue and committed USD 5 billion to acquisitions that broaden its European footprint.

Strategic thrusts converge on three vectors: (1) vertical integration into recycled aggregates and construction-demolition-waste (CDW) treatment, (2) geographic infill through bolt-on takeovers—illustrated by Çimsa Çimento’s EUR 330 million purchase of Ireland’s Mannok to secure EU market exposure, and (3) technology plays in carbon capture and alternative binders. Air Liquide’s partnership with Cementir on Danish CCS exemplifies cross-sector alliances that pool engineering expertise and funding eligibility. Competitive intensity is rising as low-carbon brands secure price premiums that outstrip tonnage losses, encouraging incumbents to accelerate product re-mixes toward blended, calcined-clay, and alkali-activated formulations.

Pricing power remains largely local given freight barriers and emission-cost asymmetries. Nonetheless, firms with diversified plant networks can arbitrage allowance prices by shifting clinker production toward sites with surplus free allocations. Digital platforms are now driving differentiation in production costs, marking a new era of operational competition in the European cement market.

Europe Cement Industry Leaders

Buzzi SpA

CEMEX S.A.B. de C.V.

CRH

Heidelberg Materials

Holcim

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Heidelberg Materials successfully completed the acquisition of Giant Cement Holding Inc. and its subsidiaries: Giant Cement Company, Dragon Products Company, and Giant Resource Recovery, on schedule. Giant Cement Holding Inc. specializes in cement production, emphasizing the use of waste-derived alternative fuels.

- May 2025: Holcim has initiated the work on the OLYMPUS project at its Milaki plant in Greece, designed to produce 2 million tons of near-zero cement annually by 2029. With an investment of EUR 400 million, the OLYMPUS project leverages innovation to support Europe’s Clean Industrial Deal. The project has also been awarded a grant from the EU Innovation Fund.

Europe Cement Market Report Scope

Cement is one of the most important construction materials. Cement is used to make concrete and mortar and has a variety of other applications in the construction sector. The cement market is segmented by type, application, and geography. By Type, the market is segmented into Portland, Blended and Other Types. By Application, the market is segmented into Residential, Commercial, Infrastructure, and Industrial and Institutional. The report also covers the market size and forecasts for the cement market in Europe. For each segment, the market sizing and forecasts have been done on the basis of volume (Million Tons).

| Ordinary Portland Cement (OPC) |

| Blended Cement |

| Others |

| Residential |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Nordic Countries |

| Poland |

| Rest of Europe |

| By Product Type | Ordinary Portland Cement (OPC) |

| Blended Cement | |

| Others | |

| By End-user Industry | Residential |

| Commercial | |

| Industrial and Institutional | |

| Infrastructure | |

| By Geography | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current Europe cement market size?

The Europe cement market size stood at 429.12 million tons in 2026 and is forecast to reach 501.68 million tons by 2031.

Which segment is growing fastest within the Europe cement market?

Blended Cement is the fastest-expanding product category, with a projected 4.62% CAGR through 2031 on the back of low-carbon mandates and performance benefits.

How does CBAM influence European cement producers?

CBAM imposes carbon costs on high-emission imports beginning in 2026, granting European producers that invest in decarbonization a pricing and market-share advantage over external competitors.

Why is Spain emerging as a key market?

Spain’s EUR 240 billion infrastructure pipeline, funded partly by the EU’s Recovery & Resilience Facility, is pushing the country’s cement demand to grow at a 4.23% CAGR through 2031.

How are energy prices affecting the Europe cement industry?

Even after demand destruction, natural-gas and electricity prices remain 21% above pre-crisis levels, squeezing margins and incentivizing fuel switching as well as long-term renewable-energy contracts.

What role does prefabrication play in future cement demand?

Prefabricated and modular construction reduces total cement tonnage per building but increases demand for high-performance specialty concretes that deliver rapid strength and dimensional accuracy, creating attractive margin opportunities.

Page last updated on: