Ester Gum Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

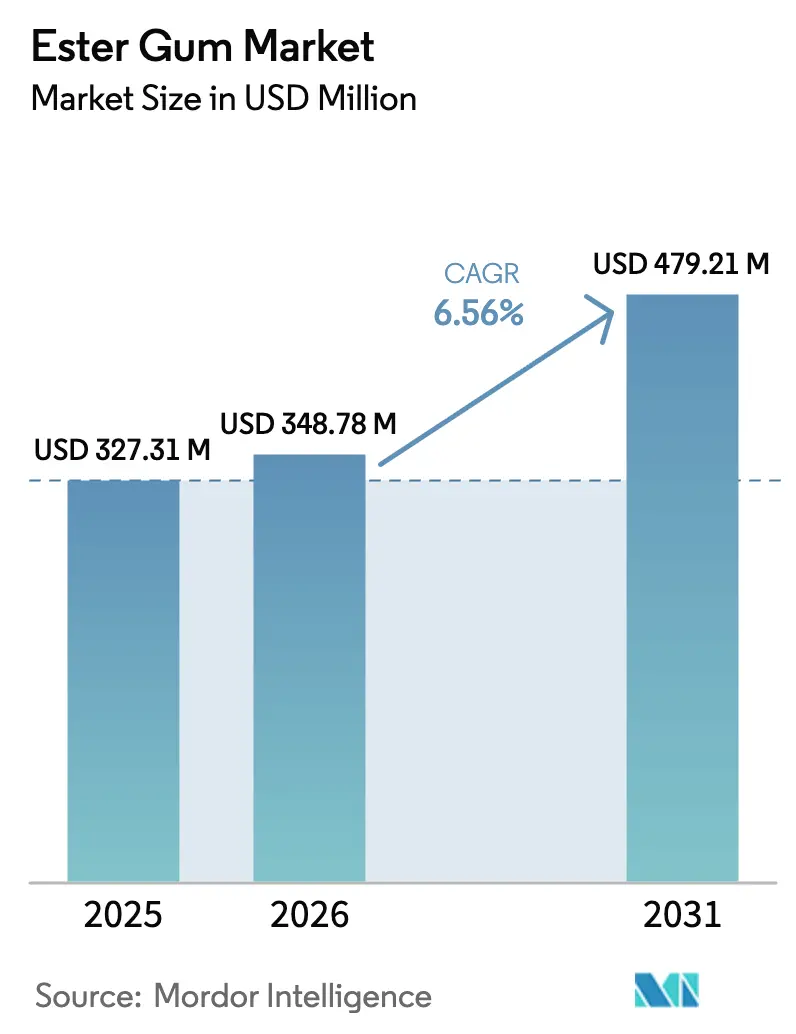

| Market Size (2026) | USD 348.78 Million |

| Market Size (2031) | USD 479.21 Million |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

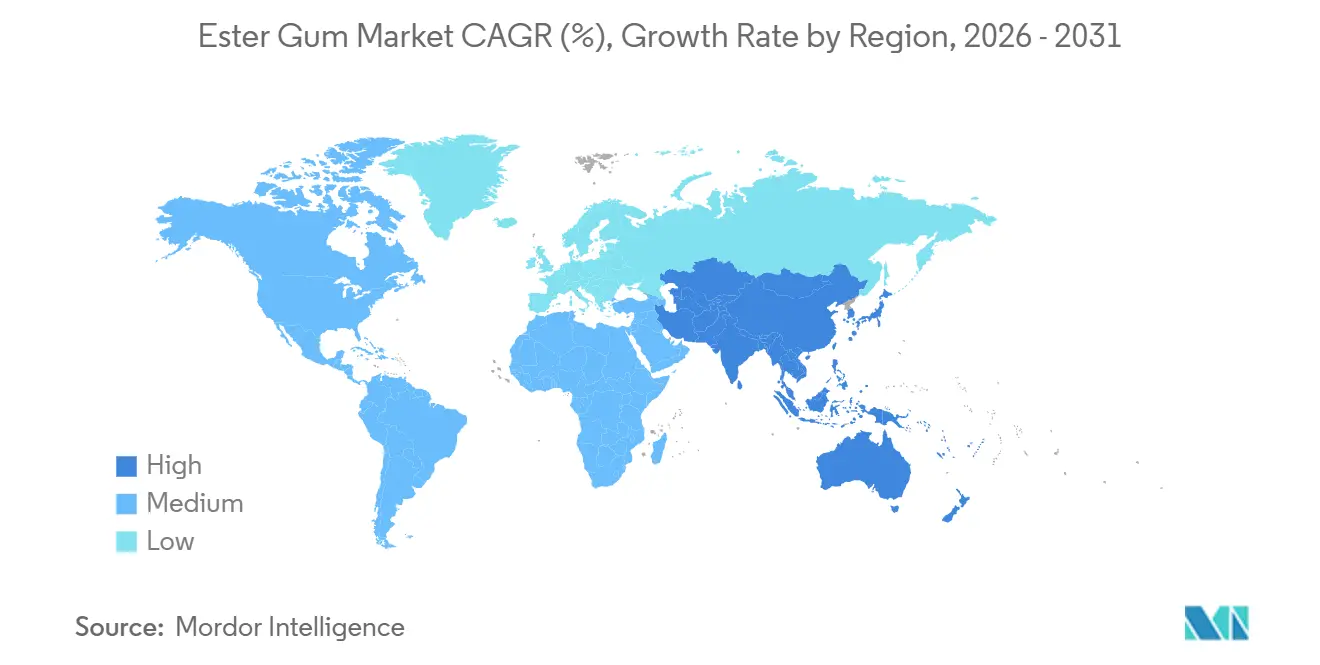

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

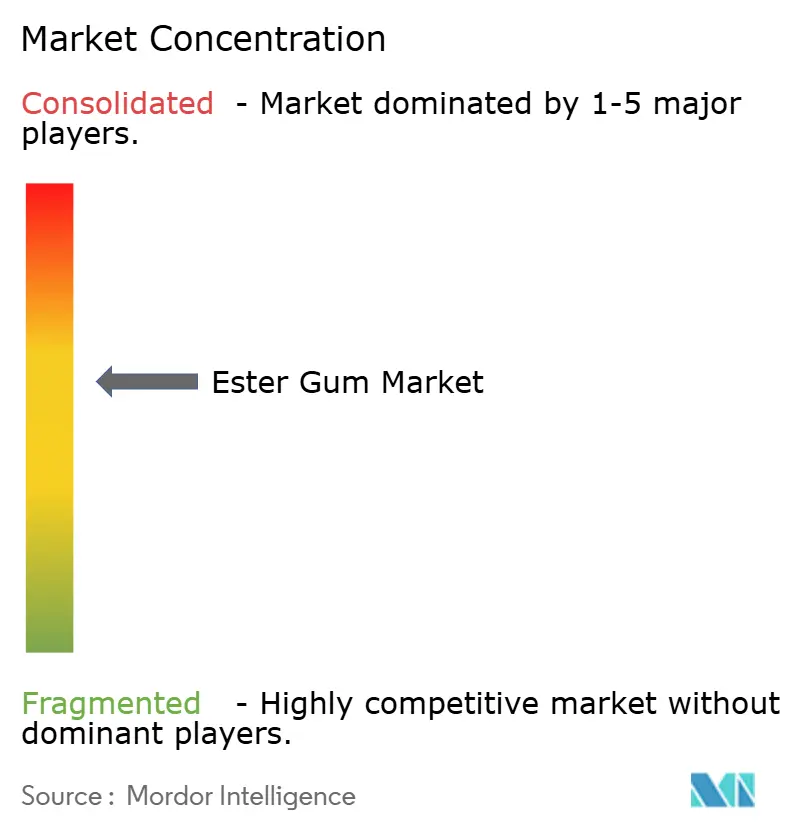

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ester Gum Market Analysis by Mordor Intelligence

The Ester Gum Market size was valued at USD 327.31 million in 2025 and is estimated to grow from USD 348.78 million in 2026 to reach USD 479.21 million by 2031, at a CAGR of 6.56% during the forecast period (2026-2031). Growth is being propelled by the FDA’s 2024 revocation of brominated vegetable oil, the adhesives sector’s pivot toward bio-based tackifiers, and stricter VOC limits that are reshaping architectural coatings. Rising demand for cloud emulsifiers in citrus beverages, cost advantages created by biodiesel-derived glycerol, and China’s dominance in gum-rosin supply are reinforcing momentum across every major region. Competitive intensity is moderate, with the top five players holding about 66% of global sales and deploying vertical integration, rapid regulatory filing, and formulation customization to defend share. Despite periodic feedstock price swings, the ester gum market continues to benefit from a structural shift toward natural ingredients, an oversupply of low-cost glycerol, and expanding construction activity in Asia-Pacific.

Key Report Takeaways

- By type, glycerol esters of wood rosin (GEWR) held 36.47% of ester gum market share in 2025, while penta ester gum (PEGR) is projected to post the fastest 6.74% CAGR through 2031.

- By application, food and beverages accounted for 34.28% of ester gum market size in 2025, yet paints, inks and coatings are advancing at a 6.68% CAGR to 2031.

- By geography, Asia-Pacific commanded 48.36% of ester gum market share in 2025 and is set to grow at a 6.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ester Gum Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Bio-Based Tackifiers in Adhesives | +1.2% | Global, with APAC core and spill-over to North America | Medium term (2-4 years) |

| Growth of Sugar-Free and Functional Chewing Gum | +0.9% | North America and Europe, expanding to APAC urban centers | Medium term (2-4 years) |

| Regulatory Replacement of BVO in Beverages | +1.5% | North America (FDA mandate), Europe (EFSA compliance), Latin America following | Short term (≤ 2 years) |

| Expansion of Eco-Friendly Paints, Inks, and Coatings | +1.1% | Europe (VOC regulations), APAC (construction boom), North America (green building standards) | Long term (≥ 4 years) |

| Oversupply of Low-Cost Glycerol from Biodiesel | +0.6% | Global, concentrated in US, EU, Brazil, Argentina biodiesel hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for Bio-Based Tackifiers in Adhesives

Packaging and pressure-sensitive adhesive formulators are switching from petroleum hydrocarbon resins to glycerol esters of rosin to satisfy brand-owner sustainability mandates and mitigate crude-oil price risk. GEWR delivers comparable peel strength with 15-20% lower VOC emissions, a key benefit as the EU’s Industrial Emissions Directive tightens limits to 50 g/L for adhesive use by 2028. Arakawa Chemical’s Super Ester W-series, offering softening points of 85 °C–115 °C, is gaining traction on Asia-Pacific e-commerce packaging lines that demand rapid set and thermal stability. A 2025 USPTO filing by Eastman Chemical details a maleic-anhydride-modified glycerol-rosin ester that bonds effectively to polyethylene films, underscoring continuing R&D investment.

Growth of Sugar-Free and Functional Chewing Gum

Sugar-free and functional gum bases rely on ester gum for film formation and adhesion, with loadings of 50-85% in the finished base. In 2025, sugar-free variants captured 62% of chewing-gum sales in North America and Europe, while functional formats fortified with caffeine, vitamins, or CBD accelerated shelf rotation. Ester gum’s neutral taste and compatibility with high-intensity sweeteners allow rapid flavor release without the waxy mouthfeel of synthetic polyvinyl acetate. GRAS status under 21 CFR 172.735 permits up to 100 ppm in finished gum, reinforcing regulatory certainty in the United States.

Regulatory Replacement of BVO in Beverages

The FDA revoked brominated vegetable oil approval in July 2024, forcing citrus soft-drink and sports-beverage manufacturers to reformulate with glycerol ester of wood rosin. EFSA simultaneously confirmed a 10 mg/kg body-weight ADI for E 445, provided the rosin originates from Pinus palustris or P. elliottii, which favors traceable North American and select Asian suppliers. Beverage multinationals have locked in multi-year supply contracts that lifted spot ester gum prices by 8-12% compared with the pre-ban period.

Oversupply of Low-Cost Glycerol from Biodiesel

Renewable-fuel mandates generated about 1.2 million t of surplus glycerol in 2025, slicing spot prices to USD 300–350 per t and trimming ester gum variable costs by up to 15%[1]U.S. Department of Agriculture, “Global Biodiesel Outlook 2025,” usda.gov . Ingevity leverages agreements with biodiesel refiners in the US Southeast to capture this margin advantage and finance capacity debottlenecking projects. Although renewable diesel produces less glycerol per liter than conventional biodiesel, the present glut is expected to support margins for at least two more years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gum-Rosin Feedstock Price Volatility | -0.8% | Global, concentrated in China (Guangxi, Yunnan) and India (Odisha, Chhattisgarh) | Short term (≤ 2 years) |

| Stringent Environmental and Food-Additive Rules | -0.5% | Europe (EFSA species restrictions), North America (FDA traceability), APAC (FSSAI compliance) | Medium term (2-4 years) |

| Competition from Terpene/Hydrocarbon Resins | -0.4% | Global, with North America and Europe most exposed to synthetic-resin substitution | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Gum-Rosin Feedstock Price Volatility

Spot gum-rosin prices swung 18–22% during 2024-2025 because labor shortages disrupted tapping in China’s Guangxi province and erratic monsoons hurt yields in Odisha and Chhattisgarh. Non-integrated producers struggle to pass costs through, risking contract losses to vertically integrated rivals such as Arakawa Chemical, which sources more than half of its rosin from owned forestry units.

Stringent Environmental and Food-Additive Rules

EFSA’s 2023 rule limiting E 445 feedstock to two pine species raised traceability and testing costs by USD 50–80 per t[2]European Food Safety Authority, “E 445 Opinion,” efsa.europa.eu . Small and mid-size producers that previously blended multiple varieties must now invest in DNA testing and chain-of-custody audits, raising entry barriers. Similar scrutiny under the U.S. Food Safety Modernization Act and India’s FSSAI alignment with Codex standards compounds compliance costs, shaving off forecast CAGR through 2029.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: GEWR Dominates, PEGR Gains in Specialty Coatings

Glycerol esters of wood rosin (GEWR) secured 36.47% of ester gum market share in 2025 thanks to dual food and industrial approvals that simplify global sourcing. GEWR’s cost advantage over polymerized alternatives anchors its position, yet the ester gum market size for penta ester gum (PEGR) is projected to expand at a 6.74% CAGR as coatings formulators demand 110 °C–130 °C softening points that improve sag resistance in water-borne systems. The ester gum market size for polymerized rosins remains limited to high-temperature adhesives because the added polymerization step inflates unit cost by up to 20%. R&D investment is migrating toward hybrid rosin-terpene esters that fuse UV resistance with the tackifying strength of glycerol esters, a path highlighted by Eastman and Kraton patent filings in 2024-2025.

PRGE and GEGR together remain entrenched in automotive refinish coatings and premium gum bases, respectively. Experimental “other types,” including maleic-modified and hybrid resins, are poised for above-average growth as PSA formulators pay premiums for resins that eliminate separate UV stabilizers.

By Application: Beverages Drive Volume, Coatings Lead Growth

Food and beverages held 34.28% of ester gum market size in 2025 after the North American BVO ban moved 8 000–10 000 t of annual demand to GEWR. Yet paints, inks and coatings are set to outpace the overall ester gum market at a 6.68% CAGR through 2031 on the back of Asia-Pacific construction expansion and Europe’s 2028 VOC limits. Adhesives represented moderate usage, propelled by e-commerce packaging volumes that grew 11-13% per year in India, Indonesia, and Vietnam. Cosmetics are advancing as clean-beauty labels adopt glyceryl rosinate, benefitting from its FDA food-contact approval and clean-label eligibility. Other applications deliver steady low-single-digit growth, supported by procurement policies that prioritize bio-based inputs.

Geography Analysis

Asia-Pacific captured 48.36% of ester gum market share in 2025 and is projected to grow at a 6.74% CAGR through 2031 as China supplies over 60% of global rosin and builds localized esterification capacity. India’s demand is accelerating due to beverage reformulation and a surge in packaging adhesives tied to booming e-commerce logistics. Japan and South Korea pay premiums for specialty low-color or high-softening-point grades, reinforcing margins for regional producers such as Arakawa Chemical. Southeast Asian joint ventures allow Chinese firms to bypass tariff risk and shorten lead times.

North America’s demand is anchored by beverage reformulation and bio-based hot-melt adhesives. Eastman Chemical and Ingevity dominate through vertical integration and established customer ties. Mexico acts as a re-export platform under USMCA rules, shipping USD 27.2 million of ester gum in 2023 to the United States, Turkey, and Poland. Europe faces margin pressure from imported feedstock and stringent EFSA compliance, yet gains from leadership in low-VOC coatings that target green-building certifications.

In South America, Brazil’s biodiesel-driven glycerol surplus could enable backward integration, though limited rosin supply keeps the region a net importer. Vision 2030 infrastructure projects in Saudi Arabia and the UAE spur adhesive and coating demand, while government procurement favors bio-based inputs, helping the ester gum market penetrate new verticals.

Competitive Landscape

The top five suppliers - Arakawa Chemical, Eastman Chemical, Ingevity, Kraton, and DSM-Firmenich - held an estimated 66% of global revenue in 2025, leaving room for regional specialists in China and India. Feedstock integration shields margins; Arakawa Chemical sources more than 50% of its rosin internally, while Ingevity leverages pine-chemicals operations in the US Southeast. Regulatory agility is equally decisive as early EFSA or FDA approvals secure premium beverage contracts. Formulation tailoring remains the third axis of competition, with suppliers adjusting acid value, softening point, and Gardner color to match specific adhesive or coating chemistries.

Patent filings reveal an industry shift toward hybrid rosin-terpene esters that combine tack and UV resistance. Eastman’s 2025 USPTO application describes a maleic-anhydride-modified GEWR that bonds to polyethylene, targeting flexible packaging. Kraton’s filing covers a rosin-polyterpene blend that eliminates the need for separate UV stabilizers in PSA formulas. Biodiesel refiners are exploring backward integration to monetize surplus glycerol, a potential new layer of competition that could compress margins for non-integrated players.

Ester Gum Industry Leaders

Eastman Chemical Company

Arakawa Chemical Industries,Ltd.

dsm-firmenich

Kraton Corporation

Ingevity Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The U.S. International Trade Commission (USITC or Commission) initiated an investigation into certain glycerol esters of rosin and their packaging. This is expected to impact the ester gum market by creating uncertainties and influencing trade dynamics.

- March 2024: Grupo RB acquired Pinopine, a Portuguese producer of gum rosin derivatives. This acquisition impacted the ester gum market by strengthening RB's position in the supply chain and enhancing its product portfolio to meet growing demand.

Global Ester Gum Market Report Scope

Ester gum is a resin produced through the esterification of esters with gum rosin. This substance is formed by combining esters, which are chemical compounds, with gum rosin, a natural resin obtained from pine trees. Ester gum possesses adhesive and binding properties, making it valuable in industrial applications. While its detailed uses can differ across sectors, the fundamental nature of ester gum involves its formation through the chemical reaction of esters and gum rosin.

The ester gum market is segmented by type, application, and geography. By type, the market is segmented into Glycerol Esters of Wood Rosin (GEWR), Polymerized Rosins of Glycerol Ester (PRGE), Glycerol Esters of Gum Rosins (GEGR), Penta Ester Gum (PEGR), and other types. By application, the market is segmented into food and beverages, paints, inks, and coatings, adhesives, cosmetics, and other applications. The report also covers the market size and forecasts for ester gum in 24 countries across major regions. For each segment, market sizing and forecasts are provided based on value (USD).

| Glycerol Esters of Wood Rosin (GEWR) |

| Polymerized Rosins of Glycerol Ester (PRGE) |

| Glycerol Esters of Gum Rosins (GEGR) |

| Penta Ester Gum (PEGR) |

| Other Types |

| Food and Beverages |

| Paints, Inks and Coatings |

| Adhesives |

| Cosmetics |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Nigeria | |

| Egypt | |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Type | Glycerol Esters of Wood Rosin (GEWR) | |

| Polymerized Rosins of Glycerol Ester (PRGE) | ||

| Glycerol Esters of Gum Rosins (GEGR) | ||

| Penta Ester Gum (PEGR) | ||

| Other Types | ||

| By Application | Food and Beverages | |

| Paints, Inks and Coatings | ||

| Adhesives | ||

| Cosmetics | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the Ester Gum market?

The Ester Gum market size stands at USD 348.78 million in 2026 and is projected to reach USD 479.21 million by 2031, at a CAGR of 6.56%.

What factors drove the ester gum market size past USD 340 million in 2026?

Regulatory replacement of BVO, bio-based adhesive demand, and stricter VOC limits in coatings together lifted sales to USD 348.78 million in 2026.

How will Asia-Pacific influence future demand?

Asia-Pacific holds 48.36% share and should maintain a 6.74% CAGR because China supplies low-cost rosin while regional construction and beverage markets expand.

Why are beverages a key application despite slower growth?

The 2024 BVO ban forced nearly universal GEWR adoption in citrus drinks, making beverages the single largest volume consumer even as coatings grow faster.

Page last updated on: