Styrene Ethylene Butylene Styrene (SEBS) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

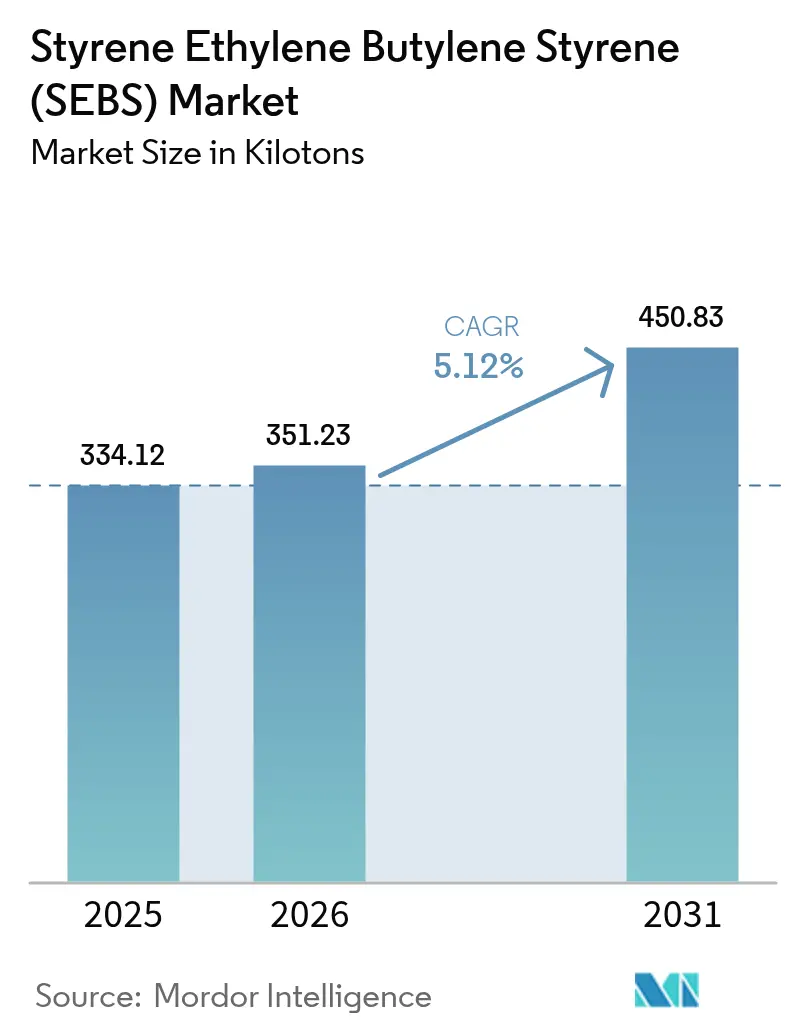

| Market Volume (2026) | 351.23 kilotons |

| Market Volume (2031) | 450.83 kilotons |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Styrene Ethylene Butylene Styrene (SEBS) Market Analysis by Mordor Intelligence

The Styrene Ethylene Butylene Styrene Market size is expected to grow from 334.12 kilotons in 2025 to 351.23 kilotons in 2026 and is forecast to reach 450.83 kilotons by 2031 at a 5.12% CAGR over 2026-2031. Low-VOC hot-melt adhesives are gaining traction, electrified vehicles are reducing weight, and bio-attributed feedstocks are being balanced - all of which are driving volume growth in the adhesives, automotive, and infrastructure sectors. In China and South Korea, producers co-located with steam crackers are effectively navigating price fluctuations from recent years by securing their feedstock. In Europe, converters are striving to meet design-for-recycling standards, driven by European Union mandates on packaging and extended producer responsibility. This has resulted in a surge in demand for recycling-ready SEBS. Vertically integrated suppliers certified by ISCC PLUS are at an advantage, as they can benefit from Scope 3 carbon reductions while maintaining throughput and mechanical performance. Consequently, the focus is shifting toward specialty grades for medical devices and e-mobility, which command a premium over standard dispersion powders, highlighting their profitability potential.

Key Report Takeaways

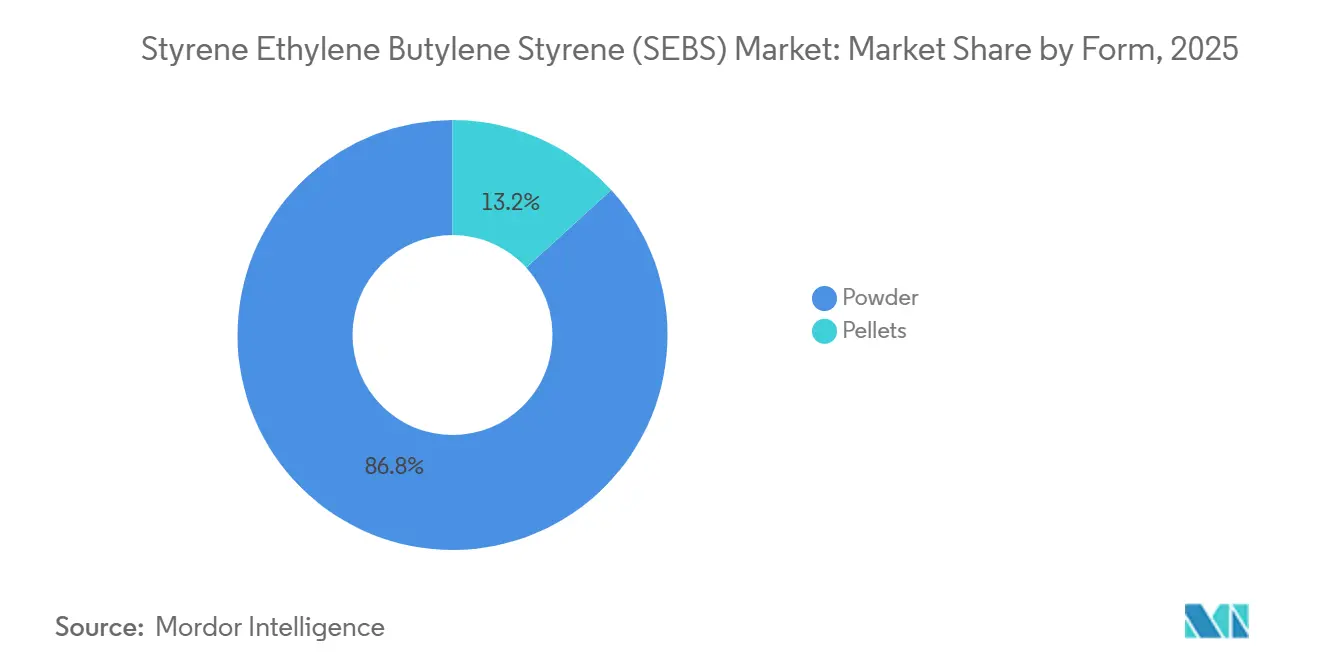

- By form, powder accounted for 86.78% of the 2025 volume, and powder is also expected to advance at a 5.31% CAGR in 2026-2031.

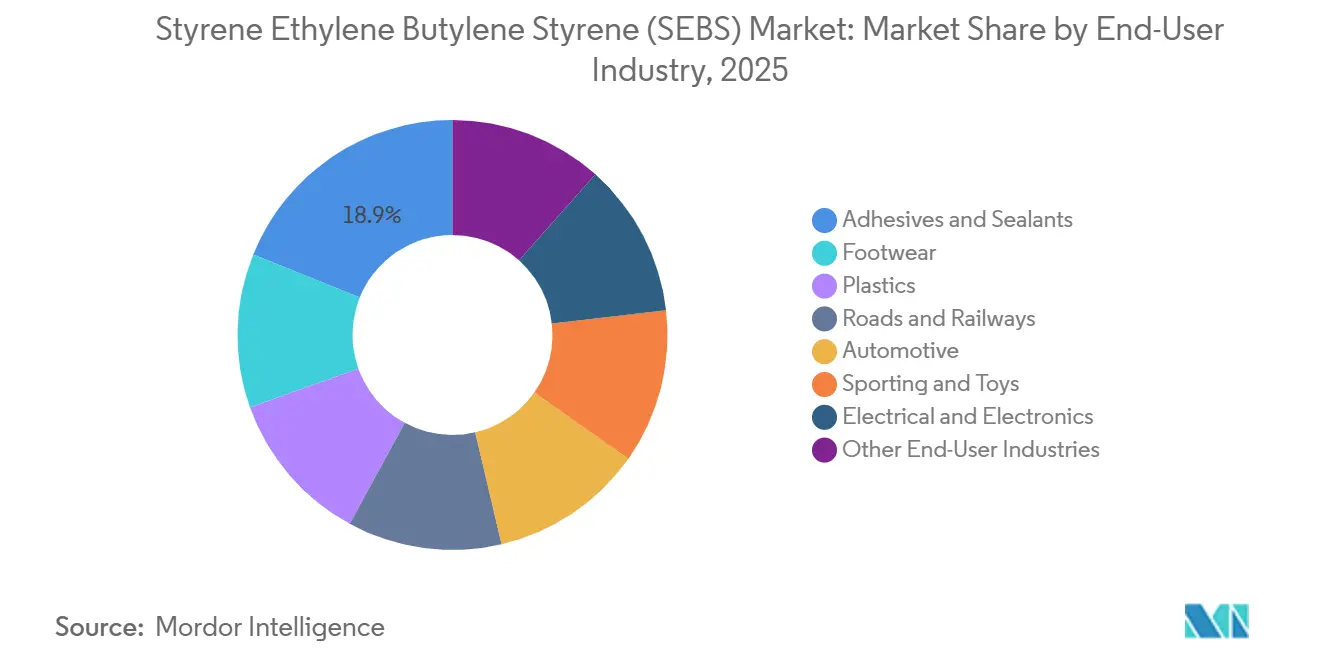

- By end-user industry, adhesives and sealants led with an 18.89% share of the 2025 styrene ethylene butylene styrene (SEBS) market, whereas plastics modification posted the fastest 6.32% CAGR to 2031.

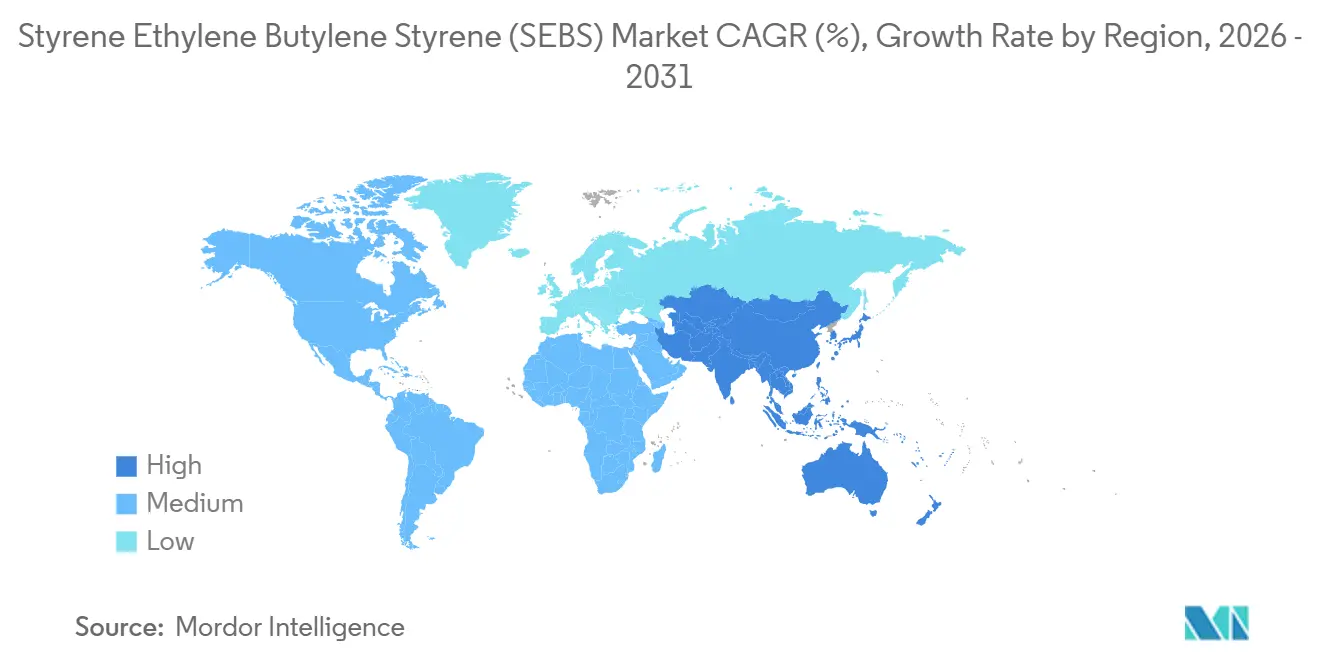

- The Asia-Pacific region captured 56.72% of global demand in 2025; it also recorded the highest 5.99% CAGR over the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Styrene Ethylene Butylene Styrene (SEBS) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for low-VOC hot-melt adhesives in Asia-Pacific | +1.2% | Asia-Pacific core, spillover to North America | Medium term (2-4 years) |

| Lightweighting imperatives in e-mobility components | +1.5% | Global, led by China, EU, United States | Long term (≥ 4 years) |

| Post-petrochemical feedstock integration at steam-cracker complexes | +0.9% | Asia-Pacific, Middle East | Medium term (2-4 years) |

| Commercialization of bio-based SEBS via mass-balance routes | +0.8% | Europe, North America, Japan | Long term (≥ 4 years) |

| Recycling-ready SEBS grades aligned with circular-polymer schemes | +0.7% | Europe core, expanding to North America and ASEAN | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Low-VOC Hot-Melt Adhesives in Asia-Pacific

Effective since 2024, China's GB 38507-2020 standard imposes stringent limits on VOC content. This regulation is driving adhesive manufacturers toward SEBS-based hot-melts, which cure without solvents and are more energy-efficient[1]China Ministry of Ecology and Environment, “GB 38507-2020 VOC Limits,” mee.gov.cn. Lintec's planned expansion in Malaysia underscores this regional pivot. SEBS adhesives are gaining traction in automotive interiors and electronics, where concerns about odor and fogging take precedence. Clariant's Licocene waxes, when paired with SEBS, extend open time, enabling brand owners to accelerate packaging-line speeds while meeting retailer sustainability standards[2]Clariant International, “Licocene Polyethylene Waxes Bulletin,” clariant.com. The rising demand in the Asia-Pacific region is further fueled by e-commerce logistics centers emphasizing quick-setting box seals for enhanced throughput, resulting in a yearly uptick in consumption. With Vietnam and Indonesia boosting their adhesive tape exports, the region's heightened consumption of hot-melts is propelling the Styrene-Ethylene-Butylene-Styrene market's growth, a trend set to persist during the forecast period of 2026–2031.

Lightweighting Imperatives in E-Mobility Components

Electric-vehicle manufacturers are aggressively pursuing weight reductions to enhance driving range, all while adhering to the EU's fleet target of 95 g CO₂/km. SEBS-modified polypropylene offers a significant weight reduction compared to talc-filled grades, while maintaining impact strength at -40 °C. Although Cooper Standard’s FlexiCore TPV highlights the competitive landscape, SEBS provides a processing-cycle advantage, particularly in thin-wall battery covers. With the global BEV production projected to grow steadily during the forecast period of 2026–2031, the demand for SEBS in molded parts is expected to outpace the market's growth. Tier-one suppliers are gravitating towards SEBS, as its color-matching and low-gloss properties eliminate the need for paint steps, resulting in reduced assembly costs. Consequently, automotive grades command a premium, yet they continue to attract interest from OEMs prioritizing total cost of ownership.

Post-Petrochemical Feedstock Integration at Steam-Cracker Complexes

South Korea's Shaheen complex established a direct link between a styrene monomer line and the downstream SEBS. This strategic integration acts as a buffer against spot-styrene price fluctuations. Chinese companies are adopting a similar approach. For example, Fujian Xiangjiang has established an SBS unit, designed for hydrogenation to produce SEBS, offering enhanced flexibility in managing the product slate. Such integrated operations not only reduce feedstock expenses but also expedite deliveries to adhesive clients. This rapid turnaround is critical, particularly when supply contracts require quarterly price stability. Meanwhile, cracker projects in the Middle-East are targeting exports of powder-grade SEBS to the Asia-Pacific region, leveraging their favorable ethane access. These strategic moves could pressure margins for Western players lacking integration, unless they adopt a similar backward integration strategy.

Commercialization of Bio-Based SEBS via Mass-Balance Routes

Bio-ethanol-derived feedstocks can now be allocated into SEBS through a book-and-claim system under ISCC PLUS certification. This system enables converters to claim renewable content without requiring reformulation. In 2023, Dynasol's certification not only reduced embodied carbon but also resulted in brand-owner premiums. Medical tubing and premium footwear have shown the strongest adoption, as either regulatory approvals or brand strategies justify the higher resin costs. However, enzyme deactivation has prevented bio-isoprene yields from reaching commercial viability, limiting fully renewable SEBS to pilot stages. Until yields exceed the 100 g/L threshold, the mass-balance approach will remain central to the sustainability narrative in the Styrene Ethylene Butylene Styrene market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-competitive TPU/TPV blends gaining footwear share | -0.6% | Global, concentrated in Asia-Pacific footwear hubs | Short term (≤ 2 years) |

| Carbon-border-tax risk for Asia-made SEBS into EU/United States | -0.5% | Asia-Pacific exports to Europe and North America | Medium term (2-4 years) |

| Restricted supply of bio-isoprene feedstock | -0.3% | Global, most acute in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-Competitive TPU/TPV Blends Gaining Footwear Share

BASF's Elastollan TPU, priced lower per kilogram than premium SEBS, offers abrasion resistance that is favored by athletic shoe brands. This pricing strategy exerts pressure on SEBS, which accounted for a significant portion of the projected global demand. In recent years, as consumer spending in North America and Europe declined, contract manufacturers in Vietnam and Indonesia transitioned midsoles to TPU. Although SEBS retains a foothold in high-rebound comfort insoles, where a low compression set is crucial, this niche is insufficient to offset its losses in the mass market. FlexiCore TPV intensifies the competition by achieving comparable Shore A hardness and improved hydrolysis resistance. Consequently, footwear is emerging as a low-growth segment within the broader Styrene Ethylene Butylene Styrene market outlook for the forecast period 2026–2031.

Carbon-Border-Tax Risk for Asia-Made SEBS into EU and United States

In its 2025 review, the EU indicated the possible inclusion of polymers in the CBAM as early as 2028. This action could lead to heightened costs for Chinese SEBS, which records CO₂ emissions per ton of styrene that surpass the EU's benchmark. Asian producers are actively seeking renewable-electricity certificates and ISCC PLUS accreditation. However, the substantial cost of upgrading each site is placing a strain on their financial resources. Concurrently, U.S. legislators are considering a similar carbon tariff, indicating a synchronized policy direction across the Pacific. In Europe, there is a growing demand from buyers for disclosures on embedded carbon. This trend is nudging procurement choices toward regional or Middle-East suppliers, who are recognized for their reduced carbon footprints. Consequently, without a marked acceleration in decarbonization initiatives, competitively priced Chinese capacities may be sidelined from the lucrative high-margin accounts in the EU's packaging and medical sectors during the forecast period of 2026–2031.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Retains Dominance Across Adhesive Compounding

In 2025, powders commanded a dominant 86.78% share of the Styrene Ethylene Butylene Styrene market. Forecasts indicate a growth trajectory of 5.31% CAGR for powders through the 2026–2031 period. This growth is largely attributed to hot-melt formulators in the Asia-Pacific region, who prefer sub-200 µm particle sizes, leading to significantly reduced mix times. The remaining market share is occupied by pellet grades, which play a pivotal role in injection-molded fascia, where consistent melt flow is paramount.

In a bid to capture larger volumes, powder suppliers are refining their processes. They are debottlenecking micronizers and incorporating maleic-anhydride functionalities, enhancing adhesion with polar tackifiers. This trend is especially pronounced in Europe, where recyclability regulations have tightened. While the demand for pellets is increasing at a more measured pace, the value per ton for pellets remains significantly elevated. This premium is attributed to automotive molders' emphasis on stringent lot-traceability and gel-content controls. Given these dynamics, powder consumption is poised to surpass that of pellets in the near future. On the other hand, pellets are relying on demand from e-mobility interiors and 3D-printing filaments to fuel their growth.

By End-User Industry: Plastics Modification Outpaces Adhesives Growth

In 2025, Adhesives and Sealants dominated the Styrene Ethylene Butylene Styrene market, capturing an 18.89% share. This segment thrived under Asia-Pacific's stringent low-VOC regulations but faced margin pressures from water-based alternatives in North American packaging. On the other hand, Plastics Modification, starting from a smaller base, is projected to expand at a 6.32% CAGR during the forecast period of 2026–2031. This growth is driven by a significant increase in electric-vehicle platforms, which is creating demand for SEBS-modified polypropylene that adheres to -40°C impact standards.

Footwear is losing market share to TPU substitutes. Roads and Railways are expected to benefit from India's stimulus, which mandates polymer-modified bitumen for national highways. The Electrical and Electronics sector maintains a consistent demand for flexible cable jacketing, with an emphasis on low fogging. In summary, while the footwear segment is softening, other non-automotive applications of engineered plastics are strengthening the demand profile for the Styrene Ethylene Butylene Styrene market.

Geography Analysis

In 2025, the Asia-Pacific region commanded a dominant 56.72% share of the global volume and is projected to expand at a CAGR of 5.99% during the forecast period of 2026–2031. This growth was largely fueled by China's impressive installed capacity and India's burgeoning output in passenger vehicles. In the first quarter of 2024, China produced significant volumes. However, a looming oversupply risk persisted, with new market entrants outpacing domestic consumption. India's stringent crash-test norms, mandating tougher bumpers, drove additional annual demand for SEBS. Meanwhile, Japan and South Korea shifted their focus to bio-attributed credits through ISCC PLUS, leveraging the integrated feedstock economics offered by Shaheen.

North America, holding a notable share of the global volume, experienced tightening regional balances. This was driven by DL Chemical's expansion in Belpre, Ohio, and Kraton's debottlenecking efforts, which coincided with a recovery in adhesive demand. Europe's share grew at a sluggish pace. Converters in the region awaited further clarity regarding the CBAM. However, there was a silver lining: the recycling-compatible Calprene H6180S gained traction in Germany's flexible packaging sector. The looming threat of border carbon levies prompted Turkish and North African entities to conduct feasibility studies for new SEBS lines tailored for EU clientele.

Both South America and the combined regions of the Middle-East and Africa contributed a small share to the global volume. In Brazil, a resurgence in the automotive sector drove up demand for impact modifiers. Concurrently, Saudi Arabia, in its quest for downstream diversification, set its sights on exporting powder to India. Dynasol's Altamira facility in Mexico catered to both NAFTA and Latin American markets. However, the fragmented nature of demand posed challenges, limiting potential scale economies.

Competitive Landscape

The Styrene Ethylene Butylene Styrene (SEBS) market is moderately consolidated. Recreus, a niche innovator, has partnered with Dynasol to enhance the application scope of SEBS filaments in 3D printing. European producers, lacking the capital for decarbonization retrofits, face potential mergers and acquisitions prospects due to their unintegrated status. The strategic focus in the Styrene Ethylene Butylene Styrene market is on achieving mass-balance certification, securing automotive-grade qualifications, and ensuring drop-in recyclability - all essential for a premium market position.

Styrene Ethylene Butylene Styrene (SEBS) Industry Leaders

China Petrochemical Corporation

Kraton Corporation

LCY Group

TSRC

KURARAY CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Kraton (DL Chemical) instituted a global USD 330 per ton price rise for styrenic block copolymers (including styrene ethylene butylene styrene), citing raw-material cost inflation and tightening North American and European balances.

- October 2025: PetroChina Guangxi Petrochemical’s ethylene project was completed and commissioned at the Qinzhou Port in Guangxi. The project includes a 1.2 million-tonne-per-year diesel adsorption separation unit and features PetroChina's first self-developed 80,000-tonne-per-year styrene-butadiene-styrene (SBS). This project can boost the SEBS production in China.

Global Styrene Ethylene Butylene Styrene (SEBS) Market Report Scope

Styrene ethylene butylene styrene (SEBS) is an important thermoplastic soft elastomer (TPE) that behaves like rubber without undergoing vulcanization. SEBS is a high-temperature, high-resistance hydrogenated product. It has high mechanical strength and high safety. It is stable in color, odorless, and free of impurities. SEBS is often mixed with other oils, such as paraffin, to increase processing efficiency.

The market is segmented by form, end-user industry, and geography. By form, the market is segmented into pellets and powder. By end-user industry, the market is segmented into footwear, adhesives and sealants, plastics, roads and railways, automotive, sporting goods and toys, electrical and electronics, and other industries. The report also covers the market size and forecasts for the market in 16 countries across major regions. For each segment, the market sizing and forecasts are done based on volume (Tons).

| Pellets |

| Powder |

| Footwear |

| Adhesives and Sealants |

| Plastics |

| Roads and Railways |

| Automotive |

| Sporting and Toys |

| Electrical and Electronics |

| Other End-User Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Form | Pellets | |

| Powder | ||

| By End-User Industry | Footwear | |

| Adhesives and Sealants | ||

| Plastics | ||

| Roads and Railways | ||

| Automotive | ||

| Sporting and Toys | ||

| Electrical and Electronics | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected volume for global Styrene Ethylene Butylene Styrene demand by 2031?

The Styrene Ethylene Butylene Styrene Market size is expected to grow from 334.12 kilotons in 2025 to 351.23 kilotons in 2026 and is forecast to reach 450.83 kilotons by 2031 at a 5.12% CAGR over 2026-2031.

Which form of SEBS dominates current consumption?

Powder form leads, holding 86.78% of 2025 volume, thanks to its rapid dispersion in hot-melt adhesives.

Why are automotive OEMs shifting toward SEBS-modified polypropylene?

SEBS impact modifiers deliver a weight reduction versus talc-filled grades while passing minus-40 °C impact tests demanded by electric-vehicle platforms.

How does the EU packaging regulation influence SEBS grades?

Regulation 2025/40 enforces recyclability and recycled content, spurring uptake of recycling-ready SEBS like Dynasol’s Calprene H6180S.

Which regions are likely to benefit from CBAM-driven supply realignment?

Middle-East and North African projects with low-carbon feedstocks could gain EU share if Asian exports face carbon-border levies.

Page last updated on: