Smart Fleet Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

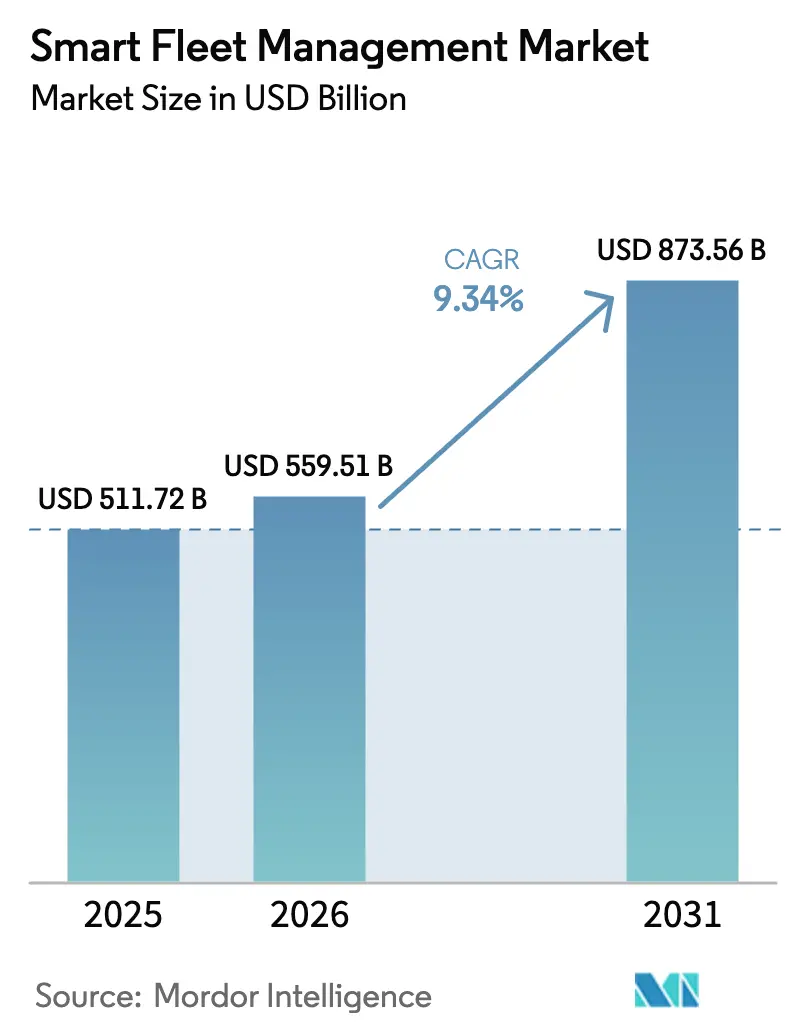

| Market Size (2026) | USD 559.51 Billion |

| Market Size (2031) | USD 873.56 Billion |

| Growth Rate (2026 - 2031) | 9.34% CAGR |

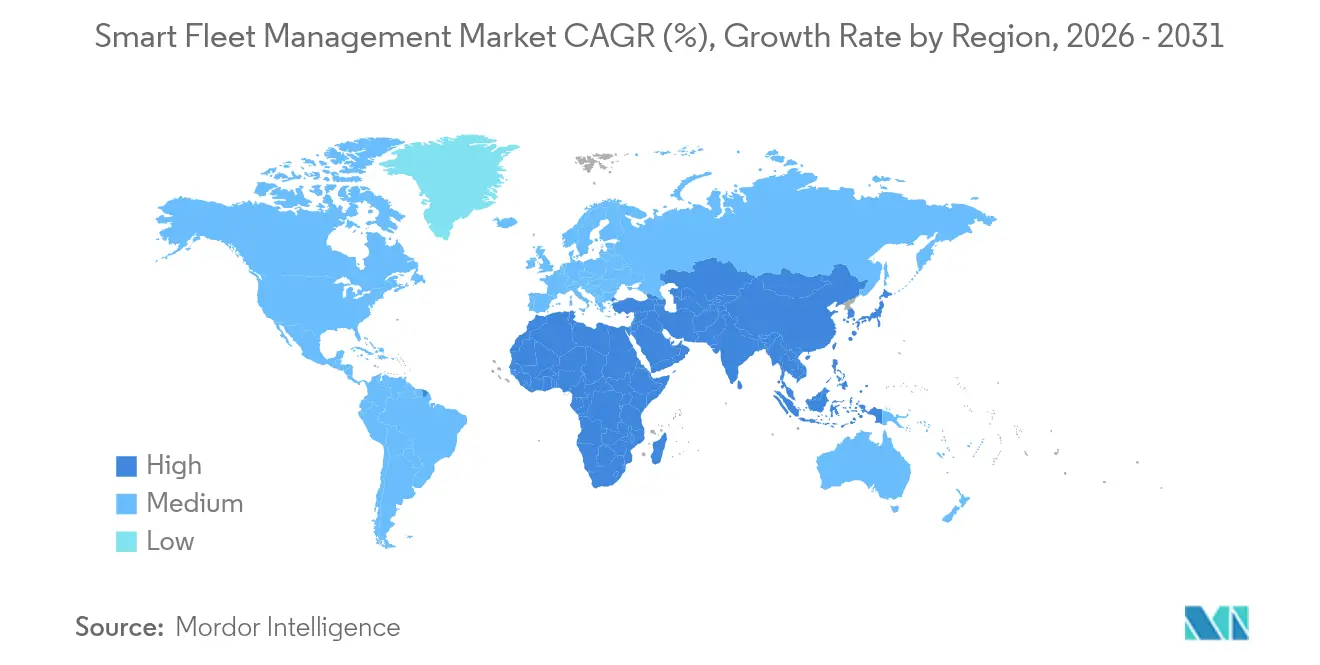

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Fleet Management Market Analysis by Mordor Intelligence

The smart fleet management market size was valued at USD 511.72 billion in 2025 and estimated to grow from USD 559.51 billion in 2026 to reach USD 873.56 billion by 2031, at a CAGR of 9.34% during the forecast period (2026-2031). A mix of mandated compliance technologies, maturing vehicle-centric connectivity, and cost-down cloud analytics keeps adoption momentum high. Insurance-linked video-telematics, OEM-installed data platforms in European trucks, and North American rules that force remote tachograph downloads push decision makers to digitize fleets rather than simply track assets. New 5G bandwidth, AI firmware updates, and falling sensor prices let providers roll out predictive safety, cold-chain tracking, and electric-vehicle (EV) energy management in one software stack. Vendors race to embed cameras and analytics directly at the edge, reducing data lag while meeting insurers’ risk-scoring needs. Meanwhile, OEMs package lifetime data services in the purchase price, trimming aftermarket hardware sales yet broadening the reachable customer base for software subscriptions.

Key Report Takeaways

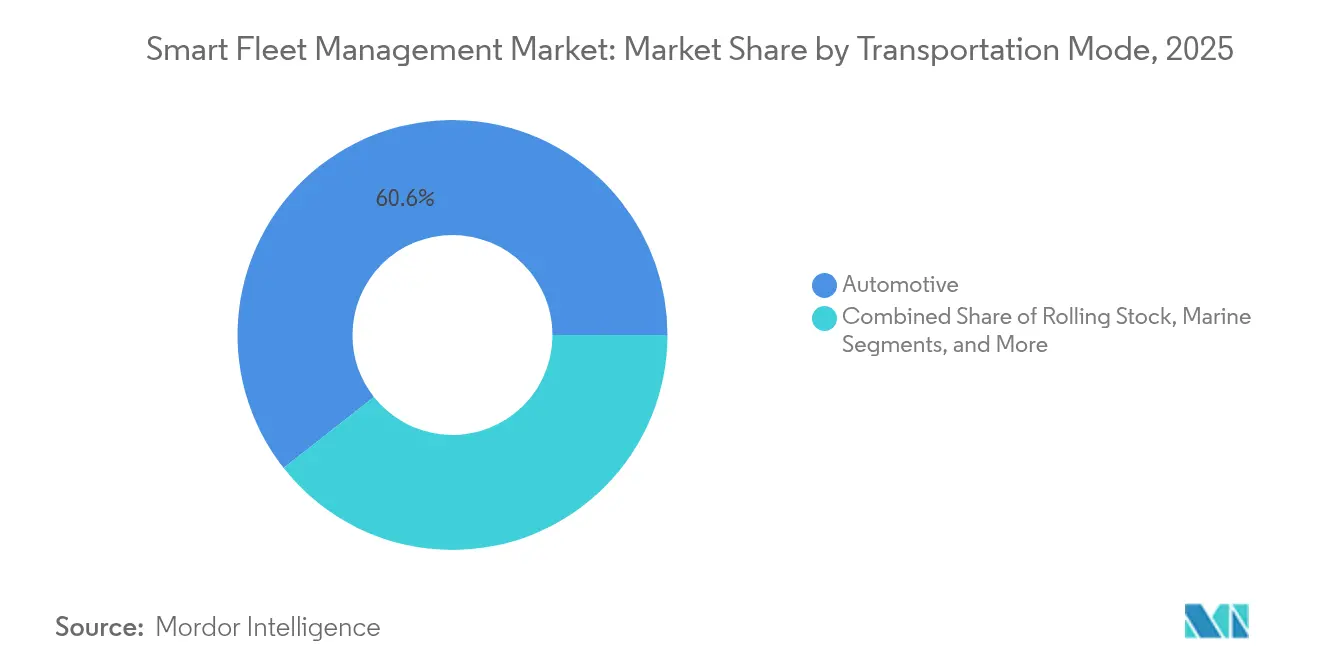

- By transportation mode, automotive operations led with 60.62% revenue share in 2025, while rolling stock is forecast to expand at a 9.55% CAGR through 2031.

- By solution, tracking and monitoring accounted for 35.10% of 2025 revenue; video-telematics and driver-safety tools post the fastest 12.15% CAGR to 2031.

- By hardware, on-board diagnostics dongles captured 28.20% market share in 2025, whereas multi-camera systems are advancing at an 11.05% CAGR.

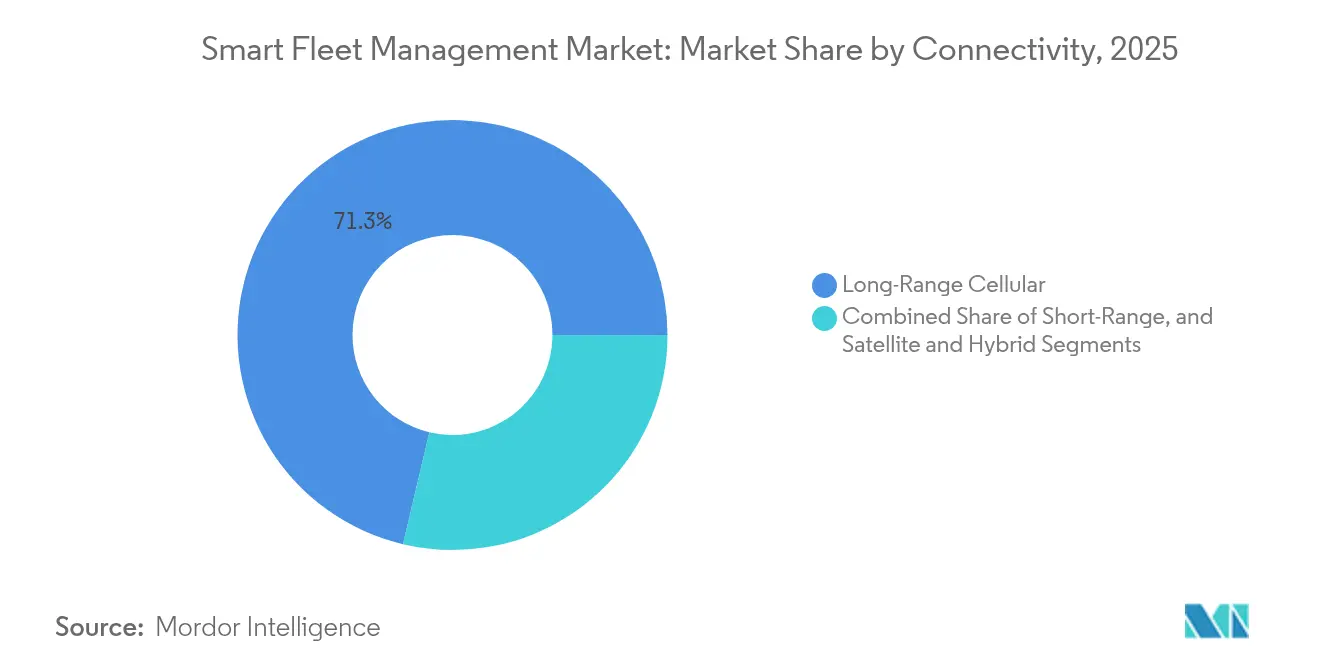

- By connectivity, long-range cellular commanded 71.30% share in 2025, and 5G long-range connectivity is projected to grow 12.65% annually through 2031.

- By fleet size, large fleets (≥250 vehicles) held 46.10% revenue share in 2025; small fleets (1-49 vehicles) record the highest 9.85% CAGR to 2031.

- By end-user vertical, logistics and last-mile delivery captured 38.20% of 2025 revenue, while public transport and MaaS segments are growing at a 9.52% CAGR.

- By geography, North America commanded 33.75% market share in 2025, and Asia-Pacific is the fastest-growing region with an 10.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Fleet Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of video-telematics for insurance-linked risk-scoring | +1.8% | Global with focus in North America and EU | Medium term (2-4 years) |

| Surge in OEM-embedded connectivity in European commercial vehicles | +1.5% | Europe core; spill-over to North America | Short term (≤ 2 years) |

| Mandates for remote tachograph data download in North America | +1.2% | North America; regulatory influence in Mexico | Short term (≤ 2 years) |

| Transition to electric delivery fleets elevating EV-specific platforms in Asia | +1.4% | Asia-Pacific core; emerging in Latin America | Long term (≥ 4 years) |

| Cloud-native AI edge analytics cutting TCO for SME fleets | +1.6% | Global with early adoption in developed markets | Medium term (2-4 years) |

| Real-time cold-chain compliance tracking boosting sensor-heavy solutions | +1.1% | Food & pharma corridors worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Video-Telematics for Insurance-linked Risk-Scoring

Fleet insurers now reward camera adoption with measurable premium reductions after risk models proved accurate in reducing fraud and collision frequency. Munich Re data shows telematics-equipped fleets cut high-risk driver incidents by 40% and fraudulent claims by 50%.[1]Munich Re, “Leveraging Telematics to Get the Most from Insurance,” munichre.com Verizon Connect users registered 13% insurance premium savings in 2025 thanks to proven safer driving records.[2]Verizon Connect, “Fleet Management 2025 Outlook,” fleetmaintenance.com AI models process footage at the edge, giving managers instant alerts and allowing underwriters to price by exposure instead of averages.

Surge in OEM-Embedded Connectivity in Commercial Vehicles across Europe

Truck makers such as Volvo now embed telematics control units for compliance, remote diagnostics, and subscription-based uptime services.[3]Volvo Trucks, “Fleet Management Services,” volvotrucks.com Continental’s 4G-to-5G TCUs reduce aftermarket install time while shielding data with secure firmware.[4]Continental Automotive, “Telematic Solutions,” continental-automotive.com Stellantis’ Mobilisights program funnels raw CAN data to cloud dashboards without add-on boxes, making data a built-in feature media.stellantis.com.

Mandates for Remote Tachograph Data Download in North America

FMCSA rules effective 2025 compel automatic emergency braking, speed limiters, and compliant ELDs on trucks above 26,000 lb, raising near-term demand for integrated fleet compliance suites. Fleets must transmit logs remotely to enforcement portals, cutting roadside inspection time and forcing laggard carriers to upgrade systems. J.J. Keller found 47% of managers cite digital Driver Qualification files as their top compliance headache.

Transition to Electric Delivery Fleets Driving EV-Specific Fleet Platforms in Asia

Philippine provider Mober scaled to 500 electric vans, relying on battery analytics that predict range and schedule charging stops. Regional policy, including the Electric Vehicle Industry Development Act, grants tax breaks for charging deployments, nudging couriers toward electrification. Samsara’s EV dashboards map state-of-charge and charger availability in one pane, a necessity for couriers chasing on-time metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented telematics hardware standards in aftermarket | -1.3% | Global; sharper in emerging markets | Long term (≥ 4 years) |

| Cyber-security liability exposure for fleet operators | -1.1% | Worldwide; strict in regulated sectors | Medium term (2-4 years) |

| Capital-intensive retrofit of legacy rail & marine assets | -0.9% | Infrastructure-heavy regions | Long term (≥ 4 years) |

| Shortage of certified installers delaying roll-outs | -0.8% | Rural & emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Telematics Hardware Standards in Aftermarket

Mixed-brand fleets juggle incompatible cables, SIMs, and firmware, locking them to specific vendors and raising total integration cost. US DoT cybersecurity guidance urges common data schemas yet stops short of mandates. Geotab supports 157 OEM data protocols, highlighting the complexity of patchwork compatibility. Without a unifying standard, emerging-market operators defer investments, slowing global penetration.

Cyber-Security Liability Exposure for Fleet Operators

Telematics endpoints expose attack surfaces ranging from SIM hijacking to CAN-bus spoofing. Academic work shows adversarial AI can alter machine-vision models that govern autonomous braking. Work Truck Online stresses that privacy breaches now escalate from IT risk to carrier liability, especially as ELD data links directly to payroll and safety scores. Fleets allocate more budget toward encryption and SOC monitoring, tempering near-term ROI expectations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transportation Mode: Automotive Dominance with Rail Acceleration

Automotive operations accounted for 60.62% of the smart fleet management market in 2025, reflecting decades of telematics familiarity among truck and van operators. Rail freight, however, is poised for 9.55% CAGR as platforms such as RailPulse stream near real-time wagon health and GPS data to North American carriers. The smart fleet management market size for rolling stock applications therefore expands faster than the baseline, spurred by regulation and shipper demand for ETA accuracy. Marine sectors integrate AI-based vibration diagnostics, while aviation explores drone traffic management feeds, yet their adoption curves trail land-based modes due to harsher certification cycles.

Rail innovation borrows from automotive successes. Amsted’s IQ Series units, now RailPulse-certified, attach to freight wagons in minutes and feed condition data to central dashboards. CAF Digital Services’ LeadMind cuts corrective maintenance hours by 51% on European commuter fleets. Cross-mode knowledge sharing accelerates deployment speed and reduces vendor risk, propelling overall smart fleet management market expansion.

By Solution: Tracking Foundation with Video-Telematics Surge

Tracking and monitoring still held 35.10% smart fleet management market share in 2025 because location visibility underpins every higher-order workflow. Video-centric safety suites, though, are logging the quickest 12.15% CAGR as insurers and regulators value visual proof during claims. The smart fleet management market size for video-based solutions rises alongside compute power that processes HD feeds on the edge without data-plan blowouts.

Samsara’s AI safety platform, after training on billions of miles, flags distraction or drowsiness in real time and cut incident rates 35% among pilot fleets. Coupled route-optimization modules then use the same telematics data to reduce empty miles, compressing ROI cycles. Customer demand is shifting from point solutions to consolidated dashboards that blend location, diagnostics, and safety footage, a trend vendors leverage by bundling services under per-vehicle subscriptions.

By Hardware: OBD Dongles Lead with Multi-Camera Growth

On-board diagnostics dongles supplied 28.20% of hardware shipments in 2025 because they snap into legacy vehicles and cost under USD 150 per unit. Yet multi-camera arrays are scaling faster at 11.05% CAGR as fleets future-proof for driver-assistance and autonomous upgrades. Magna’s fifth-generation forward camera offers 50% more processing than its predecessor, supporting full-color detection of traffic lights and emergency vehicles.

Beyond vision, GNSS modules, tire-pressure sensors, and BLE tags feed edge gateways for consolidated analytics. Zonar’s new light-duty telematics control unit extends heavy-truck grade analytics to vans, broadening addressable market. A maturing component ecosystem lowers entry costs even as functionality climbs, reinforcing the smart fleet management market’s upward trajectory.

By Connectivity: Cellular Dominance with 5G Acceleration

Long-range cellular accounted for 71.30% of active connections in 2025 thanks to mature LTE networks and global roaming agreements. The next leap is 5G, tracking a 12.65% CAGR as bandwidth-hungry video analytics and remote firmware updates migrate to new radios. Inseego’s enterprise CPE now delivers 11 Gbps download and 3.7 Gbps upload, with onboard AI shaping traffic for fleet-critical packets.

Short-range Bluetooth remains key for driver handheld integration and legacy diagnostic readers, while satellite fills Eurasian and oceanic coverage gaps. Hybrid modems blend cellular and GNSS receivers, ensuring continuous contact during route deviations. Connectivity diversity ultimately expands the smart fleet management market size by serving niches once deemed unreachable.

By Fleet Size: Enterprise Scale with SME Acceleration

Large carriers with over 250 vehicles still generated 46.10% of revenue in 2025, justified by clear ROI on downtime reduction and fuel savings. Nevertheless, the small fleet cohort shows 9.85% CAGR as SaaS pricing and self-install hardware punch through previous cost barriers. Insurance Business projects ANZ installed units to jump from 1.6 million in 2023 to 2.7 million in 2028, with SME adoption as the main lever.

Wholesale platform integration lowers per-vehicle licensing for SMEs. Geotab’s pact with EROAD targets micro-fleets that lack IT staff, providing pre-configured dashboards deployed from the cloud. The spreading user base lifts overall smart fleet management market penetration and spurs vendors to refine intuitive UIs over bespoke consulting.

By End-User Vertical: Logistics Leadership with Public Transport Growth

Logistics and last-mile couriers captured 38.20% of 2025 spend because route density and service-level penalties make telematics indispensable. Public transport and Mobility-as-a-Service segments, however, will outpace at 9.52% CAGR as agencies modernize dispatch based on AI. The Federal Transit Administration funded Prairie Hills Transit’s AI dispatch system that handles more rides without extra staff, validating ROI for rural operators.

Emergency and utility fleets require uptime and compliance above cost savings, prompting close vendor collaboration. Samsara’s integration with Esri supplies city operators real-time vehicle location against GIS layers to shorten response times. Catering to such vertical nuance enlarges the smart fleet management market while deepening vendor lock-in through specialized modules.

Geography Analysis

North America retained 33.75% share in 2025. Federal rules around ELDs, speed limiters, and zero-emission transitions nudge both public and private fleets toward unified data platforms. AT&T’s pilot with Rivian shifts its service vans to electric while piggybacking on existing LTE/5G telematics backbones. Canadian provincial projects leveraging Geotab APIs for carbon accounting reinforce policy-led adoption curves. Mexico benefits from cross-border harmonization, giving regional fleets reason to standardize on compliant hardware. As 5G coverage surpasses 85% of interstate corridors, the smart fleet management market in North America pivots toward bandwidth-heavy video analytics and over-the-air ECU updates.

Asia-Pacific is tracking 10.72% CAGR through 2031, the fastest worldwide. The smart fleet management market here skews to EV delivery fleets and leapfrog telematics where smartphones sub in for rugged MDVR units. Manila-based Mober fielded 500 e-trucks by 2025, each logging battery health via cloud dashboards and receiving route adjustments based on charging station density. China’s urban freight pilot zones and Japanese Tier-1 electronics expertise feed domestic vendor ecosystems, while India and Southeast Asia lean on subscription models priced per day, not per month, to match cash-flow realities. Hybrid satellite-cellular hardware supports mining-logistics corridors across Australia and Indonesia, lifting adoption in harsh terrains.

Europe grows steadily on the back of regulatory deadlines, notably the EU Mobility Package requiring second-gen smart tachographs by August 2025. OEM-native platforms flourish as hardware is factory-installed and billed within lease packages, cutting install downtime. Samsara’s Stellantis tie-up funnels European vehicle CAN data straight into Mobilisights without dongles, proving the hardware-less model. Specialized suppliers such as Schmitz Cargobull snap up niche players like Atlantis Global System to dominate cold-chain trailers. Eastern European carriers modernize to comply with EU cross-border cabotage audits, broadening the addressable smart fleet management market.

South America and the Middle East and Africa trail but show sporadic surges linked to infrastructure projects and mining/energy supply chains. High import duties on telematics boxes and patchy 4G coverage slow progress, yet multi-modal corridors such as Brazil–Chile and the GCC rail initiative create pockets of rapid, policy-driven deployment. Vendors now offer solar-powered gateway units and low-orbit satellite links to address coverage gaps, keeping the smart fleet management market visible even in frontier geographies.

Competitive Landscape

Competition is moderate, with the five largest vendors holding roughly one-third of global revenue. Incumbents accelerate M&A to defend scale and cross-sell breadth. Powerfleet paid USD 200 million for Fleet Complete, uniting 2.6 million connected assets under one data lake. Platform Science bought Trimble’s telematics unit; Trimble took 32.5% equity in the combined firm to secure roadmap influence. Element Fleet Management acquired Autofleet to layer route optimization onto its leasing core.

Technology vectors drive differentiation. Samsara spends heavily on AI, releasing driver drowsiness detection and Intelligent Safety Platform upgrades that slash event frequency for thousands of customers. Geotab positions its open data store and 157-OEM plug-ins as an antidote to hardware fragmentation. Carrier doubles down on cold-chain compliance via Lynx Fleet, while Wabtec and Amsted jointly push rail telematics for heavy-haul operators.

New entrants target slivers where incumbents move slowly, such as AI-only software for micro-fleets or battery analytics for last-mile e-bikes. Yet hardware commoditization pressures margin, forcing software-heavy subscription bundles. Strategic partnerships-AT&T with Fleet Complete or Hyundai Translead with Samsara-blur lines between carrier, OEM, and software house, creating integrated service tiers that lock customers for the vehicle life cycle. Price competition remains most intense in GPS-only trackers, whereas bundled safety-plus-compliance contracts defend premium pricing.

Smart Fleet Management Industry Leaders

Zonar Systems, Inc.

Hitachi Limited

Geotab Inc.

Sintrones Technology Corporation

Verizon Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Inseego unveiled 5G Advanced wireless broadband with 11 Gbps downlink and AI traffic shaping for industrial fleets.

- May 2025: Samsara rolled out Intelligent Safety Platform, Smart Trailers with tire-health sensors, and real-time hazard feeds.

- March 2025: Samsara and Hyundai Translead integrated HT LinkVue for factory-installed trailer visibility across North America.

- March 2025: Wabtec joined RailPulse vendor roster to speed rail-car digitization.

- March 2025: Fleetio raised USD 450 million Series D and bought Auto Integrate, expanding a network of 110,000 repair shops.

Global Smart Fleet Management Market Report Scope

Smart fleet management employs advanced technologies to enhance the efficiency and effectiveness of vehicle fleet operations. This modern solution refines multiple facets of fleet oversight by harnessing real-time data, GPS tracking, telematics, IoT protocols, and predictive analytics. Whether it is assessing vehicle health, fine-tuning routes, managing fuel usage, or analyzing driver behavior, smart fleet management shifts conventional operations into a data-centric, efficient, and responsive realm.

The study tracks the revenue accrued through the sale of smart fleet management types by various players globally. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report's scope encompasses market sizing and forecasts for the various market segments.

The smart fleet management market is segmented by transportation mode (marine, rolling stock, automotive, and other modes), solution (tracking and monitoring, route optimization, ADAS, remote diagnostics, telematics, and other solutions), hardware (onboard diagnostics (OBD), cameras, sensors, and GPS devices), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Automotive |

| Rolling Stock |

| Marine |

| Other Modes (Aviation, Drones, Off-highway) |

| Tracking and Monitoring |

| Route Optimization and Dispatch |

| Advanced Driver-Assistance Systems (ADAS) |

| Remote Diagnostics and Prognostics |

| Telematics Data Analytics (AI/ML) |

| Video-Telematics and Driver Safety |

| On-board Diagnostics (OBD) Dongles |

| Multi-camera (DMS, ADAS) |

| GNSS/Dual-band GPS Devices |

| Sensor Suites (LiDAR, Temp, Fuel, Tire) |

| Short-Range (Bluetooth/Wi-Fi) |

| Long-Range Cellular (4G/5G) |

| Satellite and Hybrid |

| 1-49 Vehicles (Small) |

| 50-249 Vehicles (Medium) |

| 250+ Vehicles (Large/Enterprise) |

| Logistics and Last-mile Delivery |

| Public Transport and Mobility-as-a-Service |

| Utilities, Oil and Gas, Mining |

| Emergency and Government Fleets |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Transportation Mode | Automotive | ||

| Rolling Stock | |||

| Marine | |||

| Other Modes (Aviation, Drones, Off-highway) | |||

| By Solution | Tracking and Monitoring | ||

| Route Optimization and Dispatch | |||

| Advanced Driver-Assistance Systems (ADAS) | |||

| Remote Diagnostics and Prognostics | |||

| Telematics Data Analytics (AI/ML) | |||

| Video-Telematics and Driver Safety | |||

| By Hardware | On-board Diagnostics (OBD) Dongles | ||

| Multi-camera (DMS, ADAS) | |||

| GNSS/Dual-band GPS Devices | |||

| Sensor Suites (LiDAR, Temp, Fuel, Tire) | |||

| By Connectivity | Short-Range (Bluetooth/Wi-Fi) | ||

| Long-Range Cellular (4G/5G) | |||

| Satellite and Hybrid | |||

| By Fleet Size | 1-49 Vehicles (Small) | ||

| 50-249 Vehicles (Medium) | |||

| 250+ Vehicles (Large/Enterprise) | |||

| By End-user Vertical | Logistics and Last-mile Delivery | ||

| Public Transport and Mobility-as-a-Service | |||

| Utilities, Oil and Gas, Mining | |||

| Emergency and Government Fleets | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the smart fleet management market?

The smart fleet management market is valued at USD 559.51 billion in 2026 and is forecast to reach USD 873.56 billion by 2031.

Which segment grows fastest within the smart fleet management market?

Video-telematics and driver-safety solutions record the quickest 12.15% CAGR through 2031 as insurers reward visual risk validation.

Why is Asia-Pacific the fastest-growing region?

Rapid EV adoption, supportive policy frameworks, and leapfrog cloud pricing propel Asia-Pacific to an 10.72% CAGR through 2031.

How does 5G impact smart fleet management?

5G enables real-time video streaming, edge analytics, and faster over-the-air updates, spurring a 12.65% CAGR in 5G-connected fleets.

What challenges slow market adoption?

Fragmented aftermarket hardware standards and rising cybersecurity liability remain key restraints, trimming growth by 1.3% and 1.1% points, respectively.

Which companies are leading consolidation?

Powerfleet, Platform Science, Element Fleet Management, Samsara, and Geotab spearhead recent acquisitions, together holding roughly one-third of global revenue.

Page last updated on: