Asia-Pacific Cement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

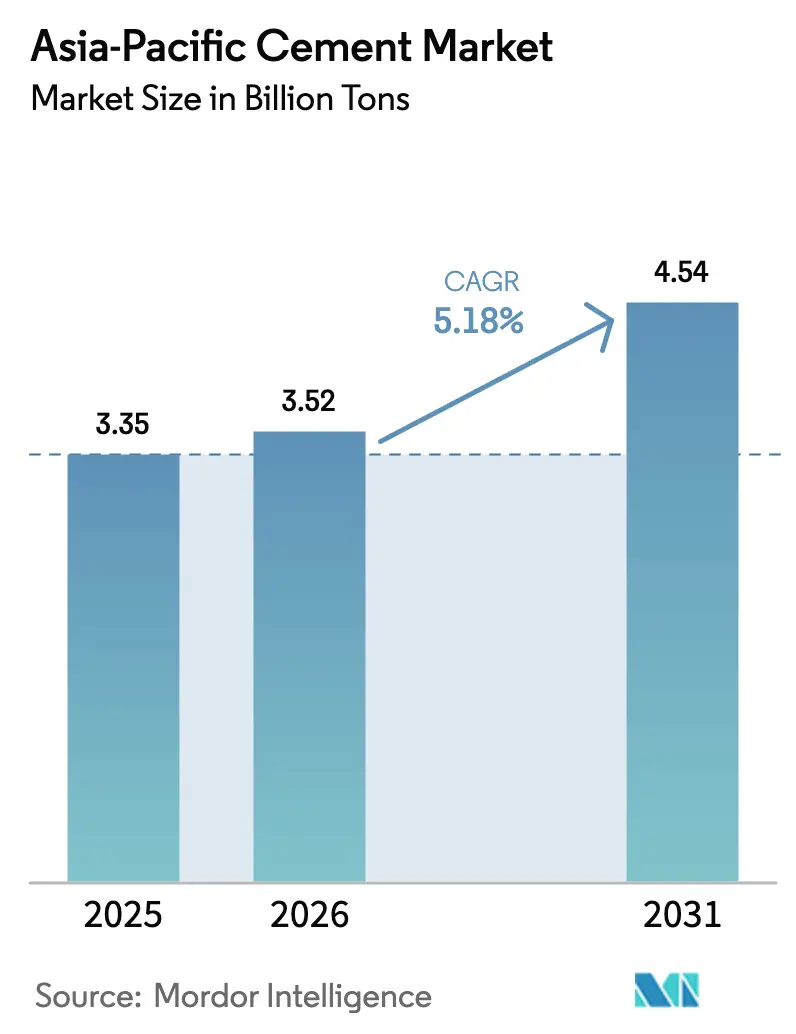

| Base Year Market Size (2025) | 3.35 Billion tons |

| Market Volume (2026) | 3.52 Billion tons |

| Market Volume (2031) | 4.54 Billion tons |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

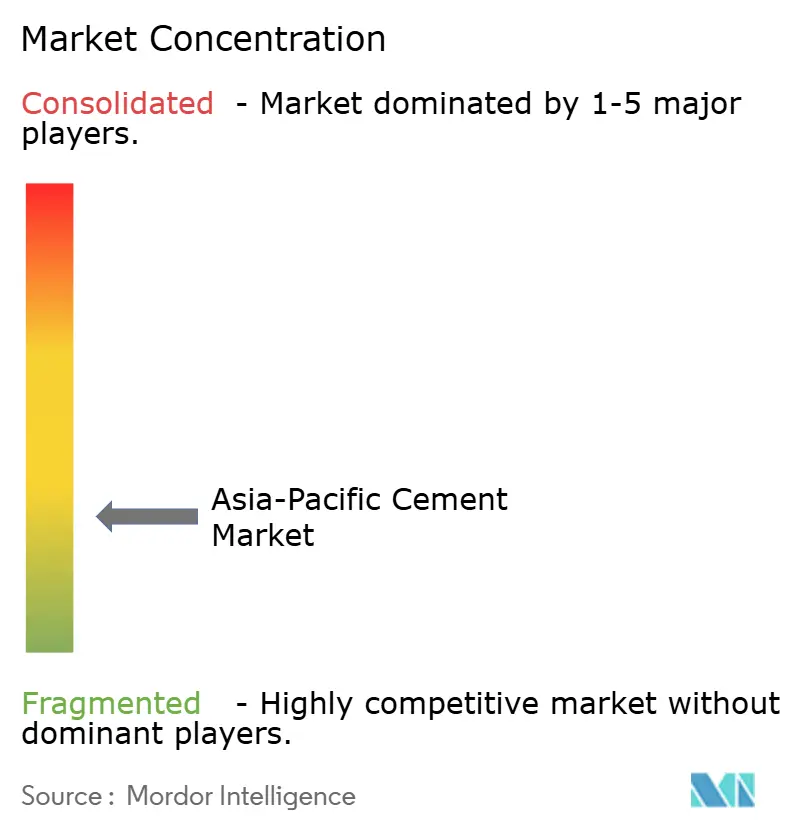

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Cement Market Analysis by Mordor Intelligence

The Asia-Pacific Cement market size is expected to grow from 3.35 billion tons in 2025 to 3.52 billion tons in 2026 and is forecast to reach 4.54 billion tons by 2031 at 5.18% CAGR over 2026-2031. The region’s cement demand rises in lockstep with infrastructure-heavy growth models, while product-mix shifts toward blended grades temper carbon intensity. Infrastructure programs across Vietnam, India, and Indonesia create natural demand hedges that offset China’s property downturn, and commercial construction accelerates on data-center and service-sector investment. Currency-diversified revenue streams, export arbitrage, and green-bond financing help large producers contain margin risk as thermal-fuel cost volatility lingers.

Key Report Takeaways

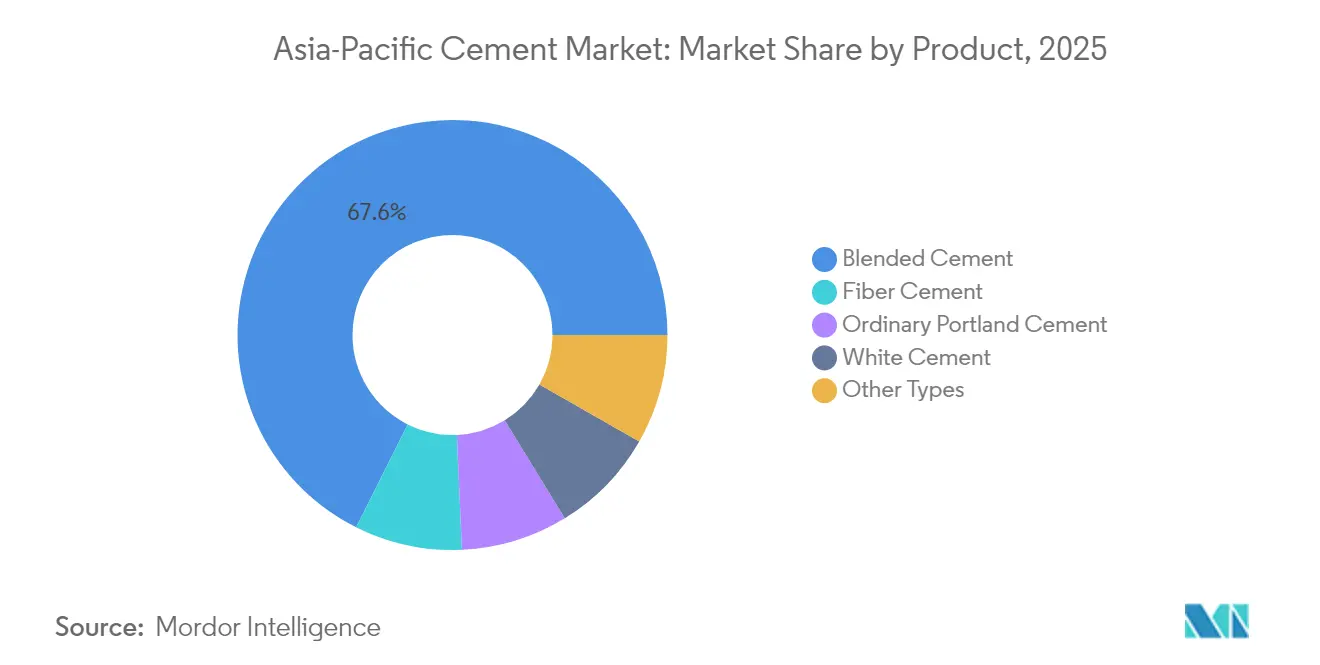

- By product, blended cement commanded 67.60% of the Asia-Pacific cement market size in 2025; fiber cement is advancing at a 6.52% CAGR through 2031.

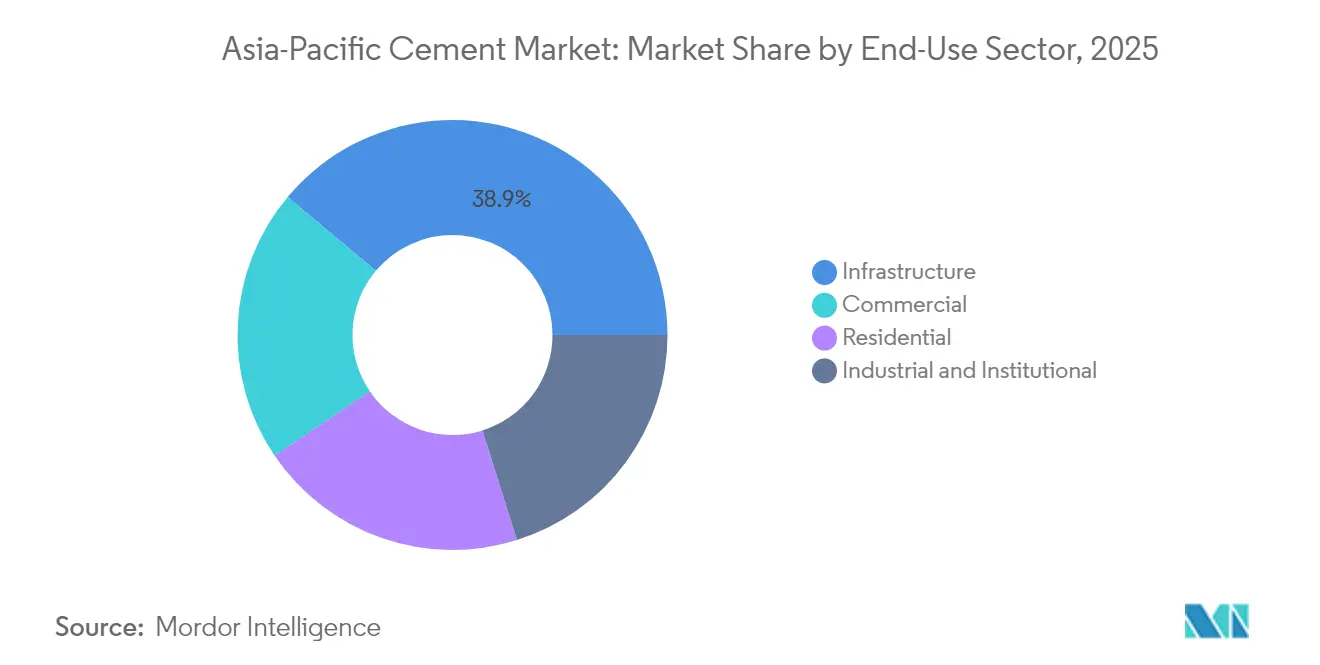

- By end-use, infrastructure led with 38.90% of the Asia-Pacific cement market share in 2025, while commercial construction posted the fastest 6.21% CAGR toward 2031.

- By geography, China held 68.10% of the Asia-Pacific cement market share in 2025, whereas Vietnam is forecast to expand at a 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Cement Market Trends and Insights

Drivers Impact Analysis*

| Drivers | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure stimulus packages | +1.8% | Vietnam, Indonesia, India; spillover to Thailand, Malaysia | Medium term (2-4 years) |

| Rapid urbanization and affordable-housing laws | +1.2% | India, Vietnam, Indonesia, Philippines | Long term (≥ 4 years) |

| Shift to blended cement | +0.9% | Australia, South Korea, Japan; spreading region-wide | Short term (≤ 2 years) |

| Green-bond funding for clinker reduction | +0.7% | Core Asia-Pacific markets with ESG-linked capital flows | Medium term (2-4 years) |

| Modular and off-site construction hubs | +0.6% | Australia, Japan, South Korea; technology transfer to ASEAN | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Infrastructure Stimulus Packages

Multi-year public-works pipelines underpin the Asia-Pacific cement market by smoothing cyclical swings in private real-estate activity. Vietnam allocates the equivalent of 7% of GDP each year to roads, rail, and climate-resilient ports, while Indonesia budgeted IDR 422.7 trillion for 2025 infrastructure projects. India’s transport corridors, Thailand’s logistics upgrades, and Malaysia’s flood-mitigation builds sustain steady order books for bulk cement and ready-mix suppliers. Project specifications increasingly require high-strength and low-carbon grades that lift average selling prices.

Rapid Urbanization and Affordable-Housing Mandates

Urban in-migration raises per-capita cement intensity as high-rise structures replace rural dwellings. National housing programs set minimum affordable-housing quotas, guaranteeing baseline demand that producers can match with staggered capacity additions. Vietnam’s protected domestic sector expands output to meet urban housing targets, while India links subsidies to energy-efficient building codes that promote blended cement. The resulting demand visibility compresses industry risk premiums and supports capital-expenditure cycles.

Shift Toward Blended Cement to Curb CO₂ Intensity

Large manufacturers accelerate supplementary-cementitious-material (SCM) usage to pre-empt carbon border adjustments and local trading-scheme costs. Thai, Japanese, and Korean projects already specify low-clinker blends that cut lifecycle emissions without sacrificing compressive strength. China is positioning the nation as a future fly-ash and slag-enhanced cement exporter. Blended grades unlock margin upside by stretching clinker kilns and generating green-premium revenue streams.

Green-Bond Funding Linked to Clinker-Factor Reduction

Banks and multilateral lenders now tie interest spreads to verified emissions performance, lowering capital costs for plants that trim clinker ratios or install waste-heat recovery. The Asian Infrastructure Investment Bank earmarks climate-adaptation bonds for kiln upgrades and carbon-capture pilots, and several producers tap local green-bond markets for alternative-fuel projects[1]Institute for Energy Economics and Financial Analysis, “EU carbon market leadership held back by weak pricing,” ieefa.org. Finance-driven decarbonization narrows the cost differential between legacy and next-generation cement and widens the moat for early adopters.

Restraints Impact Analysis*

| Restraints | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China real-estate slowdown | -2.1% | China; spillover to regional suppliers and raw-material exporters | Short term (≤ 2 years) |

| Volatile thermal-fuel prices | -0.8% | Indonesia, India, Australia; coal-intensive operations | Short term (≤ 2 years) |

| Tightening carbon pricing in Korea and Australia | -0.6% | South Korea, Australia; export-market compliance costs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining Real-Estate Investment in China

Developer liquidity stress and local-government debt controls cut housing starts and push cement output down. Surplus capacity may flow into export channels at discounts that undercut regional prices. While Beijing redirects stimulus toward infrastructure, the transition gap reduces kiln utilization and trims regional growth by an estimated 2.1 percentage points in the near term.

Volatile Thermal-Coal and Pet-Coke Prices

Kilns in Indonesia, India, and Australia still rely on coal for 60-80% of thermal input. Spot price spikes squeeze margins because fuel costs represent up to 40% of cash production expense. Producers hedge with longer-term contracts and diversify into refuse-derived fuels and biomass, yet implementation lags leave earnings exposed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Blended Cement Accelerates Decarbonization

Blended cement captured 67.60% of the Asia-Pacific cement market share in 2025, reflecting regulatory pressure and customer preference for low-carbon materials. The product lowers clinker content by combining fly-ash, slag, or calcined clay, enabling producers to sell more cement per ton of kiln capacity. Fiber cement posts a 6.52% CAGR, underpinned by demand for lightweight façade panels and weather-resistant siding in coastal regions prone to typhoons.

Ordinary Portland Cement remains pivotal for structural concrete but faces gradual share erosion as project owners adopt performance-based specifications. White cement maintains a niche for architectural finishes, commanding premium pricing despite limited volume. Producers invest in SCM grinding and distribution hubs to secure supply, and regional cross-border trade in slag and fly-ash grows as China’s industrial output provides surplus by-products.

By End-Use Sector: Infrastructure Holds the Demand Anchor

Infrastructure accounted for 38.90% of the Asia-Pacific cement market size in 2025 as highway, rail, and port projects absorbed large, continuous volumes. The segment benefits from multi-year funding pipelines that smooth cyclical swings and support procurement of blended and sulfate-resistant grades for marine structures. Commercial construction is the fastest-growing application at 6.21% CAGR, fueled by hyperscale data centers, logistics warehousing, and service-sector expansion in high-income economies.

Infrastructure spending in Vietnam, India, and Indonesia sustains clinker-plant utilizations even when residential momentum softens. New transport corridors spur follow-on commercial and residential developments, reinforcing demand chains. Meanwhile, the Asia-Pacific cement market sees residential projects supported by affordable-housing mandates and urban-mass-housing initiatives that encourage blended-cement uptake to meet energy-efficiency codes. Institutional builds—such as hospitals and schools—add incremental volume tied to social-infrastructure budgets.

Geography Analysis

China retained 68.10% of the Asia-Pacific cement market share in 2025. Producers look abroad for sales channels, with South Korean importers planning to source Chinese cement from 2026. Beijing’s emissions-trading expansion accelerates investment in SCM and carbon capture, potentially reshaping export competitiveness.

Vietnam is the fastest-growing geography at a 7.12% CAGR, buoyed by the USD 67 billion North-South high-speed railway and port upgrades. Domestic cement consumption grows year-over-year in March 2025 as megaproject sitework ramped up. Indonesia allocates IDR 422.7 trillion for its 2025 infrastructure.

India's growth is lifted by road, metro, and affordable-housing pipelines. Consolidation among large private groups improves scale efficiencies and accelerates alternative-fuel investments. Australia and Japan adopt carbon prices that encourage imports of blended cement from lower-cost Southeast Asian producers.

Malaysia and Thailand post stable mid-single-digit gains tied to logistics corridors and manufacturing-reshoring projects. The Philippines maintains anti-dumping duties on Vietnamese imports. The looming 2026 EU Carbon Border Adjustment Mechanism may redirect export flows toward intra-Asia trade and intensify competition in price-sensitive destinations.

Competitive Landscape

The Asia-Pacific Cement Market is fragmented. Asia-Pacific cement producers navigate a consolidation wave driven by carbon compliance costs and scale economies. Regional majors invest in waste-heat recovery and alternative-fuel infrastructure to lower cash costs and qualify for green finance. Corporate strategies emphasize vertical integration into ready-mix concrete, precast modules, and construction-chemical additives to capture downstream margins. Producers hedge geographic risk by acquiring stakes in Sub-Saharan Africa and Middle East plants, diversifying earnings beyond Asia-Pacific. Carbon-pricing differentials reshape trade flows, and first movers in carbon-capture and low-clinker products secure long-term offtake deals with global contractors and data-center developers.

Asia-Pacific Cement Industry Leaders

Anhui Conch Cement Co. Ltd.

China National Building Material Group (CNBM)

UltraTech Cement Ltd.

TCC GROUP HOLDINGS

SCG (Siam Cement Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Dalmia Bharat reached 49.5 million tonnes per annum (MTPA) cement capacity with the Rohtas plant expansion in Bihar, reinforcing its strategic growth in eastern India and contributing to capacity-driven momentum in the Asia-Pacific cement market. This development aligns with its long-term goal of scaling total capacity to 110 and 130 MTPA by 2031.

- January 2025: Ambuja Cements received 'no objection' from BSE and NSE for its merger with Adani Cementation, a move expected to drive consolidation, boost operational efficiency, and strengthen competitiveness in the Asia-Pacific cement market. The proposal for amalgamation between Adani Cementation and Ambuja Cements had received Board approval in June 2024.

Asia-Pacific Cement Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Blended Cement, Fiber Cement, Ordinary Portland Cement, White Cement are covered as segments by Product. Australia, China, India, Indonesia, Japan, Malaysia, South Korea, Thailand, Vietnam are covered as segments by Country.| Blended Cement |

| Fiber Cement |

| Ordinary Portland Cement |

| White Cement |

| Other Types |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| South Korea |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Product | Blended Cement |

| Fiber Cement | |

| Ordinary Portland Cement | |

| White Cement | |

| Other Types | |

| By End-Use Sector | Commercial |

| Industrial and Institutional | |

| Infrastructure | |

| Residential | |

| By Geography | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific |

Market Definition

- END-USE SECTOR - Cement consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of various types of cement such as ordinary portland cement, blended cement, white cement, fiber cement, etc. are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms