Sugar Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

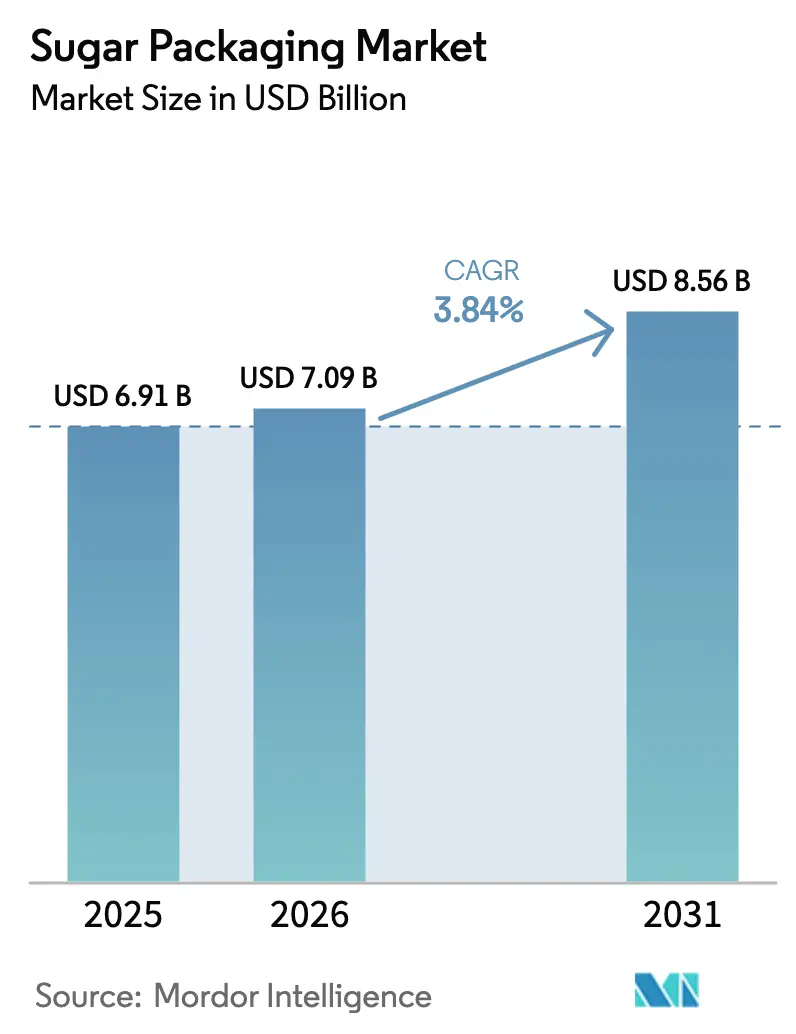

| Market Size (2026) | USD 7.09 Billion |

| Market Size (2031) | USD 8.56 Billion |

| Growth Rate (2026 - 2031) | 3.84% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sugar Packaging Market Analysis by Mordor Intelligence

The sugar packaging market size was valued at USD 6.91 billion in 2025 and is estimated to grow from USD 7.09 billion in 2026 to reach USD 8.56 billion by 2031, at a CAGR of 3.84% during the forecast period (2026-2031). Converters are pivoting away from commodity polypropylene sacks toward bio-based, high-barrier formats that protect free-flowing crystals in humid climates and simplify compliance with Extended Producer Responsibility rules, especially in Europe and much of the Asia-Pacific. Flexible formats dominate because stand-up pouches and single-serve sachets support e-commerce dimensional-weight economics and enhance shelf presentation in brick-and-mortar outlets. At the same time, blockchain-linked QR codes and nutrient-stable multi-layer films are transforming packaging from a passive cost center into a visible quality and safety differentiator for premium sugars.

Key Report Takeaways

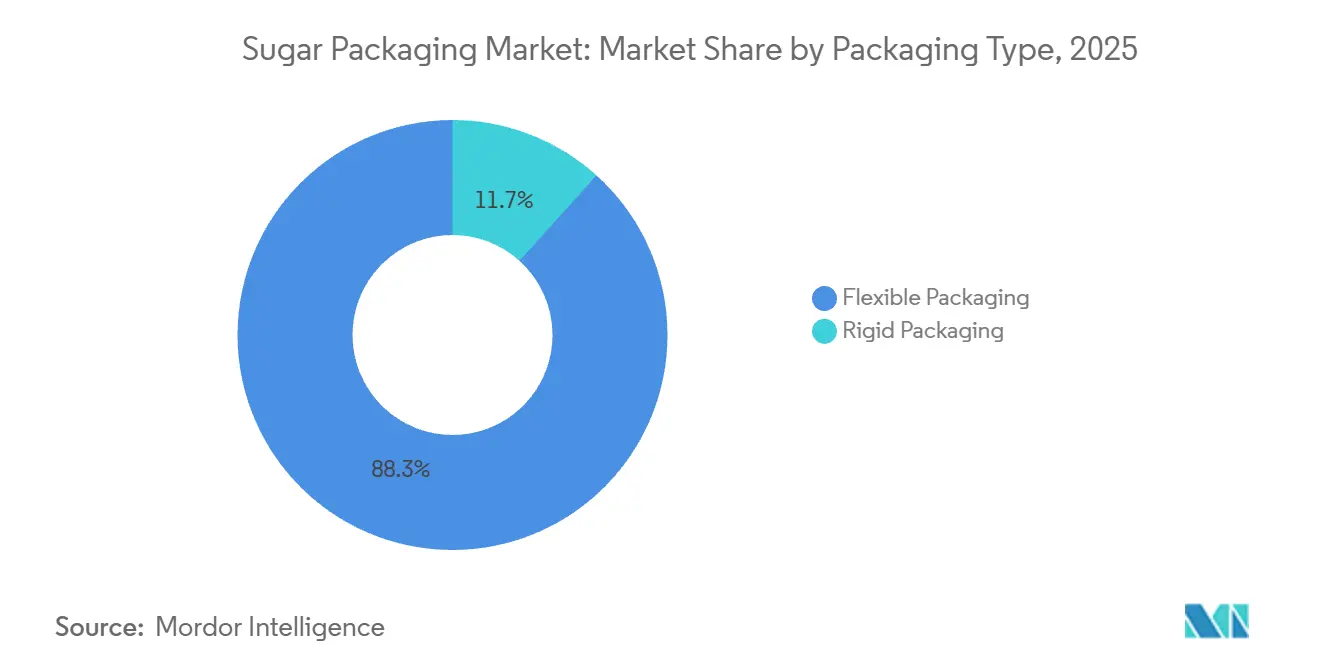

- By packaging type, flexible formats led with 88.32% sugar packaging market share in 2025, and are forecast to grow at a slower 4.62% CAGR through 2031.

- By material type, plastic retained 68.97% of the sugar packaging market size in 2025, while bio-based and compostable substrates are projected to expand at a 5.22% CAGR to 2031.

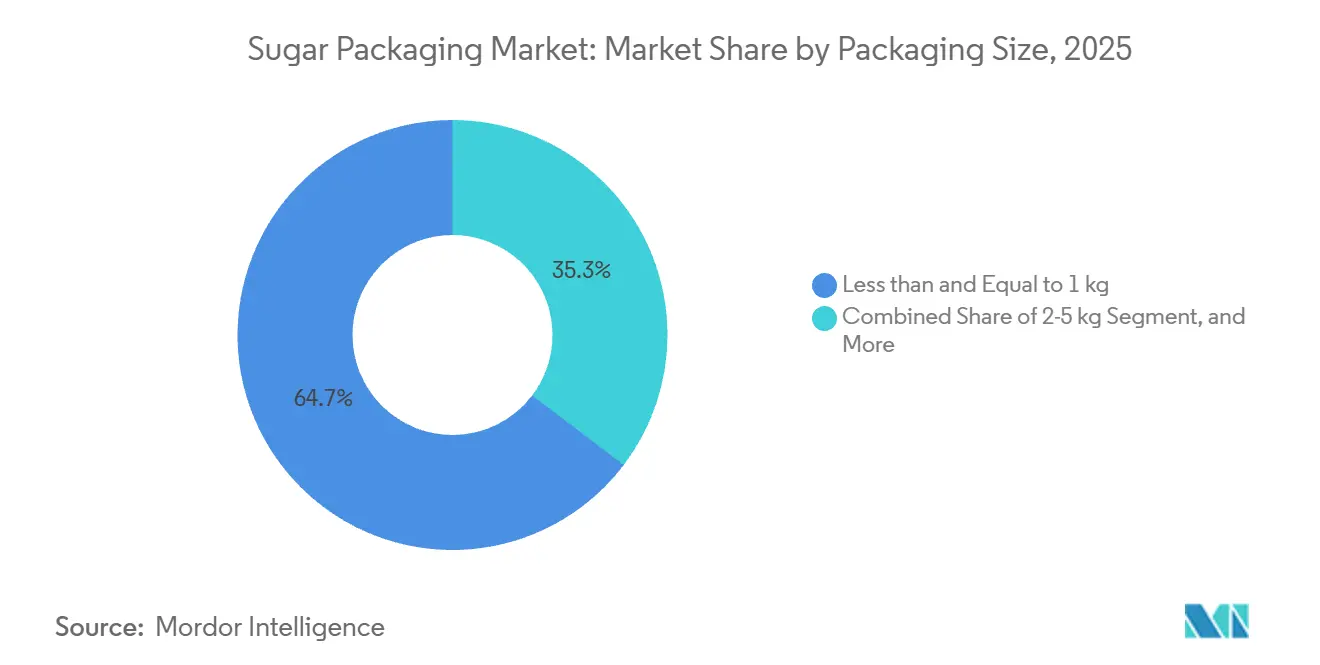

- By packaging size, ≤1 kilogram packs commanded 64.67% of the sugar packaging market in 2025, whereas 2-5 kilogram formats had the fastest growth outlook at a 4.76% CAGR.

- By end user, large scale Manufacturers accounted for 58.65% of the market share in 2025, and small scale manufacturers advanced at a 4.98% CAGR through 2031.

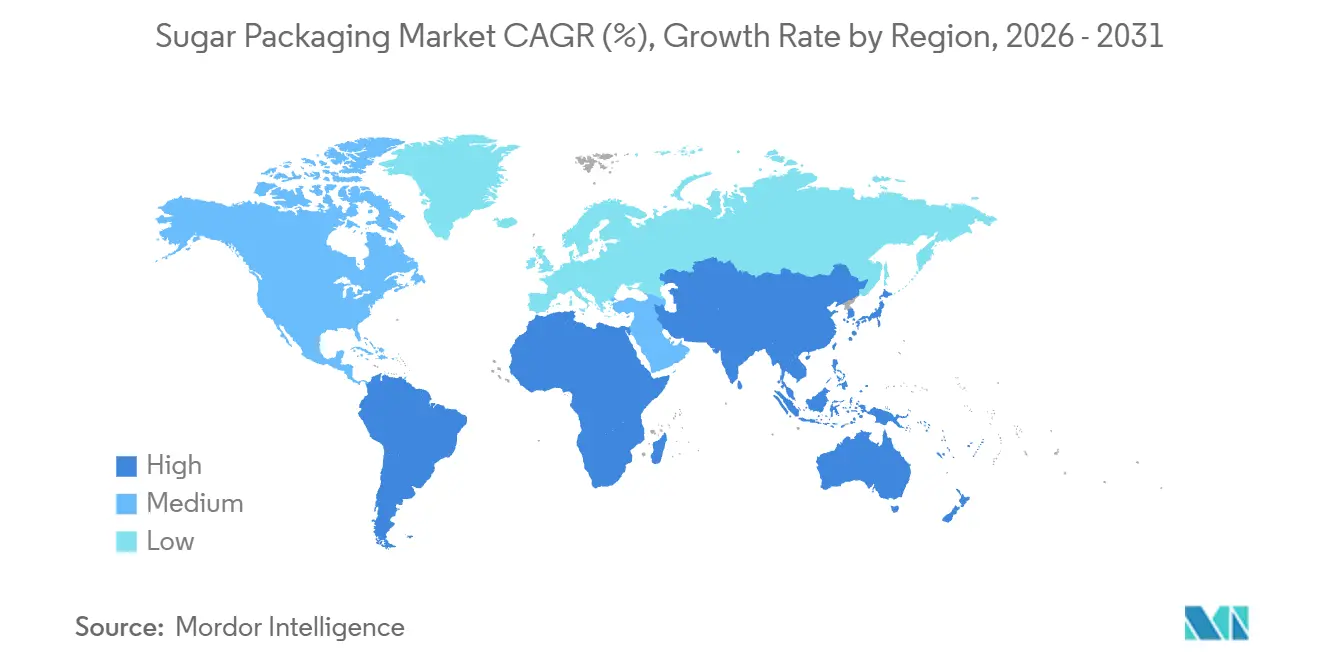

- By geography, Asia-Pacific accounted for 40.21% of market share in 2025; the Middle East and Africa region presents the strongest upside, advancing at a 5.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sugar Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steady Increase in Sugar Consumption in Emerging Economies | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Rising Demand for Customized and Sustainable Packaging Formats | +1.0% | Global, with early gains in Europe and North America | Long term (≥ 4 years) |

| Growth of E-commerce Fueling Unit-Sized Sugar Packs | +0.8% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Blockchain-Enabled Supply Chain Traceability for Premium Sugars | +0.4% | North America, Europe, premium segments in Asia-Pacific | Medium term (2-4 years) |

| Mandatory Sugar-Fortification Programs Requiring Specialized Packs | +0.6% | India, sub-Saharan Africa, select Middle East markets | Long term (≥ 4 years) |

| Adoption of Biodegradable High-Barrier Films in Humid Regions | +0.7% | Southeast Asia, Brazil, coastal Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Steady Increase in Sugar Consumption in Emerging Economies

Per-capita intake in India climbed to 20.1 kilograms in 2025, and similar gains appeared in Indonesia and Vietnam, lifting baseline demand for both bulk sacks and retail pouches.[1]International Sugar Organization, “Quarterly Market Outlook,” ISOSUGAR.ORG The 2–5 kilogram bracket benefits most because household shopping trips in these markets balance price sensitivity with storage constraints. In China, organic and specialty sugars represented 8% of consumption in 2025, requiring tamper-evident, resealable packs that justify price premiums. Southeast Asia’s net imports rose 4.2% year-on-year, further expanding volumes through flexible formats that withstand tropical humidity. Altogether, heightened regional consumption is a direct growth engine for the sugar packaging market.

Rising Demand for Customized and Sustainable Packaging Formats

The European Union’s Packaging and Packaging Waste Regulation, fully enforced in 2025, compels 65% recyclability or compostability by 2030, steering converters toward mono-material polyethylene and polylactic acid substrates. Mondi reported that bio-attributed resins reached 42% of its food-flexible mix in 2025, up sharply from 28% two years earlier.[2]Mondi plc, “Sustainability Report 2025,” MONDIGROUP.COM Brands are also embracing single-serve sachets with tear notches, resealable zippers, and laser scoring for portion control, all of which heighten shelf appeal. Amcor’s AmLite family, introduced mid-2025, cut film gauge by 15% yet preserved barrier performance via nano-clay coatings, lowering carbon intensity and shipping weight. [3]Amcor plc, “AmLite Product Launch and Sustainability Initiatives,” AMCOR.COM These design shifts keep the sugar packaging market on a path of premiumization, even as raw material prices fluctuate.

Growth of E-commerce Fueling Unit-Sized Sugar Packs

United States online grocery penetration reached 14.3% of food and beverage sales in 2025, with sugar and sweeteners among the top twenty categories by purchase frequency. E-commerce platforms favor ≤ 1-kilogram pouches because they fit dimensional-weight algorithms and withstand automated sortation. Amazon’s private-label sugar range shifted entirely to stand-up pouches with reinforced corners, decreasing damage claims and optimizing shelf presentation. In Europe, Ocado’s 2025 guidelines mandated a 1.2-meter drop-test threshold, pushing suppliers toward thicker laminates that resist puncture. The e-commerce driver, therefore, dictates both format choice and substrate engineering in the sugar packaging market.

Blockchain-Enabled Supply Chain Traceability for Premium Sugars

Tate and Lyle embedded QR-linked blockchain records on 1-kilogram pouches in late 2025, enabling consumers to verify farm origin, milling time stamps, and organic certification in seconds. IBM Food Trust data show recall response times drop by 60% once lot-level traceability is digitized, saving cost and limiting brand damage. Gulf Cooperation Council import authorities are piloting mandatory blockchain documentation to curb counterfeit shipments, elevating traceability from an optional added value to a regulatory prerequisite. Technology, therefore, is reshaping the sugar packaging market by linking physical packs to immutable data ecosystems valued by regulators and consumers alike.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Operational and Regulatory Compliance Costs for Converters | -0.9% | Europe, North America, select Asia-Pacific markets | Short term (≤ 2 years) |

| Volatility in Global Sugar Prices Impacting Packaging Demand | -0.6% | Global, with acute effects in import-dependent regions | Short term (≤ 2 years) |

| Shift Toward Alternative Sweeteners Reducing Per-Capita Sugar Use | -0.7% | North America, Western Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Extended Producer Responsibility (EPR) Increasing Packaging Costs | -0.5% | European Union, United Kingdom, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Operational and Regulatory Compliance Costs for Converters

Extended Producer Responsibility fees averaged EUR 0.12 per kilogram (USD 0.13) of plastic packaging in France, Germany, and the Netherlands during 2025, squeezing converter margins and raising shelf prices by 3–5%. Smaller converters unable to absorb these charges exited commodity contracts, prompting some supply chain consolidation. New recyclability testing rules add EUR 8,000–EUR 15,000 (USD 8,500–USD 16,000) per SKU, an upfront burden that lengthens payback periods for new film constructions. Varying standards in Canada and Asian markets complicate inventory management and duplicate testing. The result is a drag on expansion plans, especially for mid-size firms, within the sugar packaging market.

Shift Toward Alternative Sweeteners Reducing Per-Capita Sugar Use

United States refined-sugar intake fell to 22.1 kilograms per capita in 2025 as stevia and monk-fruit blends captured 11% of household sweetener volume. Germany charted a 6.8% drop in retail sugar purchases between 2023 and 2025 as zero-calorie options gained shelf space. Less throughput in mature markets reduces absolute demand for standard 1-kilogram packs and industrial sacks. Surviving volume is skewing toward high-margin, specialty sugars that require sophisticated barrier films, partially offsetting the decline but adding complexity and cost for converters. This substitution trend softens top-line growth for the sugar packaging market in advanced economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Flexible Formats Sustain Dominance Through Resealability

Flexible solutions accounted for 88.32% of the sugar packaging market in 2025 and are expanding at a 4.62% CAGR through 2031. Bags and pouches drive volume, yet sachets are steadily gaining share in quick-service restaurants and hospitality channels. Rigid containers remain niche, catering to premium organic sugars and foodservice dispensers where clarity and reuse offset higher shipment costs. Sealed Air’s recyclable polyethylene pouch with an integrated degassing valve prevents ballooning in humid climates, reducing retailer returns and validating the format’s premium positioning. In contrast, sacks are ceding space to intermediate bulk containers where automated handling favors rigid formats, underscoring how material handling innovation influences the trajectory of the sugar packaging market.

Rigid packaging’s lower 3.1% CAGR stems from concentration in mature markets and consumer price sensitivity, yet glass jars are enjoying a limited revival in European organic channels associating transparency with purity. Flexible formats, however, are likely to retain leadership because lightweighting, resealable features, and omnichannel durability remain highly valued by retailers and consumers alike. Consequently, the sugar packaging market is expected to see continued investment in film science and closure innovation.

By Material Type: Bio-Based Substrates Gain Despite Cost Gap

Plastic retained 68.97% sugar packaging market share in 2025, split between woven polypropylene for bulk and multilayer laminates for retail. Yet bio-based and compostable substrates are growing fastest at 5.22% CAGR, driven by retailer scorecards and consumer sustainability preferences. Paper packaging also edges higher as kraft pouches with biodegradable liners satisfy both visual and environmental expectations, especially in European premium segments. Billerud’s grease-resistant laminate passed EU Regulation 10/2011, demonstrating that paper can meet safety standards without plastics, though price premiums keep adoption selective.

Smurfit WestRock’s joint venture with GranBio aims to commercialize bagasse-derived polyethylene at scale, targeting cost parity with fossil-based resin by 2029. Until then, polyethylene and polypropylene films will dominate because they deliver proven moisture barriers at lower weights, minimizing logistics costs. Nonetheless, retailer mandates suggest that bio-based films will capture incremental share, sustaining innovation demand within the sugar packaging industry.

By Packaging Size: Unit Packs Lead, Mid-Range Accelerates

Packs of 1 kilogram or less accounted for 64.67% of market share in 2025, reflecting urban storage constraints and rising e-commerce demand. The 2–5 kilogram tier grows fastest at 4.76% CAGR through 2031 as warehouse clubs proliferate in North America and household sizes remain large in India, Indonesia, and Nigeria. E-commerce continues to reinforce unit packs; Glenroy recorded a 40% drop in transit damage when a leading U.S. brand switched from pillow bags to quad-seal pouches with reinforced corners.

Meanwhile, the 5–25 kilogram bracket retains relevance in bakeries and small food plants, and formats above 25 kilograms stay entrenched in industrial channels. Retailers in emerging economies allocate more shelf space to 2–5 kilogram pouches, encouraging graphic differentiation and functional add-ons like carry handles. This balanced-size portfolio supports broad-based growth across the sugar packaging market.

By End User: Small-Scale Manufacturers Outpace Incumbents

Large-scale manufacturers accounted for 58.65% of market share in 2025, yet grew more slowly than agile small-scale competitors, which grew at a 4.98% CAGR. Direct-to-consumer channels, localized sourcing, and storytelling via QR codes are propelling small brands. TedPack’s digital printing cuts minimum orders to 5,000 units, lowering barriers for artisanal producers. Large players counter with AI-enabled quality control and material lightweighting, reducing defects by 18% and protecting margins at high volumes.

The bifurcation reflects how the sugar packaging market combines a commodity tier driven by scale and a premium tier driven by customization and traceability. Packaging innovation provides the bridge that allows newcomers to command shelf presence even against entrenched incumbents. This dynamic has led to increased competition and a focus on differentiation within the market.

Geography Analysis

Asia-Pacific held 40.21% of the market share in 2025 and is expected to grow at an estimated 4.1% CAGR through 2031. India’s mandated iron-fortified sugar program drives demand for high-barrier films, while China’s blockchain adoption in premium segments differentiates products on safety credentials. Southeast Asia is transitioning rapidly from loose bulk to retail packs as urbanization accelerates. Japan’s aging demographics are pushing brands to engineer easy-open closures and smaller formats, underscoring diverse regional needs that are expanding the sugar packaging market.

The Middle East and Africa region posts the highest forecast at 5.32% CAGR. Saudi Arabia enforces tamper-evident packaging on imports, spurring holographic labels and breakable seals that local converters often cannot supply, thereby opening export opportunities for European and Asian suppliers. Nigeria’s sugar consumption reached 1.8 million metric tons in 2025, but domestic packaging capacity trails demand, promoting foreign investment. Currency volatility, such as Egypt’s 2025 devaluation, alters substrate choices, favoring lower-cost paper sacks in industrial channels and reshaping the sugar packaging market across the region.

In Europe, growth is muted by declining sugar use but buoyed by sustainability mandates. Germany raised EPR fees on non-recyclable packs, accelerating the switch to mono-material polyethylene. France’s ban on single-use plastic sachets creates uncertainty, prompting brands to hedge with paper alternatives. Closed-loop recycling pilots in Spain and Italy demonstrate the potential of the circular economy but depend on multi-stakeholder coordination. Regulatory complexity, therefore, defines the European outlook for the sugar packaging industry.

In North America, the United States relies on e-commerce to stimulate unit-pack demand, whereas Canada’s draft EPR proposal diverges from U.S. rules, complicating cross-border compliance. Mexico’s exporters use higher-barrier laminates to meet U.S. retailer shelf-life requirements. Overall, innovation skewed to resealability and graphics delivers incremental value in this mature part of the sugar packaging market.

South America is expected to be one of the growing regions, powered by Brazil’s sugarcane-derived polyethylene supply and Argentina’s stabilization of input costs. Mercosur tariff cuts on packaging materials cut production costs and encourage cross-border integration. Urban consumers in São Paulo and Buenos Aires increasingly prefer resealable pouches, while rural retail still leans on low-cost sacks. As bio-polymer capacity climbs, South America could become an exporting hub for sustainable inputs used worldwide in the sugar packaging market.

Competitive Landscape

The sugar packaging market is fragmented, with global players including Mondi, Amcor, Smurfit Westrock, Sealed Air, International Paper, and others. These leaders expand vertically into bio-polymer production, pursue regional acquisitions, and invest in barrier-coating patents that enable fully recyclable structures. Mondi’s water-based oxygen barrier, patented in 2025, shows oxygen-transmission rates below 1 cc/m²/day without aluminum or EVOH layers, promising greater recyclability once scaled. Amcor’s USD 180 million purchase of a Brazilian converter secures sugarcane-based polyethylene feedstock, illustrating how mergers combine capacity and sustainable inputs.

Technology collaborations also drive differentiation. Sealed Air tailored its coffee-grade degassing valve to humid-market sugar packs, cutting packaging failures by one-third. International Paper’s AI vision systems cut defects across containerboard destined for industrial sugar applications. Smaller digital printing specialists cater to artisanal brands by slashing minimum order sizes, earning quick traction among e-commerce-focused producers. Certification breadth, spanning EU, FDA, and BIS standards, increasingly separates preferred suppliers from competitors in the sugar packaging industry.

Mid-size converters in India, Thailand, and Brazil fill critical regional gaps by offering multilingual artwork services, faster regulatory approvals, and order-to-ship cycles under ten days, a speed unattainable for the global majors that rely on centralized plants. Several of these firms are licensing digital-holography modules to embed low-cost tamper evidence directly into pouch side gussets, thereby competing on functionality rather than scale. Private-equity funds have begun rolling up such regional assets five deals closed in 2025 alone to create sub-continental champions able to negotiate resin contracts collectively and qualify for multinational tenders that require ISO 22000 and BRC certification. Meanwhile, specialty coating start-ups in the United States are partnering with large resin suppliers to commercialize solvent-free nano-barrier layers that can be extruded in a single pass, reducing energy consumption by 22% compared with legacy aluminum-oxide vapor-deposition systems. This convergence of speed, niche technology, and financial backing suggests that the next competitive wave will be defined less by absolute capacity and more by the ability to integrate advanced materials, digital security, and agile production into one cohesive service offering, further diversifying the global sugar packaging landscape.

Sugar Packaging Industry Leaders

Mondi Group

Smurfit WestRock

Amcor plc

Sealed Air Corporation

International Paper Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Mondi plc confirmed a EUR 120 million (USD 128 million) expansion of bio-based barrier-film capacity in Germany, aiming to boost output by 25,000 metric tons annually.

- November 2025: Amcor plc closed a USD 180 million deal for Embalagens São Paulo, adding three Brazilian plants and securing bio-polymer supply under a five-year offtake contract.

- October 2025: Smurfit Westrock and GranBio launched a USD 240 million joint venture to build a 60,000 metric-ton facility producing bagasse-derived polyethylene in São Paulo, Brazil.

- September 2025: Sealed Air Corporation debuted its ProActive recyclable pouch with degassing valve, recording a 35% reduction in retailer returns after Indonesian field tests.

Global Sugar Packaging Market Report Scope

Sugar packaging is available in various formats in bulk production and retail. There are many sugar packaging products on the market. The sugar packaging market is witnessing a significant shift in favor of flexible packaging formats. The market for the study defines the revenue generated from the sales of various products made up of different materials such as paper, plastic, and more across various regions around the globe. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of Sugar Packaging Materials in terms of drivers and restraints.

The Sugar Packaging Market Report is Segmented by Packaging Type (Flexible Packaging, and Rigid Packaging), Material Type (Plastic, Paper, and Bio-based and Compostable Materials), Packaging Size (≤1 kg, 2-5 kg, 5-25 kg, and >25 kg), End User (Large Scale, Medium Scale, and Small Scale Manufacturers), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Flexible Packaging | Bags and Pouches |

| Sachets | |

| Sacks | |

| Rigid Packaging | Jars and Containers |

| Plastic | Woven Polypropylene |

| Plastic Films | |

| Paper | |

| Bio-based and Compostable Materials |

| Less than equal to 1 kg |

| 2 - 5 kg |

| 5 - 25 kg |

| More than 25 kg |

| Large Scale Manufacturers |

| Medium Scale Manufacturers |

| Small Scale Manufacturers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia -Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Type | Flexible Packaging | Bags and Pouches | |

| Sachets | |||

| Sacks | |||

| Rigid Packaging | Jars and Containers | ||

| By Material Type | Plastic | Woven Polypropylene | |

| Plastic Films | |||

| Paper | |||

| Bio-based and Compostable Materials | |||

| By Packaging Size | Less than equal to 1 kg | ||

| 2 - 5 kg | |||

| 5 - 25 kg | |||

| More than 25 kg | |||

| By End User | Large Scale Manufacturers | ||

| Medium Scale Manufacturers | |||

| Small Scale Manufacturers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia -Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the sugar packaging market by 2031?

It is expected to reach USD 8.56 billion as converters shift toward bio-based, high-barrier formats.

Which region is forecast to grow fastest?

The Middle East and Africa region shows the highest outlook at a 5.32% CAGR through 2031 due to tamper-evident mandates and rising consumption.

Why are flexible pouches preferred in e-commerce channels?

Stand-up pouches minimize dimensional weight, resist automated sortation damage, and fit consumer expectations for resealability.

How are sustainability regulations influencing packaging materials?

EU and Canadian EPR frameworks require higher recyclability, pushing converters toward mono-material polyethylene, bio-based films, and recyclable paper laminates.

What role does blockchain play in sugar packaging?

QR-linked blockchain records enhance traceability, reduce recall times by 60%, and strengthen consumer trust for premium organic sugars.

Which packaging size segment is expanding fastest?

The 2–5 kilogram bracket is growing at 4.76% CAGR because it balances bulk economics with household convenience in emerging markets.

Page last updated on: