Oncology Information System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

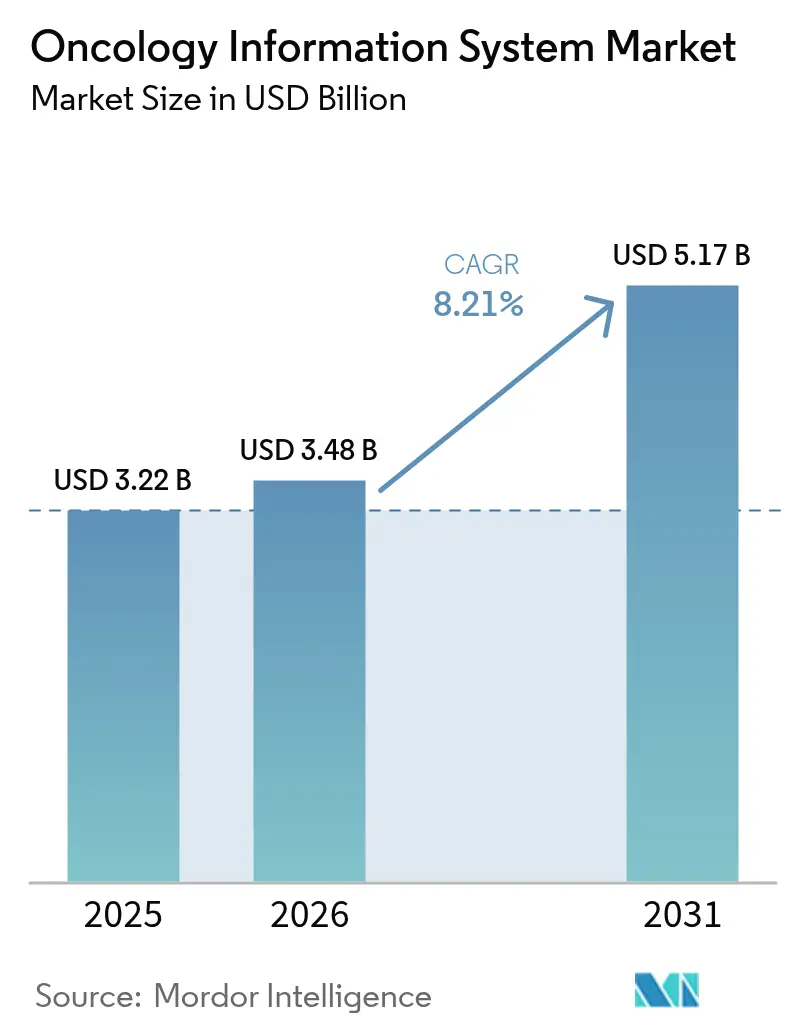

| Market Size (2026) | USD 3.48 Billion |

| Market Size (2031) | USD 5.17 Billion |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oncology Information System Market Analysis by Mordor Intelligence

The oncology information system market size is expected to grow from USD 3.22 billion in 2025 to USD 3.48 billion in 2026 and is forecast to reach USD 5.17 billion by 2031 at 8.21% CAGR over 2026-2031. The market’s current momentum is underpinned by the sharp rise in global cancer incidence, interoperability mandates such as the 21st Century Cures Act, and rapid integration of artificial intelligence into clinical workflows. Providers are deploying sophisticated platforms to manage complex, multimodality treatment plans, reduce costs, and improve outcomes through data-driven decision support. Hospitals benefit from economies of scale that enable enterprise-wide rollouts, while oncology clinics leverage cloud-hosted offerings to meet value-based reimbursement requirements. The oncology information system market is further shaped by large capital investments—more than USD 4 billion in acquisitions in 2024–2025—and by escalating cybersecurity threats that underscore the need for resilient, compliant architectures.

Key Report Takeaways

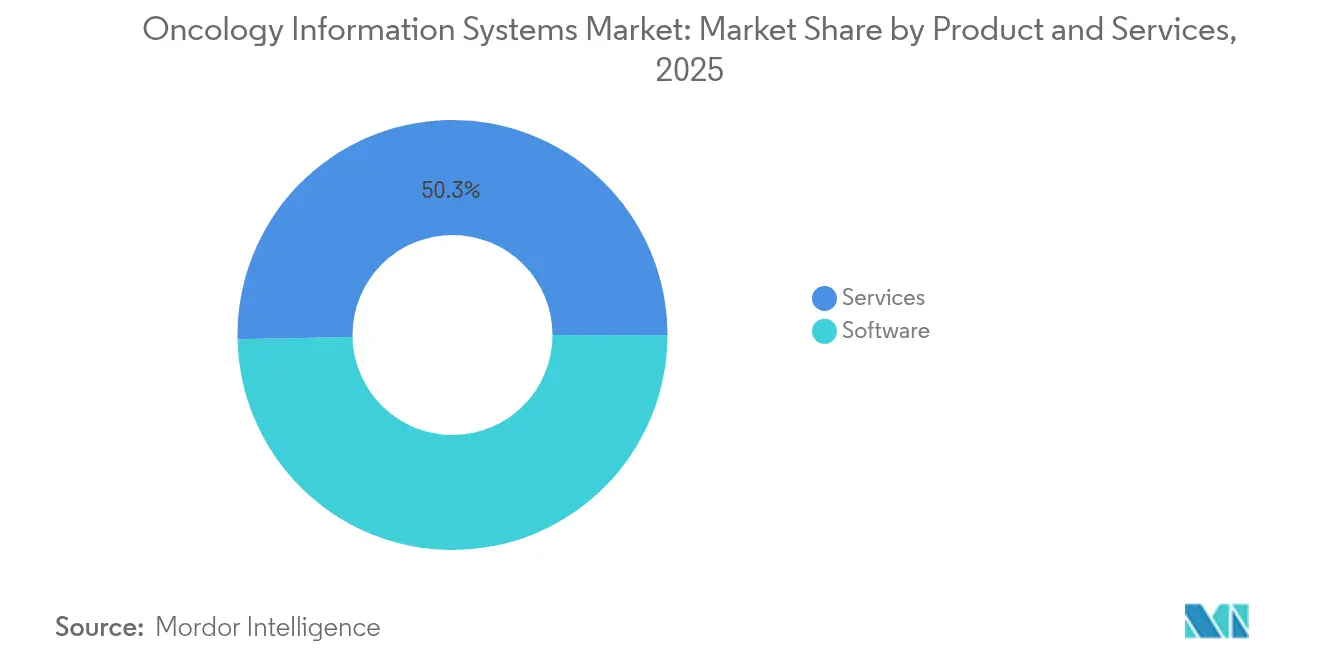

- By product & service, services led with 50.32% of oncology information system market share in 2025; software solutions are projected to expand at an 8.74% CAGR to 2031.

- By application, medical oncology accounted for 47.10% of the oncology information system market size in 2025, while radiation oncology is advancing at a 8.83% CAGR through 2031.

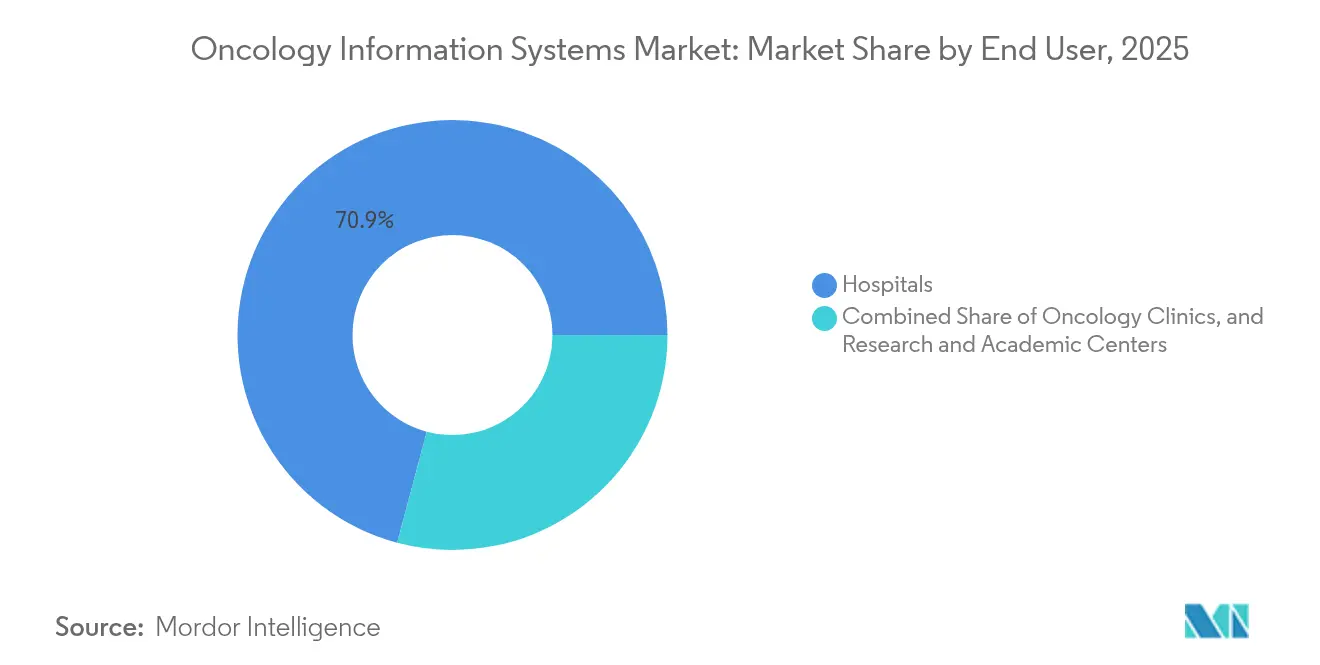

- By end user, hospital systems held 70.86% revenue share in 2025; oncology clinics record the highest forecast CAGR at 9.05% during 2026–2031.

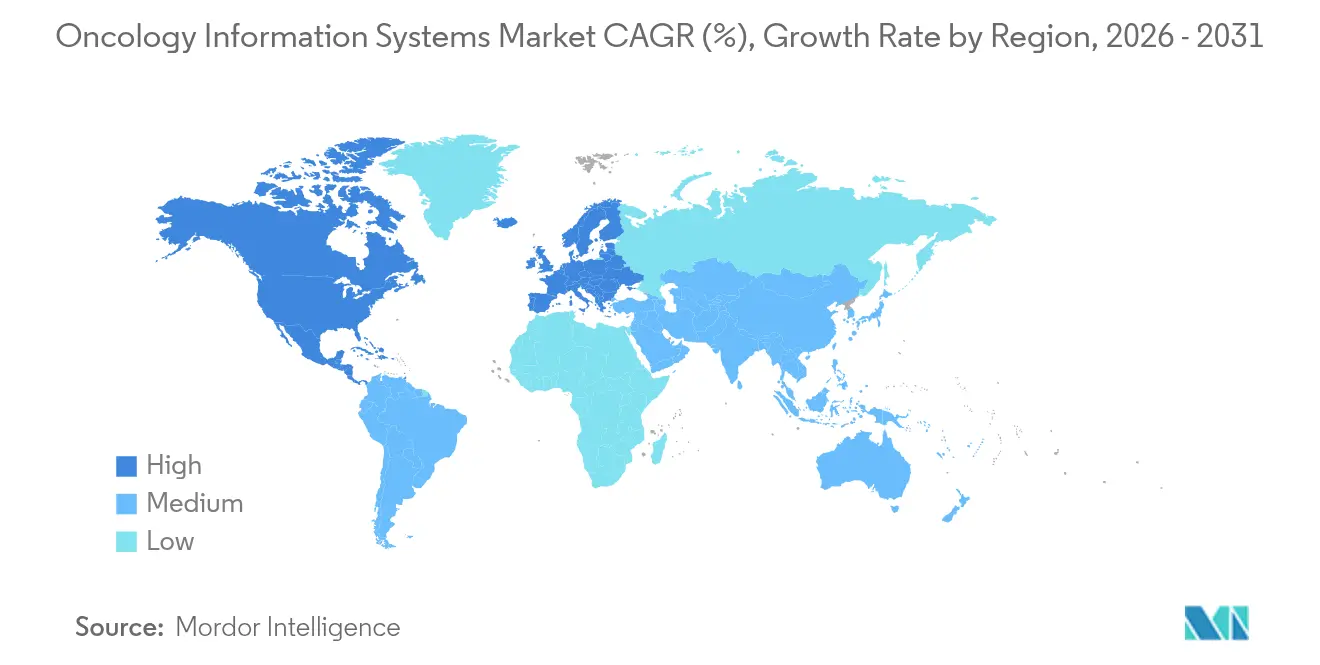

- By geography, North America dominated with 44.78% share of the oncology information system market in 2025; Asia-Pacific is on track for a 9.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oncology Information System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of cancer worldwide | +2.1% | Global | Long term (≥ 4 years) |

| Government funding for oncology IT modernization | +1.8% | North America & EU | Medium term (2–4 years) |

| Interoperability mandates (21st Century Cures Act) | +1.5% | North America, expanding to EU | Short term (≤ 2 years) |

| Cloud-hosted OIS adoption across cancer networks | +1.3% | Global, APAC acceleration | Medium term (2–4 years) |

| AI-driven clinical decision support boosting ROI | +1.7% | North America & APAC core | Short term (≤ 2 years) |

| Value-based models demanding real-time tracking | +1.4% | North America, pilot programs in EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Cancer Worldwide

Global cancer burden continues to climb, with 1.7 million new cases diagnosed each year in the United States alone, placing unprecedented demands on data management and care coordination [1]Roberto Casale, “Predicting Risk of Metastases and Recurrence in Soft-Tissue Sarcomas via Radiomics and Formal Methods,” JAMIA Open, academic.oup.com. Oncology workflows now incorporate genomic sequencing, multi-modal imaging, and real-world evidence, all of which require an integrated platform capable of supporting personalized medicine. Improved survival rates—up 33% over three decades—have created a growing cohort of cancer survivors who need long-term monitoring, further stretching information infrastructure [2]Xue Qin Yu, “Crude Probability of Death for Cancer Patients by Spread of Disease in New South Wales, Australia 1985 to 2014,” Cancer Medicine, onlinelibrary.wiley.com. Demographic shifts toward aging populations amplify these pressures, pushing healthcare organizations to scale oncology information system market deployments that support multidisciplinary teams and lifelong care pathways.

Government Funding for Oncology IT Modernization

Public-sector investment is accelerating adoption of advanced cancer informatics. The United States Cancer Moonshot allocates targeted funds for standardized oncology data elements across electronic health records, while the CDC’s AIMS platform and NOAH hub bring real-time pathology and laboratory analytics to state cancer registries. New York State committed USD 188 million to hospital modernization, prioritizing integrated cancer programs. The United Kingdom set aside GBP 2 billion for Cancer 360 technology, creating unified oncology information layers across NHS institutions [3]United Kingdom Department of Health and Social Care, “Cancer 360 Investment,” gov.uk. Such initiatives tighten interoperability rules and stimulate private investment, reinforcing growth in the oncology information system market.

Interoperability Mandates (21st Century Cures Act)

The Cures Act final rule requires FHIR R4.0.1 APIs and USCDI compliance, compelling oncology vendors to expose standardized endpoints and eliminate information-blocking practices. Six major health-IT suppliers pledged USCDI+ Cancer support in 2024, unlocking granular data exchange that spans pathology, genomics, and treatment response. Oncology practices now automate data submissions for clinical trials and quality metrics, replacing slow manual uploads. Open API architectures therefore become a competitive differentiator across the oncology information system market.

AI-Driven Clinical Decision Support Boosting ROI

Artificial intelligence is proving its value in frontline cancer care. Microsoft’s agentic orchestrator, piloted at Stanford and Johns Hopkins, links radiology, pathology, staging, and guidelines agents inside existing collaboration suites, shortening tumor board prep times. Memorial Sloan Kettering leverages AWS to process vast imaging and genomic data for bespoke treatment plans. Ontada reports that AI-enabled natural language processing unlocks up to 80% of critical patient details buried in unstructured notes, transforming research and reimbursement workflows. GPT-4 models achieved 84% accuracy in interpreting oncology guidelines using retrieval-augmented generation, indicating tangible gains in evidence-based decision support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership & implementation | -1.9% | Global, pronounced in smaller practices | Short term (≤ 2 years) |

| Shortage of oncology-informatics professionals | -1.6% | North America & EU | Long term (≥ 4 years) |

| Cyber-security & patient-data-privacy risks | -1.2% | Global | Medium term (2–4 years) |

| Integration gaps with emerging proton-therapy data formats | -0.8% | Advanced treatment centers globally | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership & Implementation

Community oncology practices must weigh capital outlays against long-term savings. Mayo Clinic’s automated dose rounding study showed potential savings of USD 39.75 million over three years yet required sizable upfront investment for technology, training, and system maintenance. The Enhancing Oncology Model adds reporting and care-management obligations that strain smaller clinics. Cost-benefit frameworks underline non-financial gains—improved safety, fewer adverse events, and higher staff productivity—yet the cash flow challenge remains acute until reimbursement adjusts.

Shortage of Oncology-Informatics Professionals

The United States anticipates a shortfall exceeding 2,000 oncologists and hematologists by end-2025, with rural communities most affected. Demand for oncology services grew 40% from 2012 to 2025, but workforce supply rose only 25%. Training pipelines for data specialists are expanding through NAACCR and AHIMA programs, though results will take years to materialize. The scarcity of cancer informatics talent constrains configuration, optimization, and support for oncology information system market deployments, especially at smaller facilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Services Lead Implementation Complexity

Services held 50.32% of oncology information system market share in 2025 as hospitals and clinics relied on implementation partners for workflow mapping, system configuration, training, and ongoing support. Cardinal Health’s USD 1.1 billion purchase of Integrated Oncology Network illustrates how bundled professional services amplify adoption and stickiness for enterprise clients. The oncology information system market size for services is projected to expand in tandem with growing proton-therapy and CAR-T monitoring deployments that demand bespoke integrations.

Software is the fastest-growing component, tracking an 8.74% CAGR through 2031. GE HealthCare’s CareIntellect for Oncology consolidates treatment history and decision support into a single dashboard, cutting data-gathering time from hours to minutes. RaySearch Laboratories integrates plan-quality analytics into RayCare, showing how vendors differentiate on AI-enabled automation. Consulting, maintenance, and managed-service subsegments rise as providers outsource FHIR upgrades, cloud migrations, and cybersecurity hardening. The result is a blended revenue model in which software licensing and recurring services generate predictable cash flows across the oncology information system market.

By Application: Medical Oncology Dominance Faces Radiation Acceleration

Medical oncology commands 47.10% of the oncology information system market size, reflecting the complexity of systemic therapy scheduling, adverse-event monitoring, and longitudinal outcomes tracking. Platforms ingest laboratory values, biomarkers, and prior authorizations to streamline chemotherapy administration and reimbursement. Radiation oncology, however, posts the quickest trajectory at a 8.83% CAGR thanks to expanding proton-therapy centers and adaptive radiotherapy techniques that require precise data orchestration.

Clinical studies show pencil-beam scanning proton therapy with static apertures improved conformity index by 15.3% and reduced dose gradients by 17.6%, underscoring the need for real-time plan adjustment. Vendors such as Elekta embed MIM Software into treatment workflows, merging imaging, planning, and follow-up data. Surgical oncology applications are also integrating, enabling tumor boards to view pre-operative imaging, operative notes, and adjuvant therapy plans in one workspace. This convergence supports multidisciplinary care pathways critical to value-based models and cements broader platform uptake across the oncology information system market.

By End User: Hospital Systems Leverage Scale Advantages

Hospital systems represented 70.86% of revenue in 2025, deploying enterprise oncology platforms that span inpatient, outpatient, and research settings. Memorial Sloan Kettering, for instance, pairs AWS analytics with AI-assisted note-taking from Abridge to accelerate documentation and clinical research. Large networks negotiate favorable pricing, support service integration, and secure data-center redundancies, enhancing system reliability.

Oncology clinics, growing at 9.05% CAGR, pivot toward cloud-hosted solutions that reduce capital expenditure and comply with value-based initiatives. The American Oncology Network realized nearly USD 6 million in Medicare savings during its first Enhancing Oncology Model performance period by harnessing real-time dashboards for quality measures. Academic centers and community practices join consortia like OneOncology to access shared technical infrastructure and data science teams, demonstrating how affiliation strategies spread costs and extend advanced capabilities. Such dynamics foster widespread yet differentiated adoption across the oncology information system market.

Geography Analysis

North America accounted for 44.78% of oncology information system market share in 2025, supported by the Cures Act interoperability mandate, robust reimbursement mechanisms, and well-established electronic health record penetration. Federal programs such as the CDC’s data-modernization initiative accelerate real-time cancer surveillance, nudging providers toward cloud-first architectures. Academic centers partner with technology firms to pioneer AI solutions, reinforcing the region’s leadership stance.

Asia-Pacific is the fastest-growing region, projecting a 9.34% CAGR through 2031. China’s Trinity smart-hospital blueprint outlines standards for unified EMRs and smart services, positioning local health systems to leapfrog legacy architectures . South Korea’s K-CURE Public Cancer Library aggregates anonymized records for 2.26 million patients, while a USD 25 million government fund backs AI-driven drug discovery. Japan’s medical DX program builds a national information platform to unify patient data, and India’s All India Institute of Medical Sciences deploys AI image analytics to detect breast and ovarian cancers earlier. These coordinated efforts tighten standards, ease procurement, and seed demand across the oncology information system market.

Europe follows with pan-regional initiatives such as the European Cancer Imaging Initiative and JANE project, which create federated networks for imaging data and AI tool validation. Member states co-invest in cloud-based registries and shared analytics, encouraging vendors to certify FHIR readiness and GDPR compliance. Middle East & Africa and Latin America show incremental adoption, often through public-private partnerships that bundle tele-oncology, remote monitoring, and basic EMR upgrades as foundational steps toward a full oncology information system market rollout.

Competitive Landscape

Moderate consolidation defines the oncology information system market, with strategic acquisitions surpassing USD 4 billion since 2024. Cardinal Health’s USD 1.1 billion buyout of Integrated Oncology Network integrates practice management, analytics, and pharmacy services into a unified stack. McKesson invested USD 2.49 billion in Core Ventures to bolster data-driven oncology distribution, signaling that supply-chain players view informatics as a growth engine.

AI-centric innovation intensifies rivalry. GE HealthCare expands its radiation oncology suite with adaptive planning modules, while Oracle Health leverages a cloud-native foundation to render longitudinal oncology timelines inside Cerner Millennium. Emerging entrants target workflow gaps: Azra AI partners with ECG Management Consultants to blend tumor-finding algorithms with operational redesign, and Knowtex installs generative voice AI at Los Angeles Cancer Network to automate note creation. Standards-body projects such as the European Cancer Imaging Initiative favor open, federated platforms, prompting vendors to advertise compliance and plug-and-play data sovereignty.

White-space opportunities appear in advanced therapy tracking. Mayo Clinic’s outpatient CAR-T monitoring uses consumer tablets and Bluetooth devices to capture vitals remotely, illustrating future niches for specialized modules. Vendors that blend device connectivity, AI analytics, and regulatory reporting gain an edge as therapy complexity grows. Overall, the oncology information system market incentivizes scale, interoperability, and AI differentiation.

Oncology Information System Industry Leaders

Oracle Corporation

Siemens Healthineers AG (Varian Medical Systems)

Elekta AB

Koninklijke Philips N.V.

McKesson Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Microsoft introduced an agentic AI orchestrator for multidisciplinary cancer care, integrating radiology, pathology, staging, guideline, and trial agents within Microsoft Teams, now piloting at Stanford and Johns Hopkins.

- April 2025: Sun Nuclear acquired Oncospace to enhance cloud-based radiation oncology quality assurance across more than 6,000 cancer centers.

- May 2024: RaySearch Laboratories launched RayCare 2024A, certified interoperable with Varian TrueBeam linear accelerators version 3.0.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global Oncology Information System (OIS) market as all purpose-built software and related services that capture, store, and exchange oncology-specific clinical, administrative, and imaging data across treatment planning, delivery, and follow-up within hospitals, cancer centers, and research facilities. Systems connecting radiotherapy units, chemotherapy suites, and multidisciplinary EHR modules are included, while generic hospital IT, AI-only analytics platforms, and standalone imaging PACS are not.

Scope exclusions: generic electronic medical record modules lacking oncology workflows are outside scope.

Segmentation Overview

- Oncology

- Software

- Patient-information systems

- Treatment-planning systems

- Services

- Consulting

- Implementation & Integration

- Maintenance & Support

- Software

- By Application

- Medical Oncology

- Radiation Oncology

- Surgical Oncology

- By End User

- Hospitals

- Oncology Clinics

- Research & Academic Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed radiation oncologists, hospital CIOs, and regional health-IT distributors across North America, Europe, and Asia-Pacific. Discussions verified upgrade cycles, cloud migration rates, and price-volume assumptions, filling gaps left by public statistics and aligning variable forecasts with on-ground sentiment.

Desk Research

We consulted open data sets such as GLOBOCAN, WHO Cancer Observatory, and OECD Health Statistics to map cancer incidence, therapy adoption, and IT spending trends. Further context came from U.S. Medicare cost reports, Eurostat hospital ICT surveys, and trade association briefs (HIMSS, ASTRO). Company 10-Ks and selected press releases clarified installed OIS bases and average selling prices. Subscription inputs from D&B Hoovers and Dow Jones Factiva helped size vendor revenues. The sources listed are illustrative; many additional publications and databases informed data gathering and sense-checking.

Market-Sizing & Forecasting

A top-down incidence-to-demand model converts newly diagnosed cancer cases into potential OIS seat counts, adjusted for treatment center penetration and multi-facility connectivity. Results are checked against selective bottom-up roll-ups of vendor revenue disclosures and sampled license fees. Key variables include: (1) annual new cancer cases, (2) average number of active treatment plans per patient, (3) share of centers using integrated OIS, (4) cloud versus on-premise pricing differentials, and (5) replacement cycle length. Multivariate regression links these drivers to historic revenue to project 2025-2030 trends, with scenario analysis capturing policy or technology shocks.

Data Validation & Update Cycle

Outputs pass variance tests versus independent cancer care spend; then senior analysts review anomalies before sign-off. The model is refreshed each year, and ad-hoc updates are triggered by substantial regulatory or M&A events, ensuring clients receive the latest calibrated view.

Why Mordor's Oncology Information System Baseline Earns Trust

Published market values often diverge because each firm chooses different scope boundaries, pricing ladders, and refresh cadences.

Key gap drivers include inclusion of broader health-IT modules, use of unverified vendor list pricing, and less frequent updates that miss rapid cloud adoption shifts. Mordor Intelligence narrows scope to oncology-dedicated platforms, applies mixed ASPs drawn from confirmed deals, and revisits variables annually, which collectively anchor a balanced baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.22 B (2025) | Mordor Intelligence | - |

| USD 3.17 B (2025) | Global Consultancy A | Uses fixed currency of prior year and limited primary validation |

| USD 5.84 B (2025) | Industry Association B | Bundles generic hospital IT and estimates vendor revenue without incidence linkage |

In summary, our disciplined variable selection, annual refresh rhythm, and cross-checks against clinician input make Mordor's numbers a dependable starting point for strategic and investment decisions.

Key Questions Answered in the Report

What is the current size of the oncology information system market?

The oncology information system market size is USD 3.48 billion in 2026 and is projected to reach USD 5.17 billion by 2031 at an 8.21% CAGR.

Who are the key players in Oncology Information System Market?

Oracle Corporation, Siemens Healthineers AG (Varian Medical Systems), Elekta AB, Koninklijke Philips N.V. and McKesson Corporation are the major companies operating in the Oncology Information System Market.

Why is radiation oncology growing faster than other applications?

Proton therapy expansion and AI-driven adaptive planning demand sophisticated data integration, propelling radiation oncology at a 8.83% CAGR.

Which region has the biggest share in Oncology Information System Market?

In 2025, the North America accounts for the largest market share in Oncology Information System Market.

Which segment holds the largest oncology information system market share?

Services account for 50.32% of revenue in 2025 due to the complexity of implementation and the need for continuous support.

Page last updated on: